Academic Profile

Statistics

Similar Authors

Papers on arXiv

Spectral precision matrix, the inverse of a spectral density matrix, is an object of central interest in frequency-domain analysis of multivariate time series. Estimation of spectral precision matri...

Sparse regression has emerged as a popular technique for learning dynamical systems from temporal data, beginning with the SINDy (Sparse Identification of Nonlinear Dynamics) framework proposed by a...

In this paper we propose univariate volatility models for irregularly spaced financial time series by modifying the regularly spaced stochastic volatility models. We also extend this approach to pro...

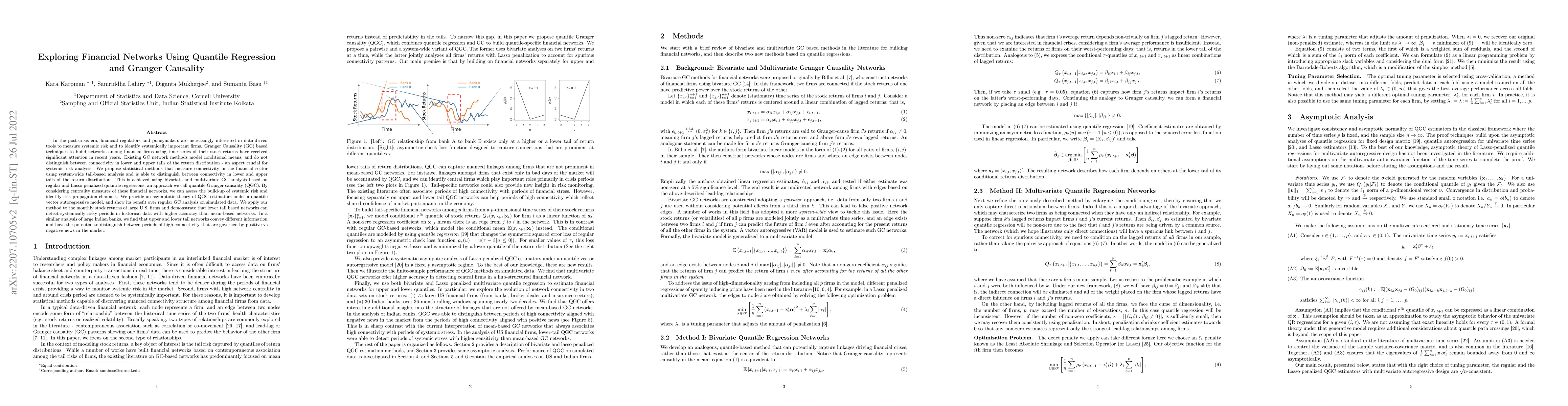

Financial networks are typically estimated by applying standard time series analyses to price-based economic variables collected at low-frequency (e.g., daily or monthly stock returns or realized vo...

In the post-crisis era, financial regulators and policymakers are increasingly interested in data-driven tools to measure systemic risk and to identify systemically important firms. Granger Causalit...

In this paper we describe fast Bayesian statistical analysis of vector positive-valued time series, with application to interesting financial data streams. We discuss a flexible level correlated mod...

Time-course gene expression datasets provide insight into the dynamics of complex biological processes, such as immune response and organ development. It is of interest to identify genes with simila...

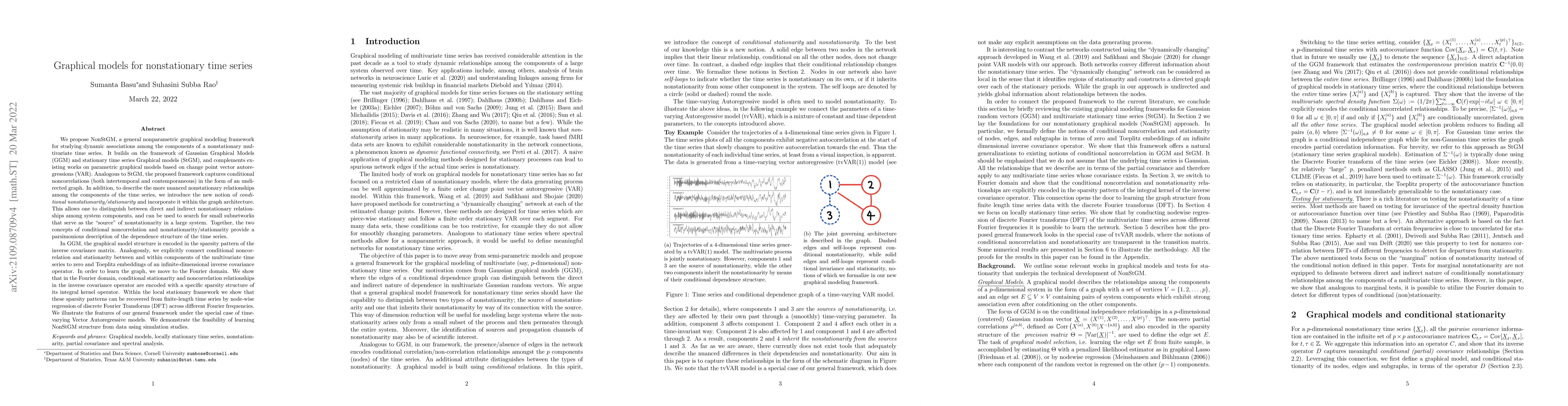

We propose NonStGM, a general nonparametric graphical modeling framework for studying dynamic associations among the components of a nonstationary multivariate time series. It builds on the framewor...

High-dimensional time series datasets are becoming increasingly common in many areas of biological and social sciences. Some important applications include gene regulatory network reconstruction usi...

Random forest (RF) is one of the most popular methods for estimating regression functions. The local nature of the RF algorithm, based on intra-node means and variances, is ideal when errors are i.i...

Tree ensembles such as Random Forests have achieved impressive empirical success across a wide variety of applications. To understand how these models make predictions, people routinely turn to feat...

Standard ChIP-seq peak calling pipelines seek to differentiate biochemically reproducible signals of individual genomic elements from background noise. However, reproducibility alone does not imply ...

The paper proposes a new algorithm for the high-dimensional financial data -- the Groupwise Interpretable Basis Selection (GIBS) algorithm, to estimate a new Adaptive Multi-Factor (AMF) asset pricin...

Genomics has revolutionized biology, enabling the interrogation of whole transcriptomes, genome-wide binding sites for proteins, and many other molecular processes. However, individual genomic assay...

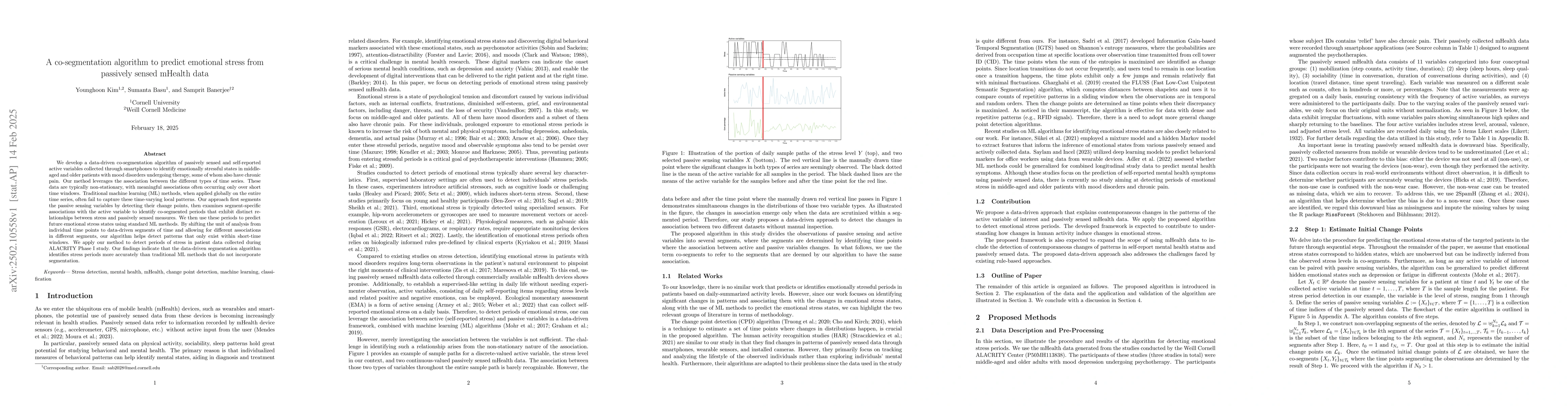

We develop a data-driven co-segmentation algorithm of passively sensed and self-reported active variables collected through smartphones to identify emotionally stressful states in middle-aged and olde...

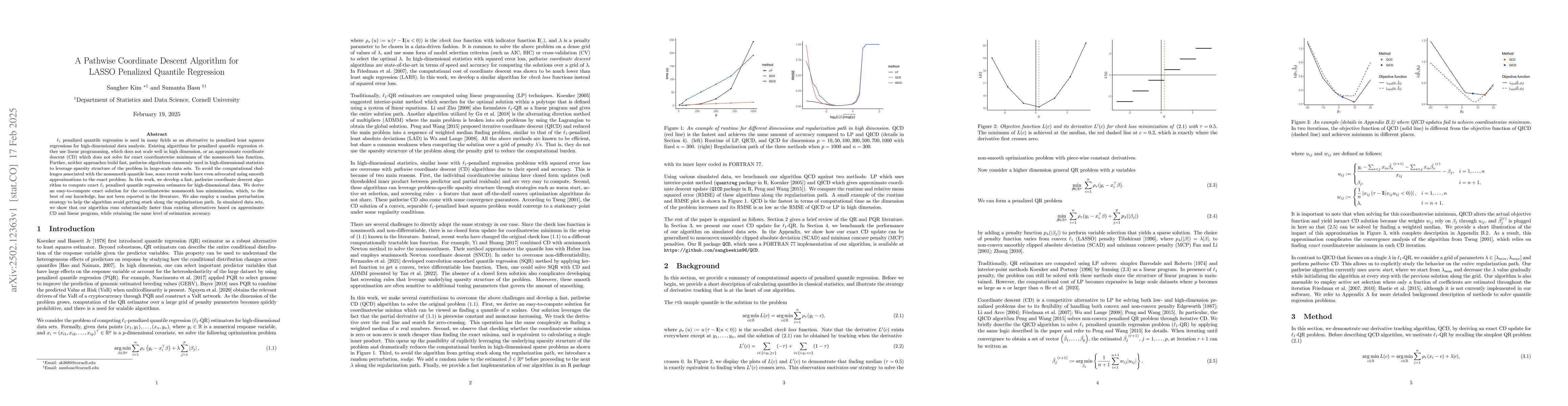

$\ell_1$ penalized quantile regression is used in many fields as an alternative to penalized least squares regressions for high-dimensional data analysis. Existing algorithms for penalized quantile re...

Clinical investigators are increasingly interested in discovering computational biomarkers from short-term longitudinal omics data sets. This work focuses on Bayesian regression and variable selection...

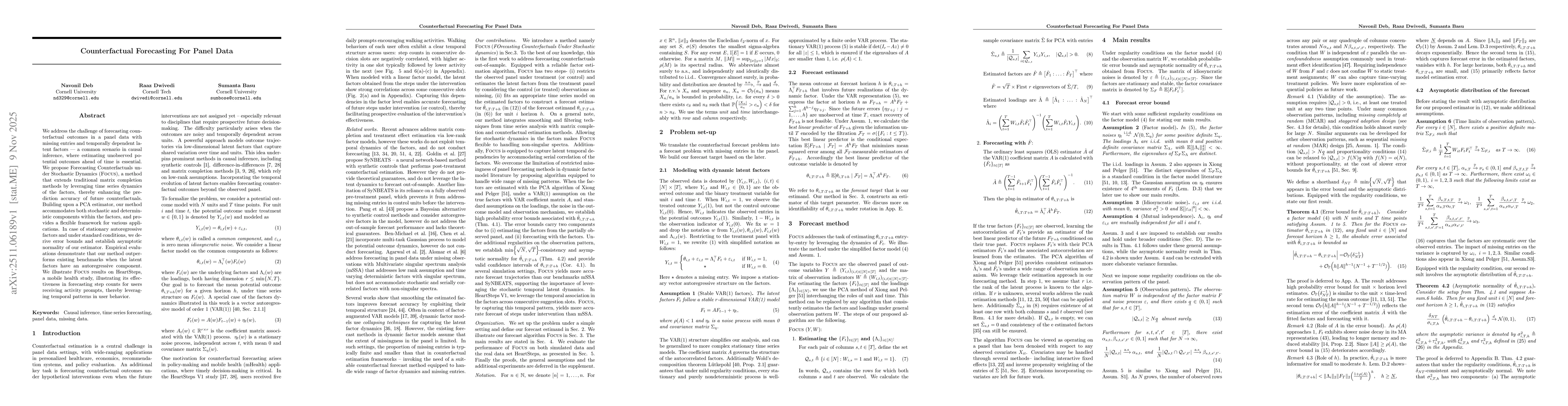

We develop an exact coordinate descent algorithm for high-dimensional regularized Huber regression. In contrast to composite gradient descent methods, our algorithm fully exploits the advantages of co...

We address the challenge of forecasting counterfactual outcomes in a panel data with missing entries and temporally dependent latent factors -- a common scenario in causal inference, where estimating ...

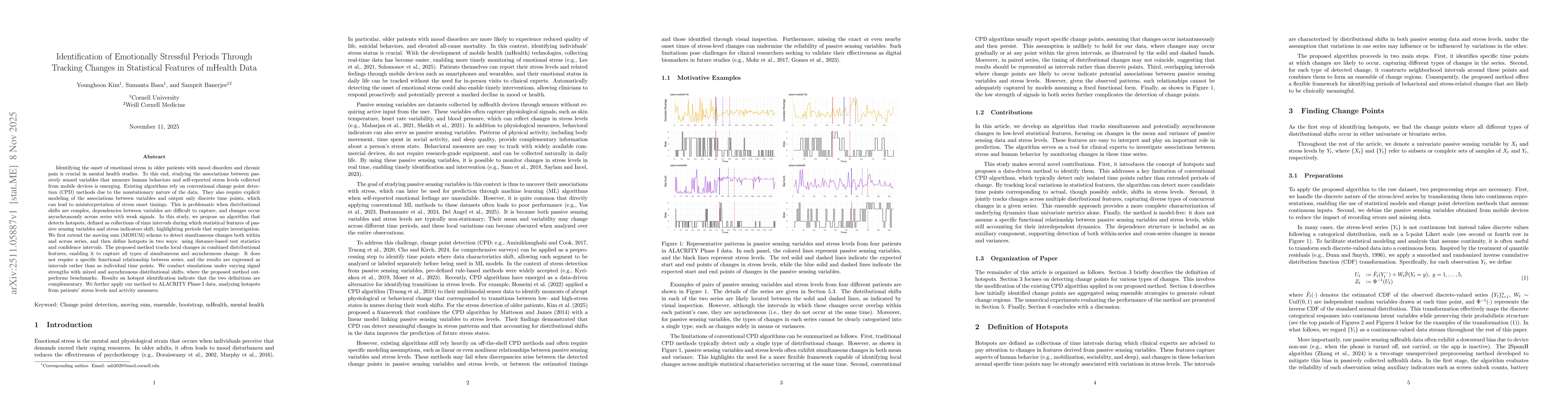

Identifying the onset of emotional stress in older patients with mood disorders and chronic pain is crucial in mental health studies. To this end, studying the associations between passively sensed va...

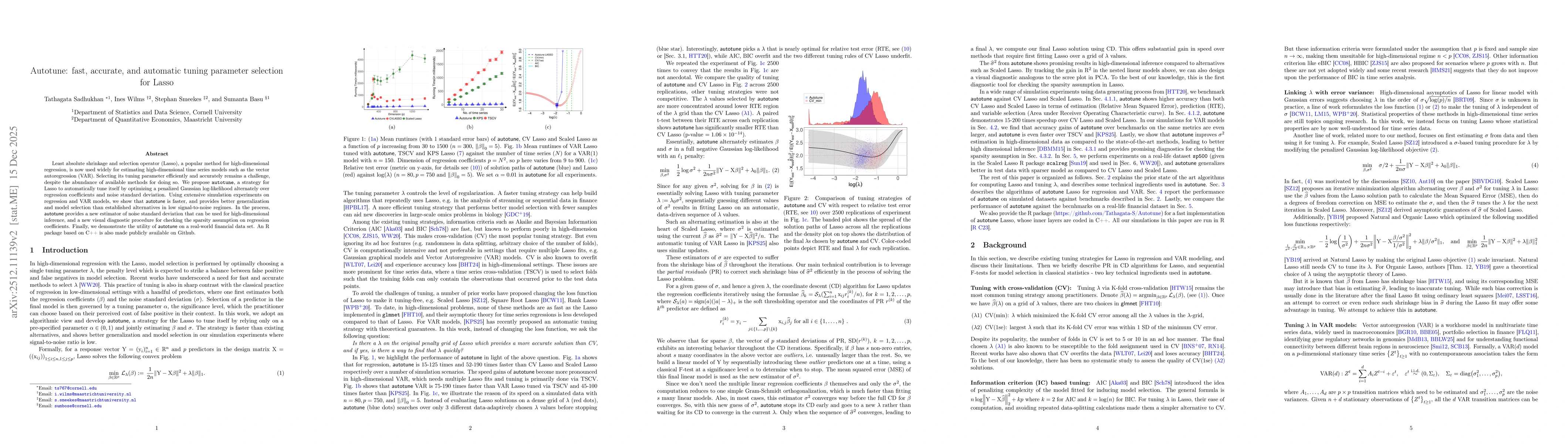

Least absolute shrinkage and selection operator (Lasso), a popular method for high-dimensional regression, is now used widely for estimating high-dimensional time series models such as the vector auto...

The graphical Lasso (GLASSO) is a widely used algorithm for learning high-dimensional undirected Gaussian graphical models (GGM). Given i.i.d. observations from a multivariate normal distribution, GLA...

Gaussian graphical models in the spectral domain offer a principled approach for recovering conditional dependence structures in stationary high-dimensional time series. Inference on the spectral prec...