Academic Profile

Statistics

Similar Authors

Papers on arXiv

We consider both $N$-player and mean-field games of optimal portfolio liquidation in which the players are not allowed to change the direction of trading. Players with an initially short position of...

We establish a probabilistic framework for analysing extended mean-field games with multi-dimensional singular controls and state-dependent jump dynamics and costs. Two key challenges arise when ana...

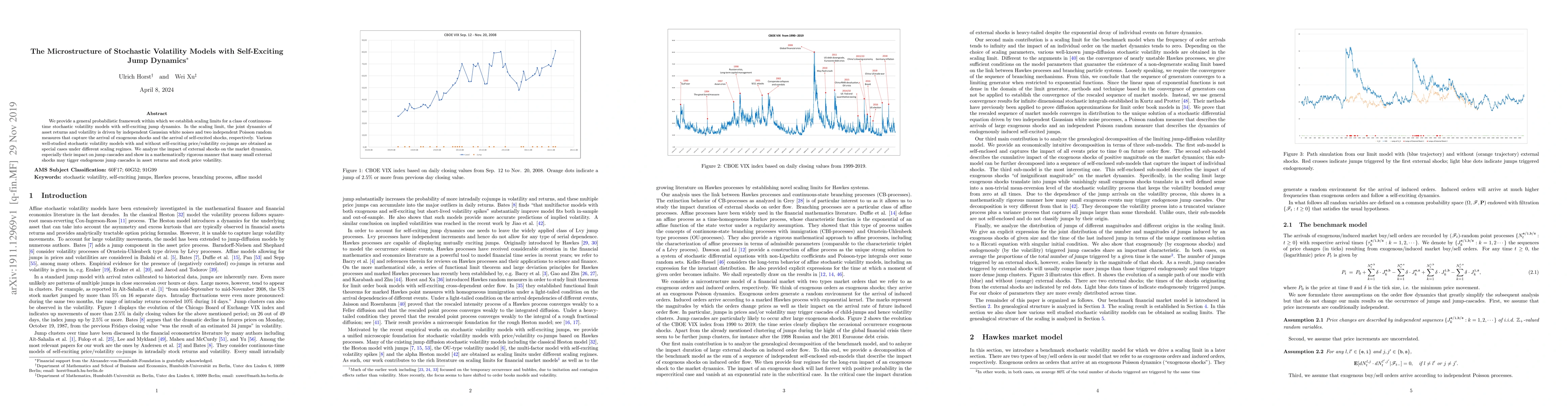

We prove that the long-run behavior of Hawkes processes is fully determined by the average number and the dispersion of child events. For subcritical processes we provide FLLNs and FCLTs under minim...

We establish the weak convergence of the intensity of a nearly-unstable Hawkes process with heavy-tailed kernel. Our result is used to derive a scaling limit for a financial market model where order...

This paper provides and extends second-order versions of several fundamental theorems on first-order regularly varying functions such as Karamata's theorem/representation and Tauberian's theorem. Ou...

We consider extended mean-field control problems with multi-dimensional singular controls. A key challenge when analysing singular controls are jump costs. When controls are one-dimensional, jump co...

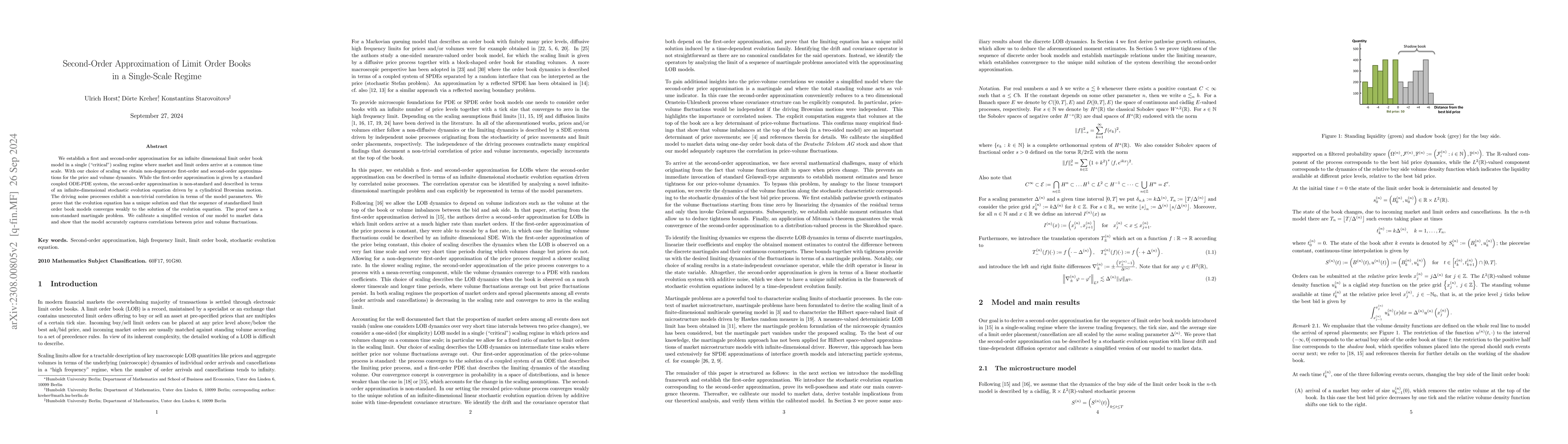

We establish a first and second-order approximation for an infinite dimensional limit order book model (LOB) in a single (''critical'') scaling regime where market and limit orders arrive at a commo...

We consider a novel class of portfolio liquidation games with market drop-out ("absorption"). More precisely, we consider mean-field and finite player liquidation games where a player drops out of t...

We consider a mean-field control problem with c\`adl\`ag semimartingale strategies arising in portfolio liquidation models with transient market impact and self-exciting order flow. We show that the...

We study a class of deterministic mean field games on finite and infinite time horizons arising in models of optimal exploitation of exhaustible resources. The main characteristic of our game is an ...

We consider an optimal liquidation problem with instantaneous price impact and stochastic resilience for small instantaneous impact factors. Within our modelling framework, the optimal portfolio pro...

We analyze novel portfolio liquidation games with self-exciting order flow. Both the N-player game and the mean-field game are considered. We assume that players' trading activities have an impact o...

We derive an explicit solution for deterministic market impact parameters in the Graewe and Horst (2017) portfolio liquidation model. The model allows to combine various forms of market impact, name...

We provide a general probabilistic framework within which we establish scaling limits for a class of continuous-time stochastic volatility models with self-exciting jump dynamics. In the scaling lim...

We consider a general framework of optimal mechanism design under adverse selection and ambiguity about the type distribution of agents. We prove the existence of optimal mechanisms under minimal as...

We study an optimal liquidation problem under the ambiguity with respect to price impact parameters. Our main results show that the value function and the optimal trading strategy can be characteriz...

This paper establishes a functional law of large numbers and a functional central limit theorem for marked Hawkes point measures and their corresponding shot noise processes. We prove that the norma...

We consider a mean field game (MFG) of optimal portfolio liquidation under asymmetric information. We prove that the solution to the MFG can be characterized in terms of a FBSDE with possibly singul...

We consider a microstructure foundation for rough volatility models driven by Poisson random measures. In our model the volatility is driven by self-exciting arrivals of market orders as well as self-...

We analyze a novel class of rough stochastic control problems that allows for a convenient approach to solving pathwise stochastic control problems with both non-anticipative and anticipative controls...

We study mean field portfolio games under Epstein-Zin preferences, which naturally encompass the classical time-additive power utility as a special case. In a general non-Markovian framework, we estab...

Motivated by mean-field games (MFG) with common noise on the one hand and pathwise stochastic control theory on the other, we formulate here a linear-quadratic (LQ) MFG with rough common noise, along ...

We establish an existence of equilibrium result for a class of non-Markovian mean-field games with unbounded control space in weak formulation. Our result is based on new existence and stability resul...

We establish a microstructural foundation of the rough Bergomi model. Specifically, we consider a sequence of order driven financial market models where orders to buy or sell an asset arrive according...

The well-posedness of multidimensional quadratic backward stochastic differential equations (qBSDEs) remains one of the central open problems in BSDE theory. Motivated by a mean-field utility maximiza...