Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper, we explore the portfolio allocation problem involving an uncertain covariance matrix. We calculate the expected value of the Constant Absolute Risk Aversion (CARA) utility function, m...

In this paper, we revisit the relationship between investors' utility functions and portfolio allocation rules. We derive portfolio allocation rules for asymmetric Laplace distributed $ALD(\mu,\sigm...

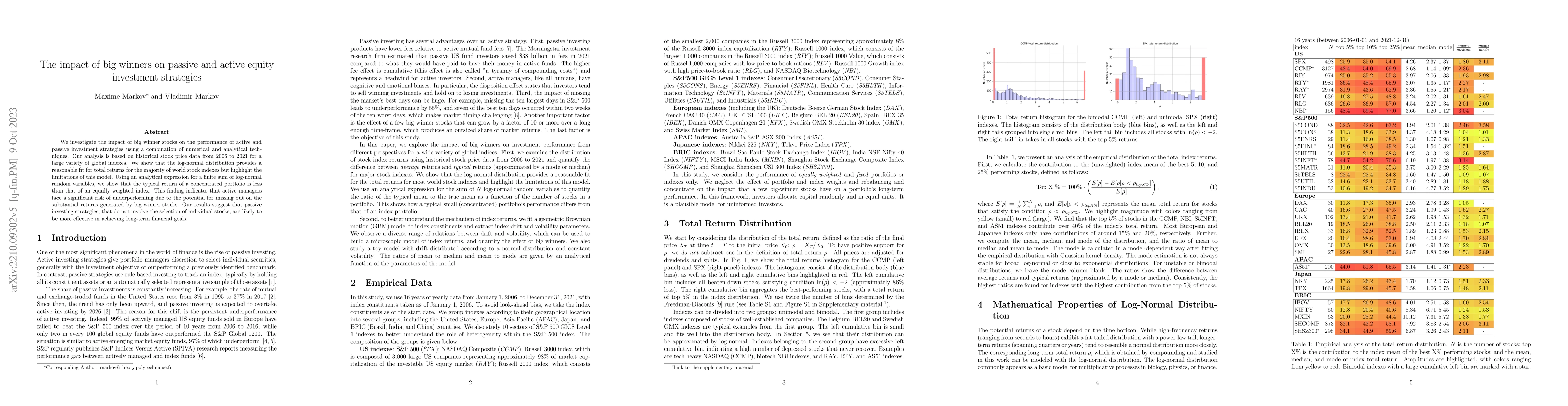

We investigate the impact of big winner stocks on the performance of active and passive investment strategies using a combination of numerical and analytical techniques. Our analysis is based on his...

We examine the problem of optimal portfolio allocation within the framework of utility theory. We apply exponential utility to derive the optimal diversification strategy and logarithmic utility to de...