Academic Profile

Statistics

Similar Authors

Papers on arXiv

Recently, diffusion probabilistic models have attracted attention in generative time series forecasting due to their remarkable capacity to generate high-fidelity samples. However, the effective uti...

In the wake of relentless digital transformation, data-driven solutions are emerging as powerful tools to address multifarious industrial tasks such as forecasting, anomaly detection, planning, and ...

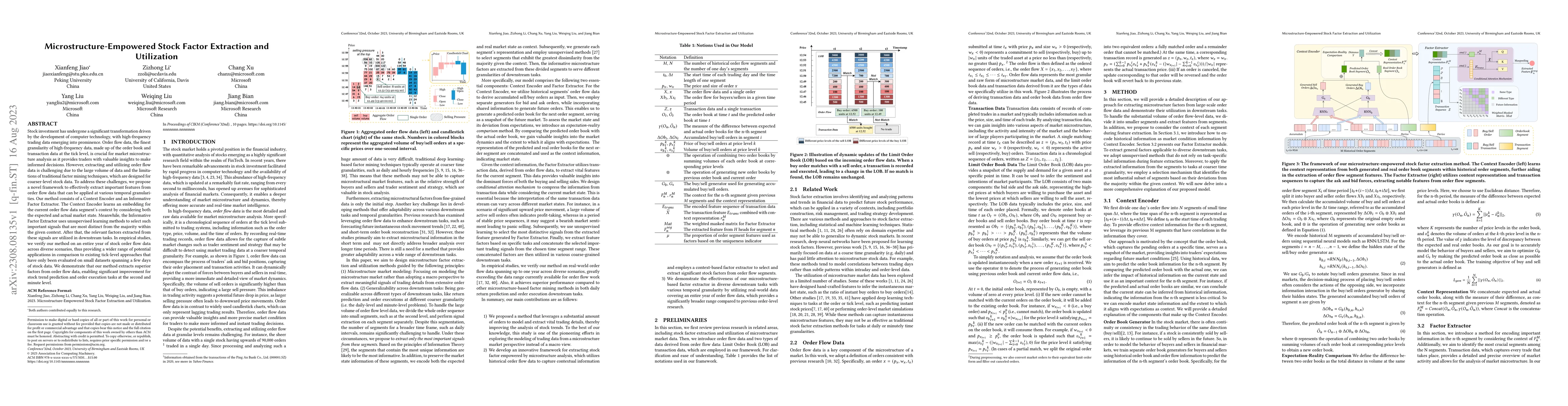

High-frequency quantitative investment is a crucial aspect of stock investment. Notably, order flow data plays a critical role as it provides the most detailed level of information among high-freque...

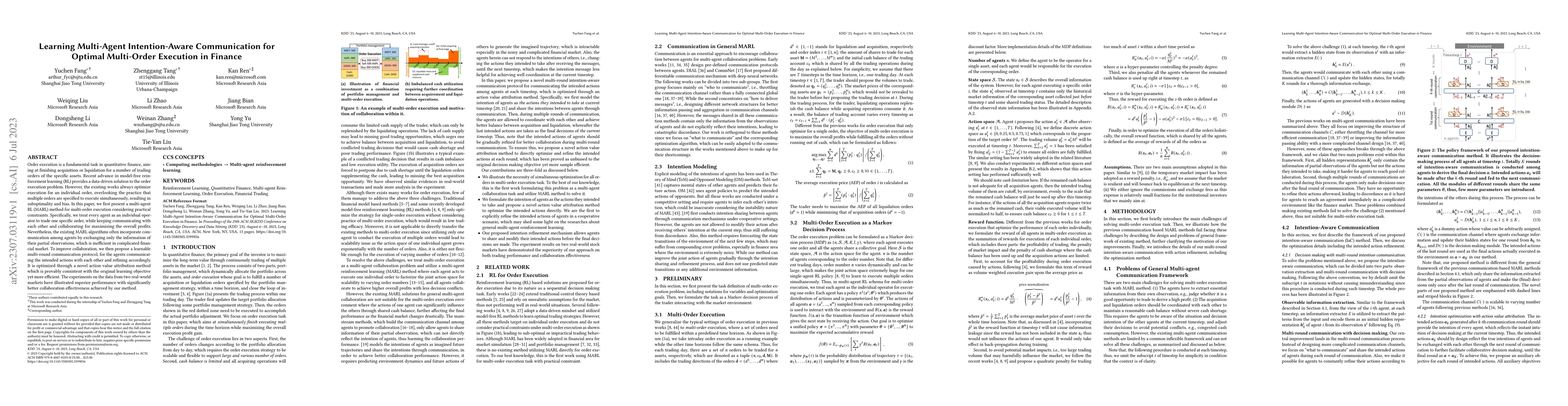

Order execution is a fundamental task in quantitative finance, aiming at finishing acquisition or liquidation for a number of trading orders of the specific assets. Recent advance in model-free rein...

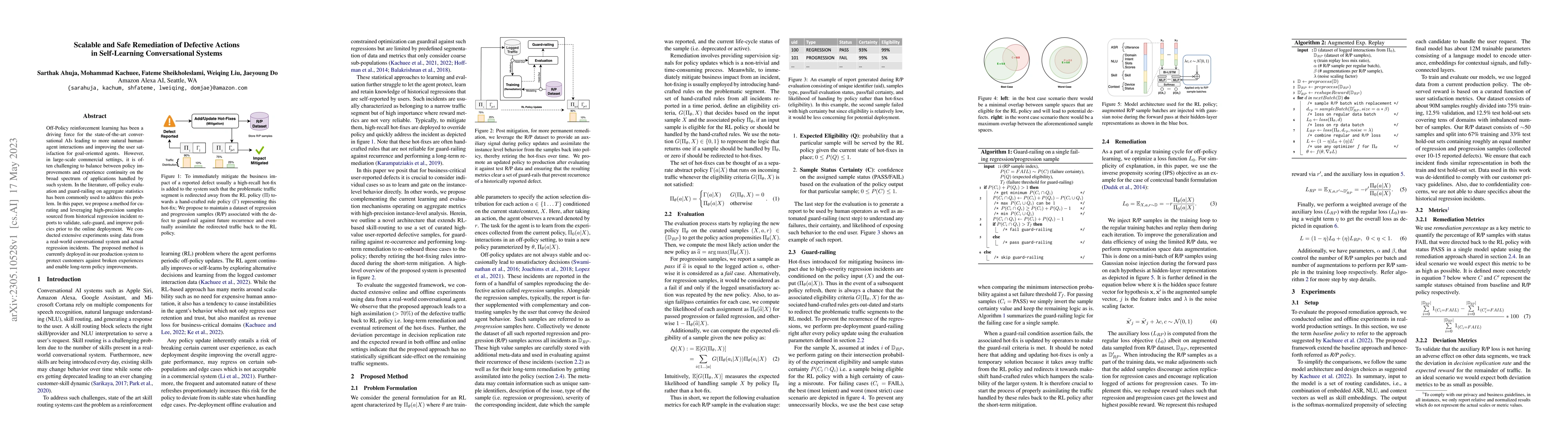

Off-Policy reinforcement learning has been a driving force for the state-of-the-art conversational AIs leading to more natural humanagent interactions and improving the user satisfaction for goal-or...

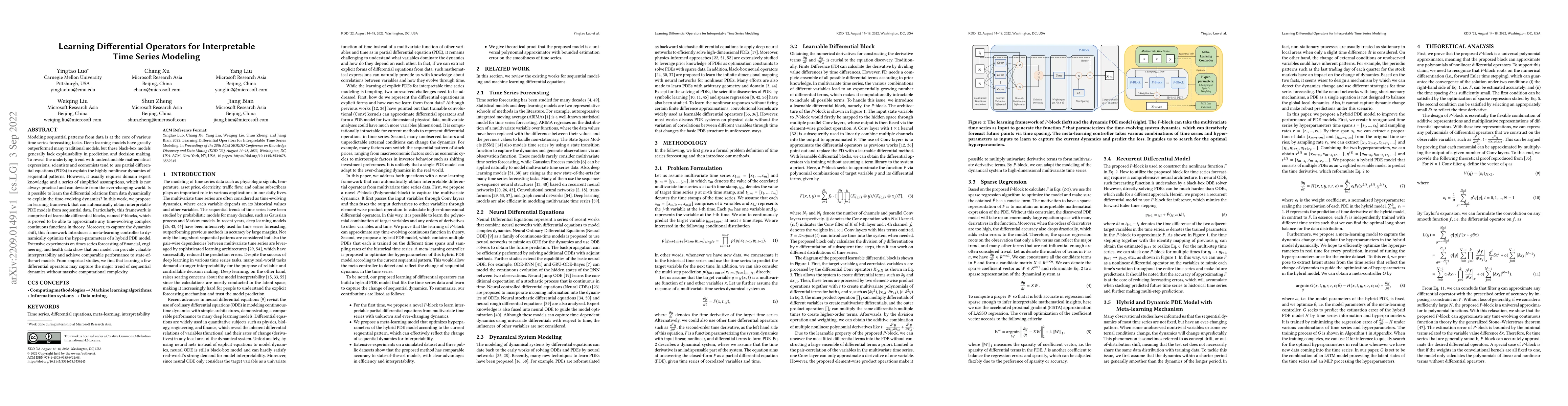

Modeling sequential patterns from data is at the core of various time series forecasting tasks. Deep learning models have greatly outperformed many traditional models, but these black-box models gen...

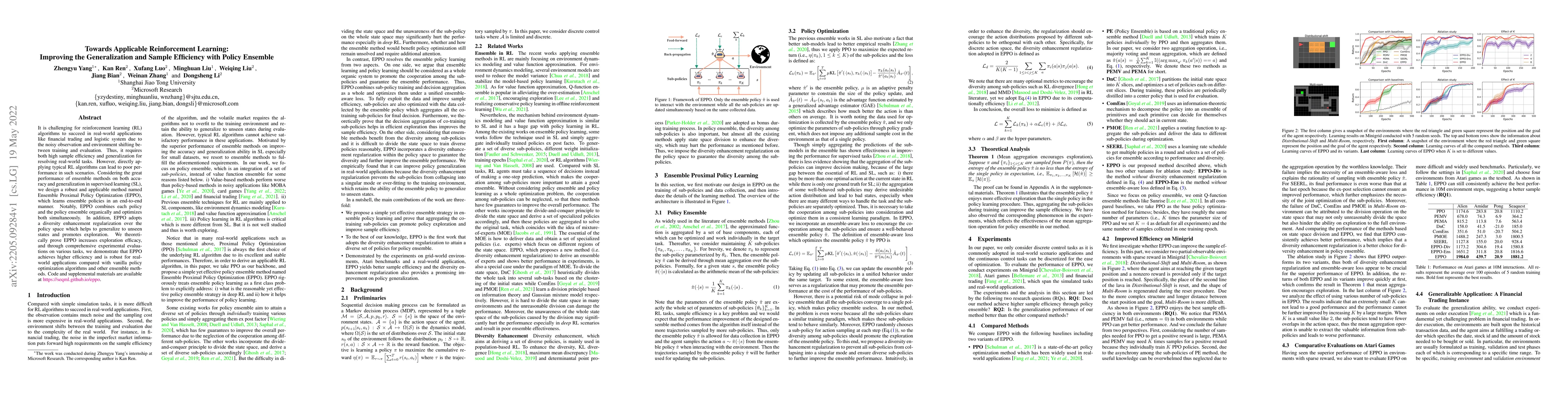

It is challenging for reinforcement learning (RL) algorithms to succeed in real-world applications like financial trading and logistic system due to the noisy observation and environment shifting be...

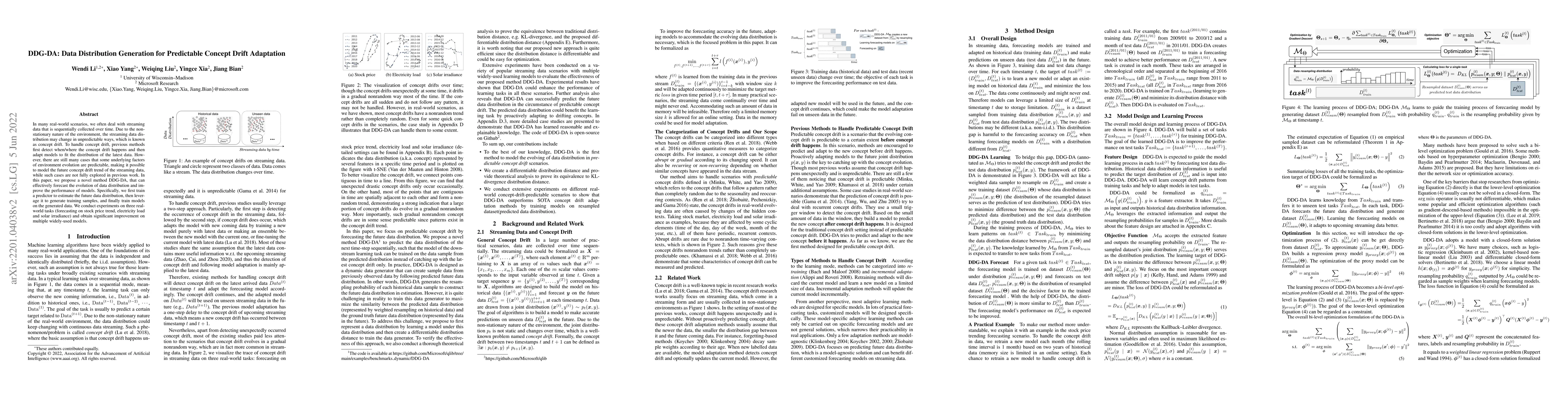

In many real-world scenarios, we often deal with streaming data that is sequentially collected over time. Due to the non-stationary nature of the environment, the streaming data distribution may cha...

Many real-world graphs (networks) are heterogeneous with different types of nodes and edges. Heterogeneous graph embedding, aiming at learning the low-dimensional node representations of a heterogen...

Learning the embeddings of knowledge graphs (KG) is vital in artificial intelligence, and can benefit various downstream applications, such as recommendation and question answering. In recent years,...

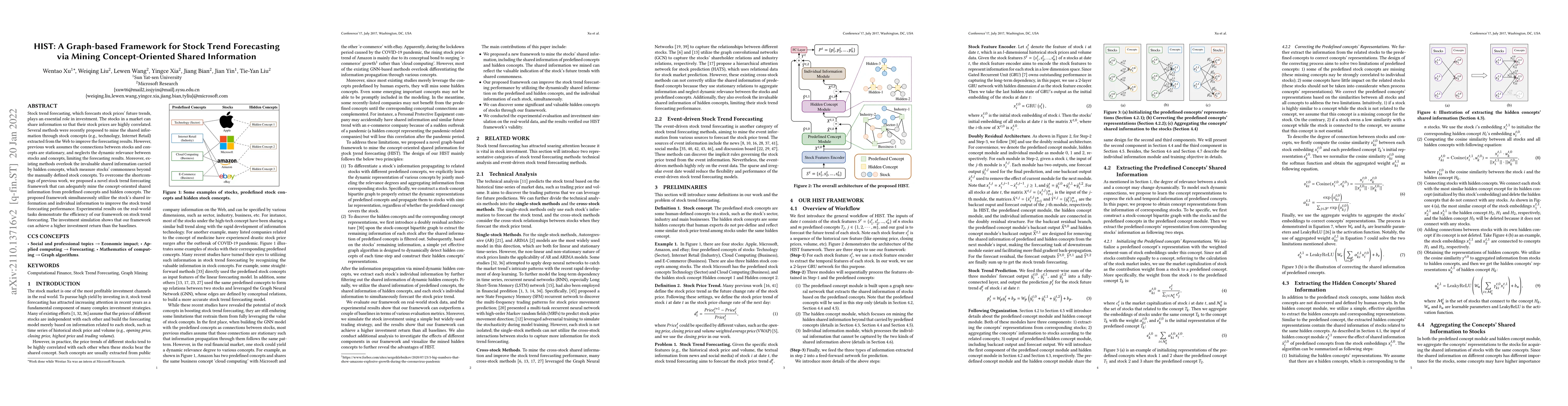

Stock trend forecasting, which forecasts stock prices' future trends, plays an essential role in investment. The stocks in a market can share information so that their stock prices are highly correl...

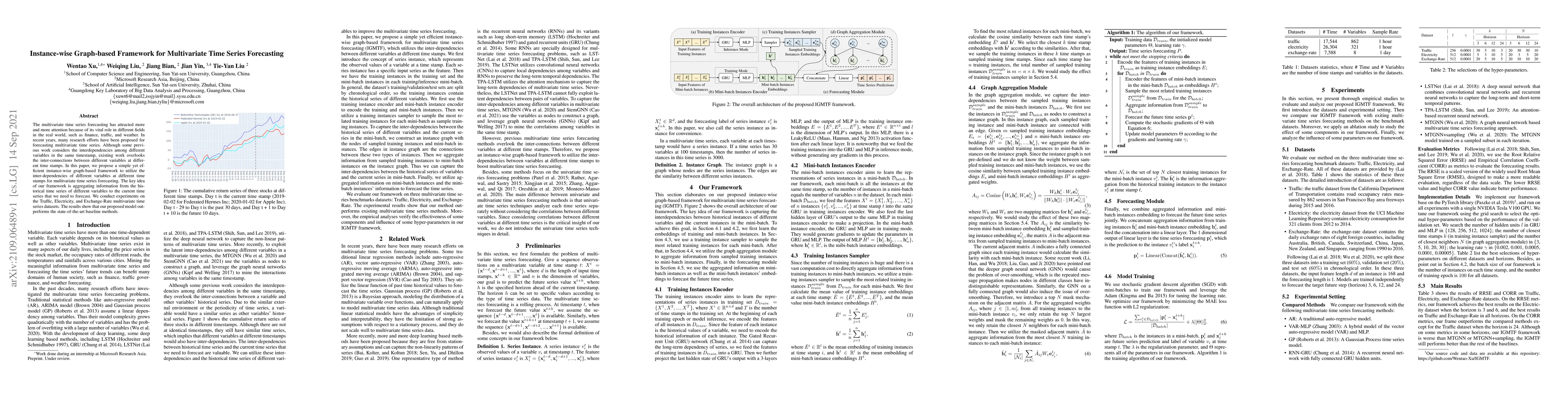

The multivariate time series forecasting has attracted more and more attention because of its vital role in different fields in the real world, such as finance, traffic, and weather. In recent years...

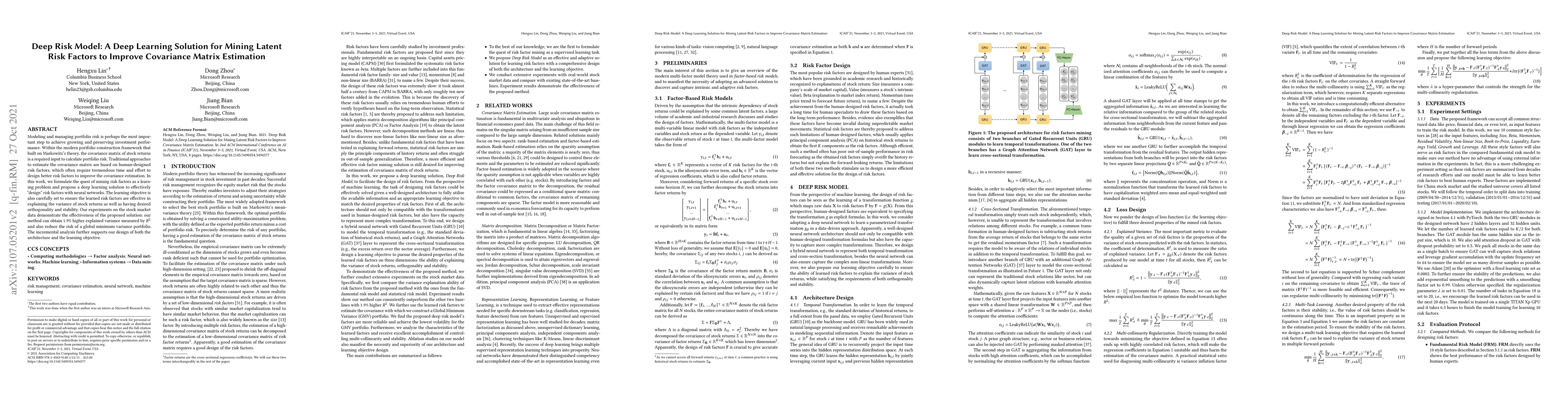

Modeling and managing portfolio risk is perhaps the most important step to achieve growing and preserving investment performance. Within the modern portfolio construction framework that built on Mar...

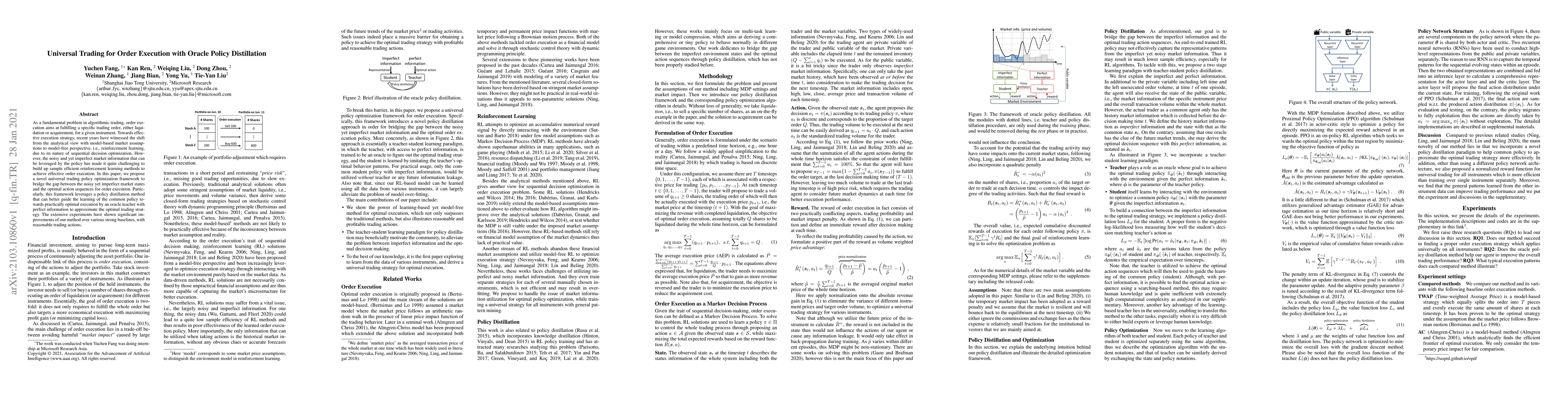

As a fundamental problem in algorithmic trading, order execution aims at fulfilling a specific trading order, either liquidation or acquirement, for a given instrument. Towards effective execution s...

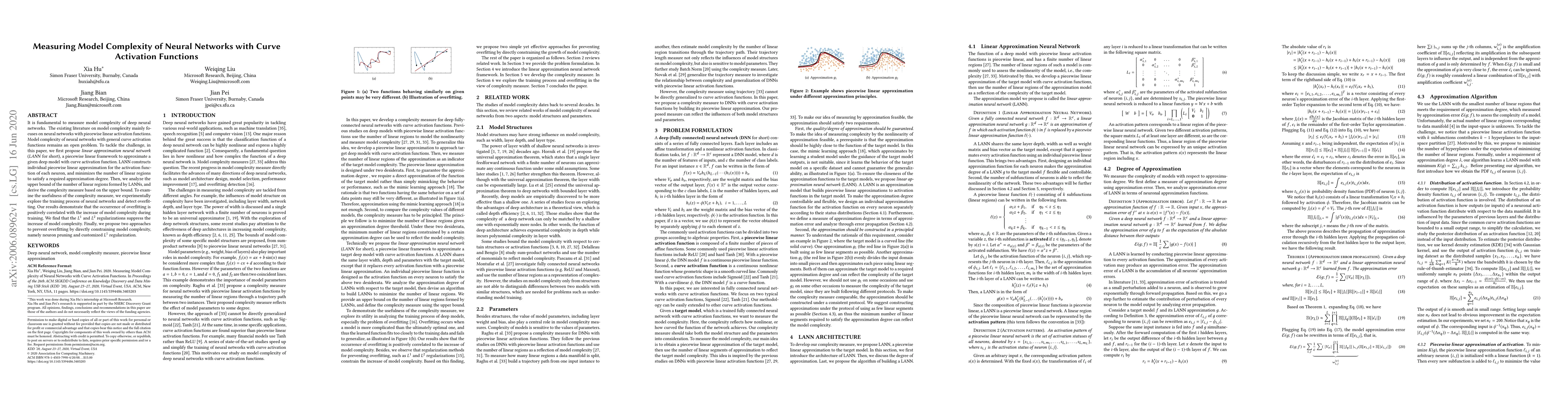

Model complexity is a fundamental problem in deep learning. In this paper we conduct a systematic overview of the latest studies on model complexity in deep learning. Model complexity of deep learni...

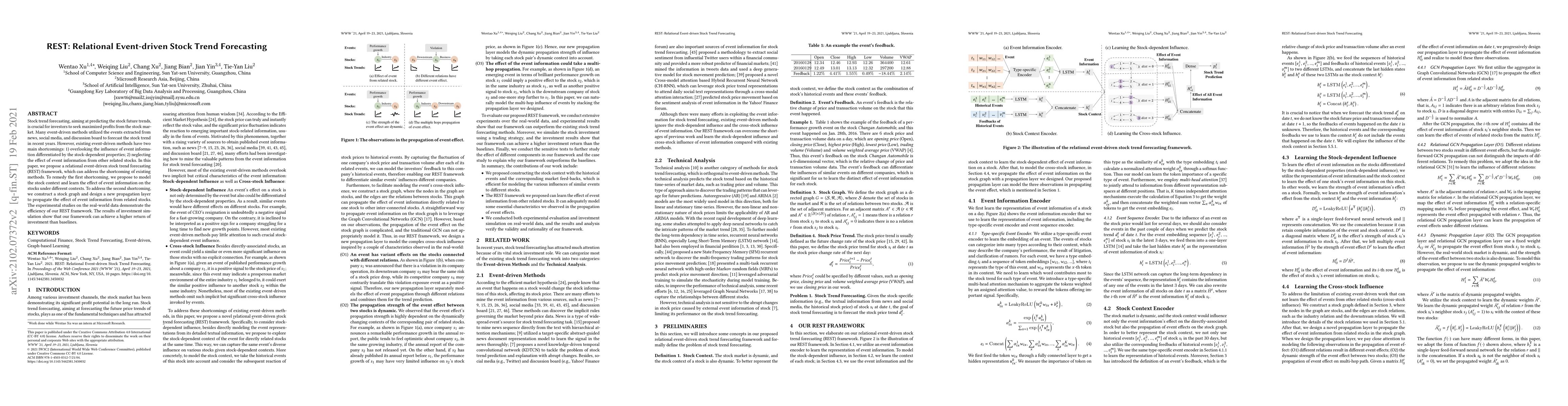

Stock trend forecasting, aiming at predicting the stock future trends, is crucial for investors to seek maximized profits from the stock market. Many event-driven methods utilized the events extract...

Stock trend forecasting has become a popular research direction that attracts widespread attention in the financial field. Though deep learning methods have achieved promising results, there are sti...

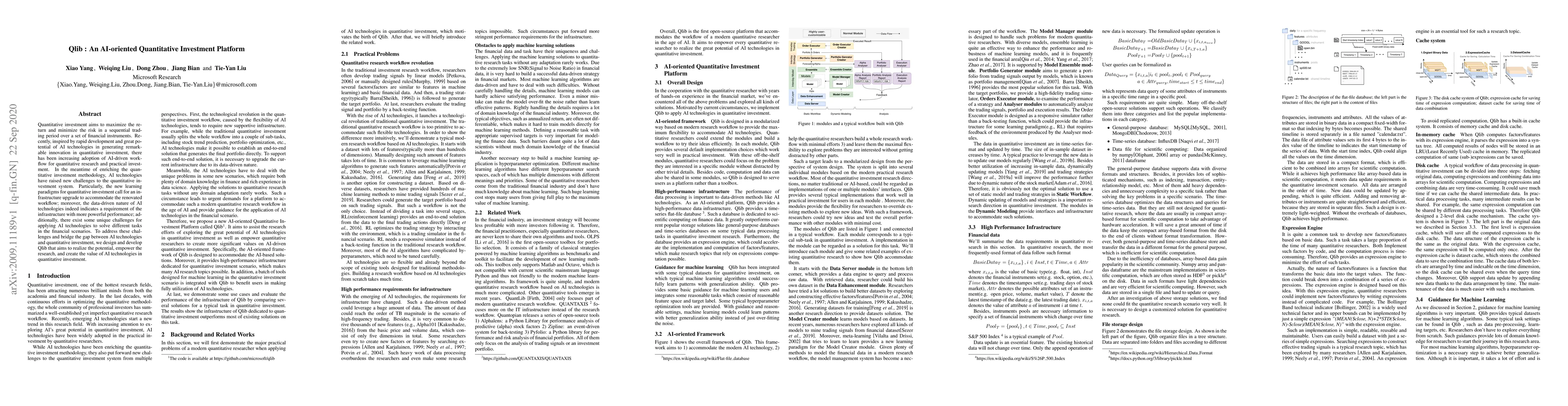

Quantitative investment aims to maximize the return and minimize the risk in a sequential trading period over a set of financial instruments. Recently, inspired by rapid development and great potent...

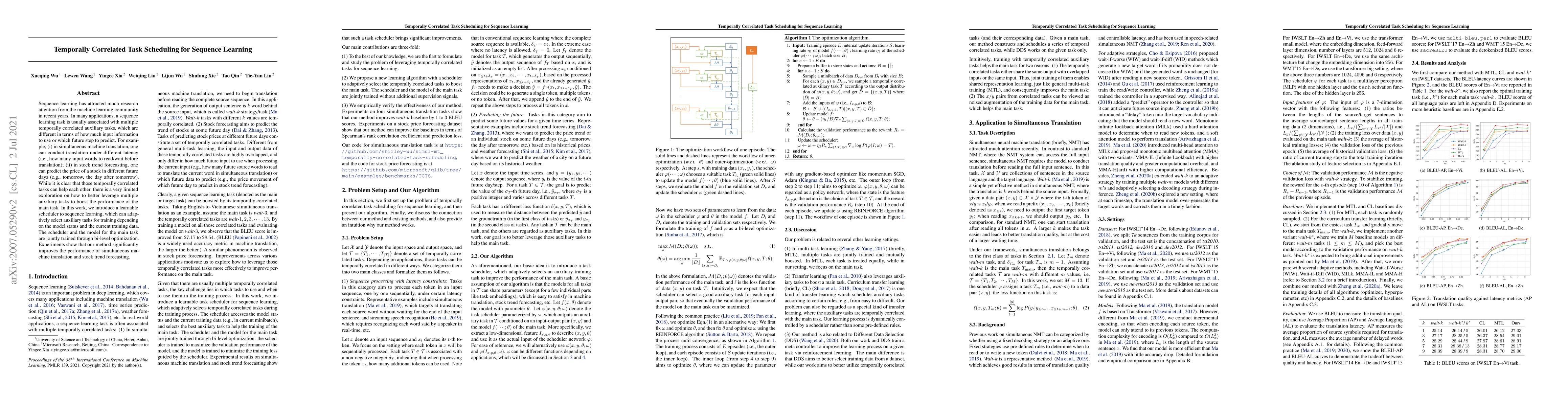

Sequence learning has attracted much research attention from the machine learning community in recent years. In many applications, a sequence learning task is usually associated with multiple tempor...

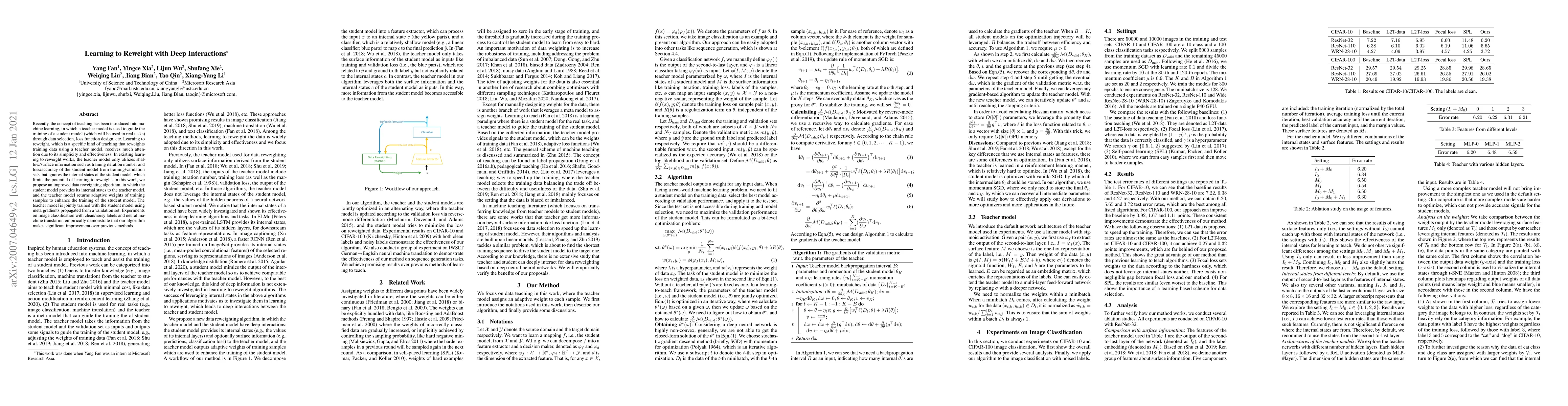

Recently, the concept of teaching has been introduced into machine learning, in which a teacher model is used to guide the training of a student model (which will be used in real tasks) through data...

It is fundamental to measure model complexity of deep neural networks. The existing literature on model complexity mainly focuses on neural networks with piecewise linear activation functions. Model...

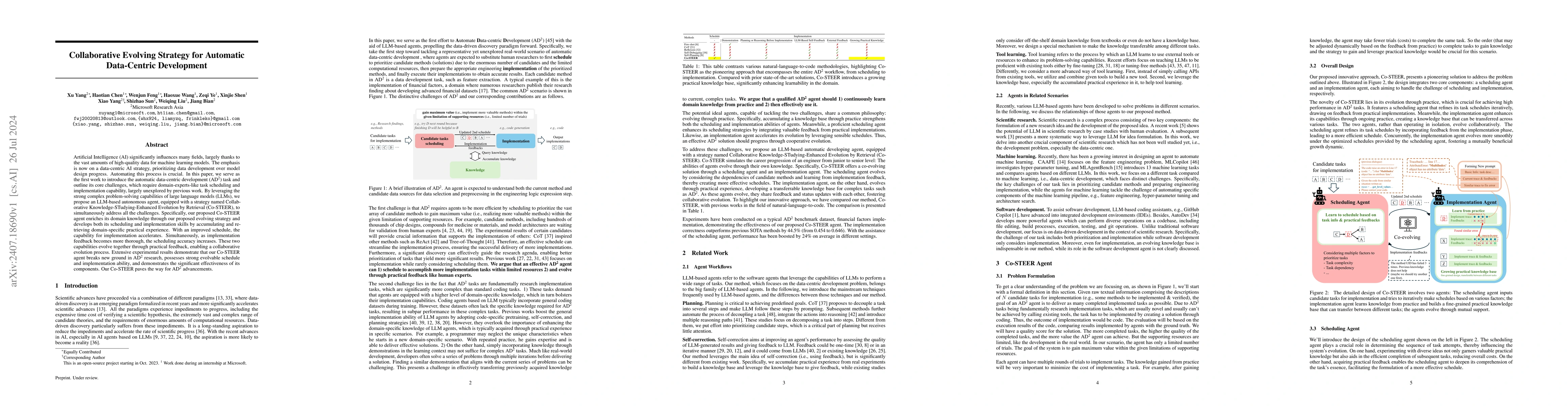

Artificial Intelligence (AI) significantly influences many fields, largely thanks to the vast amounts of high-quality data for machine learning models. The emphasis is now on a data-centric AI strateg...

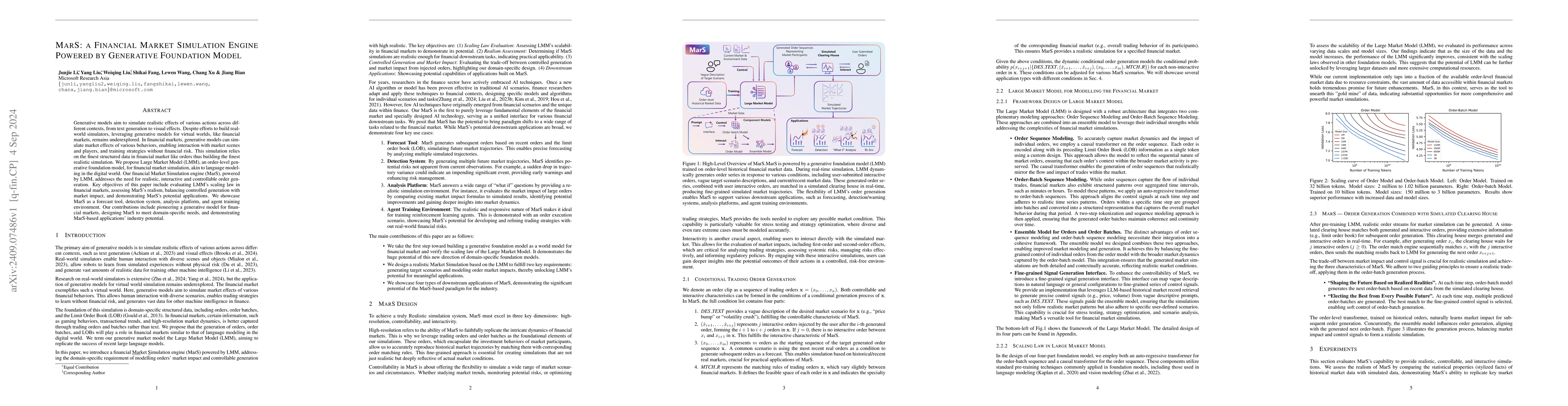

Generative models aim to simulate realistic effects of various actions across different contexts, from text generation to visual effects. Despite efforts to build real-world simulators, leveraging gen...

Data-driven decision-making processes increasingly utilize end-to-end learnable deep neural networks to render final decisions. Sometimes, the output of the forward functions in certain layers is dete...

Order flow modeling stands as the most fundamental and essential financial task, as orders embody the minimal unit within a financial market. However, current approaches often result in unsatisfactory...

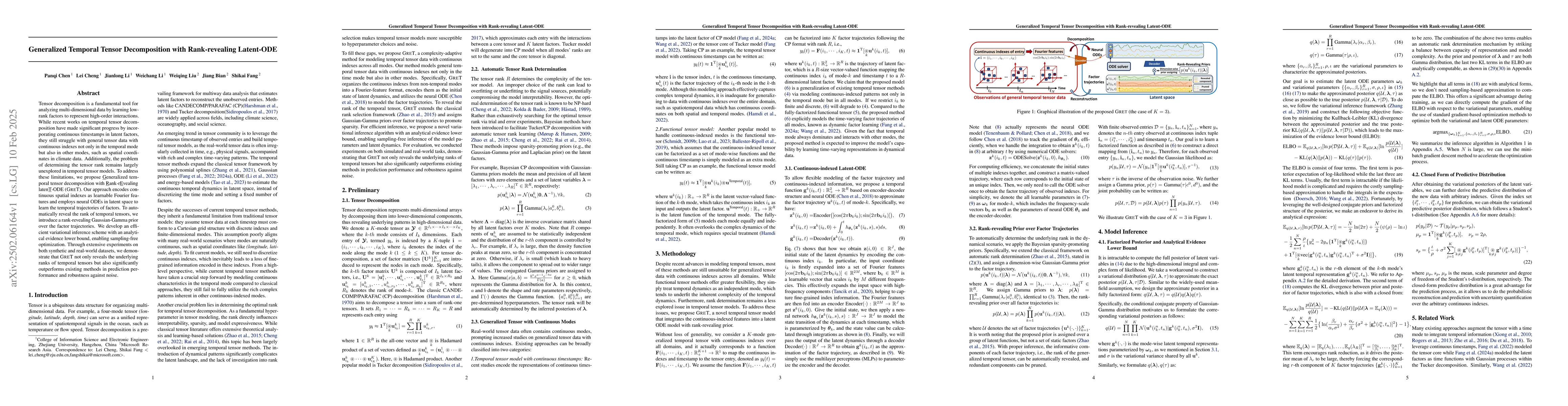

Tensor decomposition is a fundamental tool for analyzing multi-dimensional data by learning low-rank factors to represent high-order interactions. While recent works on temporal tensor decomposition h...

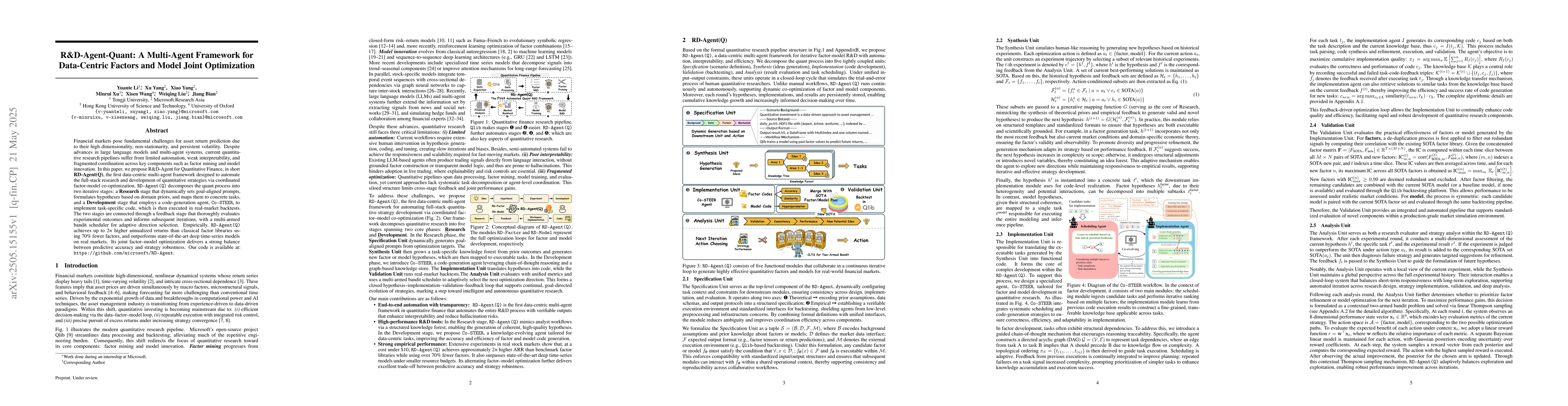

Financial markets pose fundamental challenges for asset return prediction due to their high dimensionality, non-stationarity, and persistent volatility. Despite advances in large language models and m...

Modeling and reconstructing multidimensional physical dynamics from sparse and off-grid observations presents a fundamental challenge in scientific research. Recently, diffusion-based generative model...

Recent advances in AI and ML have transformed data science, yet increasing complexity and expertise requirements continue to hinder progress. Although crowd-sourcing platforms alleviate some challenge...

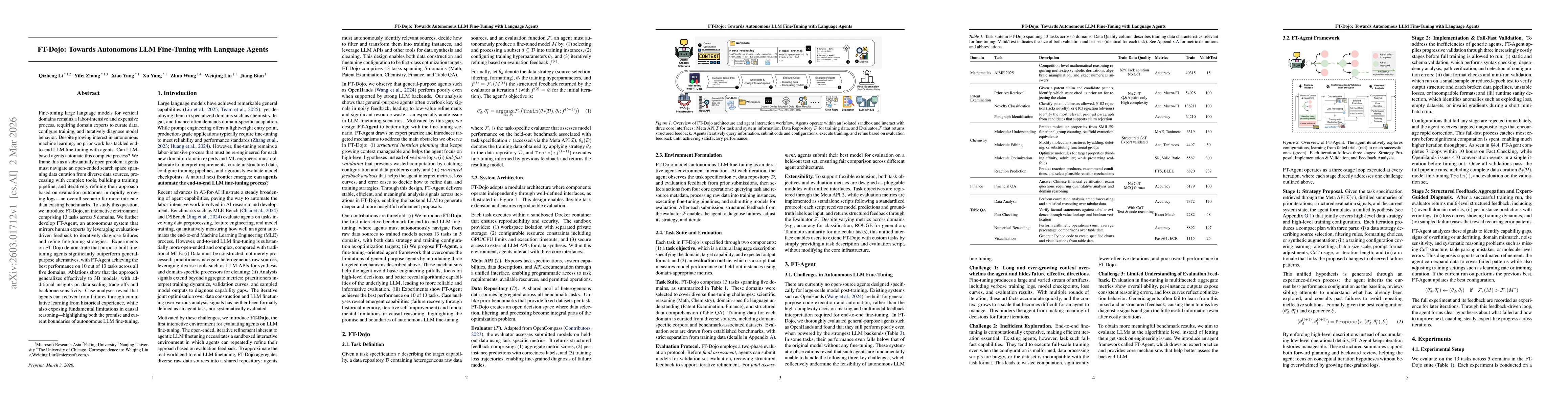

Fine-tuning large language models for vertical domains remains a labor-intensive and expensive process, requiring domain experts to curate data, configure training, and iteratively diagnose model beha...

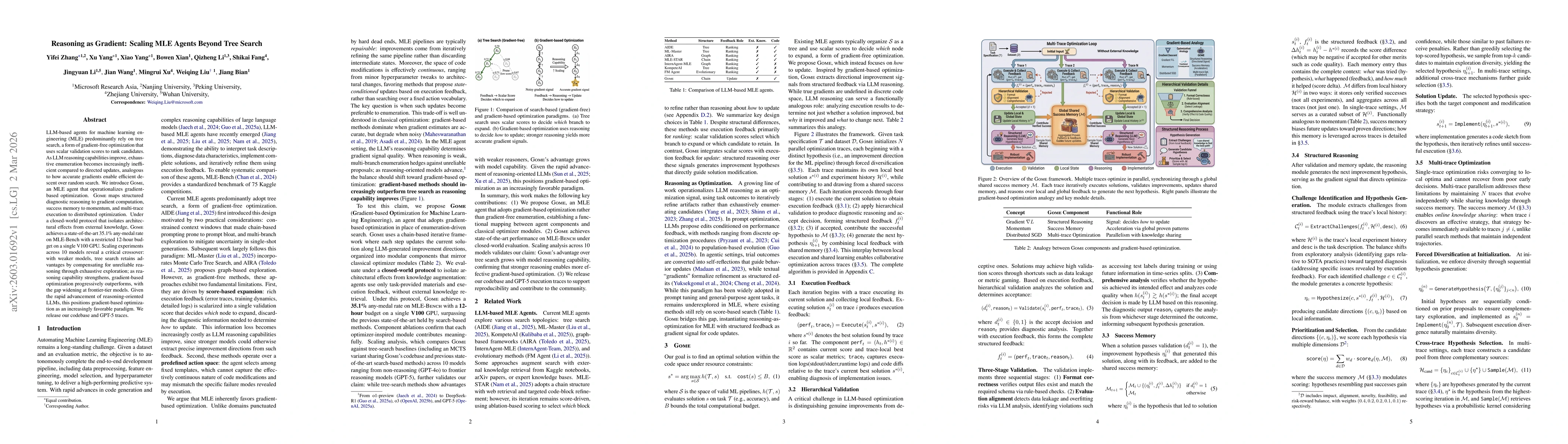

LLM-based agents for machine learning engineering (MLE) predominantly rely on tree search, a form of gradient-free optimization that uses scalar validation scores to rank candidates. As LLM reasoning ...

We introduce Agent^2 RL-Bench, a benchmark for evaluating agentic RL post-training -- whether LLM agents can autonomously design, implement, and run complete RL pipelines that improve foundation model...

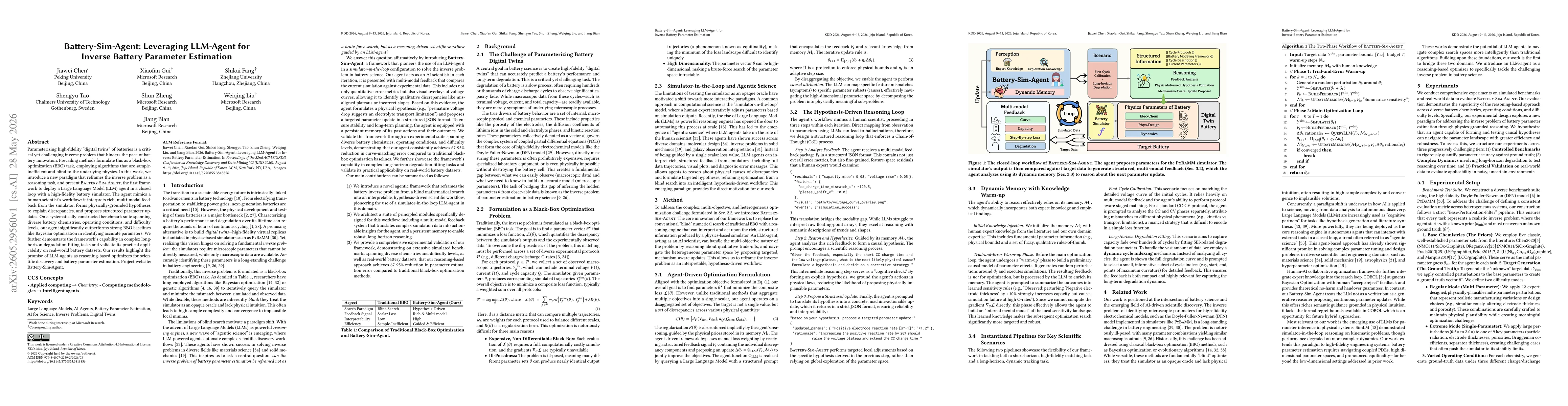

Parameterizing high-fidelity "digital twins" of batteries is a critical yet challenging inverse problem that hinders the pace of battery innovation. Prevailing methods formulate this as a black-box op...