Academic Profile

Statistics

Similar Authors

Papers on arXiv

Accounting for uncertainty in Data quality is important for accurate statistical inference. We aim to an optimal conservative allocation for a large universe of assets in mean-variance portfolio (MV...

In this paper, we propose a novel robust Principal Component Analysis (PCA) for high-dimensional data in the presence of various heterogeneities, especially the heavy-tailedness and outliers. A tran...

Principal component analysis (PCA), the most popular dimension-reduction technique, has been used to analyze high-dimensional data in many areas. It discovers the homogeneity within the data and cre...

We propose modeling raw functional data as a mixture of a smooth function and a high-dimensional factor component. The conventional approach to retrieving the smooth function from the raw data is th...

High-dimensional autocovariance matrices play an important role in dimension reduction for high-dimensional time series. In this article, we establish the central limit theorem (CLT) for spiked eige...

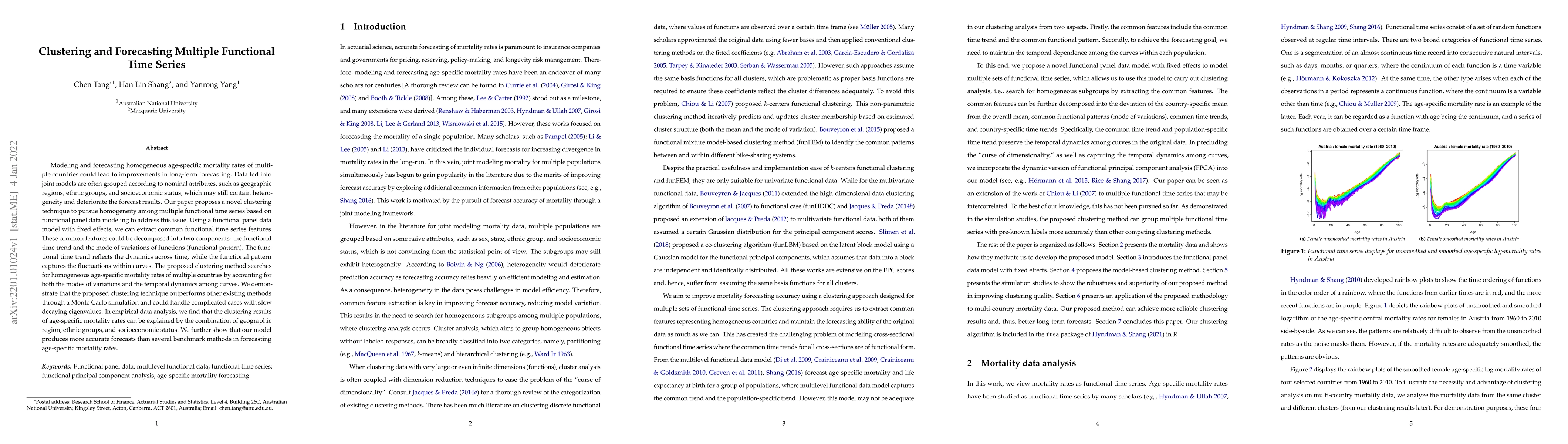

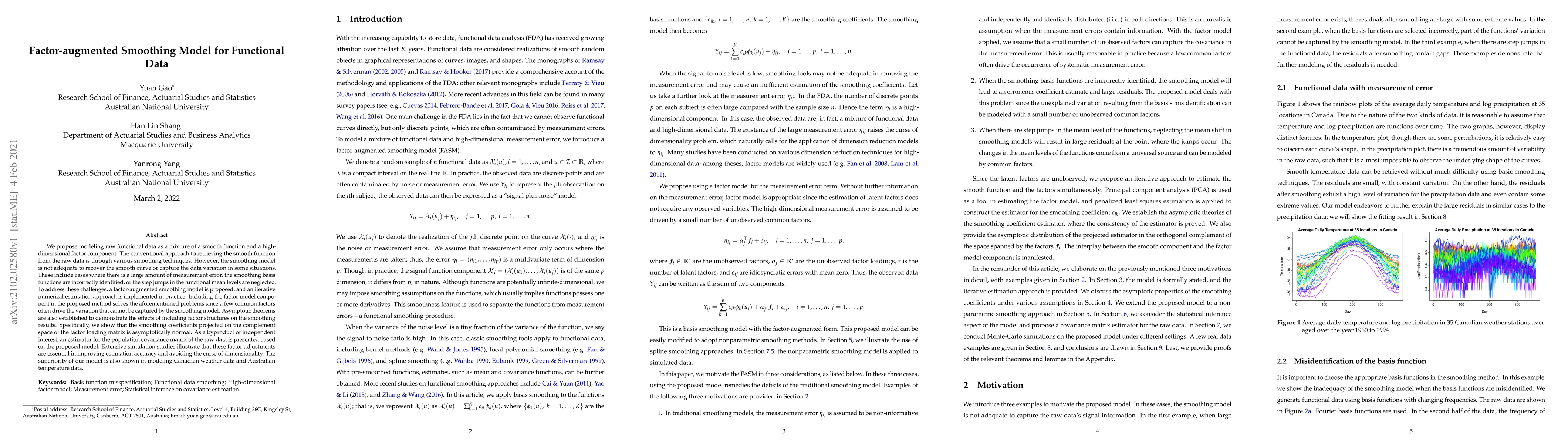

Modelling and forecasting homogeneous age-specific mortality rates of multiple countries could lead to improvements in long-term forecasting. Data fed into joint models are often grouped according t...

This paper proposes a new AR-sieve bootstrap approach on high-dimensional time series. The major challenge of classical bootstrap methods on high-dimensional time series is two-fold: the curse dimen...

This paper considers a model with general regressors and unobservable factors. An estimator based on iterated principal components is proposed, which is shown to be not only asymptotically normal an...

We propose a dual-factor model for high-dimensional functional time series (HDFTS) that considers multiple populations. The HDFTS is first decomposed into a collection of functional time series (FTS...

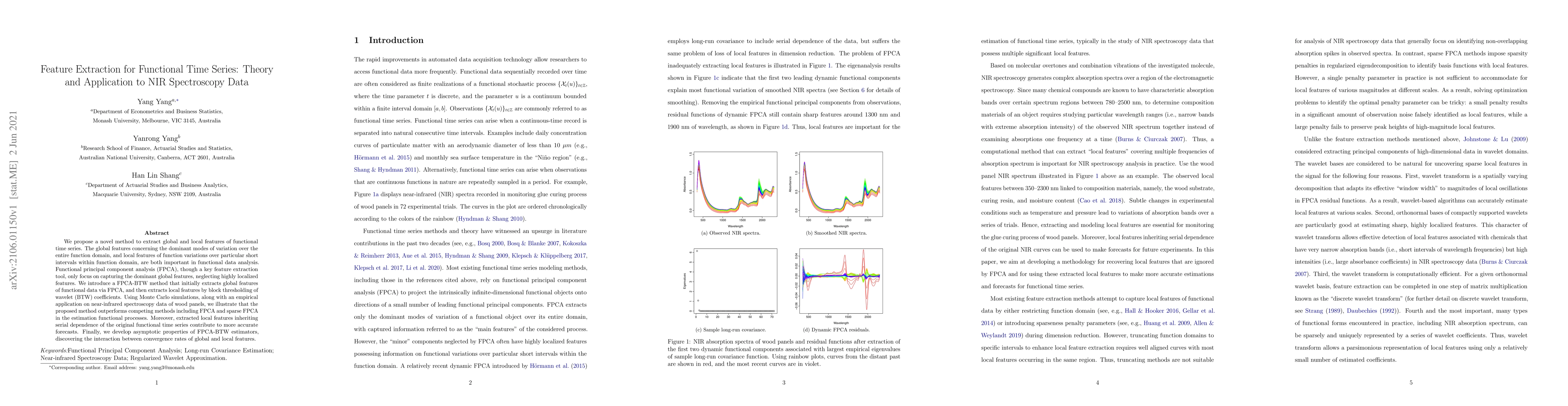

We propose a novel method to extract global and local features of functional time series. The global features concerning the dominant modes of variation over the entire function domain, and local fe...

Mortality forecasting plays a pivotal role in insurance and financial risk management of life insurers, pension funds, and social securities. Mortality data is usually high-dimensional in nature and...

We propose modeling raw functional data as a mixture of a smooth function and a highdimensional factor component. The conventional approach to retrieving the smooth function from the raw data is thr...

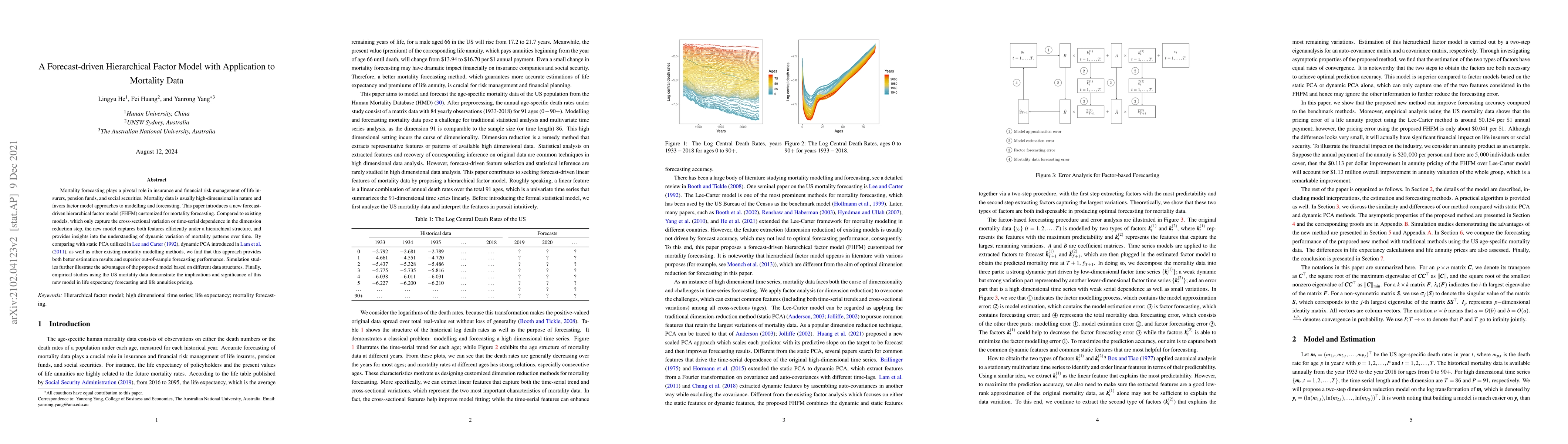

Many existing mortality models follow the framework of classical factor models, such as the Lee-Carter model and its variants. Latent common factors in factor models are defined as time-related mort...

This study decomposes the bilateral trade flows using a three-dimensional panel data model. Under the scenario that all three dimensions diverge to infinity, we propose an estimation approach to ide...

We study the relationship between model complexity and out-of-sample performance in the context of mean-variance portfolio optimization. Representing model complexity by the number of assets, we find ...

Fairness-aware statistical learning is critical for data-driven decision-making to mitigate discrimination against protected attributes, such as gender, race, and ethnicity. This is especially importa...

This paper proposes a robust, shocks-adaptive portfolio in a large-dimensional assets universe where the number of assets could be comparable to or even larger than the sample size. It is well documen...

Regression with a spherical response is challenging due to the absence of linear structure, making standard regression models inadequate. Existing methods, mainly parametric, lack the flexibility to c...

Accurate transfer of information across multiple sectors to enhance model estimation is both significant and challenging in multi-sector portfolio optimization involving a large number of assets in di...

Most existing methods for testing equality of means of functional data from multiple populations rely on assumptions of equal covariance and/or Gaussianity. In this work we provide a new testing metho...

This paper investigates the impact of environmental, social, and governance (ESG) constraint on a regularized mean-variance (MV) portfolio optimization problem in a large-dimensional setting, in which...

This article explores a general factor structure for high-dimensional nonstationary functional time series, encompassing a wide range of factor models studied in the existing literature. We investigat...

We develop a distributionally robust formulation of principal component analysis that minimizes worst-case reconstruction risk over distributions lying within a Wasserstein neighborhood of the empiric...