Academic Profile

Statistics

Papers on arXiv

Stock price prediction is a challenging problem in the field of finance and receives widespread attention. In recent years, with the rapid development of technologies such as deep learning and graph n...

As financial markets grow increasingly complex in the big data era, accurate stock prediction has become more critical. Traditional time series models, such as GRUs, have been widely used but often st...

Financial time series (FinTS) record the behavior of human-brain-augmented decision-making, capturing valuable historical information that can be leveraged for profitable investment strategies. Not su...

Recently, combining stock features with inter-stock correlations has become a common and effective approach for stock movement prediction. However, financial data presents significant challenges due t...

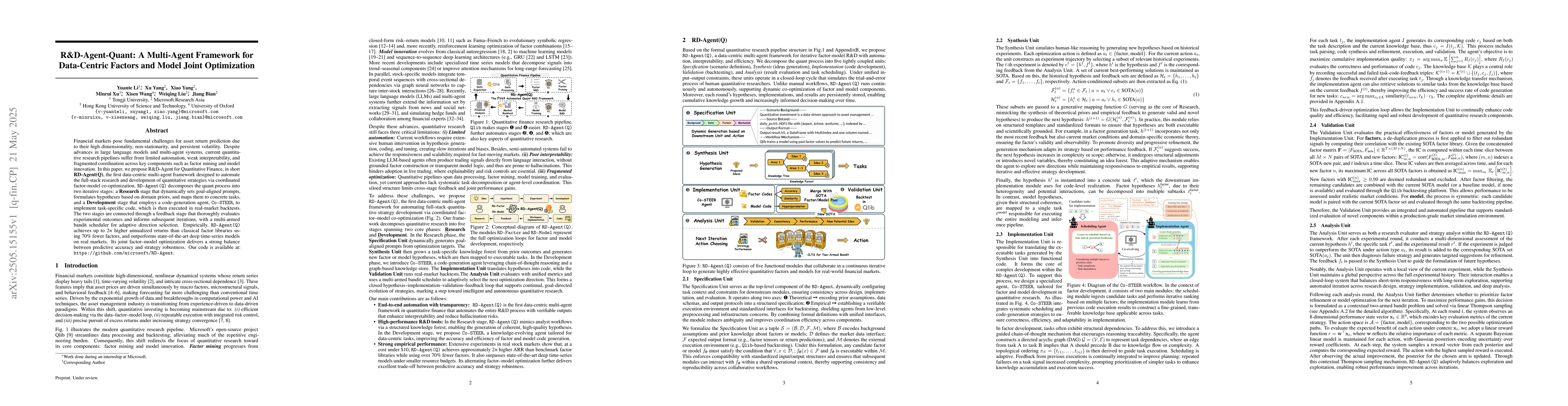

Financial markets pose fundamental challenges for asset return prediction due to their high dimensionality, non-stationarity, and persistent volatility. Despite advances in large language models and m...

Quantitative research increasingly relies on unstructured financial content such as filings, earnings calls, and research notes, yet existing LLM and RAG pipelines struggle with point-in-time correctn...

Recent advances in AI and ML have transformed data science, yet increasing complexity and expertise requirements continue to hinder progress. Although crowd-sourcing platforms alleviate some challenge...

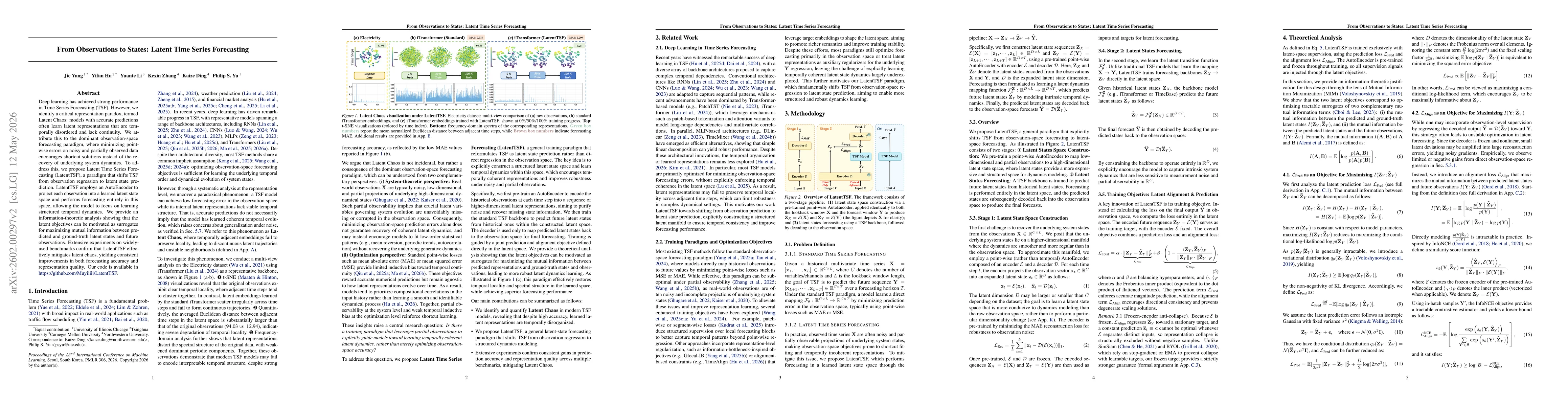

Deep learning has achieved strong performance in Time Series Forecasting (TSF). However, we identify a critical representation paradox, termed Latent Chaos: models with accurate predictions often lear...

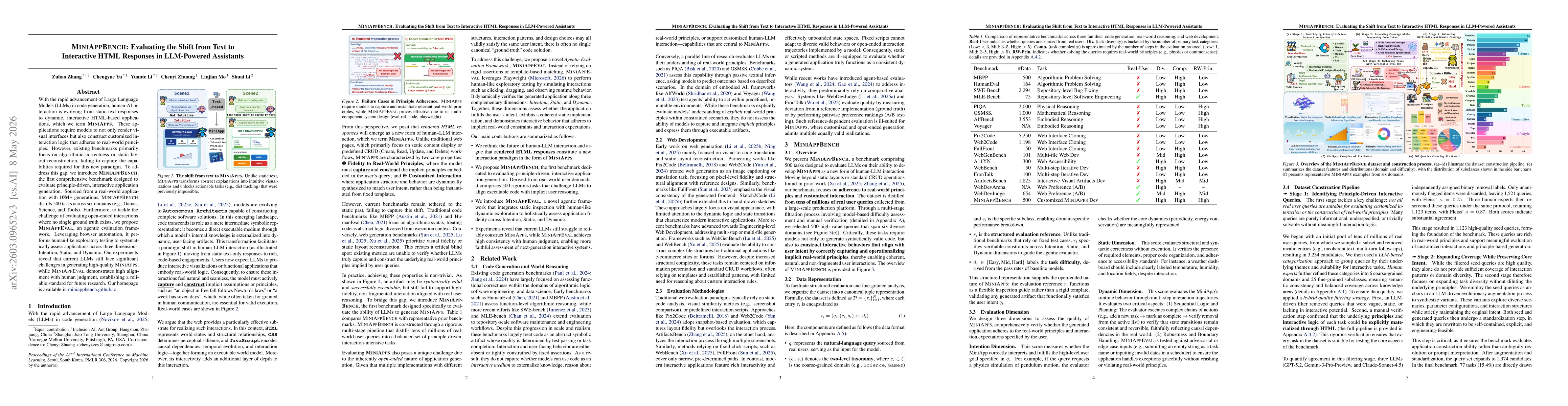

With the rapid advancement of Large Language Models (LLMs) in code generation, human-AI interaction is evolving from static text responses to dynamic, interactive HTML-based applications, which we ter...

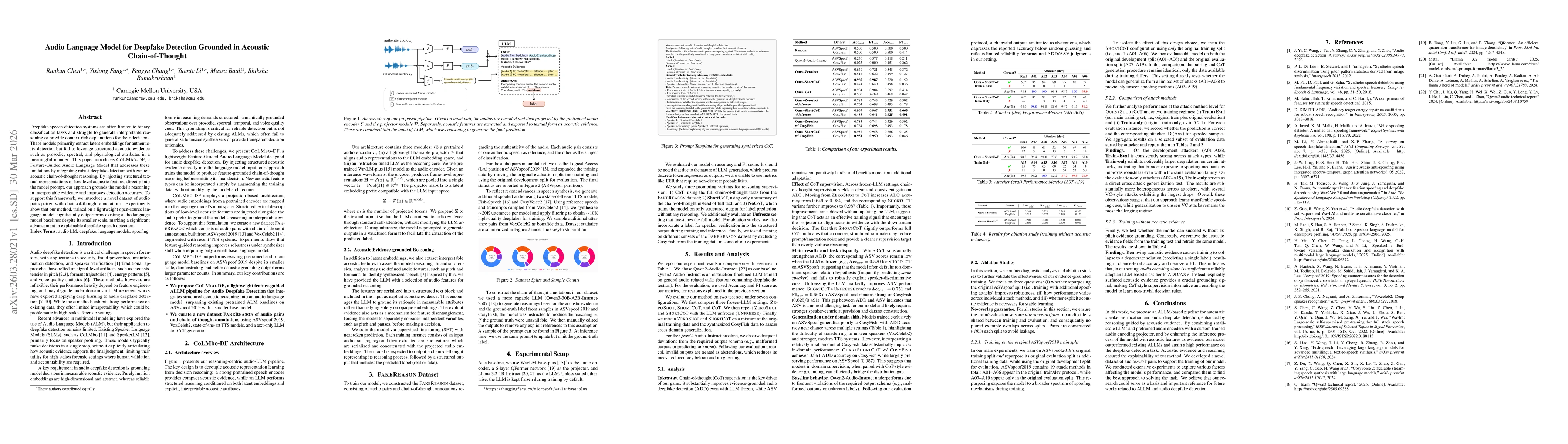

Deepfake speech detection systems are often limited to binary classification tasks and struggle to generate interpretable reasoning or provide context-rich explanations for their decisions. These mode...

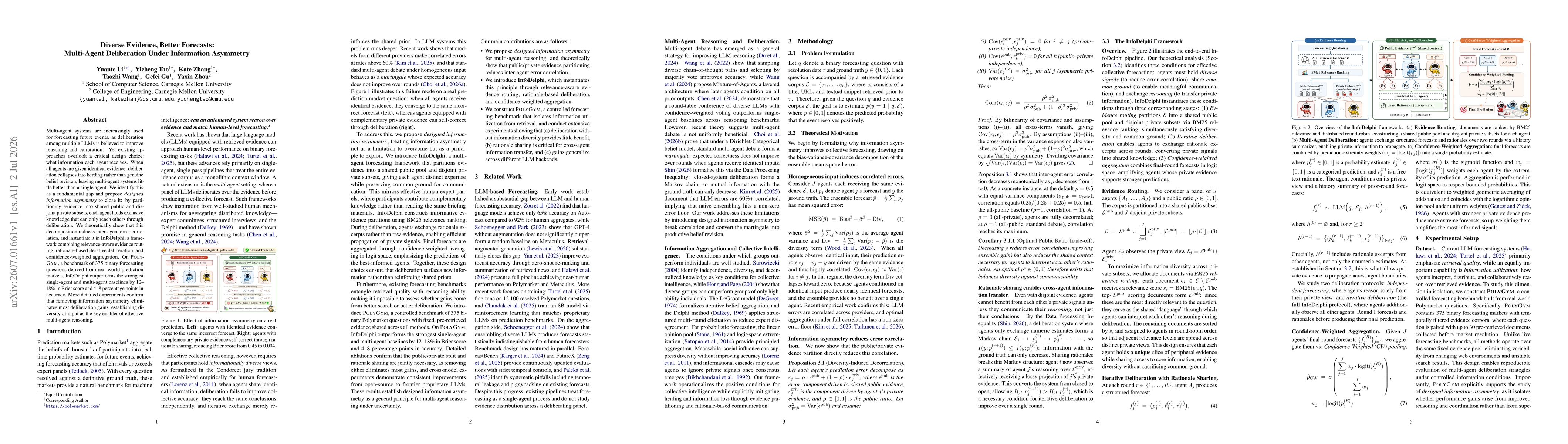

Multi-agent systems are increasingly used for forecasting future events, as deliberation among multiple LLMs is believed to improve reasoning and calibration. Yet existing approaches overlook a critic...