Recent advances in reinforcement learning, such as Dynamic Sampling Policy

Optimization (DAPO), show strong performance when paired with large language

models (LLMs). Motivated by this success, we ask whether similar gains can be

realized in financial trading. We design a trading agent that combines an

improved Group Relative Policy Optimization (GRPO) algorithm, augmented with

ideas from DAPO, with LLM-based risk and sentiment signals extracted from

financial news. On the NASDAQ-100 index (FNSPID dataset), our agent attains a

cumulative return of 230.49 percent and an information ratio of 0.37,

outperforming the CPPO-DeepSeek baseline. It also cuts training time from about

8 hours to 2.5 hours over 100 epochs while markedly reducing RAM usage. The

proposed RL-LLM framework offers a scalable path toward data-efficient trading

agents. Code: https://github.com/Ruijian-Zha/FinRL-DAPO-SR/

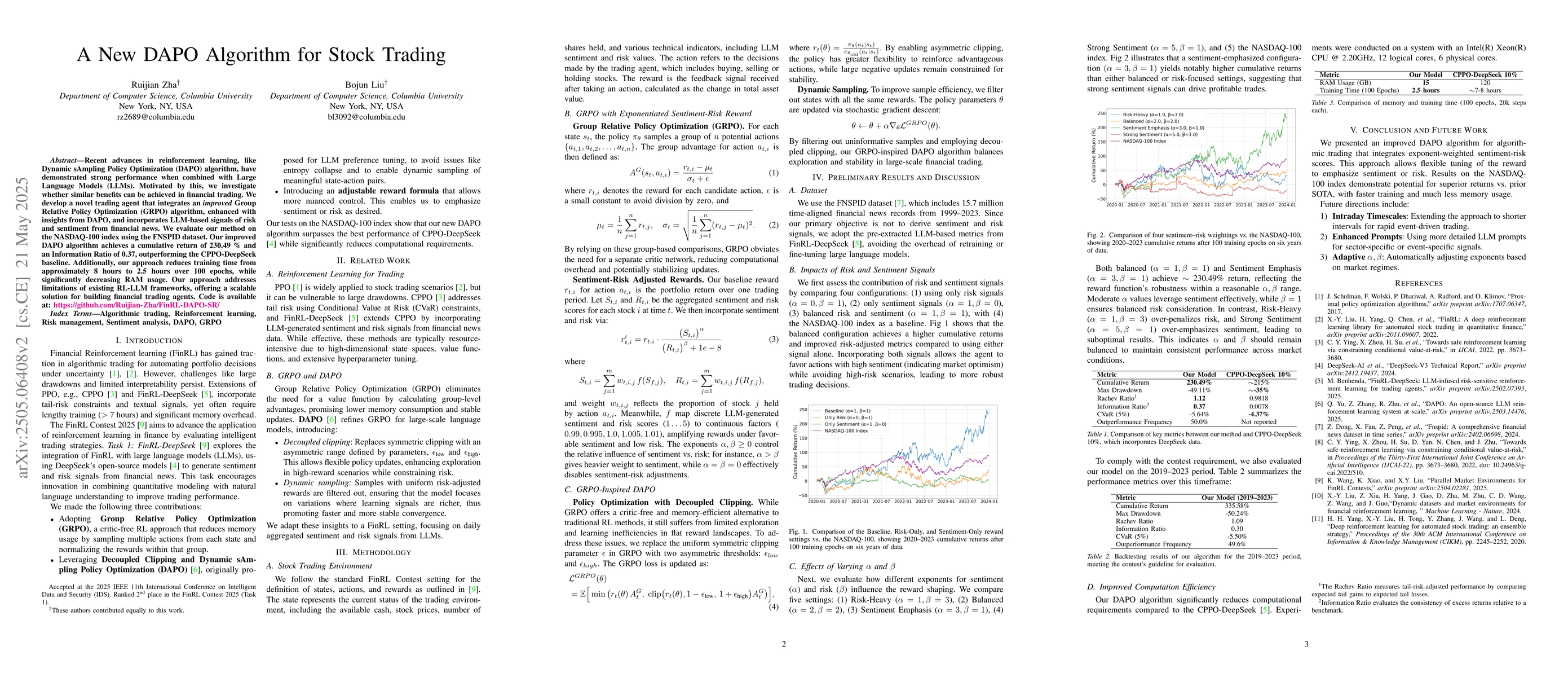

Discussion 0