Publication

Metrics

AI Quick Summary

This research paper analyzes bilateral trade from a regret minimization perspective, providing tight bounds on the regret for various feedback models and private valuations in different scenarios.

Paper Preview

Abstract

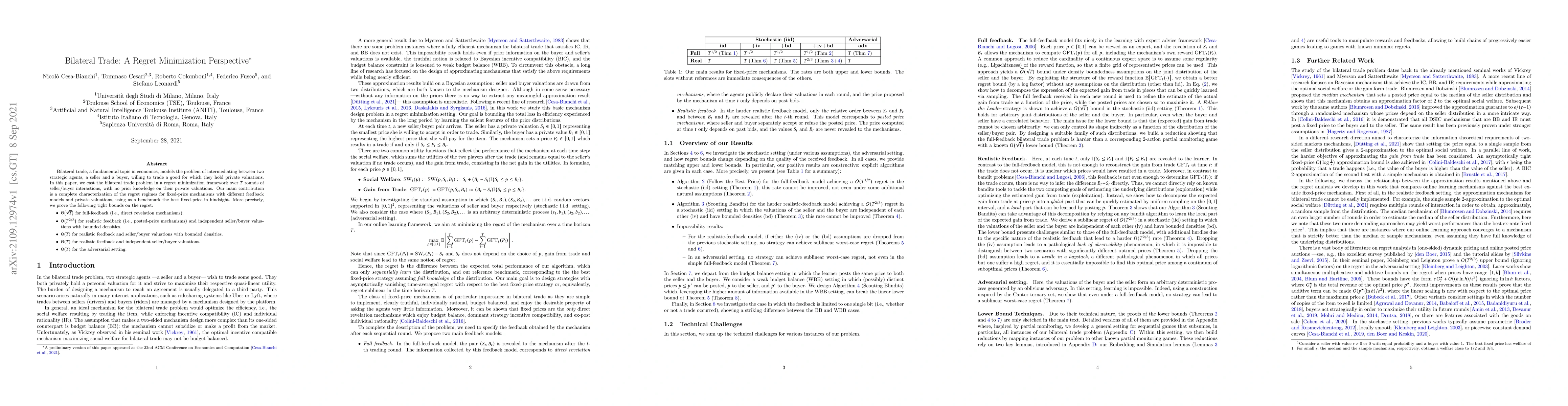

Bilateral trade, a fundamental topic in economics, models the problem of intermediating between two strategic agents, a seller and a buyer, willing to trade a good for which they hold private valuations. In this paper, we cast the bilateral trade problem in a regret minimization framework over $T$ rounds of seller/buyer interactions, with no prior knowledge on their private valuations. Our main contribution is a complete characterization of the regret regimes for fixed-price mechanisms with different feedback models and private valuations, using as a benchmark the best fixed-price in hindsight. More precisely, we prove the following tight bounds on the regret: - $\Theta(\sqrt{T})$ for full-feedback (i.e., direct revelation mechanisms). - $\Theta(T^{2/3})$ for realistic feedback (i.e., posted-price mechanisms) and independent seller/buyer valuations with bounded densities. - $\Theta(T)$ for realistic feedback and seller/buyer valuations with bounded densities. - $\Theta(T)$ for realistic feedback and independent seller/buyer valuations. - $\Theta(T)$ for the adversarial setting.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0