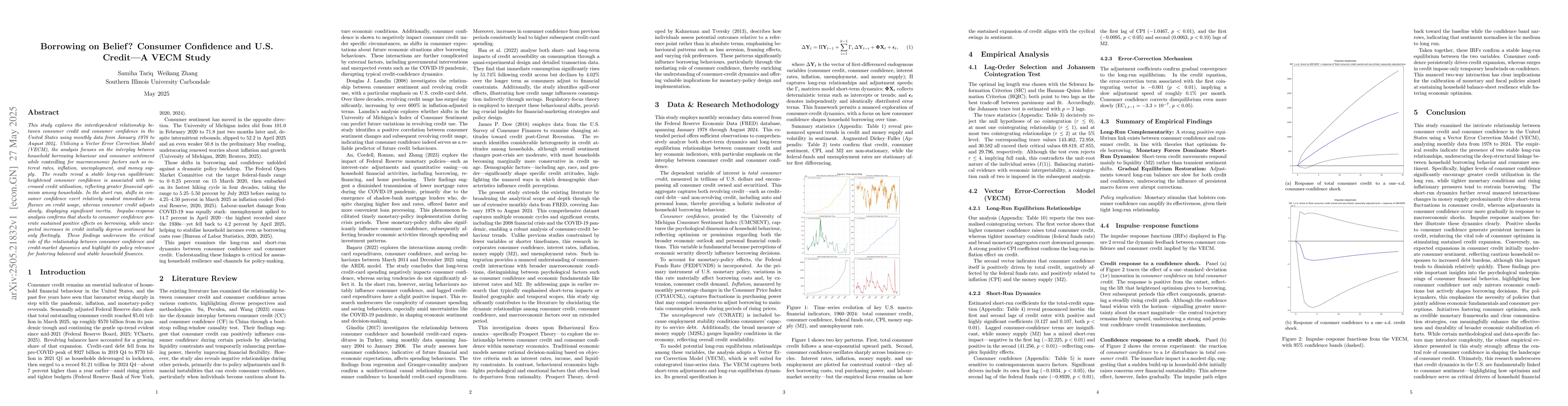

This study explores the interdependent relationship between consumer credit

and consumer confidence in the United States using monthly data from January

1978 to August 2024. Utilizing a Vector Error Correction Model (VECM), the

analysis focuses on the interplay between household borrowing behaviour and

consumer sentiment while controlling for macroeconomic factors such as interest

rates, inflation, unemployment, and money supply. The results reveal a stable

long-run equilibrium: heightened consumer confidence is associated with

increased credit utilization, reflecting greater financial optimism among

households. In the short run, shifts in consumer confidence exert relatively

modest immediate influence on credit usage, whereas consumer credit adjusts

slowly, displaying significant inertia. Impulse-response analysis confirms that

shocks to consumer confidence generate sustained positive effects on borrowing,

while unexpected increases in credit initially depress sentiment but only

fleetingly. These findings underscore the critical role of the relationship

between consumer confidence and credit-market dynamics and highlight its policy

relevance for fostering balanced and stable household finances.

Discussion 0