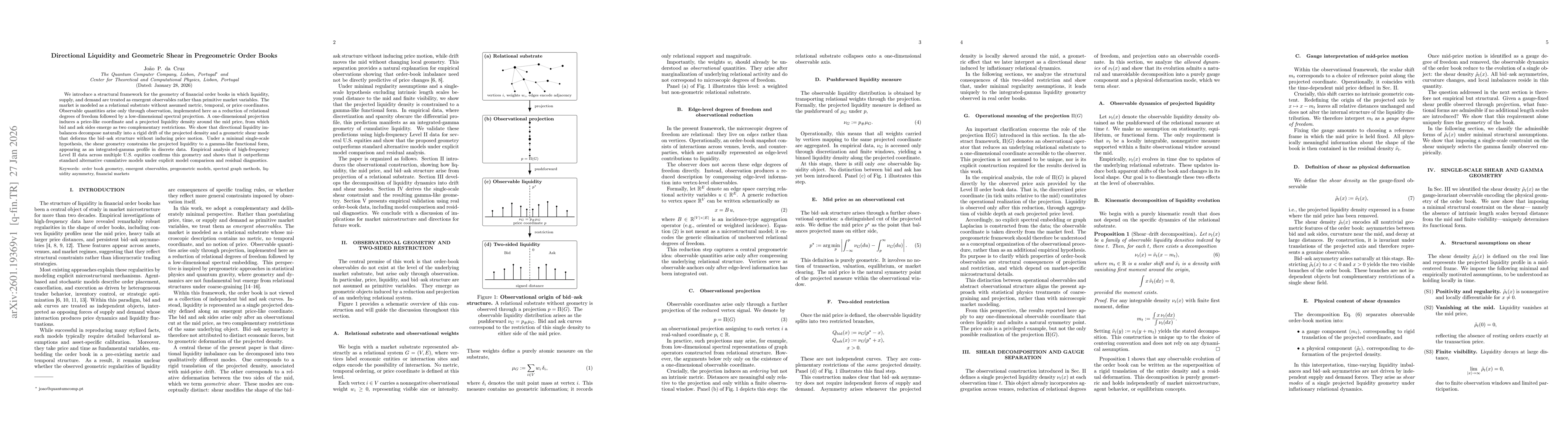

We introduce a structural framework for the geometry of financial order books in which liquidity, supply, and demand are treated as emergent observables rather than primitive market variables. The market is modeled as a relational substrate without assumed metric, temporal, or price coordinates. Observable quantities arise only through observation, implemented here as a reduction of relational degrees of freedom followed by a low-dimensional spectral projection. A one-dimensional projection induces a price-like coordinate and a projected liquidity density around the mid price, from which bid and ask sides emerge as two complementary restrictions. We show that directional liquidity imbalances decompose naturally into a rigid drift of the projected density and a geometric shear mode that deforms the bid--ask structure without inducing price motion. Under a minimal single-scale hypothesis, the shear geometry constrains the projected liquidity to a gamma-like functional form, appearing as an integrated-gamma profile in discrete data. Empirical analysis of high-frequency Level~II data across multiple U.S. equities confirms this geometry and shows that it outperforms standard alternative cumulative models under explicit model comparison and residual diagnostics.

Discussion 0