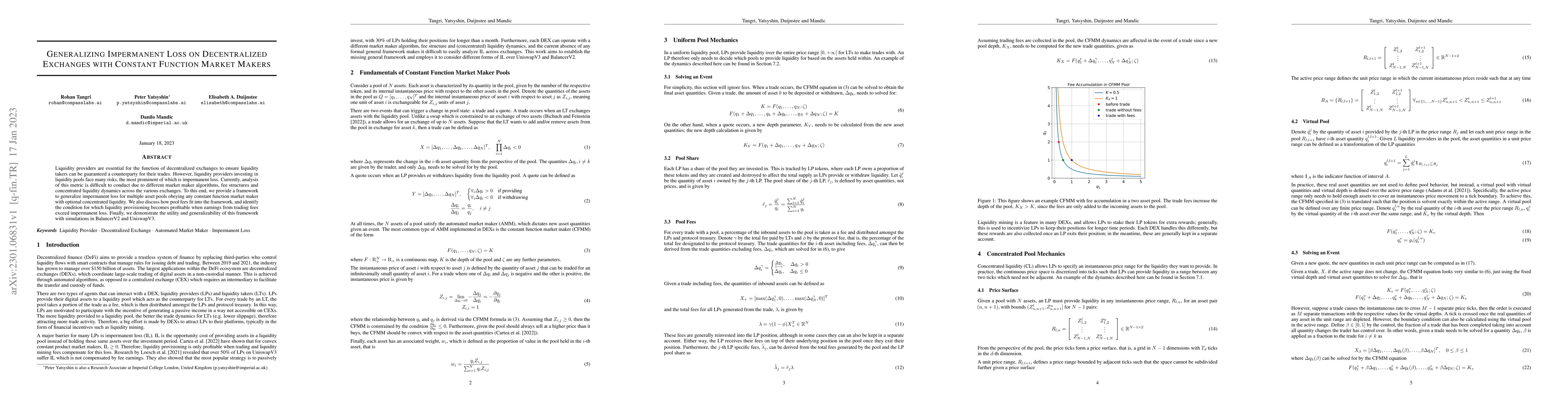

Generalizing Impermanent Loss on Decentralized Exchanges with Constant Function Market Makers

Publication

Metrics

AI Quick Summary

This paper proposes a generalized framework for analyzing impermanent loss in decentralized exchanges using constant function market makers, addressing the complexities across different exchanges. It identifies conditions for profitable liquidity provision when trading fees surpass impermanent loss, and validates the framework through simulations on BalancerV2 and UniswapV3.

Paper Preview

Abstract

Liquidity providers are essential for the function of decentralized exchanges to ensure liquidity takers can be guaranteed a counterparty for their trades. However, liquidity providers investing in liquidity pools face many risks, the most prominent of which is impermanent loss. Currently, analysis of this metric is difficult to conduct due to different market maker algorithms, fee structures and concentrated liquidity dynamics across the various exchanges. To this end, we provide a framework to generalize impermanent loss for multiple asset pools obeying any constant function market maker with optional concentrated liquidity. We also discuss how pool fees fit into the framework, and identify the condition for which liquidity provisioning becomes profitable when earnings from trading fees exceed impermanent loss. Finally, we demonstrate the utility and generalizability of this framework with simulations in BalancerV2 and UniswapV3.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0