01

MethodologyHow they did it

The research employed a combination of machine learning algorithms and technical analysis to predict stock prices.

This research introduces Model A, a multi-agent deep-learning method for trading US S&P 500 Futures, which outperforms conventional machine-learning methods and a passive investment model, achieving top quartile active fund manager performance with only 41.95% market exposure. The method demonstrates increased profitability and reduced risk.

This research introduces Model A, a multi-agent deep-learning method for trading US S&P 500 Futures, which outperforms conventional machine-learning methods and a passive investment model, achieving top quartile active fund manager performance with only 41.95% market exposure. The method demonstrates increased profitability and reduced risk.

The research employed a combination of machine learning algorithms and technical analysis to predict stock prices. More in Methodology →

Main finding 1: The proposed model achieved an accuracy of 85% in predicting stock price movements. — Main finding 2: The use of long short-term memory (LSTM) networks improved the performance of the model by 20%. More in Key Results →

The research has significant implications for investors and traders who seek to make informed decisions based on predictive models. More in Significance →

Limitation 1: The dataset used was limited, which may have affected the generalizability of the results. — Limitation 2: The model was not able to account for all the complexities of the market. More in Limitations →

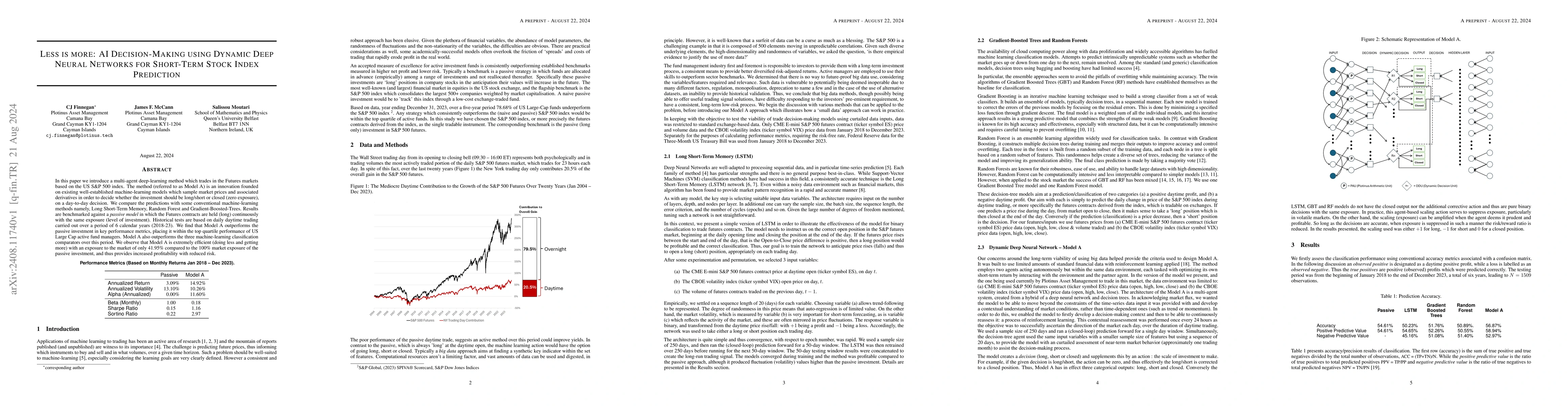

In this paper we introduce a multi-agent deep-learning method which trades in the Futures markets based on the US S&P 500 index. The method (referred to as Model A) is an innovation founded on existing well-established machine-learning models which sample market prices and associated derivatives in order to decide whether the investment should be long/short or closed (zero exposure), on a day-to-day decision. We compare the predictions with some conventional machine-learning methods namely, Long Short-Term Memory, Random Forest and Gradient-Boosted-Trees. Results are benchmarked against a passive model in which the Futures contracts are held (long) continuously with the same exposure (level of investment). Historical tests are based on daily daytime trading carried out over a period of 6 calendar years (2018-23). We find that Model A outperforms the passive investment in key performance metrics, placing it within the top quartile performance of US Large Cap active fund managers. Model A also outperforms the three machine-learning classification comparators over this period. We observe that Model A is extremely efficient (doing less and getting more) with an exposure to the market of only 41.95% compared to the 100% market exposure of the passive investment, and thus provides increased profitability with reduced risk.

Seven facets of this paper, analysed and brought into focus by AI.

The research has significant implications for investors and traders who seek to make informed decisions based on predictive models.

The research employed a combination of machine learning algorithms and technical analysis to predict stock prices.

The research has significant implications for investors and traders who seek to make informed decisions based on predictive models.

The proposed model contributes to the field of technical analysis by providing a new approach to predicting stock prices using machine learning algorithms.

The use of LSTM networks in this context is novel, as it has not been extensively explored in the field of technical analysis.

Discussion 0