We discuss stochastic modeling of volatility persistence and

anti-correlations in electricity spot prices, and for this purpose we present

two mean-reverting versions of the multifractal random walk (MRW). In the first

model the anti-correlations are modeled in the same way as in an

Ornstein-Uhlenbeck process, i.e. via a drift (damping) term, and in the second

model the anti-correlations are included by letting the innovations in the MRW

model be fractional Gaussian noise with H < 1/2. For both models we present

approximate maximum likelihood methods, and we apply these methods to estimate

the parameters for the spot prices in the Nordic electricity market. The

maximum likelihood estimates show that electricity spot prices are

characterized by scaling exponents that are significantly different from the

corresponding exponents in stock markets, confirming the exceptional nature of

the electricity market. In order to compare the damped MRW model with the

fractional MRW model we use ensemble simulations and wavelet-based variograms,

and we observe that certain features of the spot prices are better described by

the damped MRW model. The characteristic correlation time is estimated to

approximately half a year.

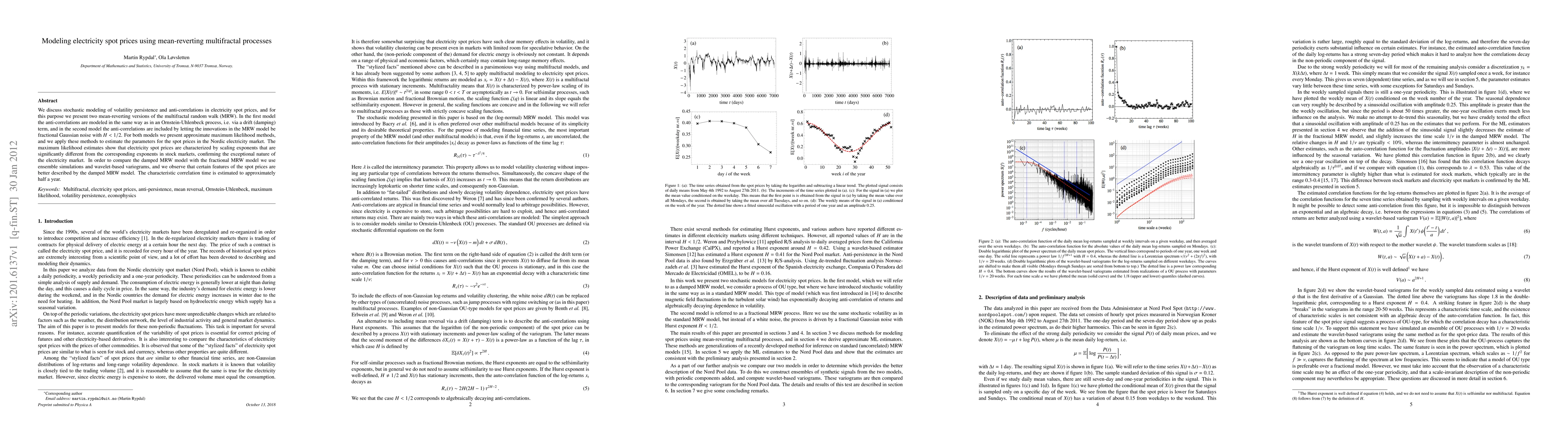

Discussion 0