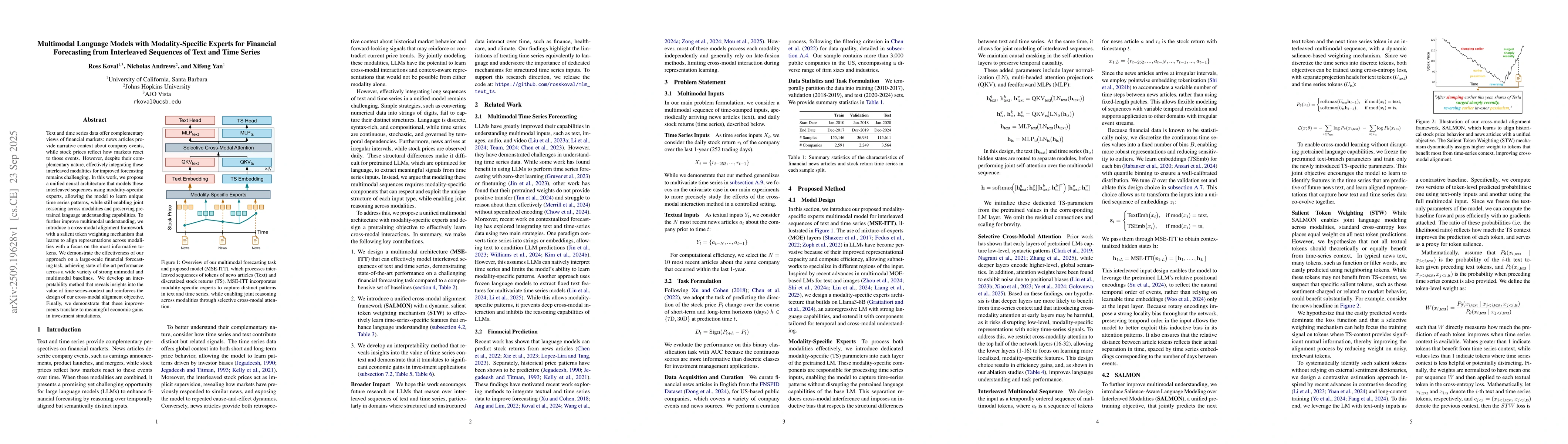

Text and time series data offer complementary views of financial markets:

news articles provide narrative context about company events, while stock

prices reflect how markets react to those events. However, despite their

complementary nature, effectively integrating these interleaved modalities for

improved forecasting remains challenging. In this work, we propose a unified

neural architecture that models these interleaved sequences using

modality-specific experts, allowing the model to learn unique time series

patterns, while still enabling joint reasoning across modalities and preserving

pretrained language understanding capabilities. To further improve multimodal

understanding, we introduce a cross-modal alignment framework with a salient

token weighting mechanism that learns to align representations across

modalities with a focus on the most informative tokens. We demonstrate the

effectiveness of our approach on a large-scale financial forecasting task,

achieving state-of-the-art performance across a wide variety of strong unimodal

and multimodal baselines. We develop an interpretability method that reveals

insights into the value of time series-context and reinforces the design of our

cross-modal alignment objective. Finally, we demonstrate that these

improvements translate to meaningful economic gains in investment simulations.

Discussion 0