Authors

Summary

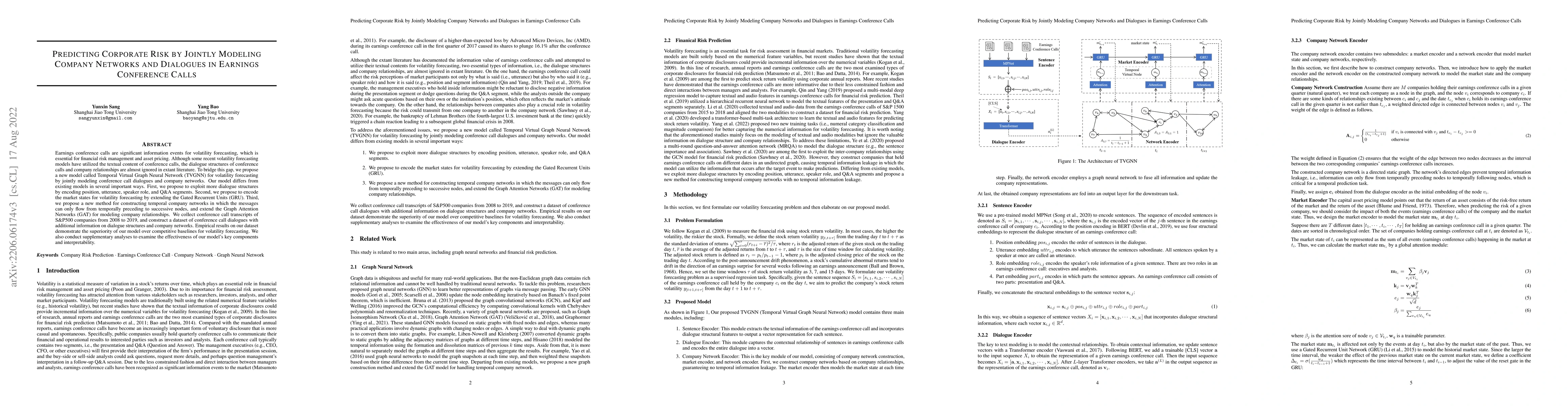

Earnings conference calls are significant information events for volatility forecasting, which is essential for financial risk management and asset pricing. Although some recent volatility forecasting models have utilized the textual content of conference calls, the dialogue structures of conference calls and company relationships are almost ignored in extant literature. To bridge this gap, we propose a new model called Temporal Virtual Graph Neural Network (TVGNN) for volatility forecasting by jointly modeling conference call dialogues and company networks. Our model differs from existing models in several important ways. First, we propose to exploit more dialogue structures by encoding position, utterance, speaker role, and Q\&A segments. Second, we propose to encode the market states for volatility forecasting by extending the Gated Recurrent Units (GRU). Third, we propose a new method for constructing temporal company networks in which the messages can only flow from temporally preceding to successive nodes, and extend the Graph Attention Networks (GAT) for modeling company relationships. We collect conference call transcripts of S\&P500 companies from 2008 to 2019, and construct a dataset of conference call dialogues with additional information on dialogue structures and company networks. Empirical results on our dataset demonstrate the superiority of our model over competitive baselines for volatility forecasting. We also conduct supplementary analyses to examine the effectiveness of our model's key components and interpretability.

AI Key Findings

Generated Sep 07, 2025

Methodology

The research proposes a model called TVGNN for volatility forecasting by jointly modeling conference call dialogues and company networks. It constructs company networks and develops a graph neural network model to learn from conference calls, market state, and company networks.

Key Results

- TVGNN outperforms competitive baseline models in company risk prediction tasks for three time windows (τ=3, 7, 15).

- TVGNN improves MSE by 13.26% compared to the best baseline model HTML, demonstrating its effectiveness.

Significance

This research is significant as it contributes to financial risk management and asset pricing by improving volatility forecasting using conference call textual content and company network structures.

Technical Contribution

The paper introduces a novel method for constructing company networks and a new graph neural network model (TVGNN) for jointly modeling conference call dialogues and company networks.

Novelty

The research bridges the gap in extant literature by considering dialogue structures and company relationships in volatility forecasting models, proposing TVGNN that outperforms existing models.

Limitations

- The study does not explore the impact of other financial reports or data sources on volatility forecasting.

- The model's performance may vary with different market conditions or economic environments not covered in the dataset.

Future Work

- Investigate the effect of incorporating additional financial data sources on model performance.

- Explore the model's applicability in different market conditions or economic environments.

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Similar Papers

Found 4 papersMiMIC: Multi-Modal Indian Earnings Calls Dataset to Predict Stock Prices

Sudip Kumar Naskar, Sohom Ghosh, Arnab Maji

| Title | Authors | Year | Actions |

|---|

Comments (0)