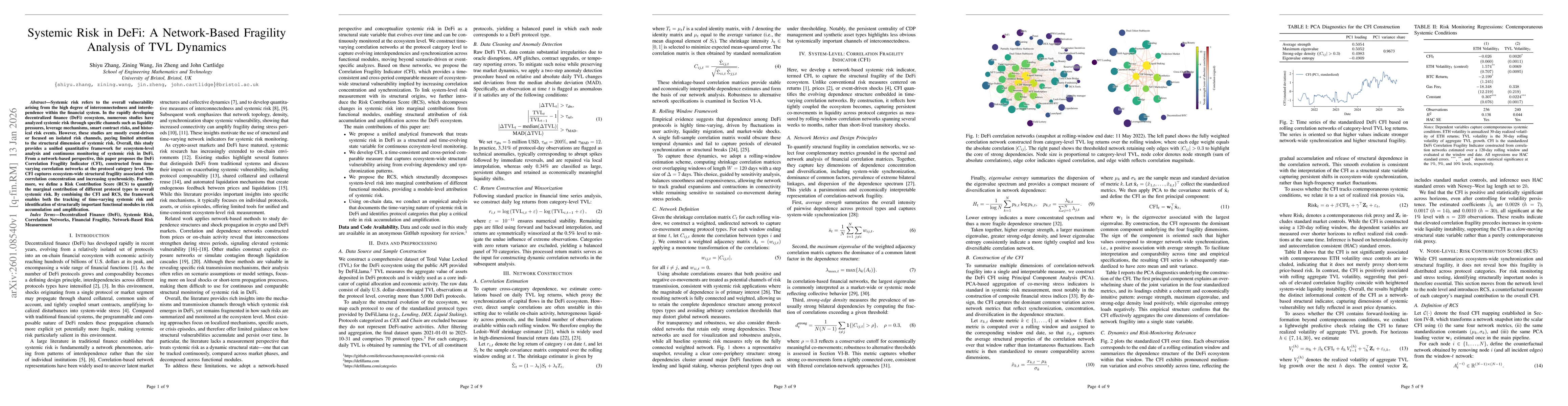

Systemic risk refers to the overall vulnerability arising from the high degree of interconnectedness and interdependence within the financial system. In the rapidly developing decentralized finance (DeFi) ecosystem, numerous studies have analyzed systemic risk through specific channels such as liquidity pressures, leverage mechanisms, smart contract risks, and historical risk events. However, these studies are mostly event-driven or focused on isolated risk channels, paying limited attention to the structural dimension of systemic risk. Overall, this study provides a unified quantitative framework for ecosystem-level analysis and continuous monitoring of systemic risk in DeFi. From a network-based perspective, this paper proposes the DeFi Correlation Fragility Indicator (CFI), constructed from time-varying correlation networks at the protocol category level. The CFI captures ecosystem-wide structural fragility associated with correlation concentration and increasing synchronicity. Furthermore, we define a Risk Contribution Score (RCS) to quantify the marginal contribution of different protocol types to overall systemic risk. By combining the CFI and RCS, the framework enables both the tracking of time-varying systemic risk and identification of structurally important functional modules in risk accumulation and amplification.

Discussion 0