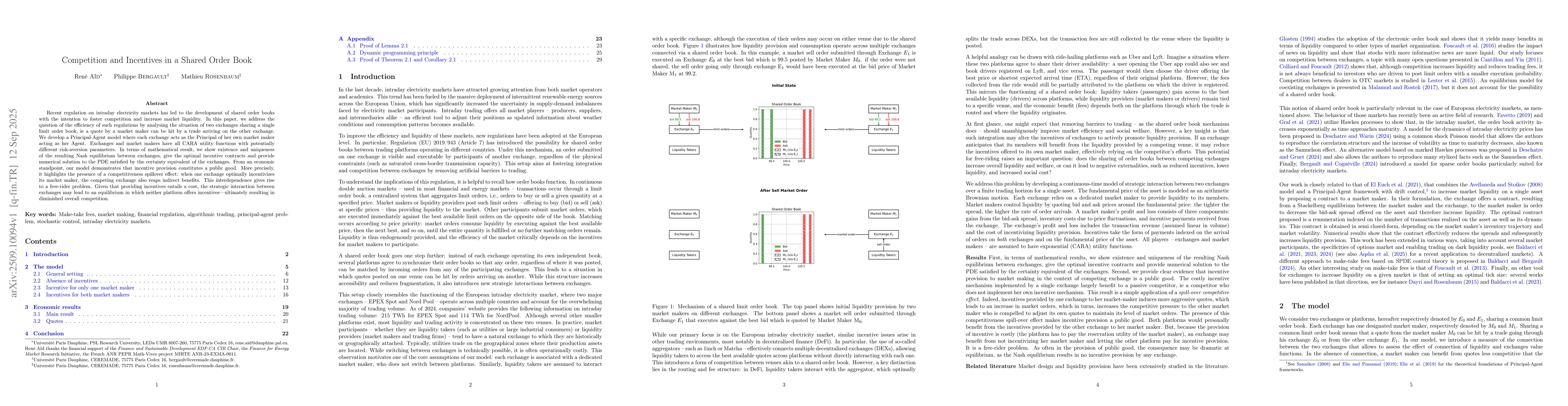

Recent regulation on intraday electricity markets has led to the development

of shared order books with the intention to foster competition and increase

market liquidity. In this paper, we address the question of the efficiency of

such regulations by analysing the situation of two exchanges sharing a single

limit order book, i.e. a quote by a market maker can be hit by a trade arriving

on the other exchange. We develop a Principal-Agent model where each exchange

acts as the Principal of her own market maker acting as her Agent. Exchanges

and market makers have all CARA utility functions with potentially different

risk-aversion parameters. In terms of mathematical result, we show existence

and uniqueness of the resulting Nash equilibrium between exchanges, give the

optimal incentive contracts and provide numerical solution to the PDE satisfied

by the certainty equivalent of the exchanges. From an economic standpoint, our

model demonstrates that incentive provision constitutes a public good. More

precisely, it highlights the presence of a competitiveness spillover effect:

when one exchange optimally incentivizes its market maker, the competing

exchange also reaps indirect benefits. This interdependence gives rise to a

free-rider problem. Given that providing incentives entails a cost, the

strategic interaction between exchanges may lead to an equilibrium in which

neither platform offers incentives -- ultimately resulting in diminished

overall competition.

Discussion 0