Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper, we introduce a suite of models for price-aware automated market making platforms willing to optimize their quotes. These models incorporate advanced price dynamics, including stochast...

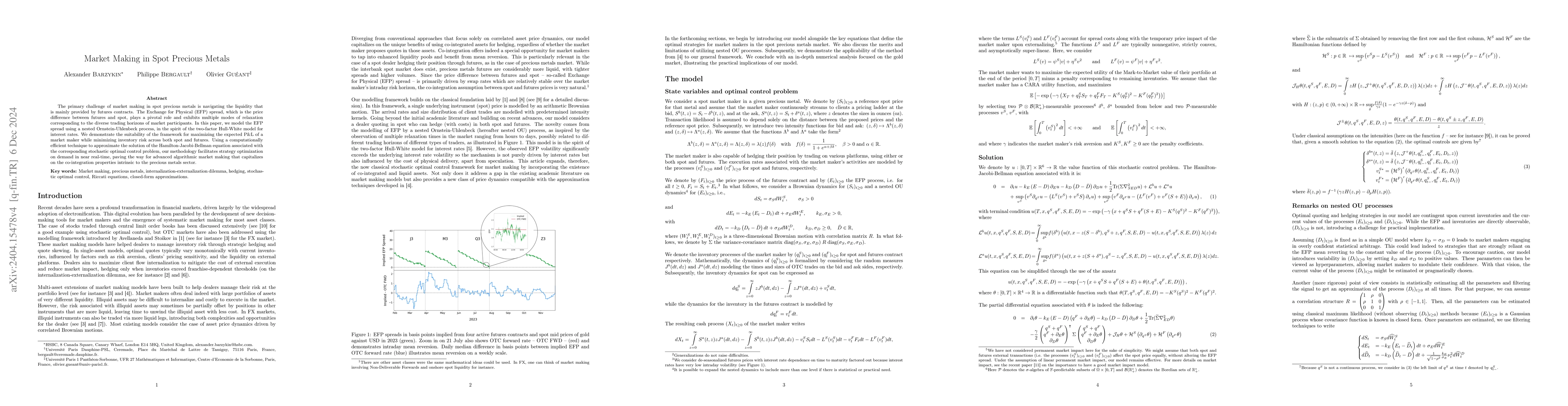

The primary challenge of market making in spot precious metals is navigating the liquidity that is mainly provided by futures contracts. The Exchange for Physical (EFP) spread, which is the price di...

This paper introduces a novel methodology for the pricing and management of share buyback contracts, overcoming the limitations of traditional optimal control methods, which frequently encounter dif...

We find closed-form solutions to the stochastic game between a broker and a mean-field of informed traders. In the finite player game, the informed traders observe a common signal and a private sign...

We investigate a stochastic differential game in which a major player has a private information (the knowledge of a random variable), which she discloses through her control to a population of small...

To assign a value to a portfolio, it is common to use Mark-to-Market prices. However, how should one proceed when the securities are illiquid? When transaction prices are scarce, how can one use all...

With the emergence of decentralized finance, new trading mechanisms called Automated Market Makers have appeared. The most popular Automated Market Makers are Constant Function Market Makers. They h...

In FX cash markets, market makers provide liquidity to clients for a wide variety of currency pairs. Because of flow uncertainty and market volatility, they face inventory risk. To mitigate this ris...

We design a market-making model \`a la Avellaneda-Stoikov in which the market-takers act strategically, in the sense that they design their trading strategy based on an exogenous trading signal. The...

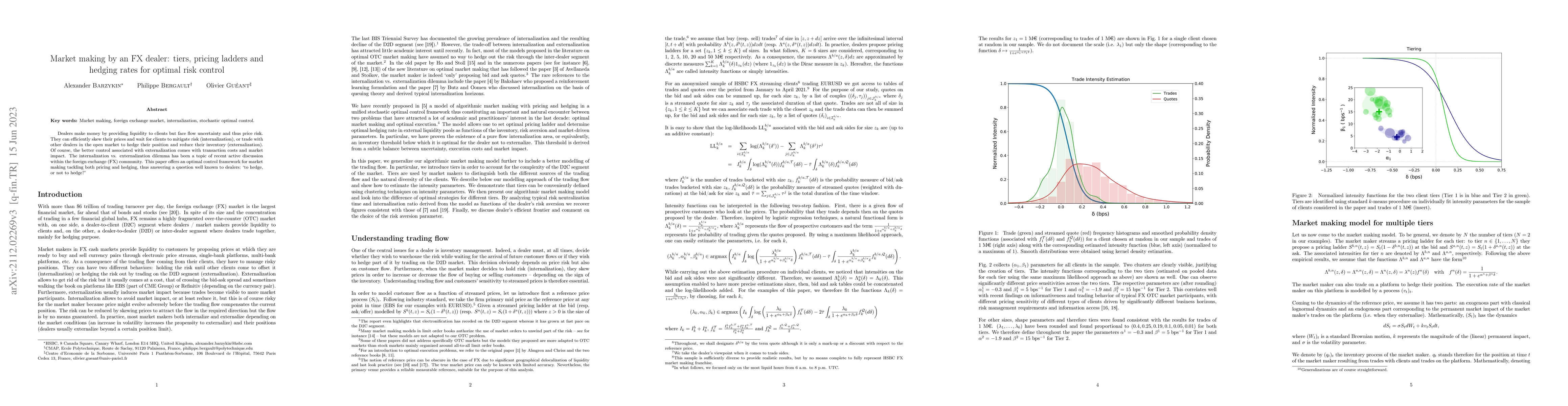

Dealers make money by providing liquidity to clients but face flow uncertainty and thus price risk. They can efficiently skew their prices and wait for clients to mitigate risk (internalization), or...

With the fragmentation of electronic markets, exchanges are now competing in order to attract trading activity on their platform. Consequently, they developed several regulatory tools to control liq...

In dealer markets, dealers provide prices at which they agree to buy and sell the assets and securities they have in their scope. With ever increasing trading volume, this quoting task has to be don...

In recent years, academics, regulators, and market practitioners have increasingly addressed liquidity issues. Amongst the numerous problems addressed, the optimal execution of large orders is proba...

The tick size, which is the smallest increment between two consecutive prices for a given asset, is a key parameter of market microstructure. In particular, the behavior of high frequency market mak...

In this article, we tackle the problem of a market maker in charge of a book of options on a single liquid underlying asset. By using an approximation of the portfolio in terms of its vega, we show ...

In most OTC markets, a small number of market makers provide liquidity to other market participants. More precisely, for a list of assets, they set prices at which they agree to buy and sell. Market...

A large proportion of market making models derive from the seminal model of Avellaneda and Stoikov. The numerical approximation of the value function and the optimal quotes in these models remains a...

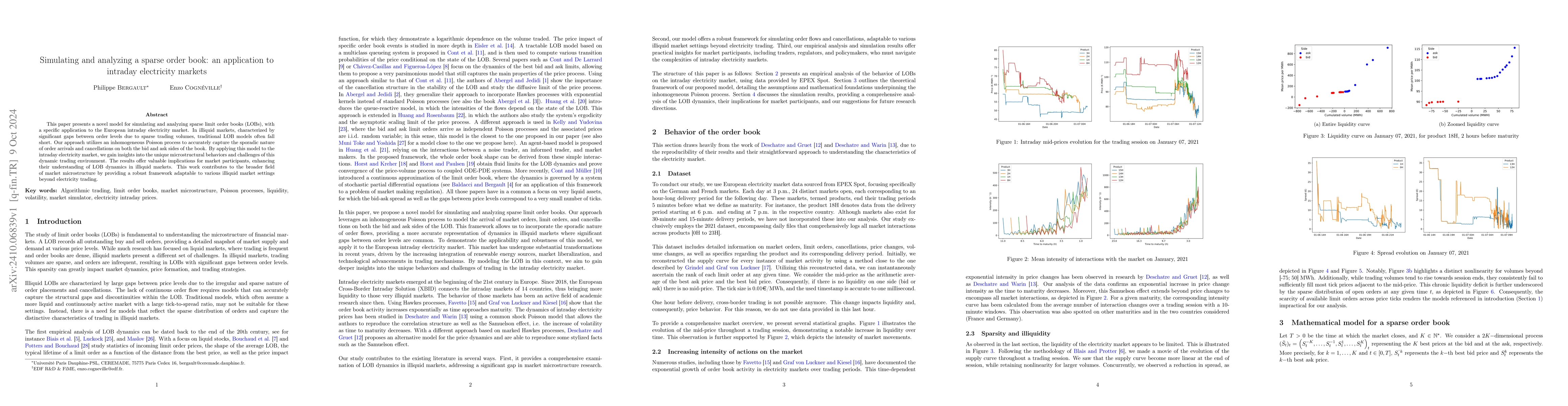

This paper presents a novel model for simulating and analyzing sparse limit order books (LOBs), with a specific application to the European intraday electricity market. In illiquid markets, characteri...

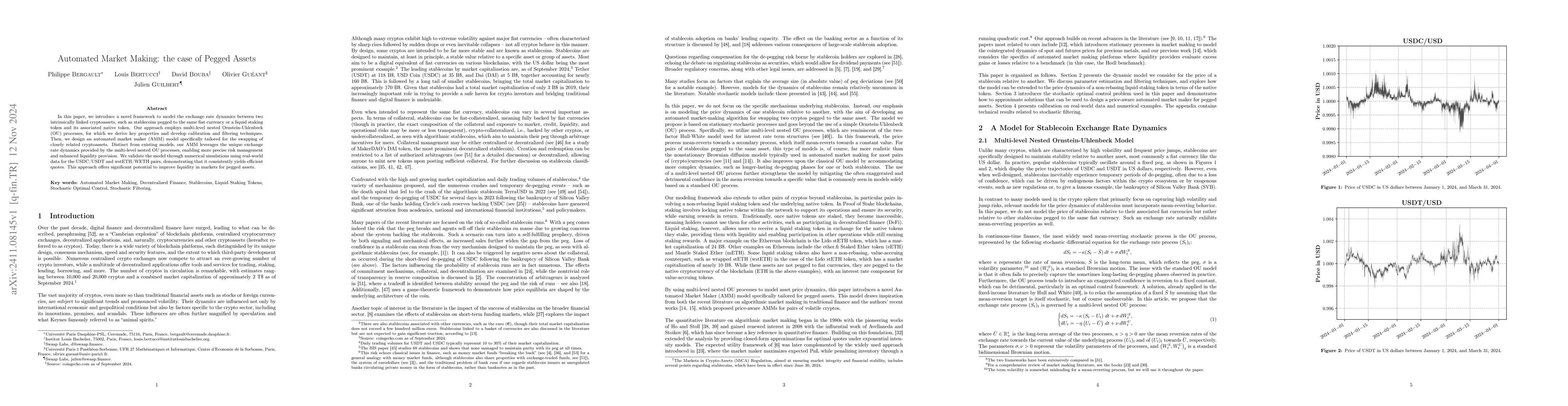

In this paper, we introduce a novel framework to model the exchange rate dynamics between two intrinsically linked cryptoassets, such as stablecoins pegged to the same fiat currency or a liquid stakin...

This paper addresses the trade-off between internalisation and externalisation in the management of stochastic trade flows. We consider agents who must absorb flows and manage risk by deciding whether...

We find the equilibrium contract that an automated market maker (AMM) offers to their strategic liquidity providers (LPs) in order to maximize the order flow that gets processed by the venue. Our mode...

This paper investigates the optimal hedging strategies of an informed broker interacting with multiple traders in a financial market. We develop a theoretical framework in which the broker, possessing...

Passive liquidity providers (LPs) in automated market makers (AMMs) face losses due to adverse selection (LVR), which static trading fees often fail to offset in practice. We study the key determinant...

In traditional financial markets, yield curves are widely available for countries (and, by extension, currencies), financial institutions, and large corporates. These curves are used to calibrate stoc...

Over the past decade, many dealers have implemented algorithmic models to automatically respond to RFQs and manage flows originating from their electronic platforms. In parallel, building on the found...

We study the problem of optimal liquidity withdrawal for a representative liquidity provider (LP) in an automated market maker (AMM). LPs earn fees from trading activity but are exposed to impermanent...

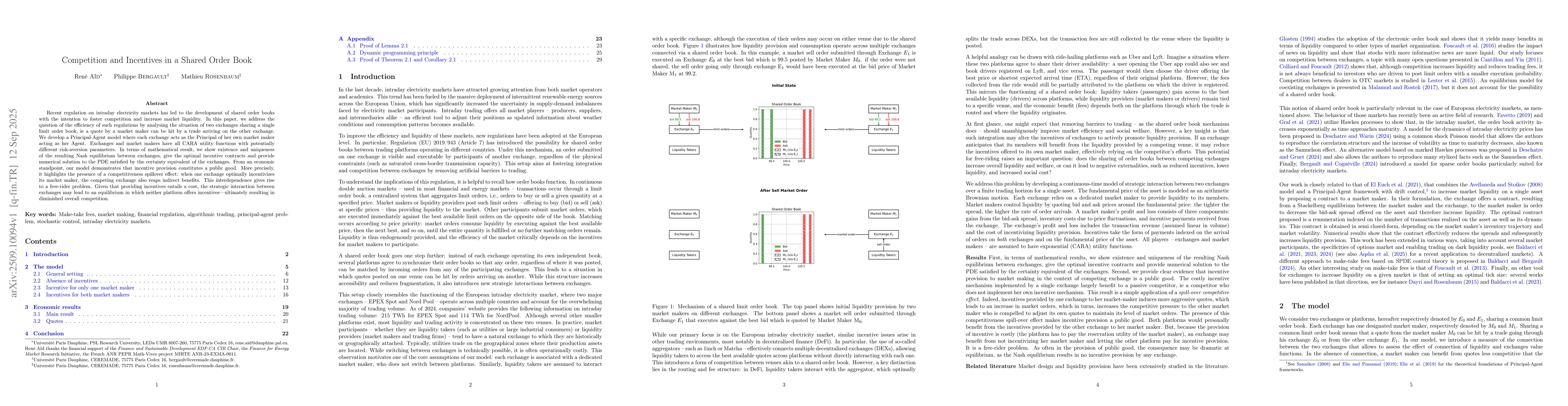

Recent regulation on intraday electricity markets has led to the development of shared order books with the intention to foster competition and increase market liquidity. In this paper, we address the...

We develop a mixed control framework that combines absolutely continuous controls with impulse interventions subject to stochastic execution delays. The model extends current impulse control formulati...