01

MethodologyHow they did it

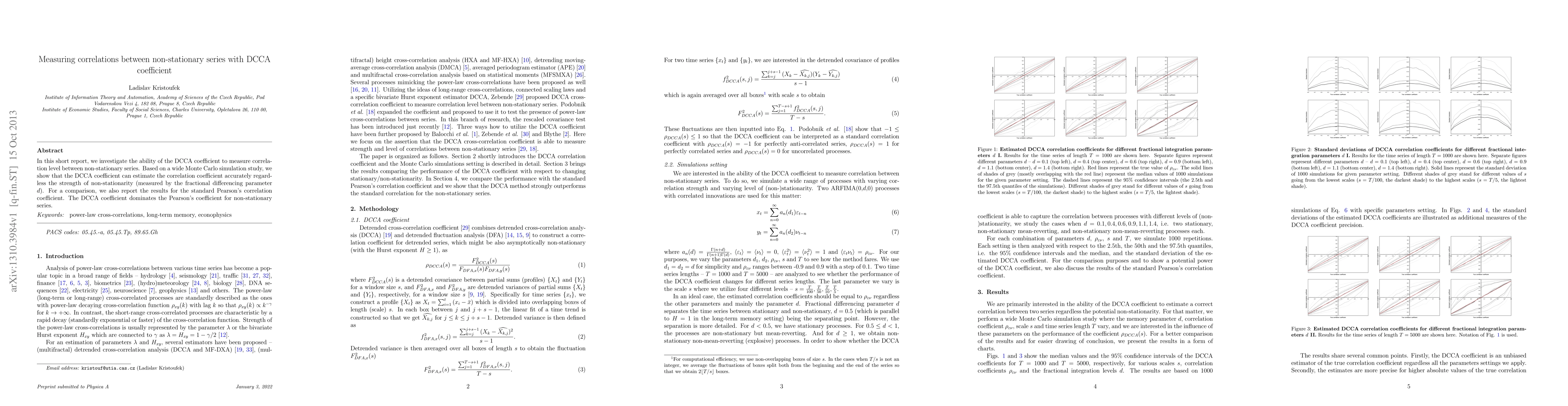

The research employs a Monte Carlo simulation study to evaluate the DCCA coefficient's performance in measuring correlation between non-stationary series, varying parameters such as memory (d), correlation coefficient (ρεν), scales (s), and time series length (T).

Discussion 0