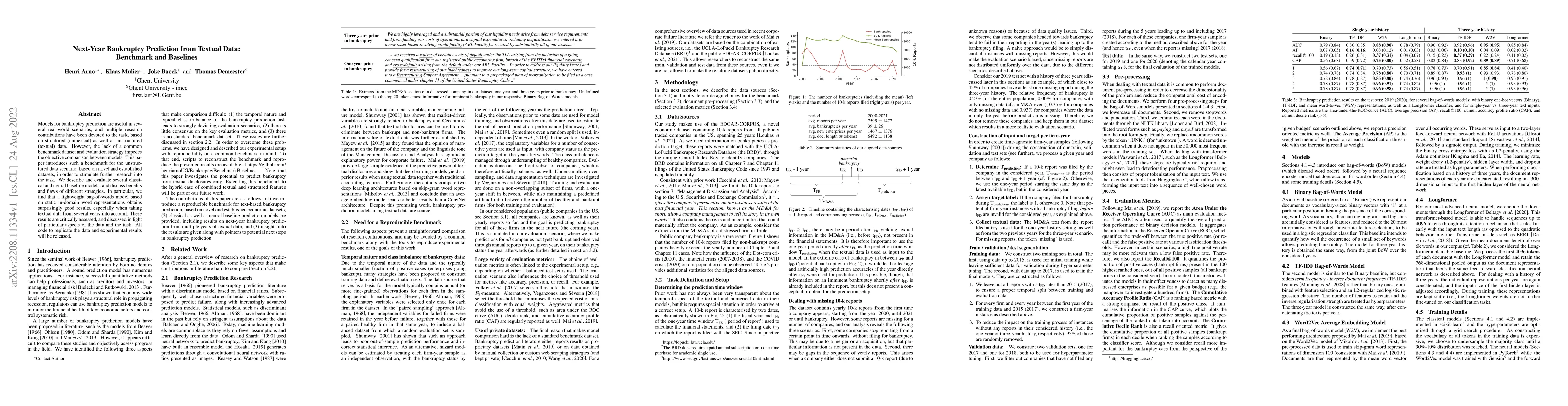

Models for bankruptcy prediction are useful in several real-world scenarios,

and multiple research contributions have been devoted to the task, based on

structured (numerical) as well as unstructured (textual) data. However, the

lack of a common benchmark dataset and evaluation strategy impedes the

objective comparison between models. This paper introduces such a benchmark for

the unstructured data scenario, based on novel and established datasets, in

order to stimulate further research into the task. We describe and evaluate

several classical and neural baseline models, and discuss benefits and flaws of

different strategies. In particular, we find that a lightweight bag-of-words

model based on static in-domain word representations obtains surprisingly good

results, especially when taking textual data from several years into account.

These results are critically assessed, and discussed in light of particular

aspects of the data and the task. All code to replicate the data and

experimental results will be released.

Discussion 0