Publication

Metrics

AI Quick Summary

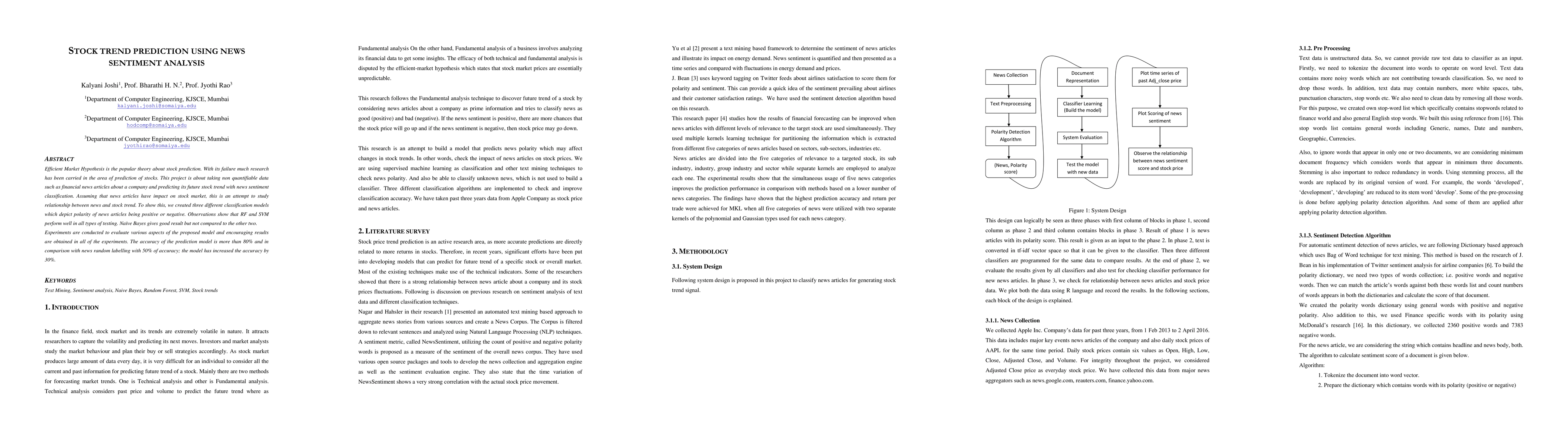

This research explores stock trend prediction using sentiment analysis of financial news articles. The study employs three classification models to determine the polarity of news articles and their impact on stock trends, finding that Random Forest and Support Vector Machines outperform Naive Bayes, achieving over 80% accuracy compared to a 50% accuracy of random labeling.

Paper Preview

Abstract

Efficient Market Hypothesis is the popular theory about stock prediction. With its failure much research has been carried in the area of prediction of stocks. This project is about taking non quantifiable data such as financial news articles about a company and predicting its future stock trend with news sentiment classification. Assuming that news articles have impact on stock market, this is an attempt to study relationship between news and stock trend. To show this, we created three different classification models which depict polarity of news articles being positive or negative. Observations show that RF and SVM perform well in all types of testing. Na\"ive Bayes gives good result but not compared to the other two. Experiments are conducted to evaluate various aspects of the proposed model and encouraging results are obtained in all of the experiments. The accuracy of the prediction model is more than 80% and in comparison with news random labeling with 50% of accuracy; the model has increased the accuracy by 30%.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0