Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper is devoted to obtaining a wellposedness result for multidimensional BSDEs with possibly unbounded random time horizon and driven by a general martingale in a filtration only assumed to sa...

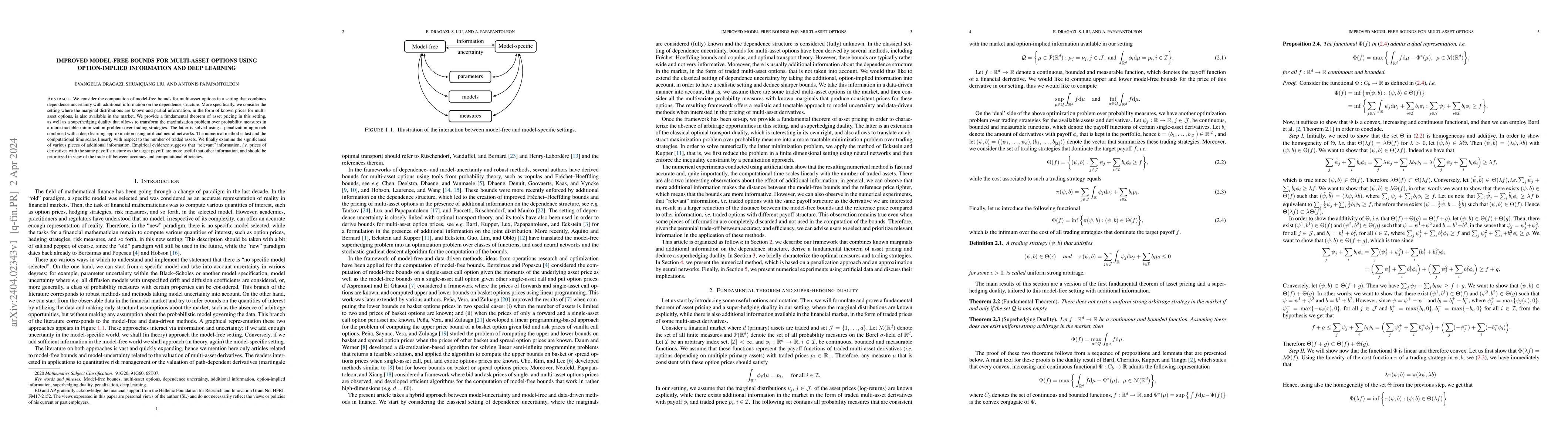

We consider the computation of model-free bounds for multi-asset options in a setting that combines dependence uncertainty with additional information on the dependence structure. More specifically,...

Efficiently pricing multi-asset options poses a significant challenge in quantitative finance. The Monte Carlo (MC) method remains the prevalent choice for pricing engines; however, its slow converg...

We develop a novel deep learning approach for pricing European options in diffusion models, that can efficiently handle high-dimensional problems resulting from Markovian approximations of rough vol...

We consider L\'evy processes that are approximated by compound Poisson processes and, correspondingly, BSDEs driven by L\'evy processes that are approximated by BSDEs driven by their compound Poisso...

We develop a novel deep learning approach for pricing European basket options written on assets that follow jump-diffusion dynamics. The option pricing problem is formulated as a partial integro-dif...

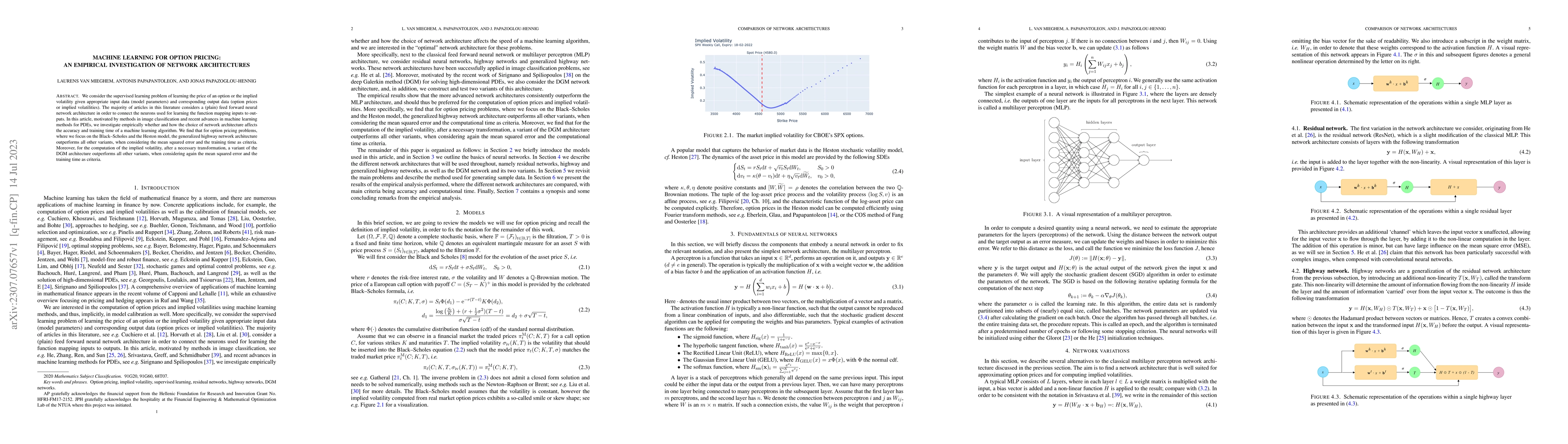

We consider the supervised learning problem of learning the price of an option or the implied volatility given appropriate input data (model parameters) and corresponding output data (option prices ...

In this paper, we obtain stability results for backward stochastic differential equations with jumps (BSDEs) in a very general framework. More specifically, we consider a convergent sequence of stan...

We consider derivatives written on multiple underlyings in a one-period financial market, and we are interested in the computation of model-free upper and lower bounds for their arbitrage-free price...

We are interested in the existence of equivalent martingale measures and the detection of arbitrage opportunities in markets where several multi-asset derivatives are traded simultaneously. More spe...

In this paper, we obtain stability results for martingale representations in a very general framework. More specifically, we consider a sequence of martingales each adapted to its own filtration, an...

We consider backward stochastic differential equations (BSDEs) with mean-field and McKean-Vlasov interactions in their generators in a general setting, where the drivers are square-integrable martinga...

The purpose of the present paper is to introduce and establish a notion of stability for the backward propagation of chaos, with respect to (initial) data sets. Consider, for example, a sequence of di...

The aim of this article is to provide a firm mathematical foundation for the application of deep gradient flow methods (DGFMs) for the solution of (high-dimensional) partial differential equations (PD...