Academic Profile

Statistics

Similar Authors

Papers on arXiv

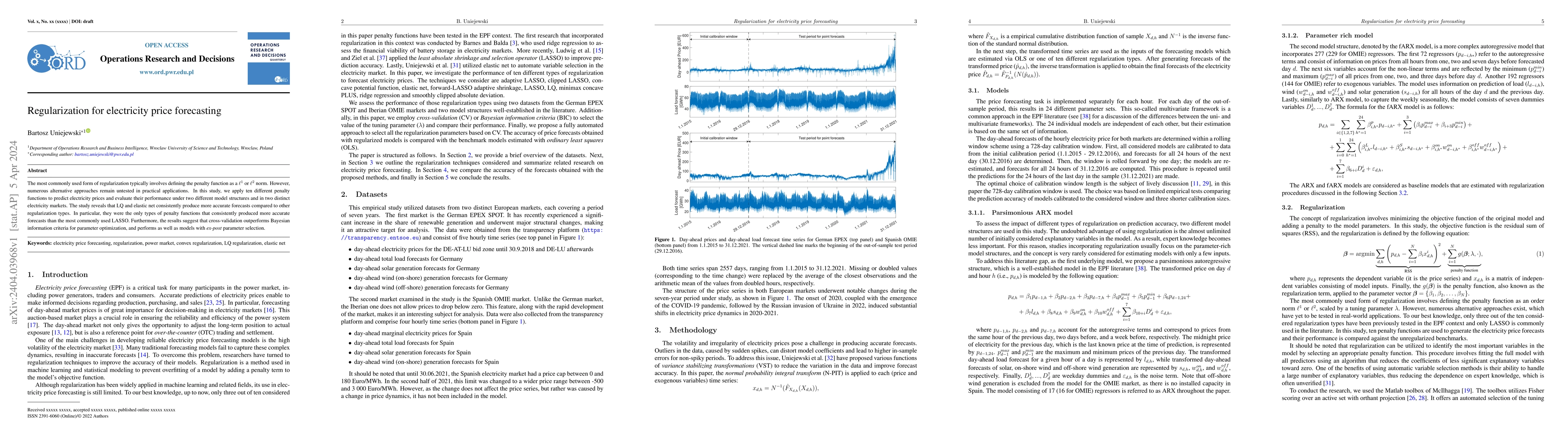

The most commonly used form of regularization typically involves defining the penalty function as a L1 or L2 norm. However, numerous alternative approaches remain untested in practical applications....

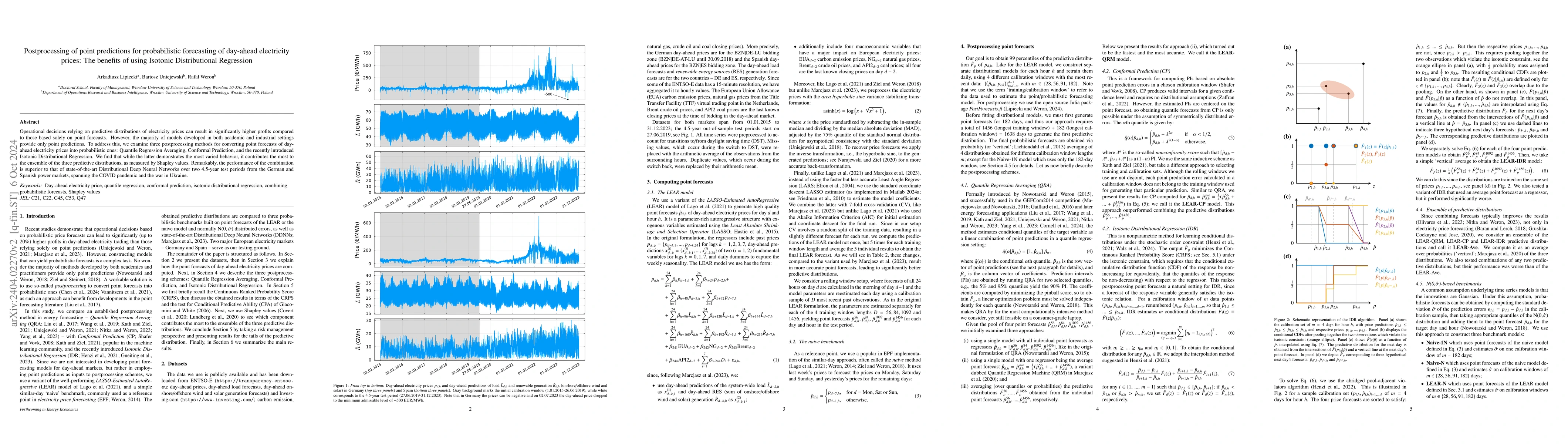

Operational decisions relying on predictive distributions of electricity prices can result in significantly higher profits compared to those based solely on point forecasts. However, the majority of...

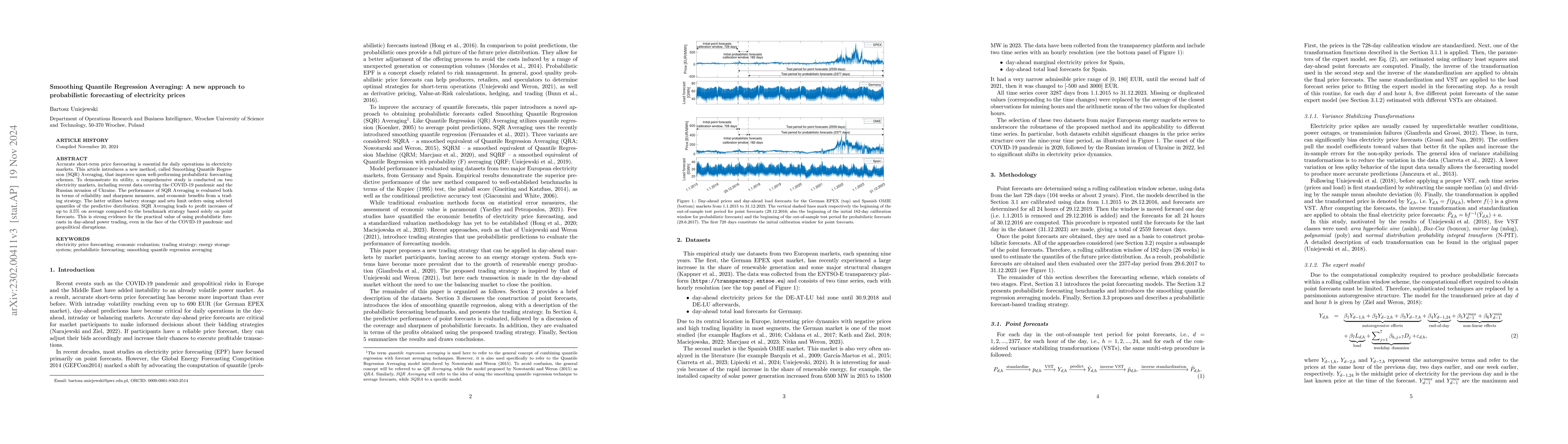

In the world of the complex power market, accurate electricity price forecasting is essential for strategic bidding and affects both daily operations and long-term investments. This article introduc...

This paper develops a novel, fully automated forecast averaging scheme, which combines LASSO estimation method with Principal Component Averaging (PCA). LASSO-PCA (LPCA) explores a pool of predictio...

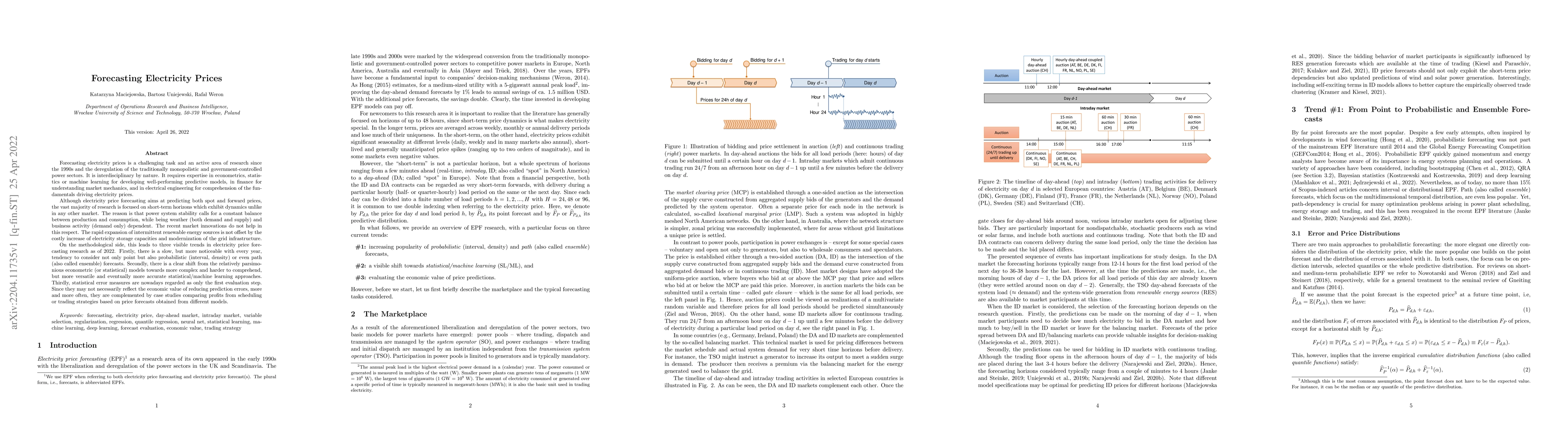

Forecasting electricity prices is a challenging task and an active area of research since the 1990s and the deregulation of the traditionally monopolistic and government-controlled power sectors. Al...

In this study, we introduced various statistical performance metrics, based on the pinball loss and the empirical coverage, for the ranking of probabilistic forecasting models. We tested the ability o...

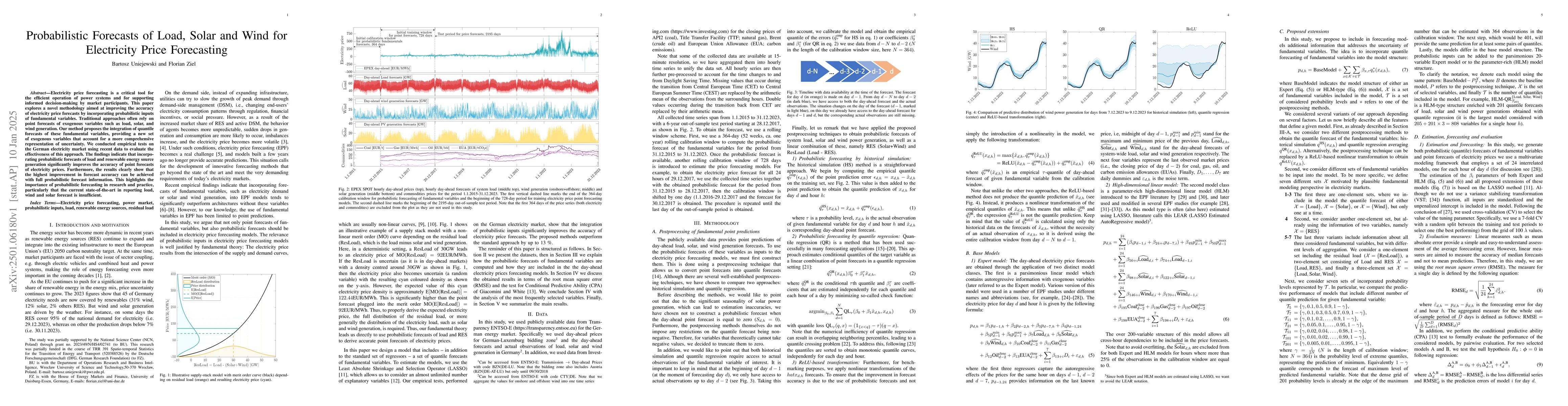

Electricity price forecasting is a critical tool for the efficient operation of power systems and for supporting informed decision-making by market participants. This paper explores a novel methodolog...

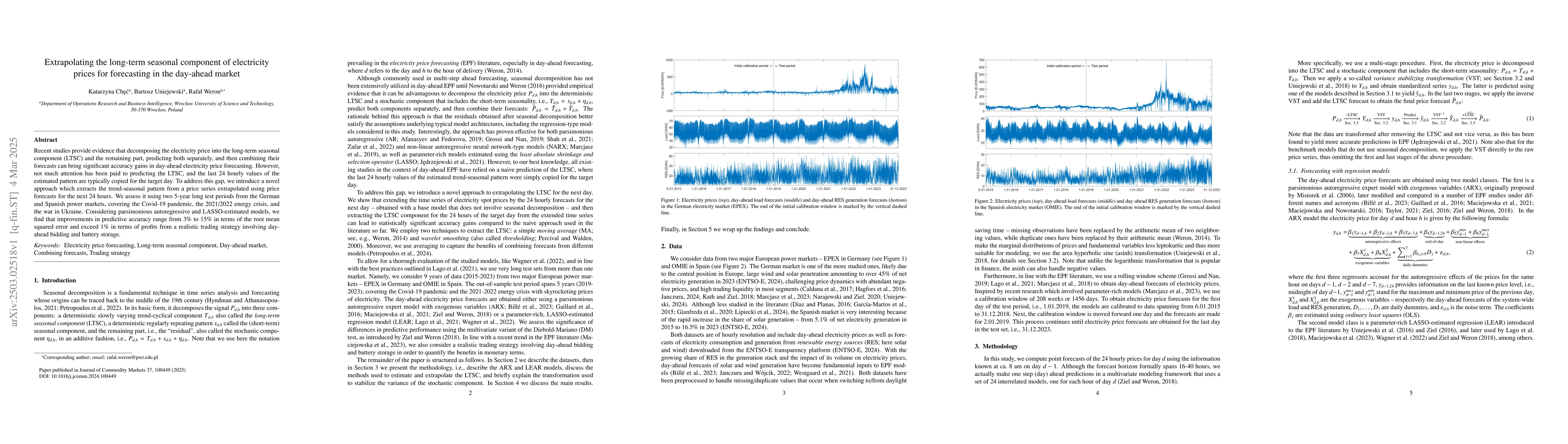

Recent studies provide evidence that decomposing the electricity price into the long-term seasonal component (LTSC) and the remaining part, predicting both separately, and then combining their forecas...

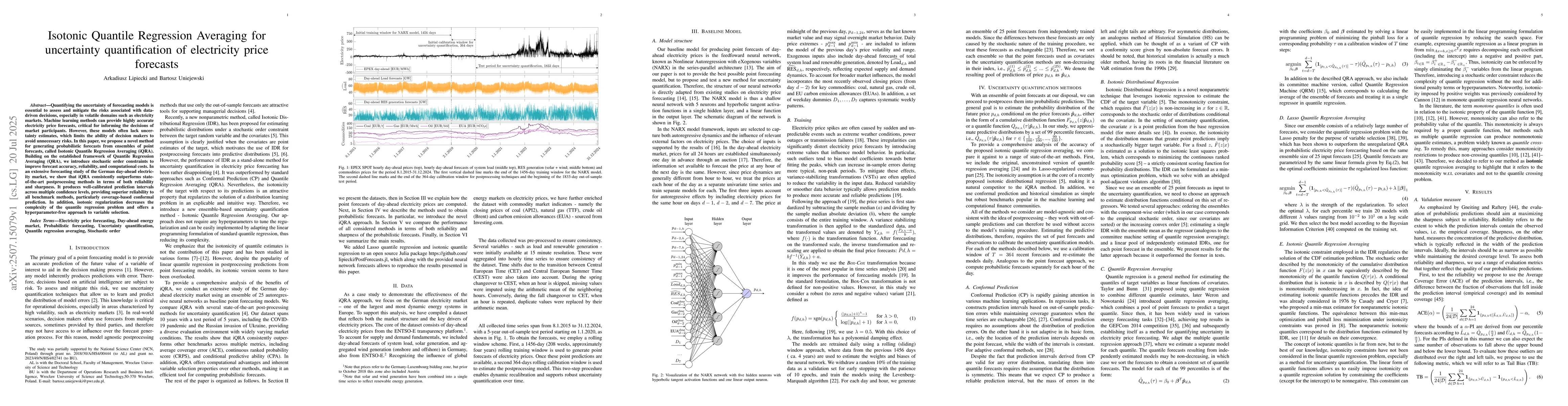

Quantifying the uncertainty of forecasting models is essential to assess and mitigate the risks associated with data-driven decisions, especially in volatile domains such as electricity markets. Machi...

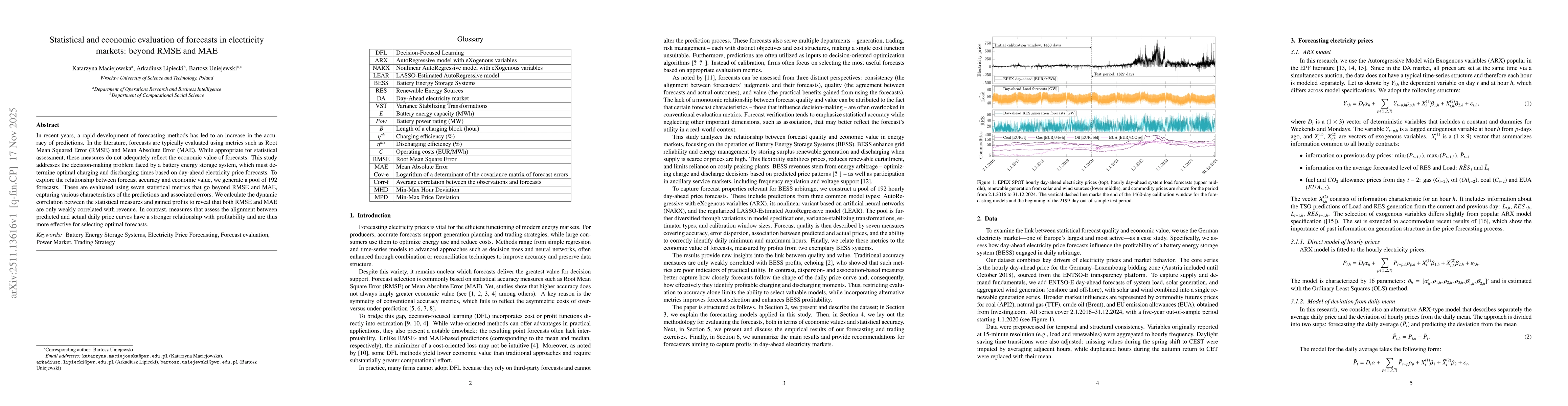

In recent years, a rapid development of forecasting methods has led to an increase in the accuracy of predictions. In the literature, forecasts are typically evaluated using metrics such as Root Mean ...

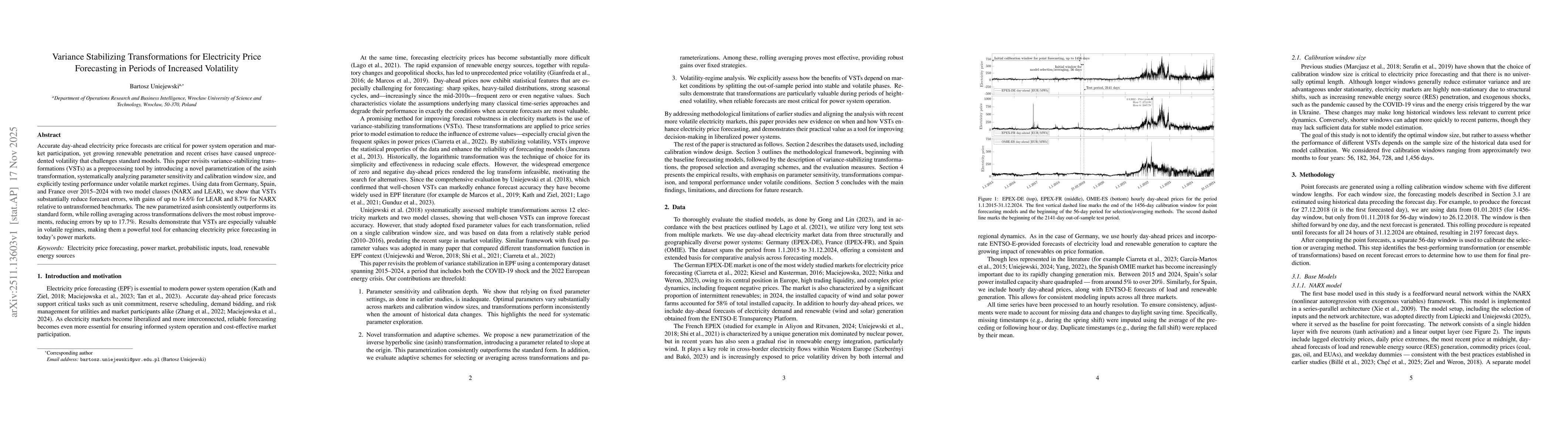

Accurate day-ahead electricity price forecasts are critical for power system operation and market participation, yet growing renewable penetration and recent crises have caused unprecedented volatilit...