Academic Profile

Statistics

Similar Authors

Papers on arXiv

We revisit the dividend payment problem in the dual model of Avanzi et al. ([2], [1], and [3]). Using the fluctuation theory of spectrally positive L\'{e}vy processes, we give a short exposition in ...

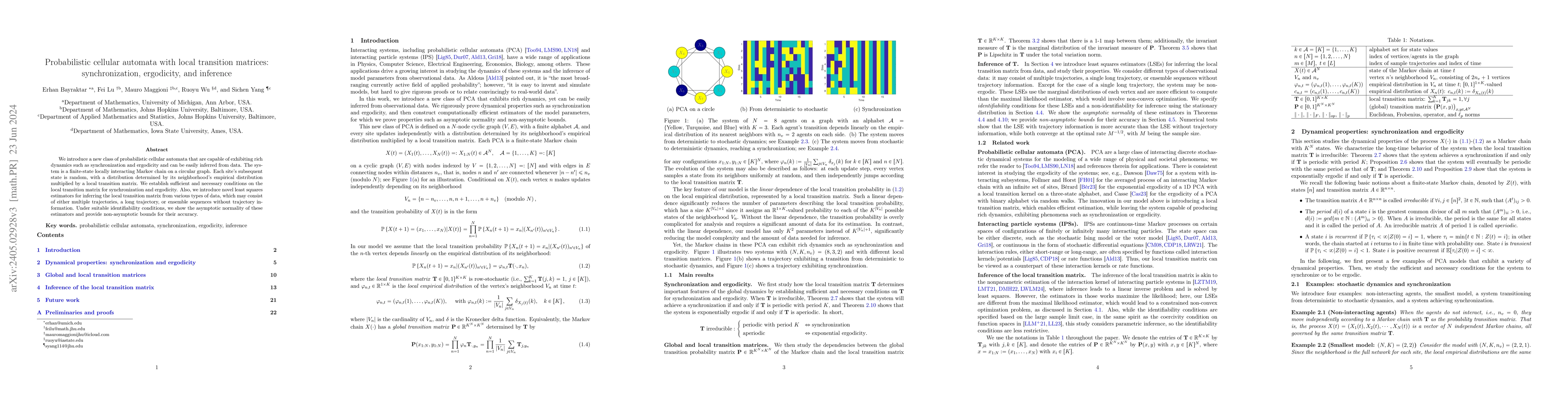

We introduce a new class of probabilistic cellular automata that are capable of exhibiting rich dynamics such as synchronization and ergodicity and can be easily inferred from data. The system is a ...

We investigate the behavior of liquidity providers (LPs) by modeling a decentralized cryptocurrency exchange (DEX) based on Uniswap v3. LPs with heterogeneous characteristics choose optimal liquidit...

We consider the graphon mean-field system introduced in the work of Bayraktar, Chakraborty, and Wu. It is the large-population limit of a heterogeneously interacting diffusive particle system, where...

For time-inconsistent stopping in a one-dimensional diffusion setup, we investigate how to use discrete-time models to approximate the original problem. In particular, we consider the value function...

Martingale optimal transport (MOT) often yields broad price bounds for options, constraining their practical applicability. In this study, we extend MOT by incorporating causality constraints among ...

We investigate an infinite-horizon time-inconsistent mean-field game (MFG) in a discrete time setting. We first present a classic equilibrium for the MFG and its associated existence result. This cl...

We study mean-field control problems in discrete-time under the infinite horizon average cost optimality criteria. We focus on both the finite population and the infinite population setups. We show ...

We prove a comparison result for viscosity solutions of second order parabolic partial differential equations in the Wasserstein space. The comparison is valid for semisolutions that are Lipschitz c...

For time-inconsistent stochastic controls in discrete time and finite horizon, an open problem in Bj\"ork and Murgoci (Finance Stoch, 2014) is the existence of an equilibrium control. A nonrandomize...

This paper considers an infinite-horizon Markov decision process (MDP) that allows for general non-exponential discount functions, in both discrete and continuous time. Due to the inherent time inco...

We develop a fitted value iteration (FVI) method to compute bicausal optimal transport (OT) where couplings have an adapted structure. Based on the dynamic programming formulation, FVI adopts a func...

We study a stochastic control/stopping problem with a series of inequality-type and equality-type expectation constraints in a general non-Markovian framework. We demonstrate that the stochastic con...

In this paper, we develop the theory of functional generation of portfolios in an equity market with changing dimension. By introducing dimensional jumps in the market, as well as jumps in stock cap...

Given two probability measures on sequential data, we investigate the transport problem with time-inconsistent preferences under a discrete-time setting. Motivating examples are nonlinear objectives...

We explicitly construct the supermartingale version of the Fr{\'e}chet-Hoeffding coupling in the setting with infinitely many marginal constraints. This extends the results of Henry-Labordere et al....

This paper is concerned with the problem of budget control in a large particle system modeled by stochastic differential equations involving hitting times, which arises from considerations of system...

This paper studies an equity market of stochastic dimension, where the number of assets fluctuates over time. In such a market, we develop the fundamental theorem of asset pricing, which provides th...

We study stability and sample complexity properties of divergence regularized optimal transport (DOT). First, we obtain quantitative stability results for optimizers of DOT measured in Wasserstein d...

In this work, we study the deep signature algorithms for path-dependent options. We extend the backward scheme in [Hur\'e-Pham-Warin. Mathematics of Computation 89, no. 324 (2020)] for state-depende...

We study a multi-agent mean field type control problem in discrete time where the agents aim to find a socially optimal strategy and where the state and action spaces for the agents are assumed to b...

We develop a backward-in-time machine learning algorithm that uses a sequence of neural networks to solve optimal switching problems in energy production, where electricity and fossil fuel prices ar...

In this note, we provide a smooth variational principle on Wasserstein space by constructing a smooth gauge-type function using the sliced Wasserstein distance. This function is a crucial tool for o...

We consider a multi-period stochastic control problem where the multivariate driving stochastic factor of the system has known marginal distributions but uncertain dependence structure. To solve the...

In this paper, we consider the problem of a Principal aiming at designing a reward function for a population of heterogeneous agents. We construct an incentive based on the ranking of the agents, so...

In this paper, we study a learning problem in which a forecaster only observes partial information. By properly rescaling the problem, we heuristically derive a limiting PDE on Wasserstein space whi...

For two measures $\mu$ and $\nu$ that are in convex-decreasing order, Nutz and Stebegg (Canonical supermartingale couplings, Ann. Probab., 46(6):3351--3398, 2018) studied the optimal transport probl...

We investigate the stability of the equilibrium-induced optimal value in one-dimensional diffusion setting for a time-inconsistent stopping problem under non-exponential discounting. We show that th...

We investigate the stability of equilibrium-induced optimal values with respect to (w.r.t.) reward functions $f$ and transition kernels $Q$ for time-inconsistent stopping problems under nonexponenti...

We study heterogeneously interacting diffusive particle systems with mean-field type interaction characterized by an underlying graphon and their finite particle approximations. Under suitable condi...

We study long-time dynamical behaviors of weakly self-consistent Vlasov-Fokker-Planck equations. We introduce Hessian matrix conditions on mean-field kernel functions, which characterizes the expone...

Inspired by allocation strategies in multi-armed bandit model, we propose a pathwise construction of Walsh diffusions. For any infinitesimal generator on a star shaped graph, there exists a unique t...

We study a Q learning algorithm for continuous time stochastic control problems. The proposed algorithm uses the sampled state process by discretizing the state and control action spaces under piece...

We consider a discrete time stochastic Markovian control problem under model uncertainty. Such uncertainty not only comes from the fact that the true probability law of the underlying stochastic pro...

In this paper, we study graphon mean field games using a system of forward-backward stochastic differential equations. We establish the existence and uniqueness of solutions under two different assu...

We consider three equilibrium concepts proposed in the literature for time-inconsistent stopping problems, including mild equilibria, weak equilibria and strong equilibria. The discount function is ...

We consider a jump-diffusion mean field control problem with regime switching in the state dynamics. The corresponding value function is characterized as the unique viscosity solution of a HJB maste...

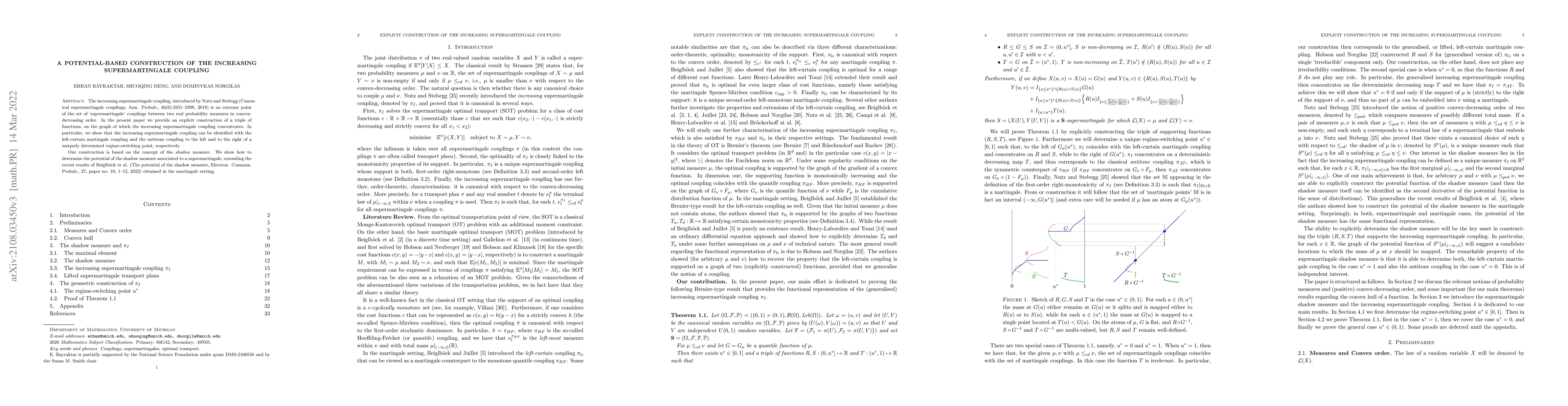

The increasing supermartingale coupling, introduced by Nutz and Stebegg (Canonical supermartingale couplings, Annals of Probability, 46(6):3351--3398, 2018) is an extreme point of the set of `superm...

In this paper, we consider graphon particle systems with heterogeneous mean-field type interactions and the associated finite particle approximations. Under suitable growth (resp. convexity) assumpt...

We consider bootstrap percolation and diffusion in sparse random graphs with fixed degrees, constructed by configuration model. Every node has two states: it is either active or inactive. We assume ...

In this paper, we show existence and uniqueness of solutions of the infinite horizon McKean-Vlasov FBSDEs using two different methods, which lead to two different sets of assumptions. We use these r...

We formulate an infinite-horizon optimal investment and consumption problem, in which an individual forms a habit based on the exponentially weighted average of her past consumption rate, and in whi...

The non-exponential Schilder-type theorem in Backhoff-Veraguas, Lacker and Tangpi [Ann. Appl. Probab., 30 (2020), pp. 1321-1367] is expressed as a convergence result for path-dependent partial diffe...

We determine the size of $k$-core in a large class of dense graph sequences. Let $G_n$ be a sequence of undirected, $n$-vertex graphs with edge weights $\{a^n_{i,j}\}_{i,j \in [n]}$ that converges t...

Forcing finite state mean field games by a relevant form of common noise is a subtle issue, which has been addressed only recently. Among others, one possible way is to subject the simplex valued dy...

We formulate and solve a deterministic optimal consumption problem to maximize the discounted CRRA utility of an individual's consumption-to-habit process assuming she only invests in a riskless mar...

We analyze an optimal stopping problem with a series of inequality-type and equality-type expectation constraints in a general non-Markovian framework. We show that the optimal stopping problem with...

We study the problem of prediction with expert advice with adversarial corruption where the adversary can at most corrupt one expert. Using tools from viscosity theory, we characterize the long-time...

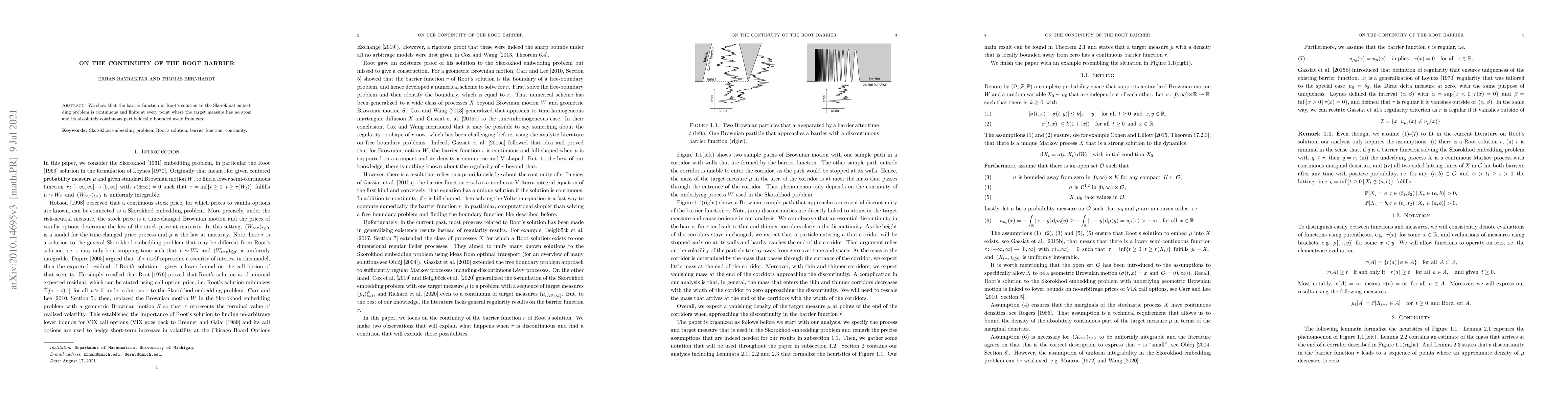

We show that the barrier function in Root's solution to the Skorokhod embedding problem is continuous and finite at every point where the target measure has no atom and its absolutely continuous par...

This paper is concerned with the analysis of blow-ups for two McKean-Vlasov equations involving hitting times. Let $(B(t); \, t \ge 0)$ be standard Brownian motion, and $\tau:= \inf\{t \ge 0: X(t) \...

The current COVID-19 pandemic and subsequent lockdowns have highlighted the close and delicate relationship between a country's public health and economic health. Macroeconomic models that use preex...

We consider heterogeneously interacting diffusive particle systems and their large population limit. The interaction is of mean field type with weights characterized by an underlying graphon. A law ...

We consider a prediction problem with two experts and a forecaster. We assume that one of the experts is honest and makes correct prediction with probability $\mu$ at each round. The other one is ma...

We study the Wiener disorder detection problem where each observation is associated with a positive cost. In this setting, a strategy is a pair consisting of a sequence of observation times and a st...

We appended an errata to the original submission. The purpose of this errata is to point out two errors in [2] and give a weakened version of those statements made.

We force uniqueness in finite state mean field games by adding a Wright-Fisher common noise. We achieve this by analyzing the master equation of this game, which is a degenerate parabolic second-ord...

We explicitly solve the nonlinear PDE that is the continuous limit of dynamic programming of \emph{expert prediction problem} in finite horizon setting with $N=4$ experts. The \emph{expert predictio...

We analyze an $N+1$-player game and the corresponding mean field game with state space $\{0,1\}$. The transition rate of $j$-th player is the sum of his control $\alpha^j$ plus a minimum jumping rat...

We analyze a mean field tournament: a mean field game in which the agents receive rewards according to the ranking of the terminal value of their projects and are subject to cost of effort. Using Sc...

Let $(Z,\kappa)$ be a Walsh Brownian motion with spinning measure $\kappa$. Suppose $\mu$ is a probability measure on $\mathbb{R}^n$. We characterize all the $\kappa$ such that $\mu$ is a stopping d...

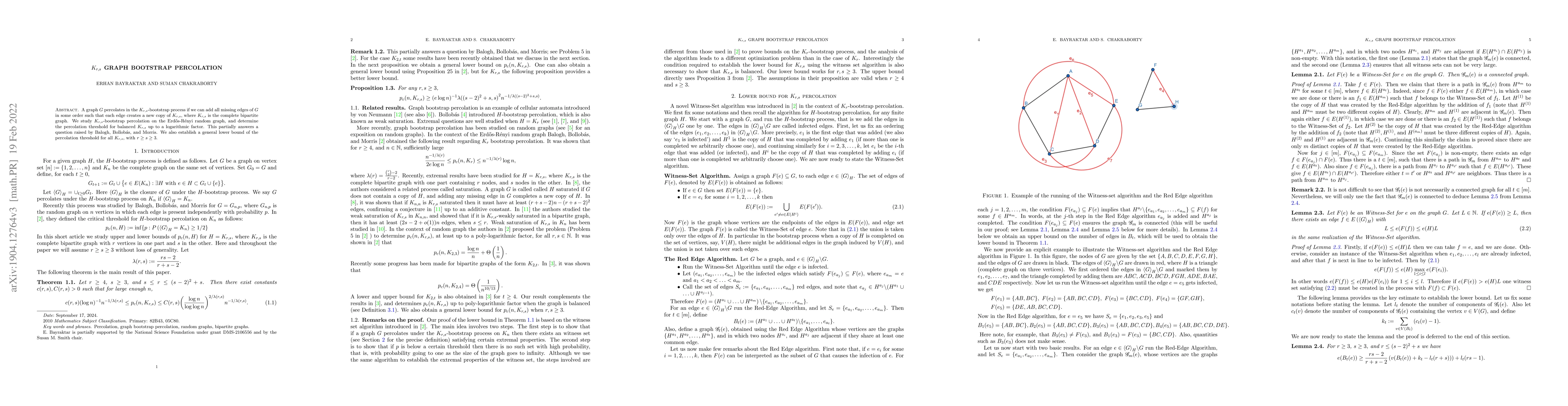

A graph $G$ percolates in the $K_{r,s}$-bootstrap process if we can add all missing edges of $G$ in some order such that each edge creates a new copy of $K_{r,s}$, where $K_{r,s}$ is the complete bi...

In this paper we find tight sufficient conditions for the continuity of the value of the utility maximization problem from terminal wealth with respect to the convergence in distribution of the unde...

We prove the superhedging duality for a discrete-time financial market with proportional transaction costs under model uncertainty. Frictions are modeled through solvency cones as in the original mo...

Motivated by recent data analytics applications, we study the adversarial robustness of robust estimators. Instead of assuming that only a fraction of the data points are outliers as considered in t...

This paper focuses on martingale optimal transport problems when the martingales are assumed to have bounded quadratic variation. First, we give a result that characterizes the existence of a probab...

In this paper we study a principal-agent problem in continuous time with multiple lump-sum payments (contracts) paid at different deterministic times. We reduce the non-zero sum Stackelberg game betwe...

We consider an $N$-player game where the players control the drifts of their diffusive states which have no interaction in the noise terms. The aim of each player is to minimize the expected value of ...

Portfolio selection problems that optimize expected utility are usually difficult to solve. If the number of assets in the portfolio is large, such expected utility maximization problems become even h...

We study an approximation method for partially observed Markov decision processes (POMDPs) with continuous spaces. Belief MDP reduction, which has been the standard approach to study POMDPs requires r...

The paper focuses on mean-field type multi-agent control problems where the dynamics and cost structures are symmetric and homogeneous, and are affected by the distribution of the agents. A standard s...

In this paper, we provide a convergence rate for particle approximations of a class of second-order PDEs on Wasserstein space. We show that, up to some error term, the infinite-dimensional inf(sup)-co...

In this paper we solve the dividend optimization problem for a corporation or a financial institution when the managers of the corporation are facing (regulatory) implementation delays. We consider se...

We establish when the two problems of minimizing a function of lifetime minimum wealth and of maximizing utility of lifetime consumption result in the same optimal investment strategy on a given open ...

In this article we revisit the weak optimal transport (WOT) problem, introduced by Gozlan, Roberto, Samson and Tetali (2017). We work on the real line, with barycentric cost functions, and as our firs...

In this paper, we show that the value functions of mean field control problems with common noise are the unique viscosity solutions to fully second-order Hamilton-Jacobi-Bellman equations, in a Cranda...

We study the asymptotic behavior of solutions to linear-quadratic mean field stochastic optimal control problems. By formulating an ergodic control framework, we characterize the convergence between t...

We study the uniform-in-time weak propagation of chaos for the consensus-based optimization (CBO) method on a bounded searching domain. We apply the methodology for studying long-time behaviors of int...

This work provides a unified framework for exploring games. In existing literature, strategies of players are typically assigned scalar values, and the concept of Nash equilibrium is used to identify ...

In this paper, we prove a comparison result for semi-continuous viscosity solutions of a class of second-order PDEs in the Wasserstein space. This allows us to remove the Lipschitz continuity assumpti...

We present a continuous-time portfolio selection framework that reflects goal-based investment principles and mental accounting behavior. In this framework, an investor with multiple investment goals ...

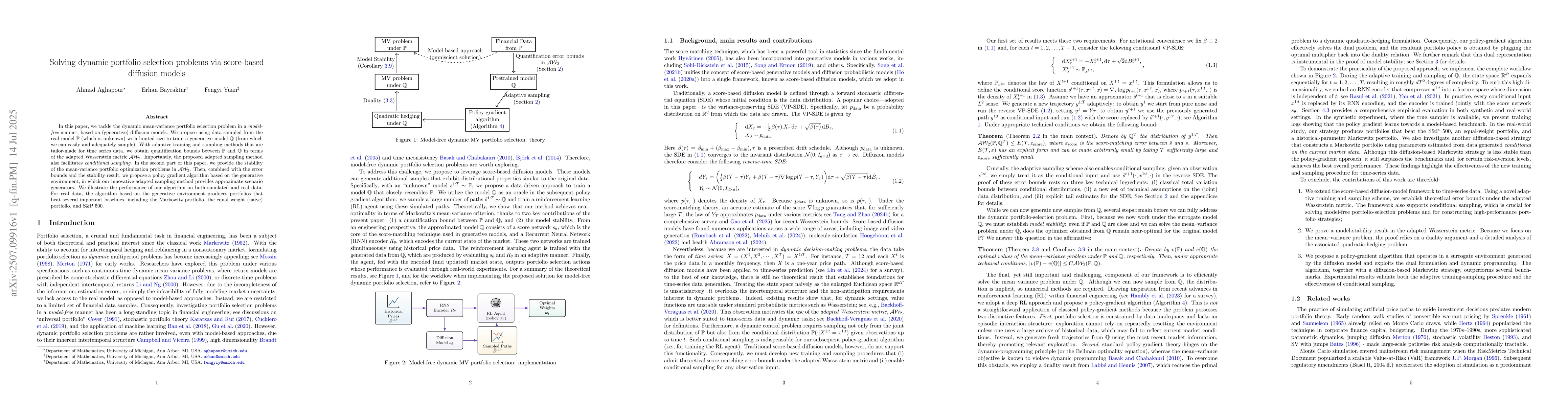

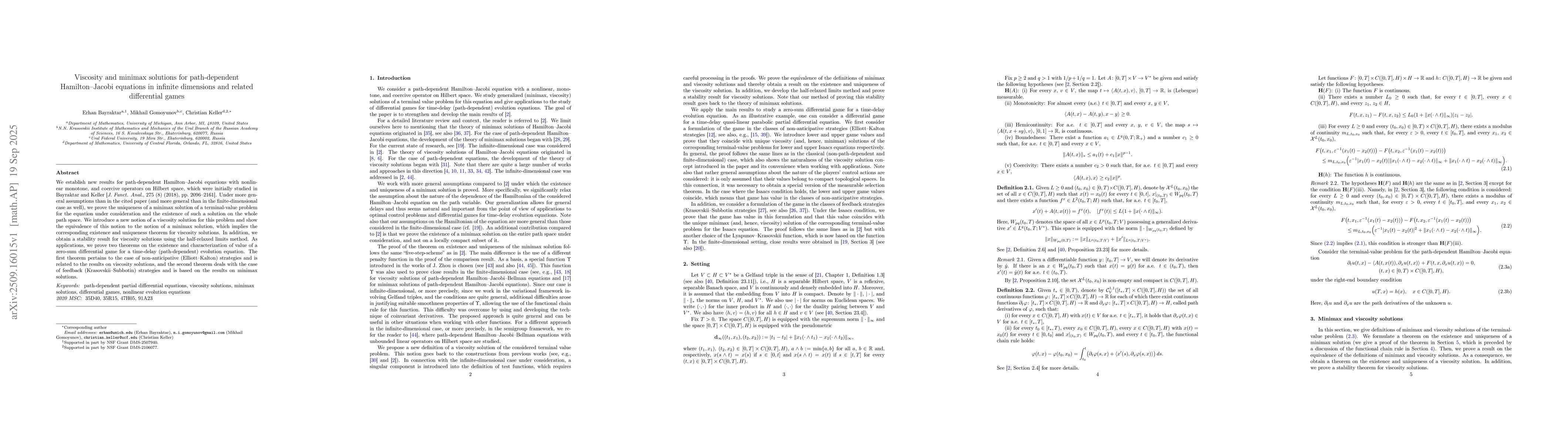

In this paper, we tackle the dynamic mean-variance portfolio selection problem in a {\it model-free} manner, based on (generative) diffusion models. We propose using data sampled from the real model $...

We study a principal-agent model involving a large population of heterogeneously interacting agents. By extending the existing methods, we find the optimal contracts assuming a continuum of agents, an...

We study a nonlinear graphon particle system driven by both idiosyncratic and common noise, where interactions are governed by a graphon and represented as positive finite measures. Each particle evol...

We establish new results for path-dependent Hamilton-Jacobi equations with nonlinear monotone, and coercive operators on Hilbert space, which were initially studied in Bayraktar and Keller [J. Funct. ...

This paper develops a mean field game framework for dynamic two-sided matching markets, extending existing matching theory by integrating micro-macro dynamics in two-sided environments. Unlike traditi...

We study a goal-based portfolio selection problem in which an investor aims to meet multiple financial goals, each with a specific deadline and target amount. Trading the stock incurs a strictly posit...

We study a class of degenerate diffusion generators that arise in sequential testing and quickest detection problems with partial information. The observation process is driven by $k$ independent Brow...

We propose a deep neural-operator framework for a general class of probability models. Under global Lipschitz conditions on the operator over the entire Euclidean space-and for a broad class of probab...

In this paper we solve the dividend optimization problem for a corporation or a financial institution when the managers of the corporation are facing (regulatory) implementation delays. We consider se...

We establish when the two problems of minimizing a function of lifetime minimum wealth and of maximizing utility of lifetime consumption result in the same optimal investment strategy on a given open ...

We investigate convergence and turnpike properties for linear-quadratic mean field control problems with common noise. Within a unified framework, we analyze a finite-horizon social optimization probl...

We investigate the convergence of symmetric stochastic differential games with interactions via control, where the volatility terms of both idiosyncratic and common noises are controlled. We apply the...

Diffusion generative models synthesize samples by discretizing reverse-time dynamics driven by a learned score (or denoiser). Existing convergence analyses of diffusion models typically scale at least...

We study the large-population convergence of a consensus-based algorithm for the saddle point problem proposed by ArXiv: 2212.12334, establishing the uniform-in-time propagation of chaos using a coupl...

We study mean-field game (MFG) problems with rough common noise where the representative state dynamics is governed by a controlled rough stochastic differential equation driven by an idiosyncratic Br...

This paper develops a quantized Q-learning algorithm for the optimal control of controlled diffusion processes on $\mathbb{R}^d$ under both discounted and ergodic (average) cost criteria. We first est...

Banks must optimize risky investments, dividend payouts, and capital structure under tight Basel III solvency and liquidity constraints, while costly equity issuance serves as a distress-recovery tool...

We study continuous-time online learning where data are generated by a diffusion process with unknown coefficients. The learner employs a two-layer neural network, continuously updating its parameters...

Automation raises productivity and reduces paid human labor, but it also reallocates income and ownership claims. This paper studies that tradeoff in a static benchmark and in a stationary heterogeneo...

We study zero-shot conditional sampling with pretrained diffusion models for linear inverse problems, including inpainting and super-resolution. In these problems, the observation determines only part...

Diffusion models perform remarkably well on high-dimensional data such as images, often using only a modest number of reverse-time steps. Despite this practical success, existing convergence theory do...

This paper studies the existence and approximation of equilibria for general time-inconsistent mean field game (MFG) problems in the continuous-time setting. To handle the intricate nonlocal equilibri...

We study causal optimal transport in continuous time, with Markovian cost, between a finite-state Markov source and a diffusion target. By replacing the source with its conditional law given the obser...

This paper develops a policy gradient method for entropy-regularized mean-field control in the discounted infinite-horizon setting. We consider randomized feedback policies and a coupled representativ...

We prove a comparison principle for a class of second-order Hamilton--Jacobi--Bellman equations on the Wasserstein space whose second-order term is generated by a general common-noise Hessian. The mai...

We study an infinite-horizon optimal consumption-investment problem for an investor with Epstein-Zin stochastic differential utility with stochastic investment opportunities in an incomplete market. R...

We study optimal control of a system with multiple decision makers who share a common hidden state and receive fully decentralized observations through identical channels. The dynamics of the hidden s...

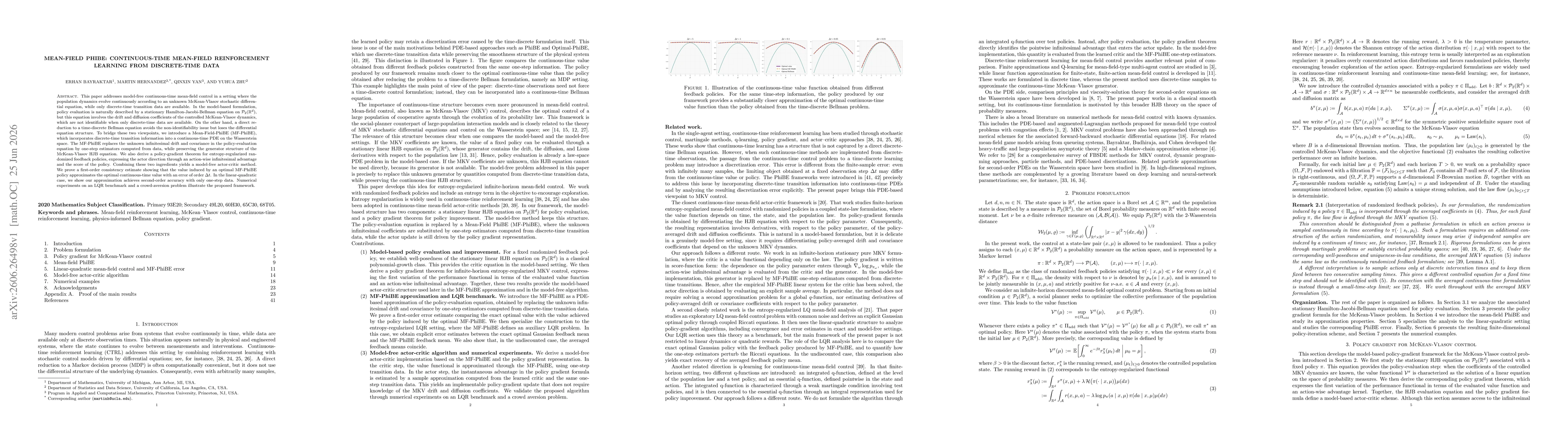

This paper addresses model-free continuous-time mean-field control in a setting where the population dynamics evolve continuously according to an unknown McKean-Vlasov stochastic differential equation...