Academic Profile

Statistics

Similar Authors

Papers on arXiv

Maximizing monotone submodular functions under cardinality constraints is a classic optimization task with several applications in data mining and machine learning. In this paper we study this probl...

We address a generalization of the bandit with knapsacks problem, where a learner aims to maximize rewards while satisfying an arbitrary set of long-term constraints. Our goal is to design best-of-b...

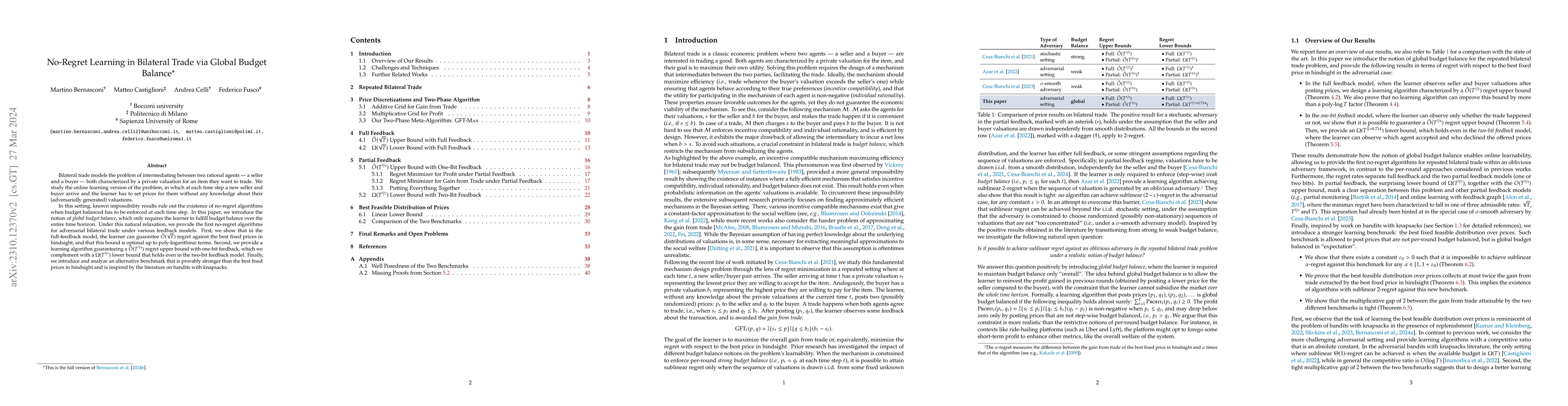

Bilateral trade models the problem of intermediating between two rational agents -- a seller and a buyer -- both characterized by a private valuation for an item they want to trade. We study the onl...

We study the problem of regret minimization for a single bidder in a sequence of first-price auctions where the bidder discovers the item's value only if the auction is won. Our main contribution is...

The bandits with knapsack (BwK) framework models online decision-making problems in which an agent makes a sequence of decisions subject to resource consumption constraints. The traditional model as...

Maximizing monotone submodular functions under a matroid constraint is a classic algorithmic problem with multiple applications in data mining and machine learning. We study this classic problem in ...

Streaming submodular maximization is a natural model for the task of selecting a representative subset from a large-scale dataset. If datapoints have sensitive attributes such as gender or race, it ...

Pandora's problem is a fundamental model in economics that studies optimal search strategies under costly inspection. In this paper we initiate the study of Pandora's problem with combinatorial cost...

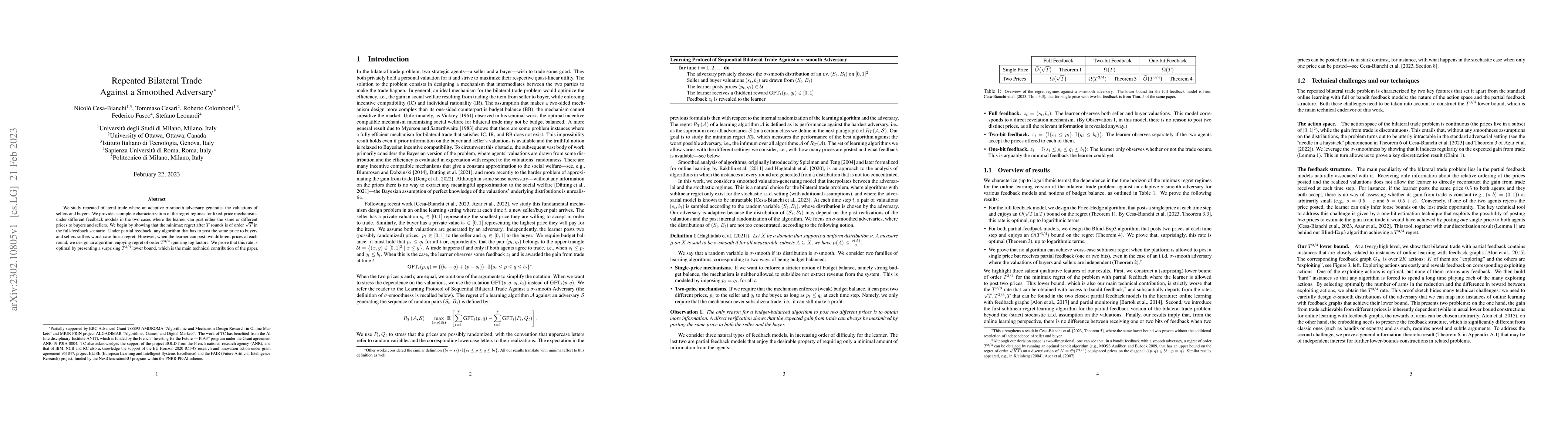

We study repeated bilateral trade where an adaptive $\sigma$-smooth adversary generates the valuations of sellers and buyers. We provide a complete characterization of the regret regimes for fixed-p...

We study truthful mechanisms for welfare maximization in online bipartite matching. In our (multi-parameter) setting, every buyer is associated with a (possibly private) desired set of items, and ha...

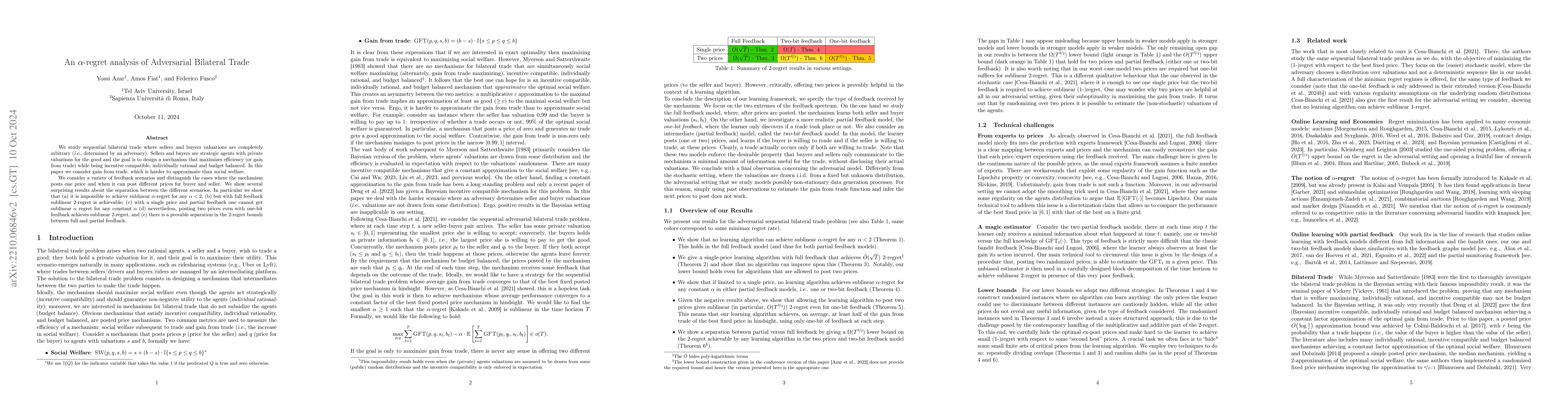

We study sequential bilateral trade where sellers and buyers valuations are completely arbitrary (i.e., determined by an adversary). Sellers and buyers are strategic agents with private valuations f...

The framework of feedback graphs is a generalization of sequential decision-making with bandit or full information feedback. In this work, we study an extension where the directed feedback graph is ...

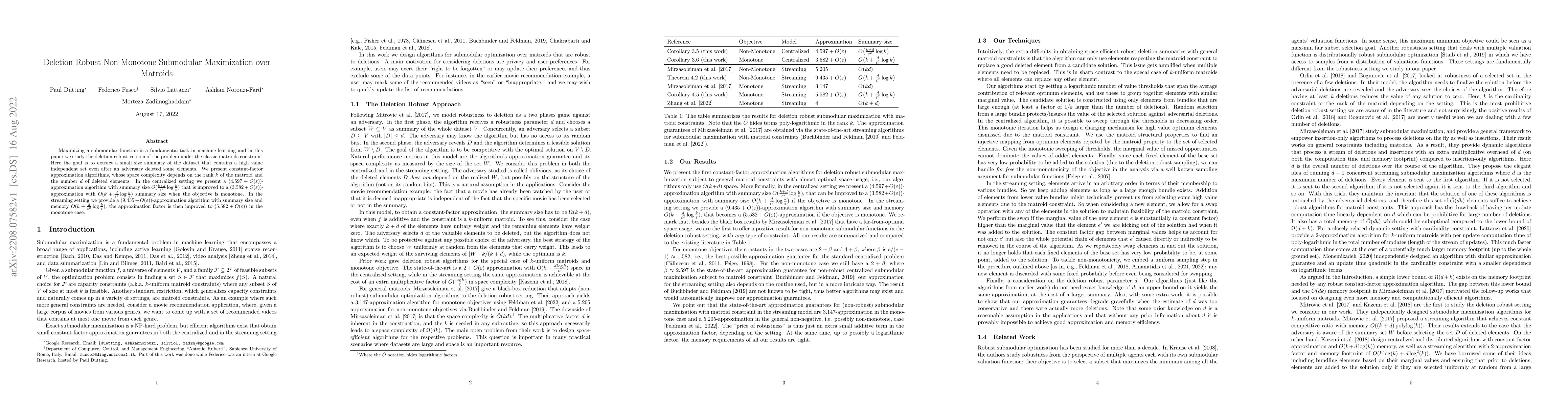

Maximizing a submodular function is a fundamental task in machine learning and in this paper we study the deletion robust version of the problem under the classic matroids constraint. Here the goal ...

Maximizing a monotone submodular function is a fundamental task in machine learning. In this paper, we study the deletion robust version of the problem under the classic matroids constraint. Here th...

We study single-sample prophet inequalities (SSPIs), i.e., prophet inequalities where only a single sample from each prior distribution is available. Besides a direct, and optimal, SSPI for the basi...

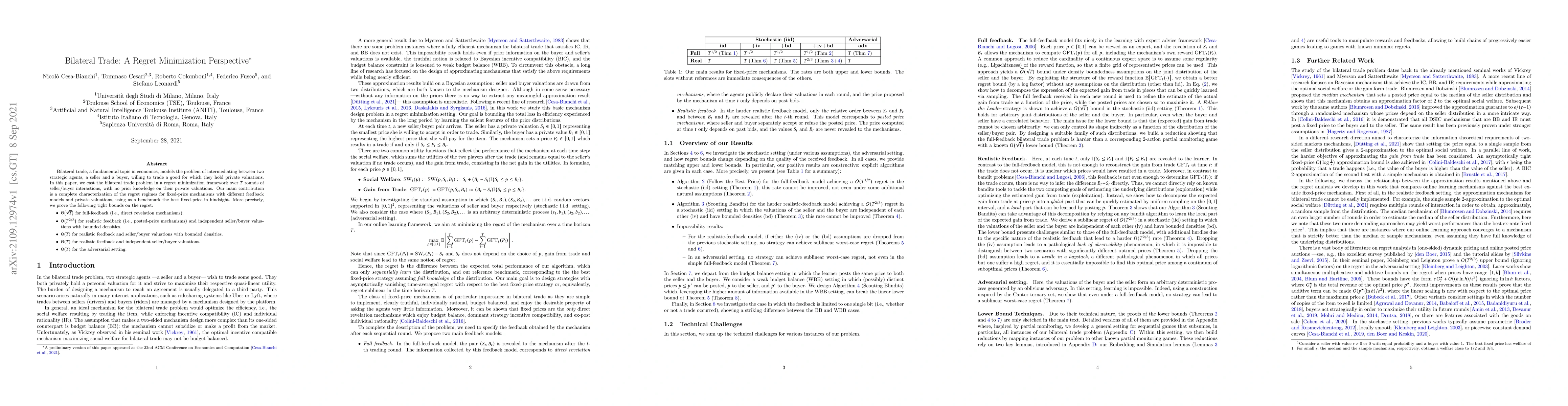

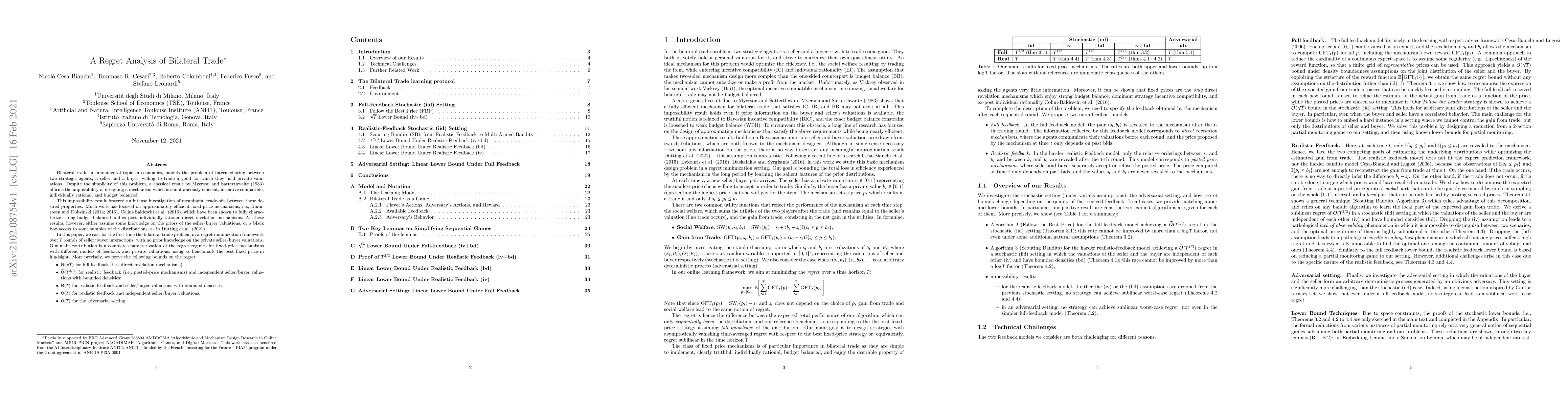

Bilateral trade, a fundamental topic in economics, models the problem of intermediating between two strategic agents, a seller and a buyer, willing to trade a good for which they hold private valuat...

We consider the problem of fairly allocating a set of indivisible goods to a set of strategic agents with additive valuation functions. We assume no monetary transfers and, therefore, a mechanism in...

We study the problem of online multiclass classification in a setting where the learner's feedback is determined by an arbitrary directed graph. While including bandit feedback as a special case, fe...

We consider the prophet inequality problem for (not necessarily bipartite) matching problems with independent edge values, under both edge arrivals and vertex arrivals. We show constant-factor proph...

Bilateral trade, a fundamental topic in economics, models the problem of intermediating between two strategic agents, a seller and a buyer, willing to trade a good for which they hold private valuat...

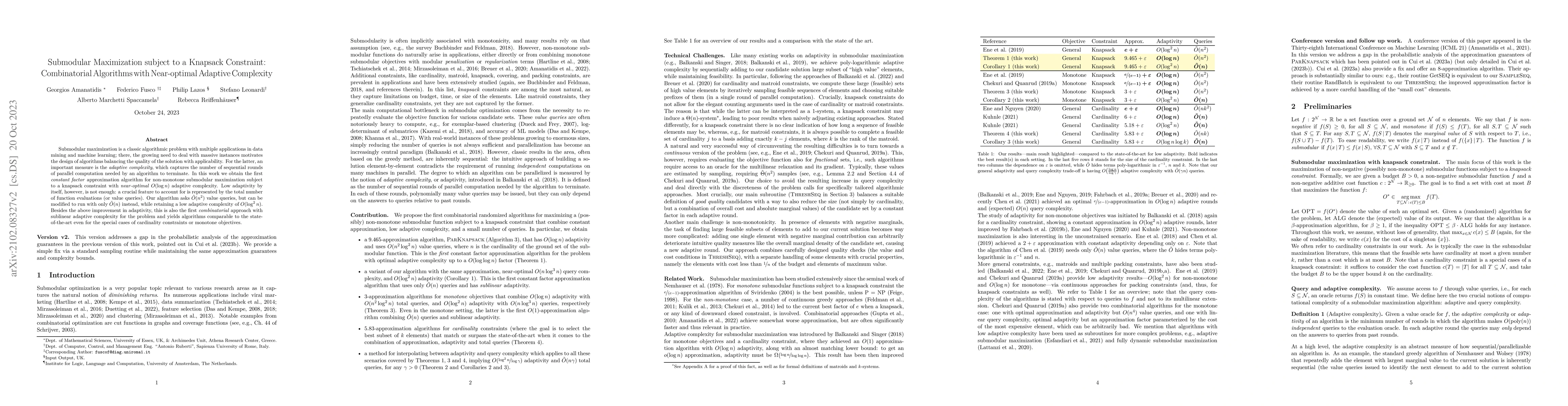

Submodular maximization is a classic algorithmic problem with multiple applications in data mining and machine learning; there, the growing need to deal with massive instances motivates the design o...

Constrained submodular maximization problems encompass a wide variety of applications, including personalized recommendation, team formation, and revenue maximization via viral marketing. The massiv...

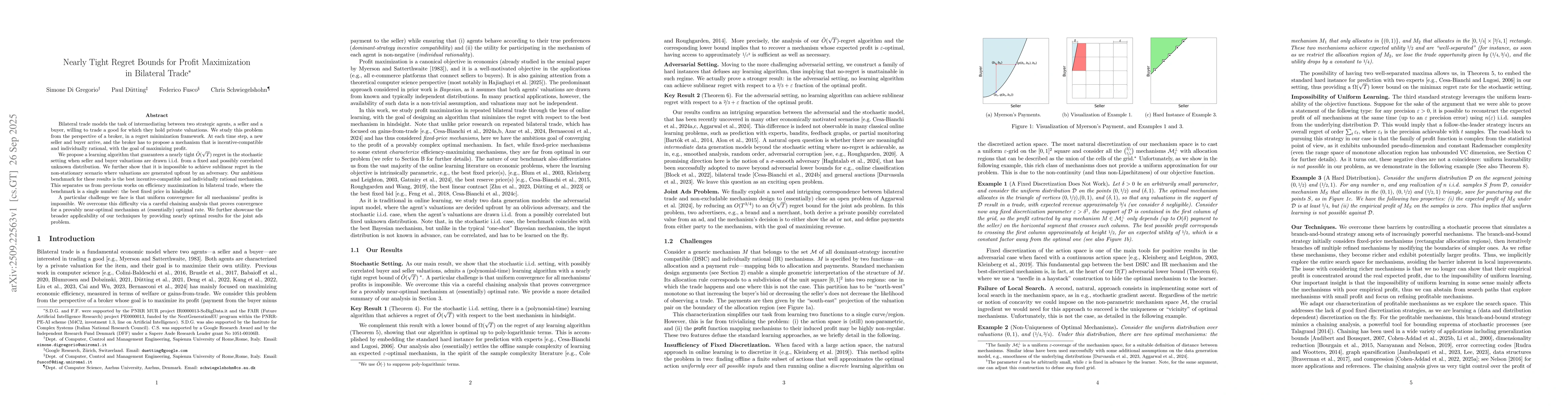

A celebrated impossibility result by Myerson and Satterthwaite (1983) shows that any truthful mechanism for two-sided markets that maximizes social welfare must run a deficit, resulting in a necessi...

The Pandora's Box Problem, originally formalized by Weitzman in 1979, models selection from set of random, alternative options, when evaluation is costly. This includes, for example, the problem of ...

Efficient and truthful mechanisms to price resources on remote servers/machines has been the subject of much work in recent years due to the importance of the cloud market. This paper considers reve...

In online learning, a decision maker repeatedly selects one of a set of actions, with the goal of minimizing the overall loss incurred. Following the recent line of research on algorithms endowed with...

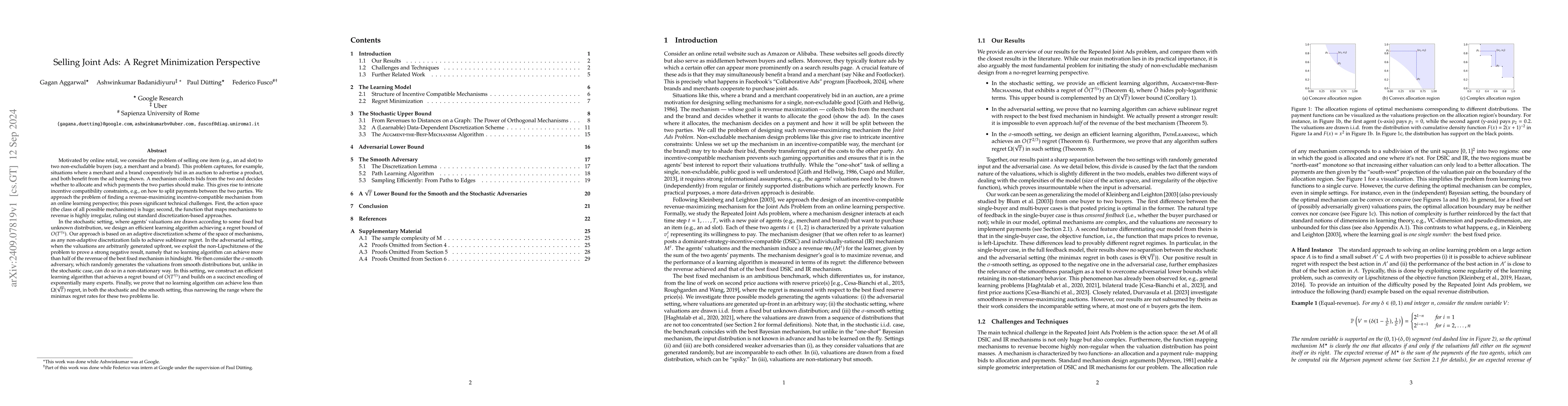

Motivated by online retail, we consider the problem of selling one item (e.g., an ad slot) to two non-excludable buyers (say, a merchant and a brand). This problem captures, for example, situations wh...

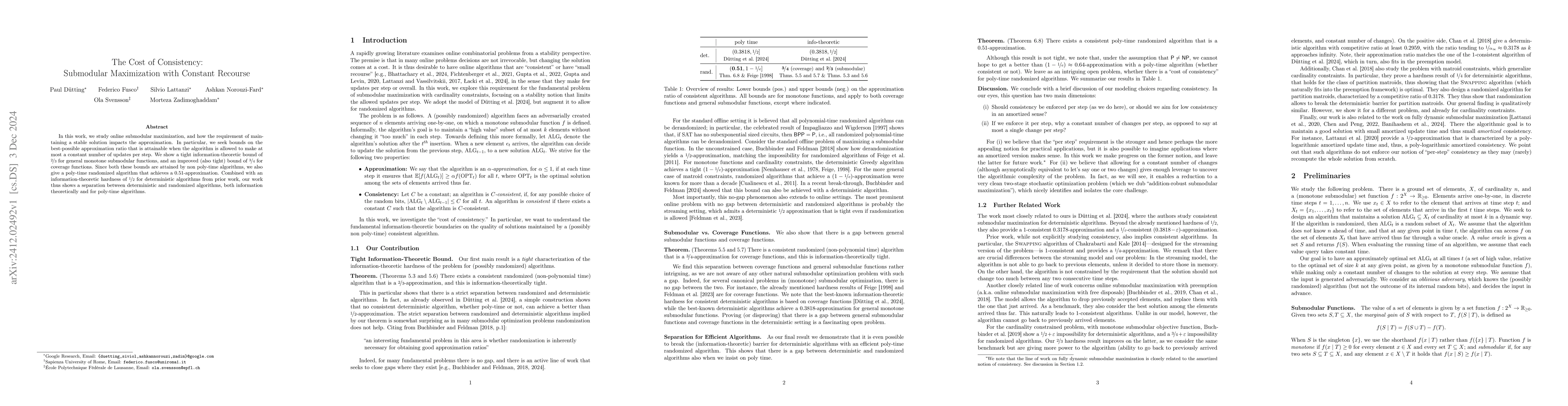

In this work, we study online submodular maximization, and how the requirement of maintaining a stable solution impacts the approximation. In particular, we seek bounds on the best-possible approximat...

The Pandora's Box problem models the search for the best alternative when evaluation is costly. In its simplest variant, a decision maker is presented with $n$ boxes, each associated with a cost of in...

Bilateral trade models the task of intermediating between two strategic agents, a seller and a buyer, willing to trade a good for which they hold private valuations. We study this problem from the per...

In the random-order model for online learning, the sequence of losses is chosen upfront by an adversary and presented to the learner after a random permutation. Any random-order input is \emph{asy...

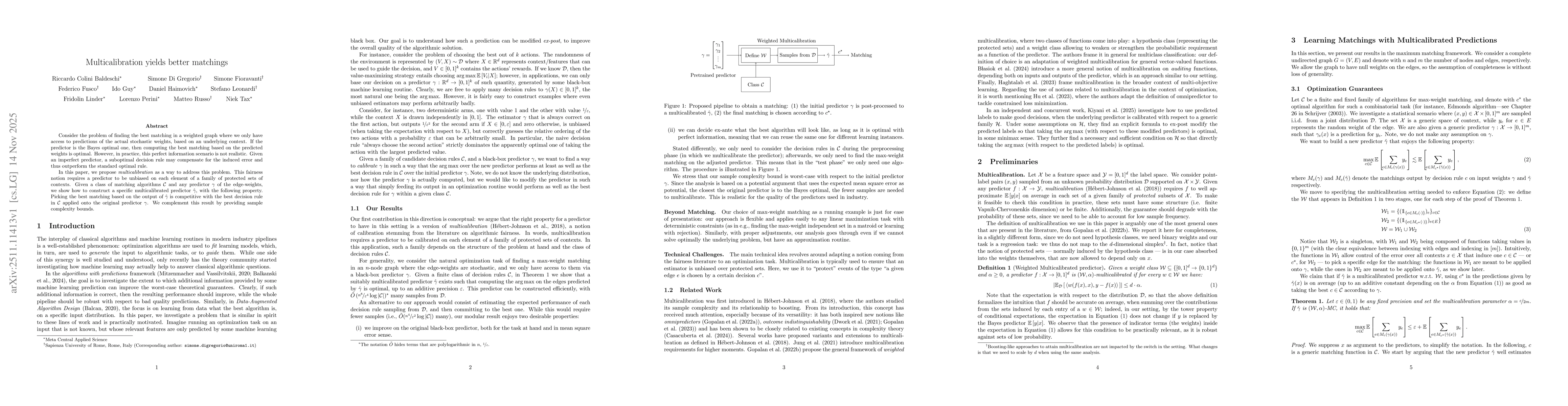

Consider the problem of finding the best matching in a weighted graph where we only have access to predictions of the actual stochastic weights, based on an underlying context. If the predictor is the...

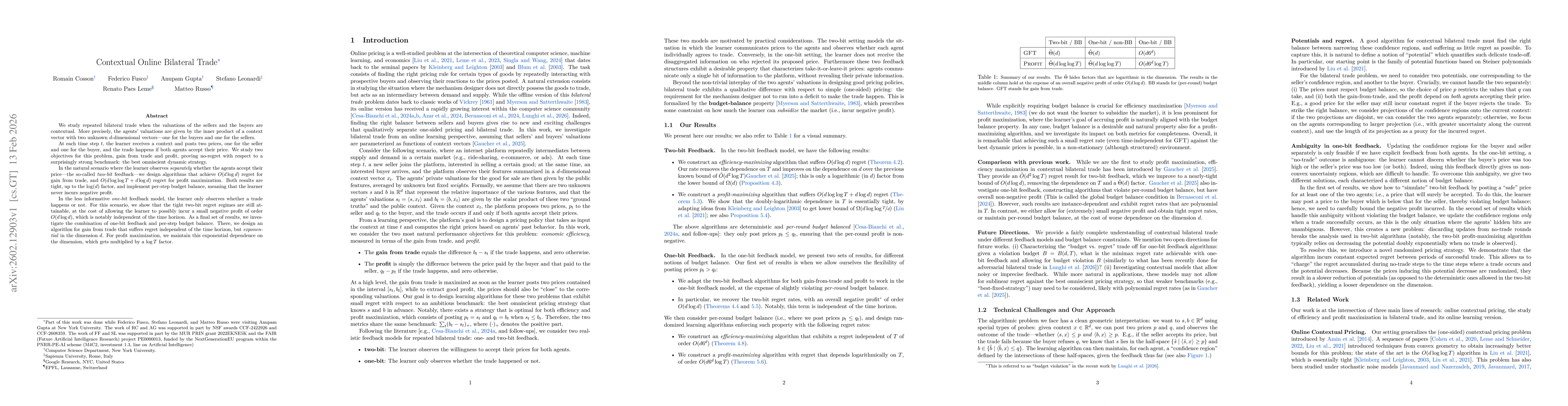

We study repeated bilateral trade when the valuations of the sellers and the buyers are contextual. More precisely, the agents' valuations are given by the inner product of a context vector with two u...

Bilateral trade models the task of intermediating between two strategic agents, a seller and a buyer, who wish to trade a good. We study this problem from the perspective of a profit-maximizing broker...

Bilateral trade models one of the most fundamental economic interactions: the intermediation between two strategic agents, a seller and a buyer, willing to trade a good. We consider the learning versi...

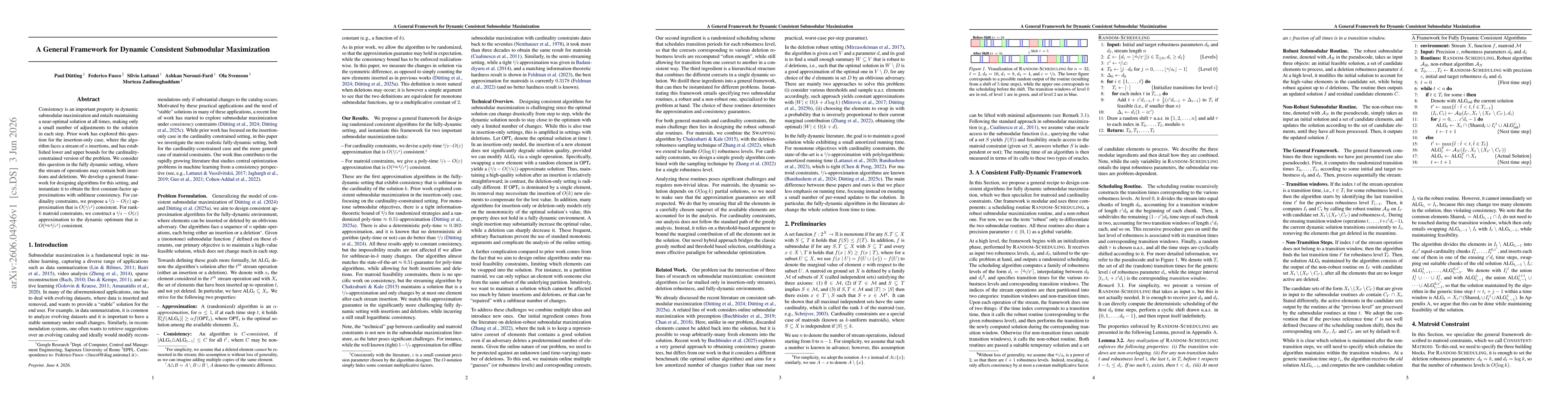

Consistency is an important property in dynamic submodular maximization and entails maintaining a near-optimal solution at all times, making only a small number of adjustments to the solution in each ...