Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper, we discuss portfolio selection strategies for Enhanced Indexation (EI), which are based on stochastic dominance relations. The goal is to select portfolios that stochastically dominat...

We focus on a behavioral model, that has been recently proposed in the literature, whose rational can be traced back to the Half-Full/Half-Empty glass metaphor. More precisely, we generalize the Hal...

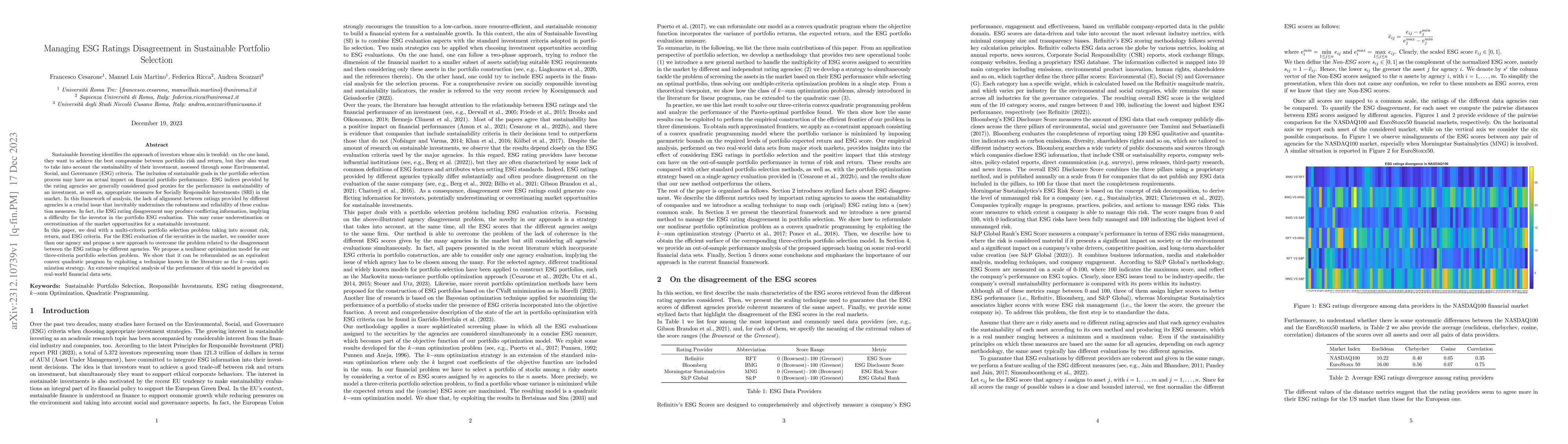

Sustainable Investing identifies the approach of investors whose aim is twofold: on the one hand, they want to achieve the best compromise between portfolio risk and return, but they also want to ta...

In this paper, we propose a general bi-objective model for portfolio selection, aiming to maximize both a diversification measure and the portfolio expected return. Within this general framework, we...

In this paper, we propose an outlier detection algorithm for multivariate data based on their projections on the directions that maximize the Cumulant Generating Function (CGF). We prove that CGF is...

Among professionals and academics alike, it is well known that active portfolio management is unable to provide additional risk-adjusted returns relative to their benchmarks. For this reason, passiv...

Value-at-Risk is one of the most popular risk management tools in the financial industry. Over the past 20 years several attempts to include VaR in the portfolio selection process have been proposed...

In this paper, we investigate the features and the performance of the Risk Parity (RP) portfolios using the Mean Absolute Deviation (MAD) as a risk measure. The RP model is a recent strategy for ass...