Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper, we study the estimation and inference of change points under a functional linear regression model with changes in the slope function. We present a novel Functional Regression Binary S...

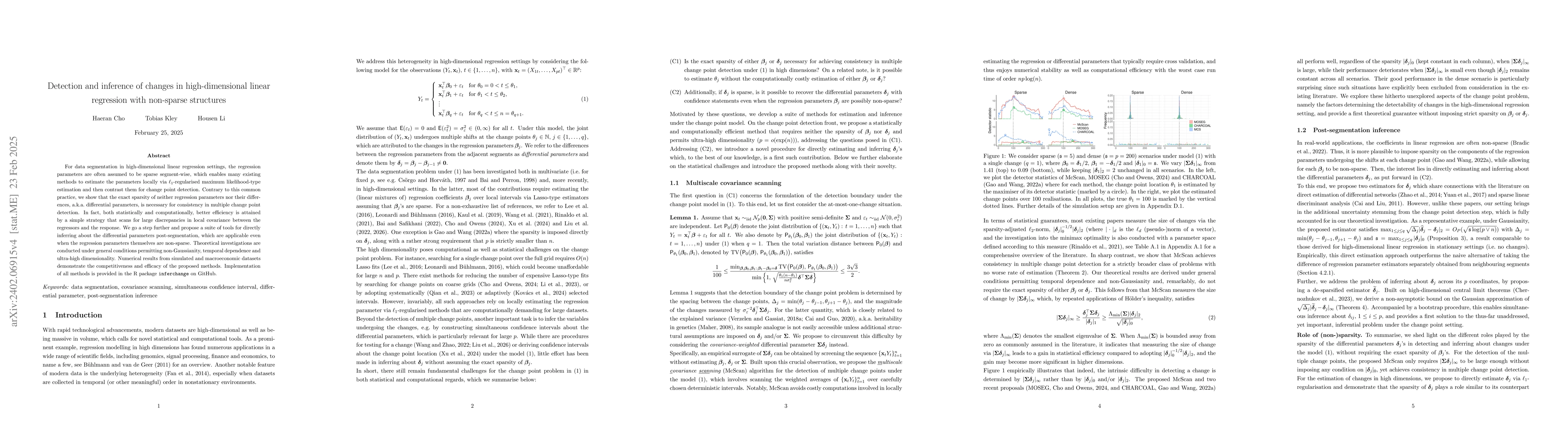

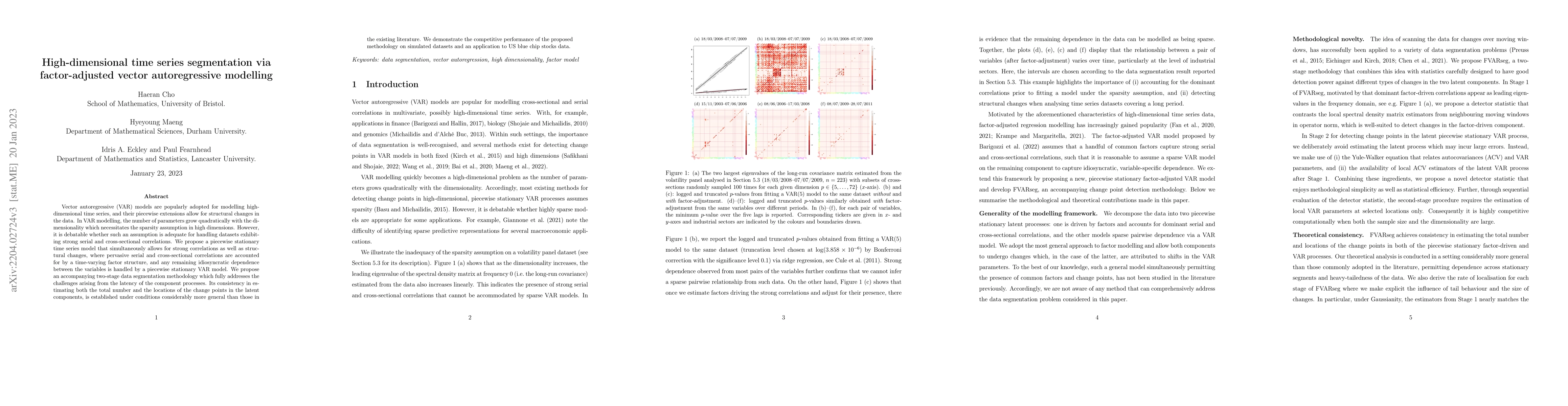

For data segmentation in high-dimensional linear regression settings, the regression parameters are often assumed to be sparse segment-wise, which enables many existing methods to estimate the param...

Modern time series data often exhibit complex dependence and structural changes which are not easily characterised by shifts in the mean or model parameters. We propose a nonparametric data segmenta...

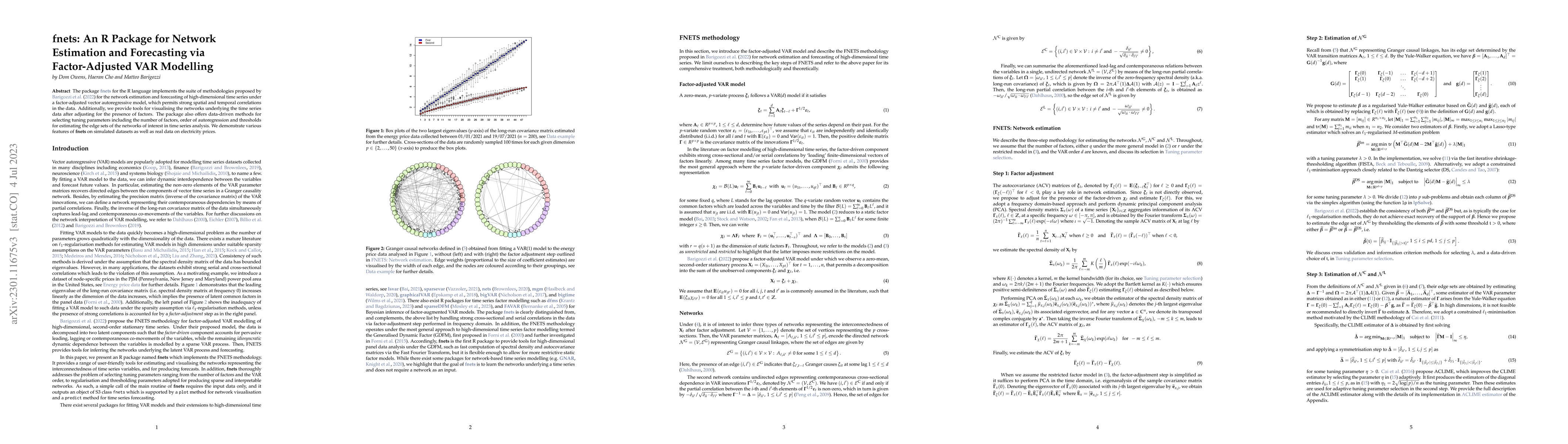

The package fnets for the R language implements the suite of methodologies proposed by Barigozzi et al. (2022) for the network estimation and forecasting of high-dimensional time series under a fact...

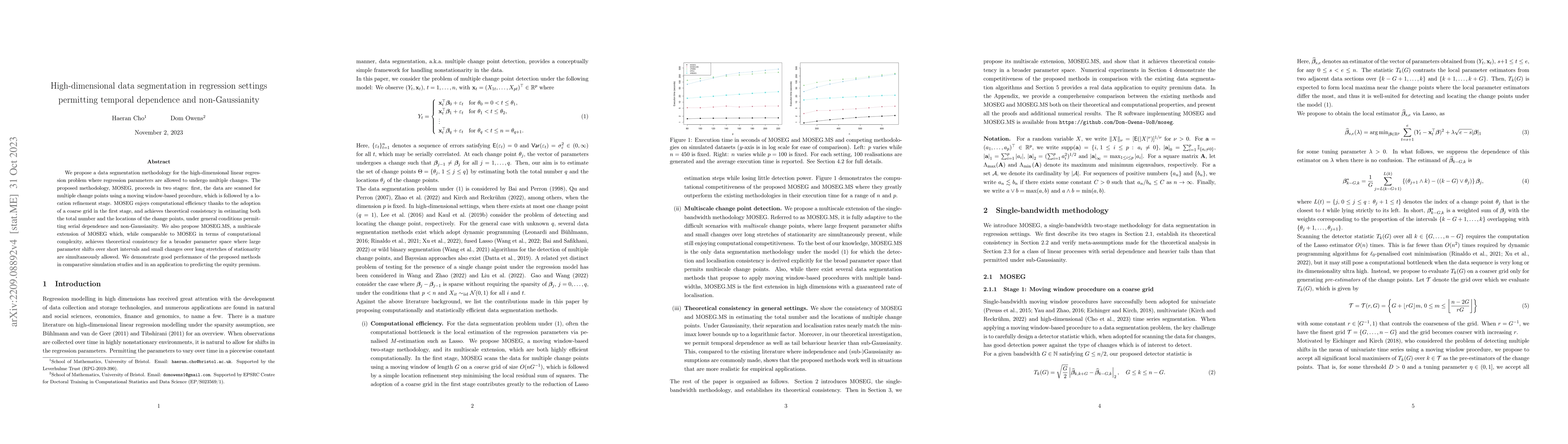

We propose a data segmentation methodology for the high-dimensional linear regression problem where regression parameters are allowed to undergo multiple changes. The proposed methodology, MOSEG, pr...

Data collected from a bike-sharing system exhibit complex temporal and spatial features. We analyze shared-bike usage data collected in Seoul, South Korea, at the level of individual stations while ...

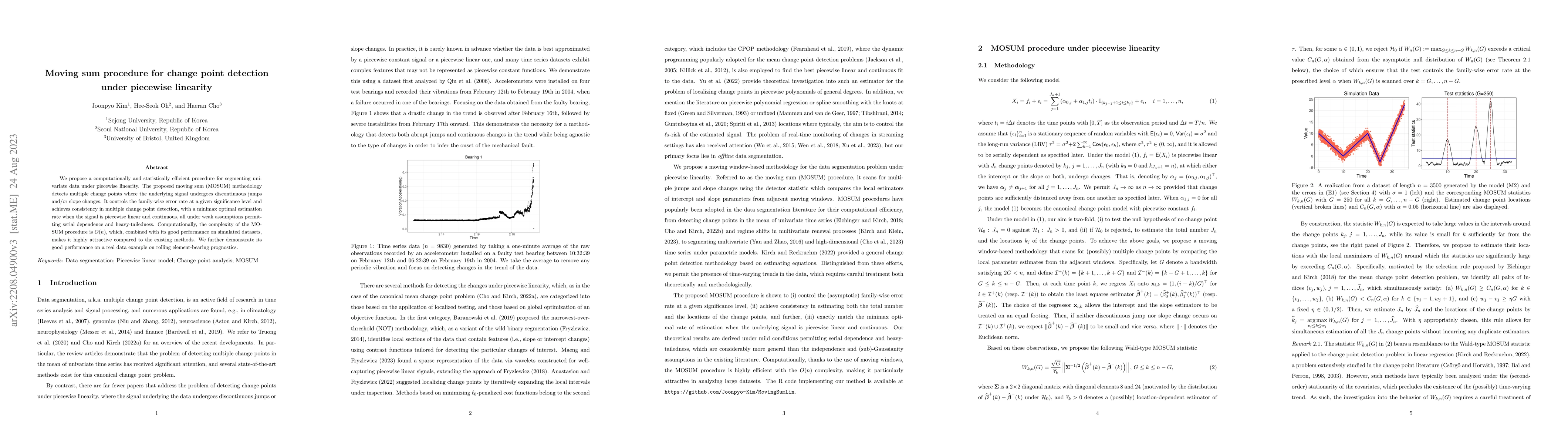

We propose a computationally and statistically efficient procedure for segmenting univariate data under piecewise linearity. The proposed moving sum (MOSUM) methodology detects multiple change point...

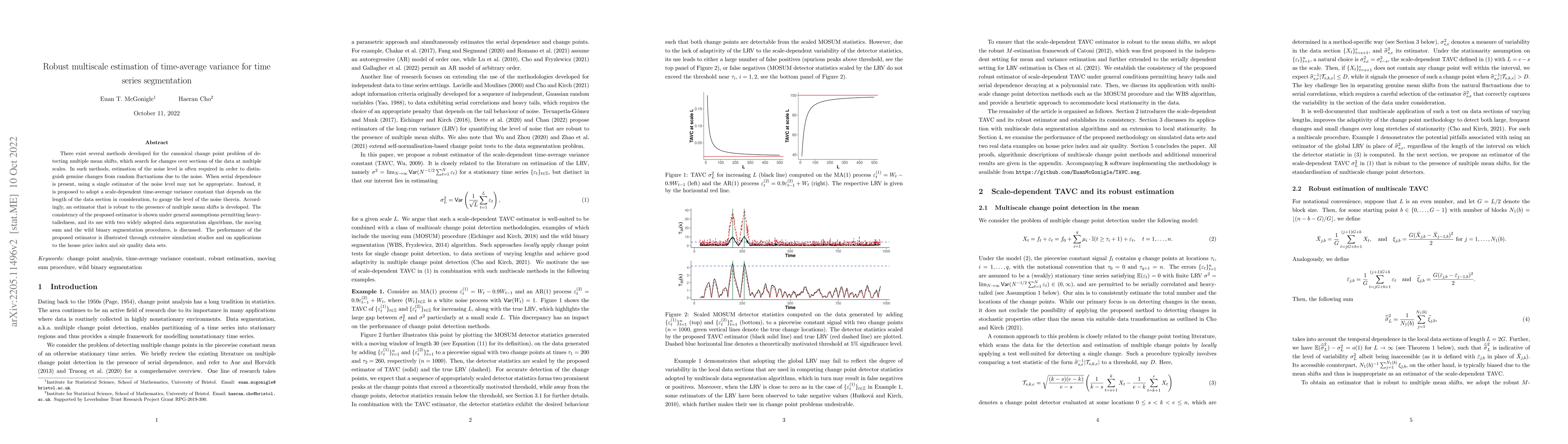

There exist several methods developed for the canonical change point problem of detecting multiple mean shifts, which search for changes over sections of the data at multiple scales. In such methods...

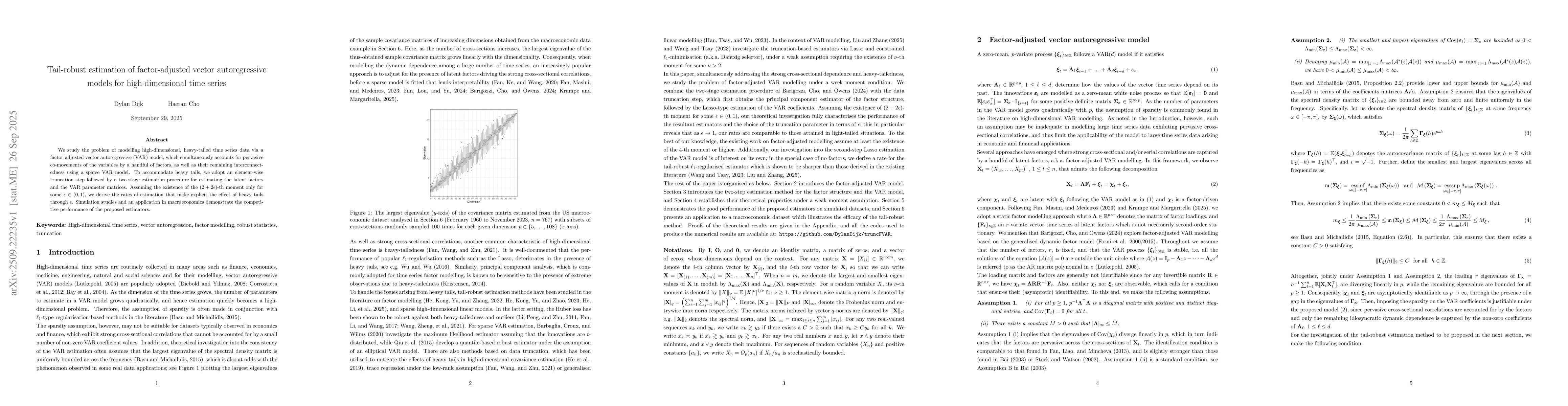

Vector autoregressive (VAR) models are popularly adopted for modelling high-dimensional time series, and their piecewise extensions allow for structural changes in the data. In VAR modelling, the nu...

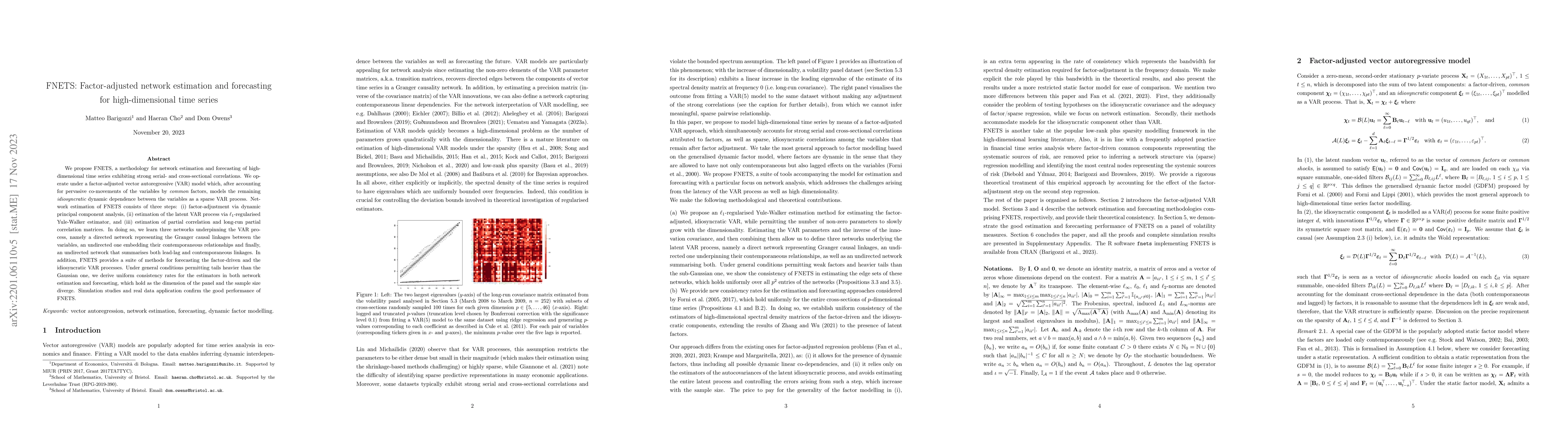

We propose FNETS, a methodology for network estimation and forecasting of high-dimensional time series exhibiting strong serial- and cross-sectional correlations. We operate under a factor-adjusted ...

The problem of quantifying uncertainty about the locations of multiple change points by means of confidence intervals is addressed. The asymptotic distribution of the change point estimators obtaine...

Data segmentation a.k.a. multiple change point analysis has received considerable attention due to its importance in time series analysis and signal processing, with applications in a variety of fie...

We propose a methodology for detecting multiple change points in the mean of an otherwise stationary, autocorrelated, linear time series. It combines solution path generation based on the wild contr...

The segmentation of a time series into piecewise stationary segments, a.k.a. multiple change point analysis, is an important problem both in time series analysis and signal processing. In the presen...

The paper proposes a moving sum methodology for detecting multiple change points in high-dimensional time series under a factor model, where changes are attributed to those in loadings as well as emer...

We study the problem of factor modelling vector- and tensor-valued time series in the presence of heavy tails in the data, which produce anomalous observations with non-negligible probability. For thi...

This paper investigates the detection and estimation of a single change in high-dimensional linear models. We derive minimax lower bounds for the detection boundary and the estimation rate, which unco...

We study the problem of modelling high-dimensional, heavy-tailed time series data via a factor-adjusted vector autoregressive (VAR) model, which simultaneously accounts for pervasive co-movements of t...

We study the problems arising from modeling high-dimensional tensor-valued time series under a Tucker decomposition-based factor model with multiple structural change points. First, we propose an algo...