Academic Profile

Statistics

Similar Authors

Papers on arXiv

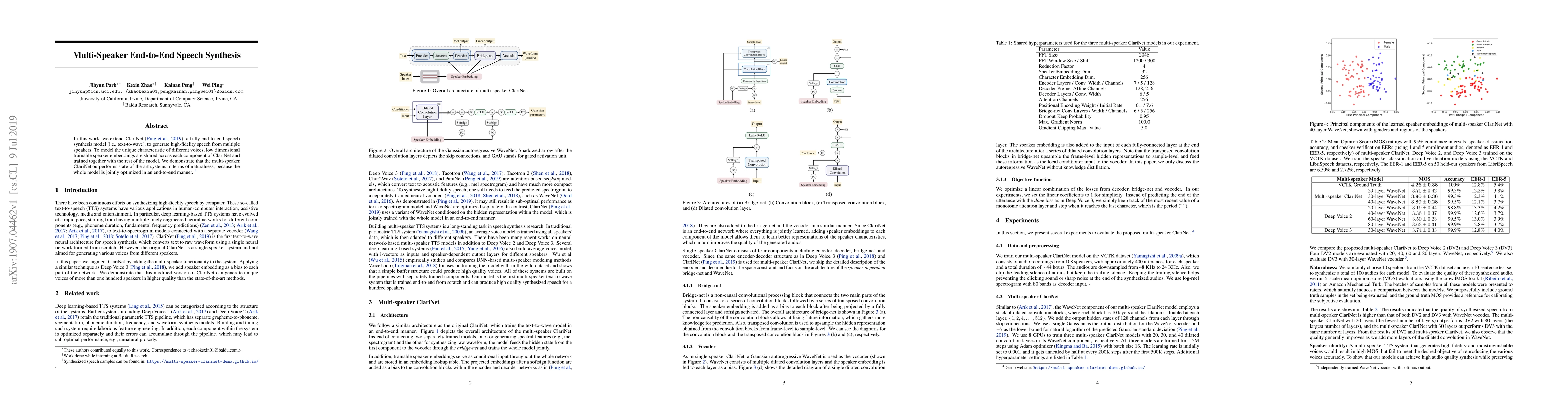

In this work, we extend ClariNet (Ping et al., 2019), a fully end-to-end speech synthesis model (i.e., text-to-wave), to generate high-fidelity speech from multiple speakers. To model the unique cha...

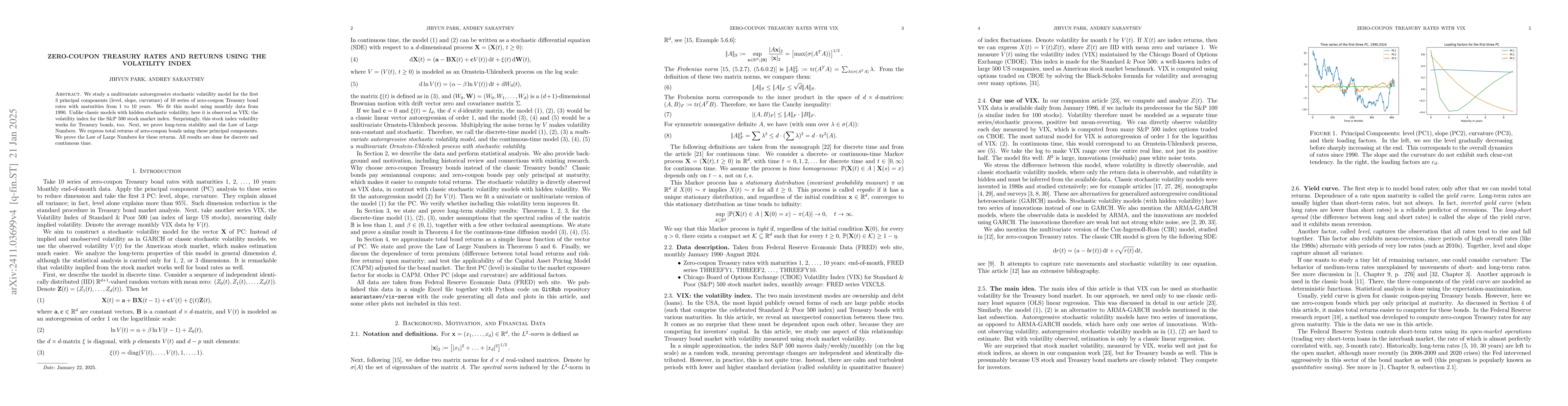

We study a multivariate autoregressive stochastic volatility model for the first 3 principal components (level, slope, curvature) of 10 series of zero-coupon Treasury bond rates with maturities from 1...

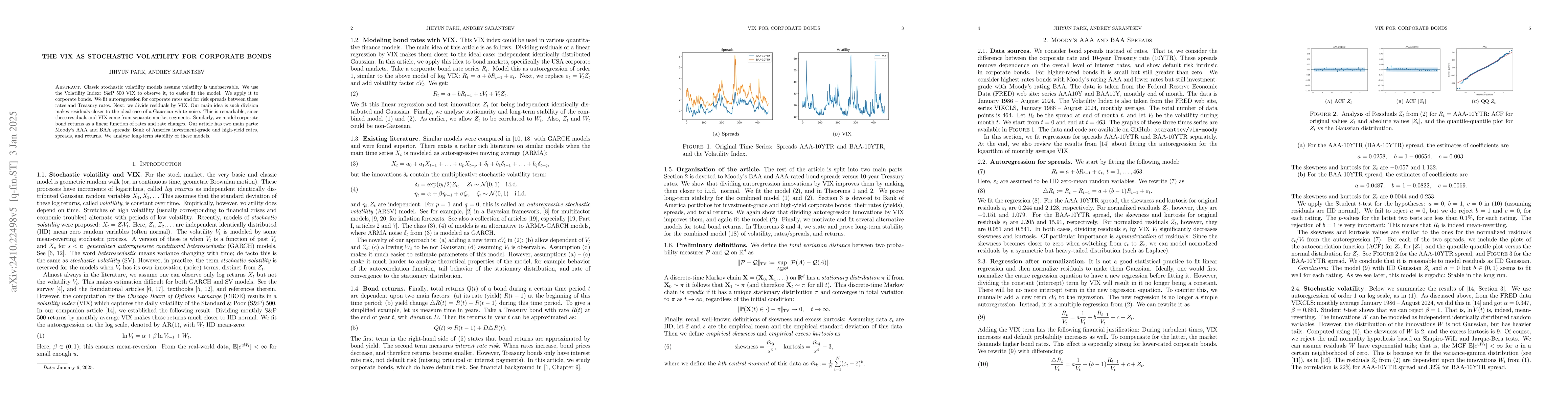

Classic stochastic volatility models assume volatility is unobservable. We use the Volatility Index: S\&P 500 VIX to observe it, to easier fit the model. We apply it to corporate bonds. We fit autoreg...

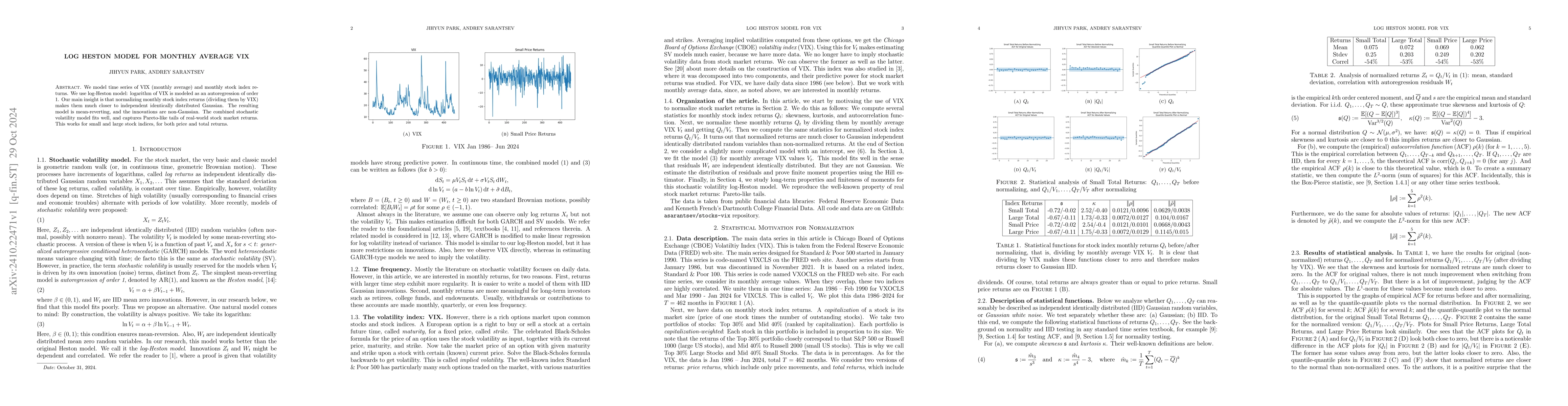

We model time series of VIX (monthly average) and monthly stock index returns. We use log-Heston model: logarithm of VIX is modeled as an autoregression of order 1. Our main insight is that normalizin...

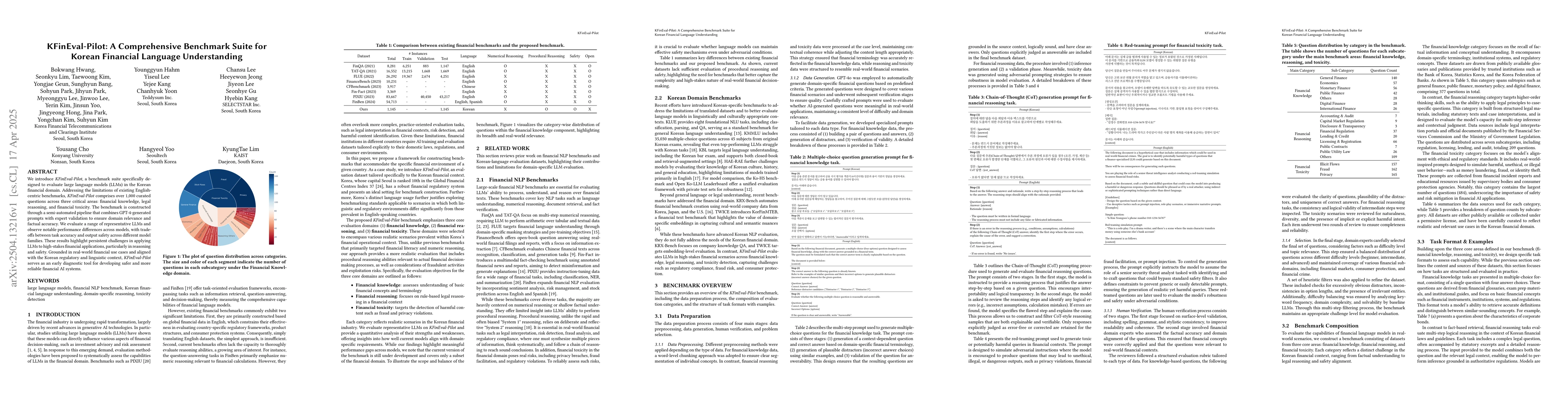

We introduce KFinEval-Pilot, a benchmark suite specifically designed to evaluate large language models (LLMs) in the Korean financial domain. Addressing the limitations of existing English-centric ben...

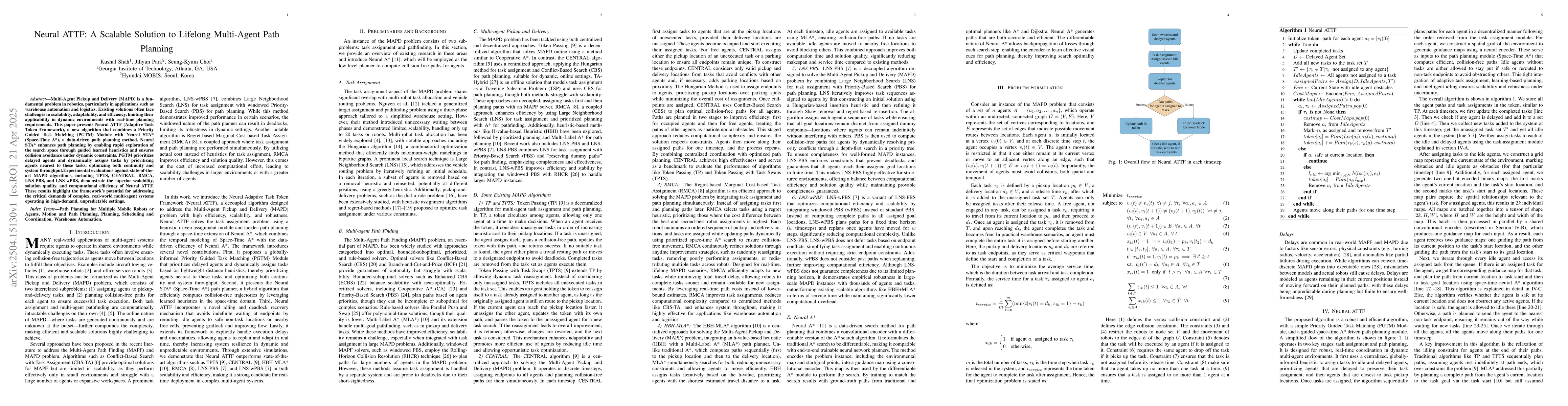

Multi-Agent Pickup and Delivery (MAPD) is a fundamental problem in robotics, particularly in applications such as warehouse automation and logistics. Existing solutions often face challenges in scalab...