Academic Profile

Statistics

Similar Authors

Papers on arXiv

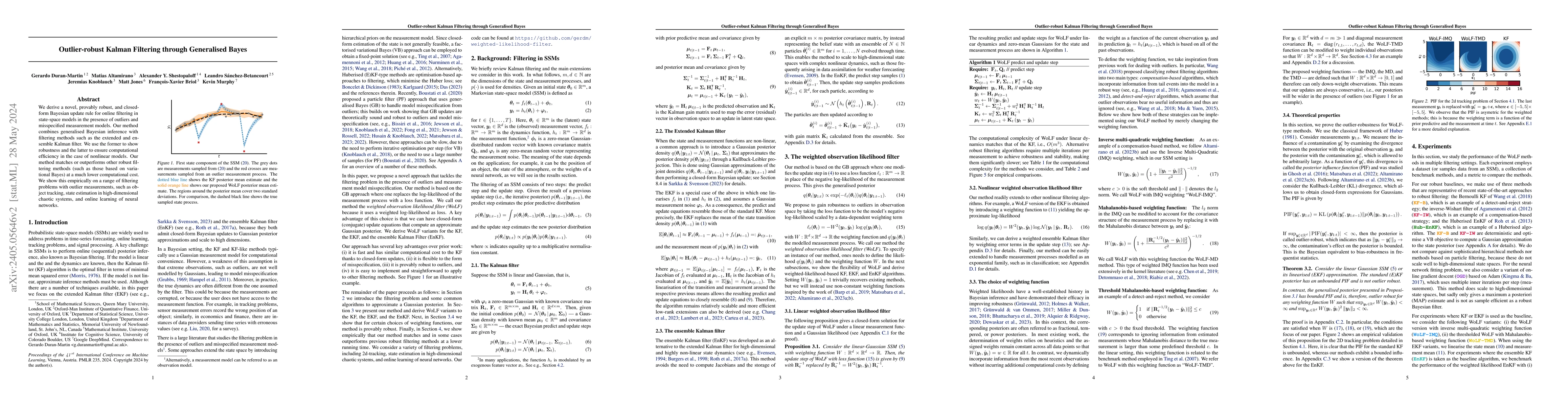

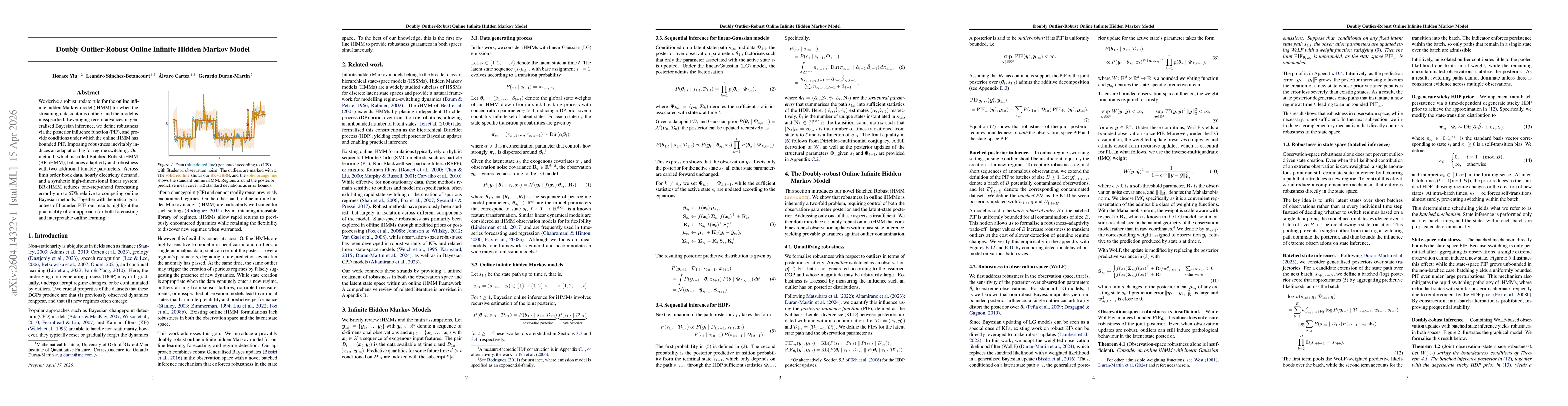

We derive a novel, provably robust, and closed-form Bayesian update rule for online filtering in state-space models in the presence of outliers and misspecified measurement models. Our method combin...

We find closed-form solutions to the stochastic game between a broker and a mean-field of informed traders. In the finite player game, the informed traders observe a common signal and a private sign...

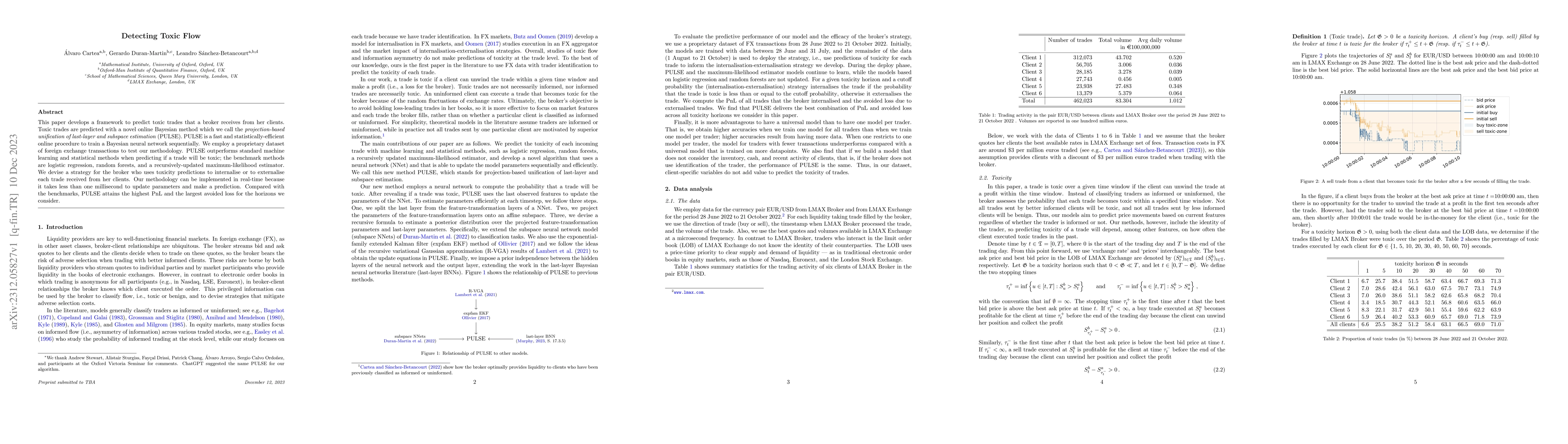

This paper develops a framework to predict toxic trades that a broker receives from her clients. Toxic trades are predicted with a novel online Bayesian method which we call the projection-based uni...

We consider a rational agent who at time $0$ enters into a financial contract for which the payout is determined by a quantum measurement at some time $T>0$. The state of the quantum system is given...

We consider a pair of traders in a market where the information available to the second trader is a strict subset of the information available to the first trader. The traders make prices based on t...

In the information-based pricing framework of Brody, Hughston and Macrina, the market filtration $\{ \mathcal F_t\}_{t\geq 0}$ is generated by an information process $\{ \xi_t\}_{t\geq0}$ defined in...

Latency (i.e., time delay) in electronic markets affects the efficacy of liquidity taking strategies. During the time liquidity takers process information and send marketable limit orders (MLOs) to ...

We propose a unifying framework for methods that perform Bayesian online learning in non-stationary environments. We call the framework BONE, which stands for (B)ayesian (O)nline learning in (N)on-sta...

We study liquidity provision in the presence of exogenous competition. We consider a `reference market maker' who monitors her inventory and the aggregated inventory of the competing market makers. We...

We study the perfect information Nash equilibrium between a broker and her clients -- an informed trader and an uniformed trader. In our model, the broker trades in the lit exchange where trades have ...

We study strategic interactions in a broker-mediated market. A broker provides liquidity to an informed trader and to noise traders while managing inventory in the lit market. The broker and the infor...

We characterise the solutions to a continuous-time optimal liquidity provision problem in a market populated by informed and uninformed traders. In our model, the asset price exhibits fads -- these ar...

We model the trading activity between a broker and her clients (informed and uninformed traders) as an infinite-horizon stochastic control problem. We derive the broker's optimal dealing strategy in c...

We find the equilibrium contract that an automated market maker (AMM) offers to their strategic liquidity providers (LPs) in order to maximize the order flow that gets processed by the venue. Our mode...

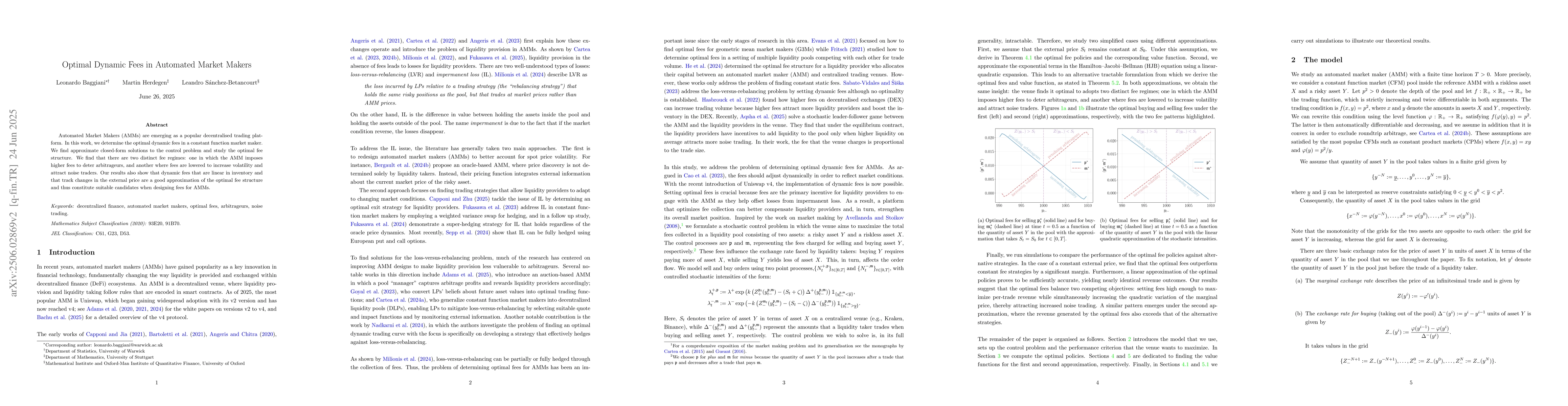

Automated Market Makers (AMMs) are emerging as a popular decentralised trading platform. In this work, we determine the optimal dynamic fees in a constant function market maker. We find approximate cl...

We introduce scalable algorithms for online learning and generalized Bayesian inference of neural network parameters, designed for sequential decision making tasks. Our methods combine the strengths o...

We study the problem of optimal liquidity withdrawal for a representative liquidity provider (LP) in an automated market maker (AMM). LPs earn fees from trading activity but are exposed to impermanent...

We develop a mixed control framework that combines absolutely continuous controls with impulse interventions subject to stochastic execution delays. The model extends current impulse control formulati...

We study a signature-driven numerical scheme to solve multi-dimensional linear-quadratic (LQ) stochastic control problems. Using that linear signature functionals are dense in the natural class of adm...

We derive a robust update rule for the online infinite hidden Markov model (iHMM) for when the streaming data contains outliers and the model is misspecified. Leveraging recent advances in generalised...