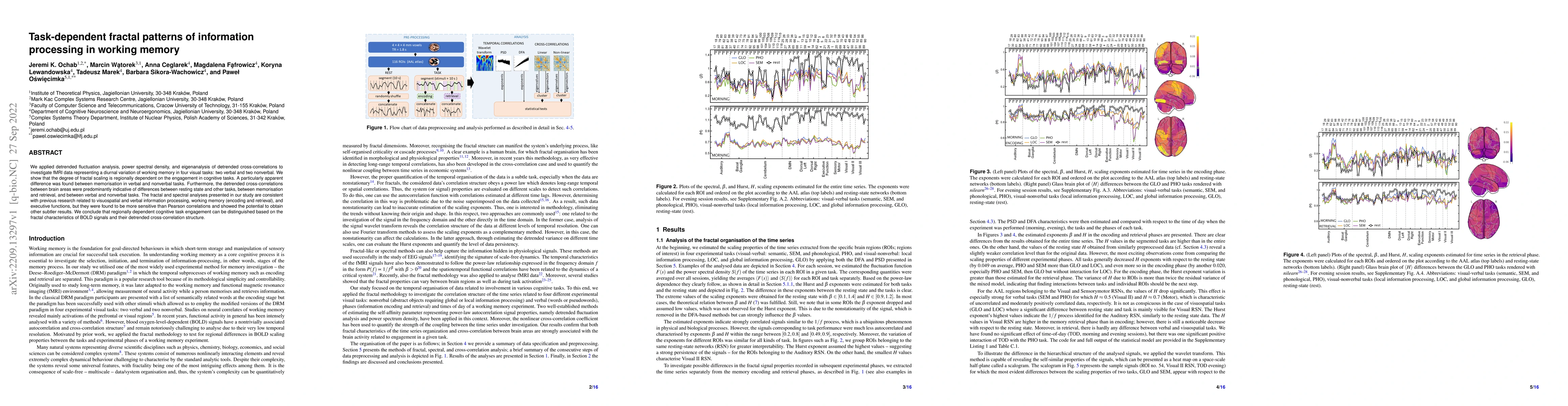

Academic Profile

Statistics

Similar Authors

Papers on arXiv

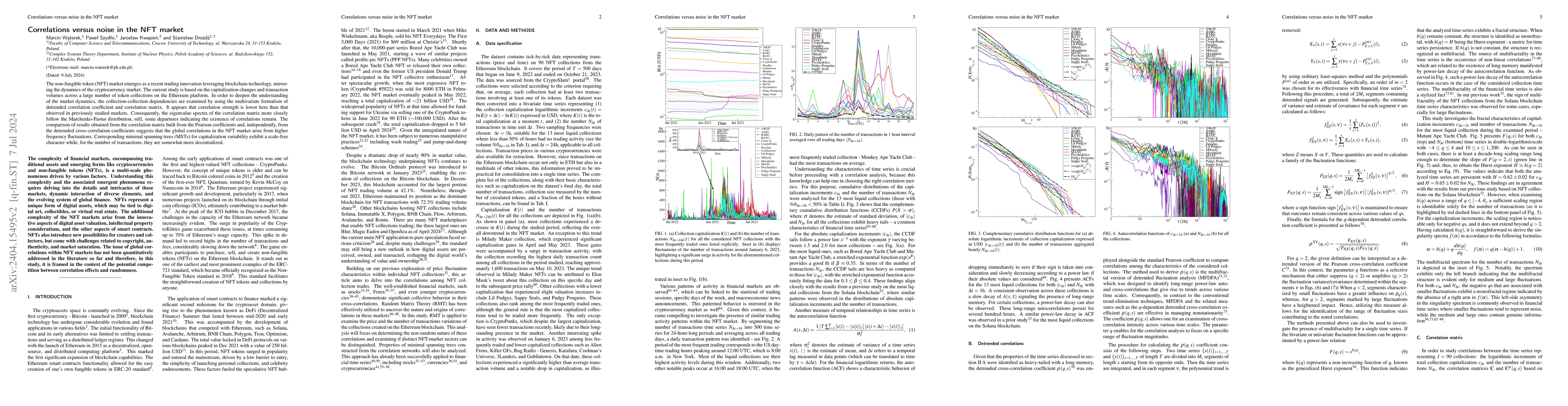

The non-fungible token (NFT) market emerges as a recent trading innovation leveraging blockchain technology, mirroring the dynamics of the cryptocurrency market. The current study is based on the capi...

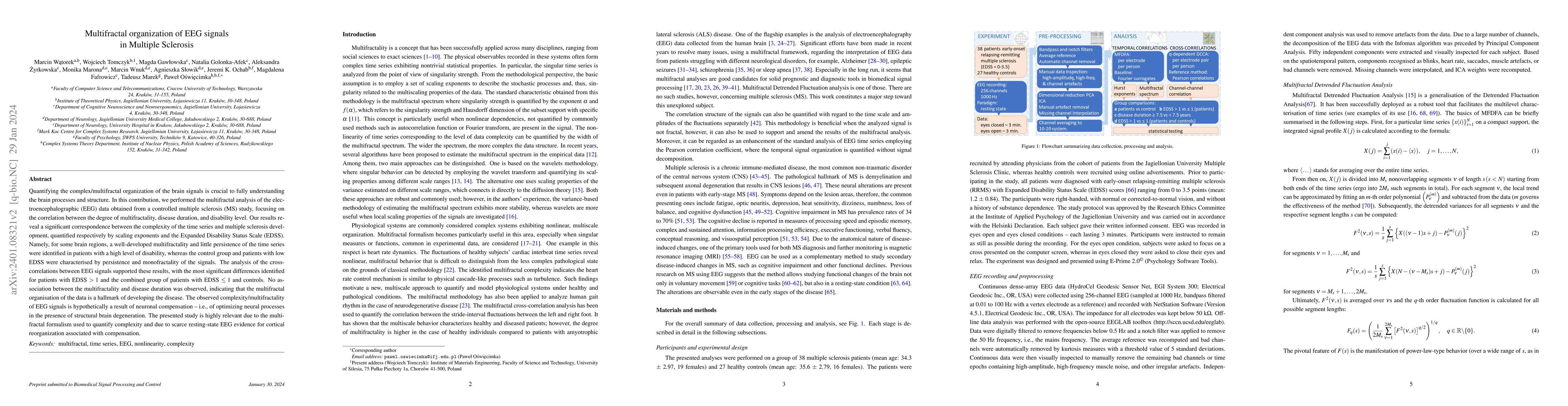

Quantifying the complex/multifractal organization of the brain signals is crucial to fully understanding the brain processes and structure. In this contribution, we performed the multifractal analys...

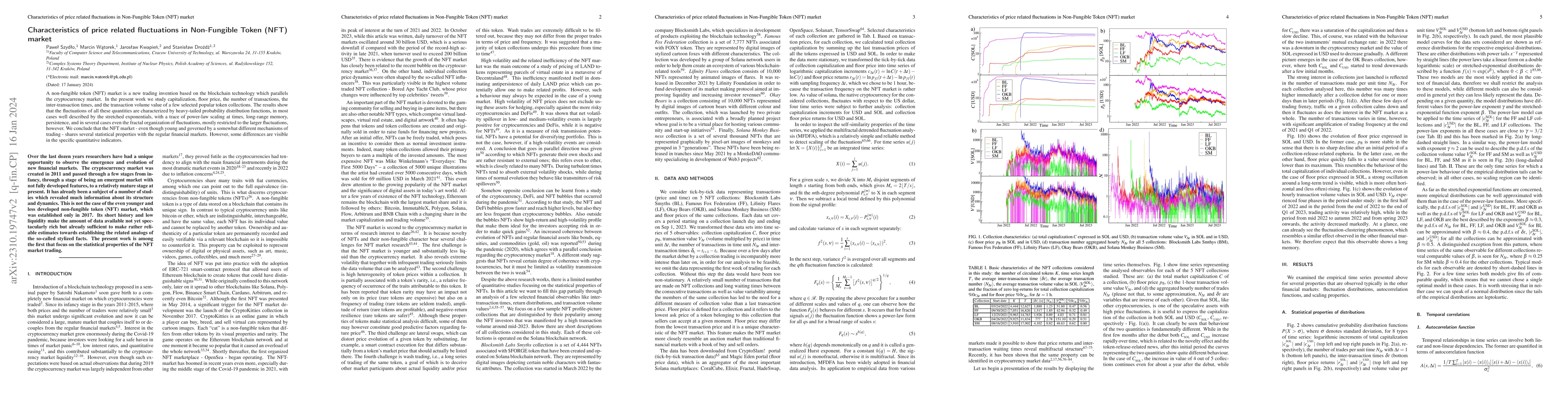

A non-fungible token (NFT) market is a new trading invention based on the blockchain technology which parallels the cryptocurrency market. In the present work we study capitalization, floor price, t...

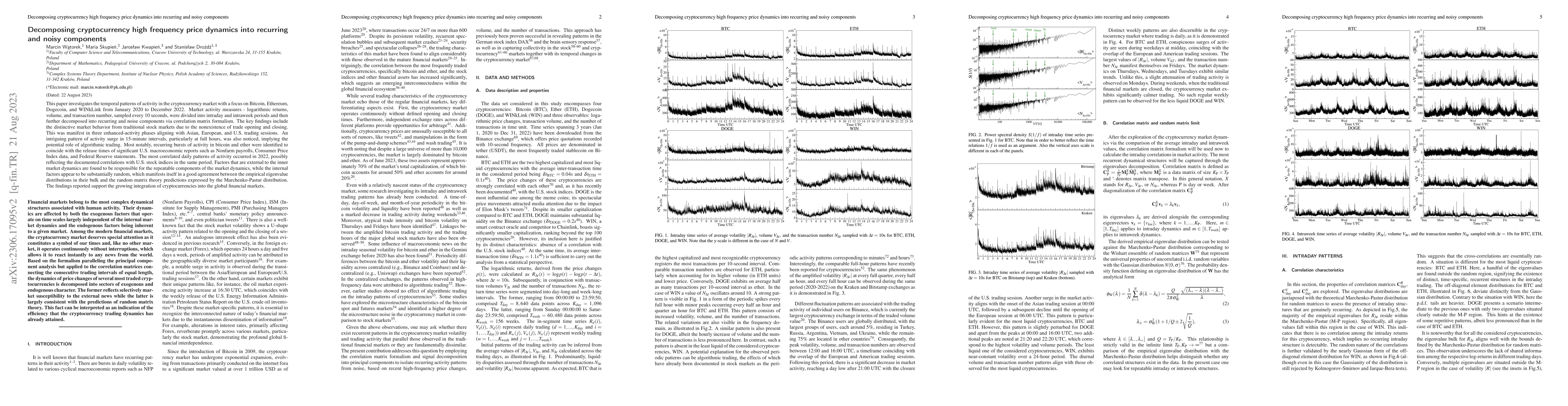

This paper investigates the temporal patterns of activity in the cryptocurrency market with a focus on Bitcoin, Ethereum, Dogecoin, and WINkLink from January 2020 to December 2022. Market activity m...

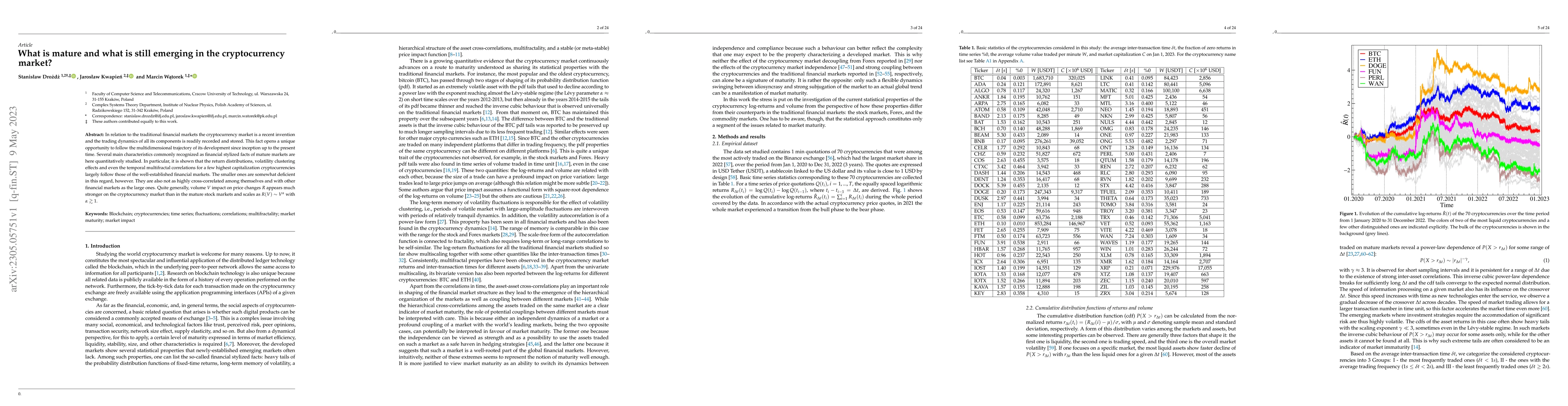

In relation to the traditional financial markets, the cryptocurrency market is a recent invention and the trading dynamics of all its components are readily recorded and stored. This fact opens up a...

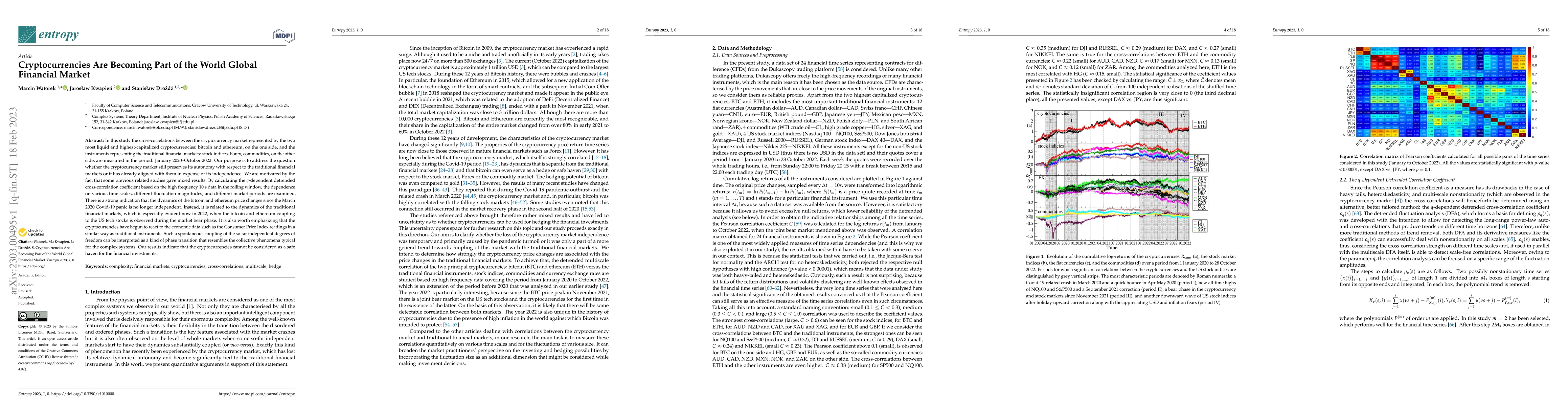

In this study the cross-correlations between the cryptocurrency market represented by the two most liquid and highest-capitalized cryptocurrencies: bitcoin and ethereum, on the one side, and the ins...

We applied detrended fluctuation analysis, power spectral density, and eigenanalysis of detrended cross-correlations to investigate fMRI data representing a diurnal variation of working memory in fo...

Unlike price fluctuations, the temporal structure of cryptocurrency trading has seldom been a subject of systematic study. In order to fill this gap, we analyse detrended correlations of the price r...

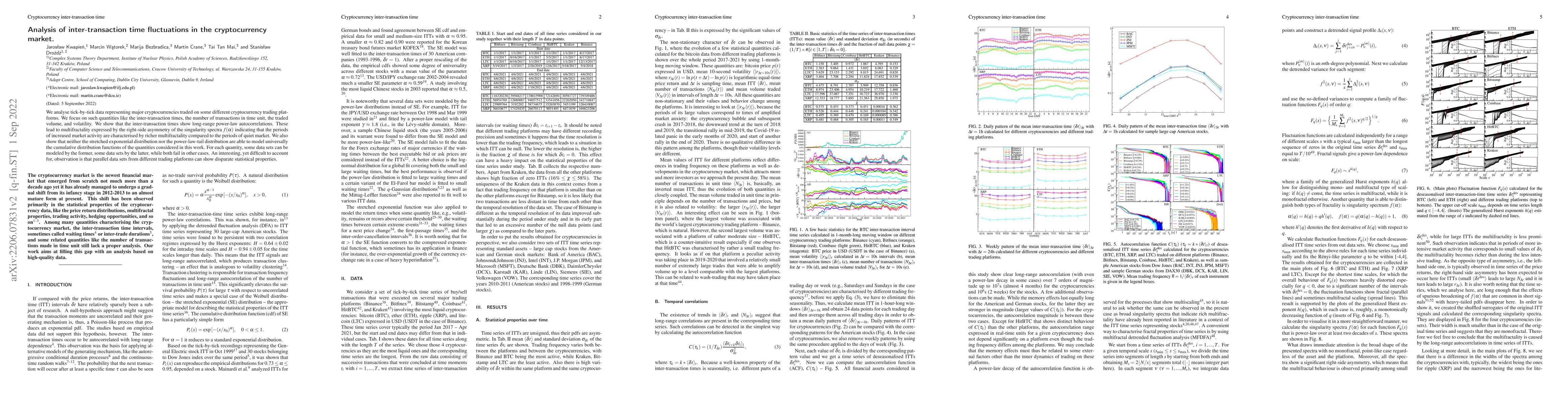

We analyse tick-by-tick data representing major cryptocurrencies traded on some different cryptocurrency trading platforms. We focus on such quantities like the inter-transaction times, the number o...

Time series of price returns for 80 of the most liquid cryptocurrencies listed on Binance are investigated for the presence of detrended cross-correlations. A spectral analysis of the detrended corr...

We analyze the price return distributions of currency exchange rates, cryptocurrencies, and contracts for differences (CFDs) representing stock indices, stock shares, and commodities. Based on recen...

The review introduces the history of cryptocurrencies, offering a description of the blockchain technology behind them. Differences between cryptocurrencies and the exchanges on which they are trade...

Social systems are characterized by an enormous network of connections and factors that can influence the structure and dynamics of these systems. All financial markets, including the cryptocurrency...

This study investigates the multifractality of streamflow data of 192 stations located in 13 river basins in India using the Multifractal Detrended Fluctuation Analysis (MF-DFA). The streamflow data...

Based on the high-frequency recordings from Kraken, a cryptocurrency exchange and professional trading platform that aims to bring Bitcoin and other cryptocurrencies into the mainstream, the multisc...

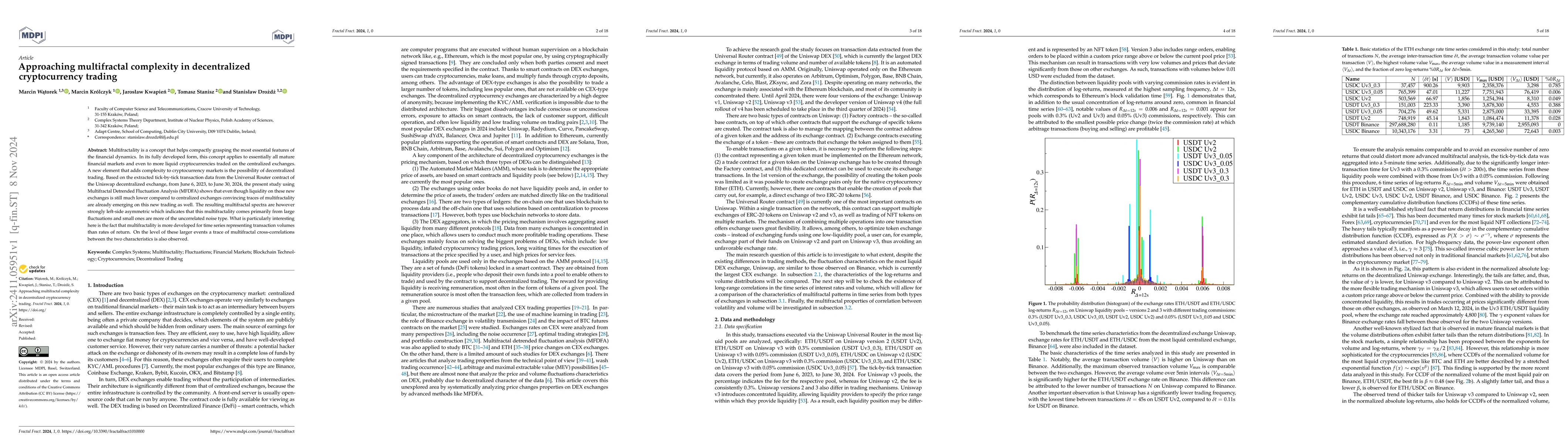

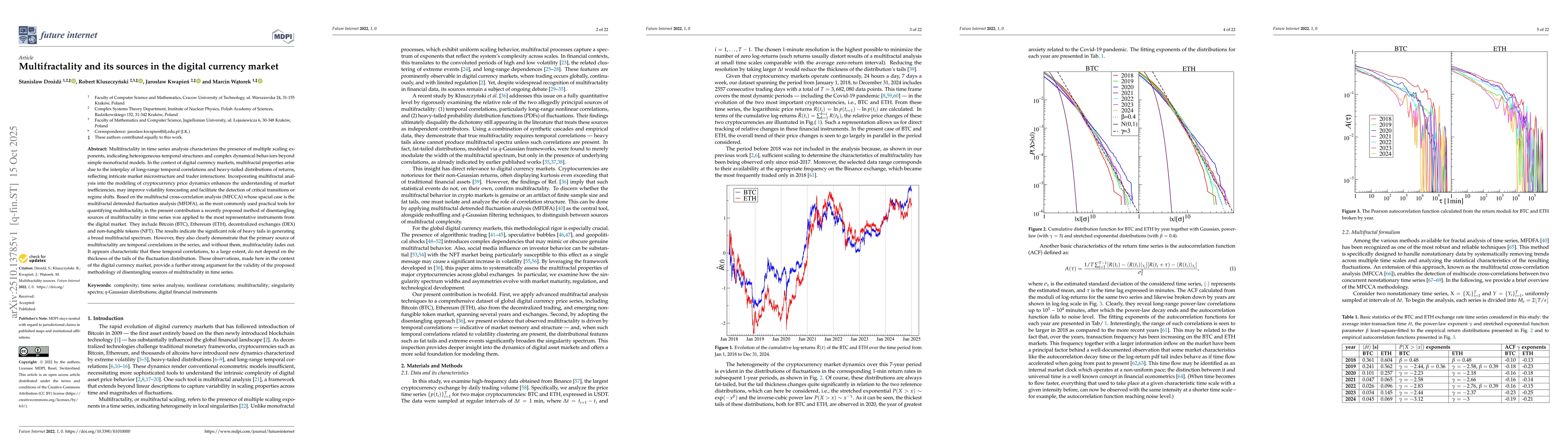

Multifractality is a concept that helps compactly grasping the most essential features of the financial dynamics. In its fully developed form, this concept applies to essentially all mature financial ...

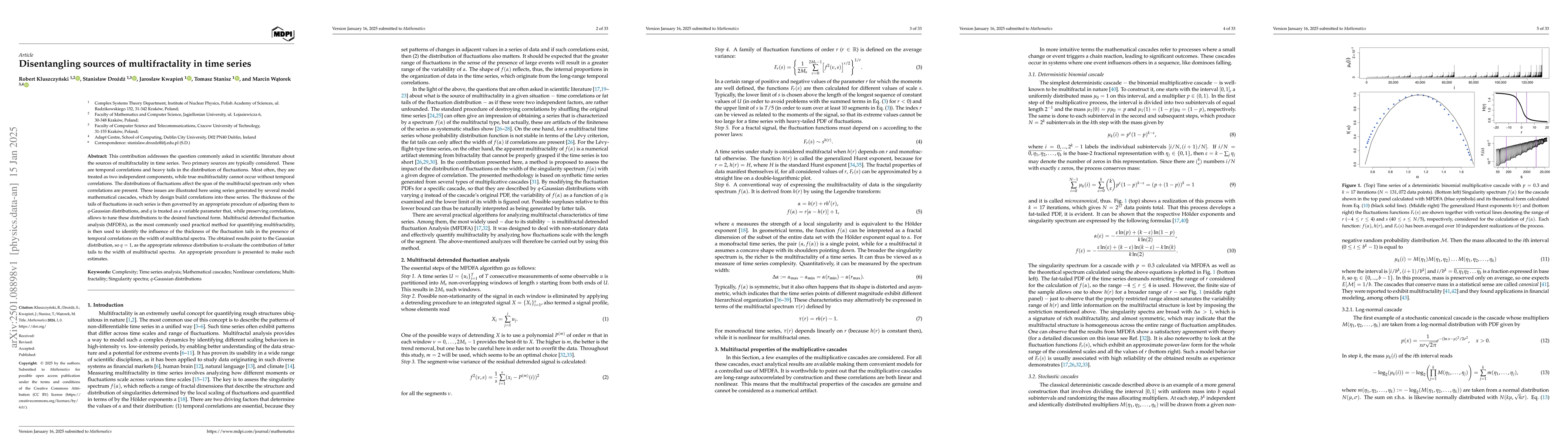

This contribution addresses the question commonly asked in scientific literature about the sources of multifractality in time series. Two primary sources are typically considered. These are temporal c...

Based on the cryptocurrency market dynamics, this study presents a general methodology for analyzing evolving correlation structures in complex systems using the $q$-dependent detrended cross-correlat...

Multifractality in time series analysis characterizes the presence of multiple scaling exponents, indicating heterogeneous temporal structures and complex dynamical behaviors beyond simple monofractal...

Correlations in complex systems are often obscured by nonstationarity, long-range memory, and heavy-tailed fluctuations, which limit the usefulness of traditional covariance-based analyses. To address...