Academic Profile

Statistics

Similar Authors

Papers on arXiv

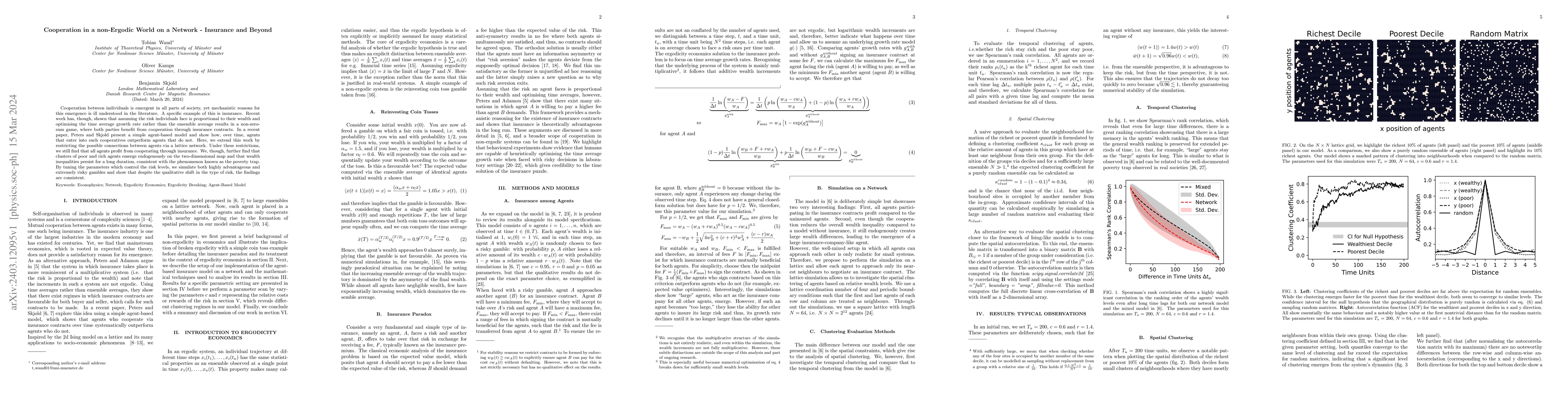

Cooperation between individuals is emergent in all parts of society, yet mechanistic reasons for this emergence is ill understood in the literature. A specific example of this is insurance. Recent w...

The Eocene-Oligocene transition marks a watershed point of earth's climate history. The climate shifts from a greenhouse state to an icehouse state in which Antarctica glaciated for the first time a...

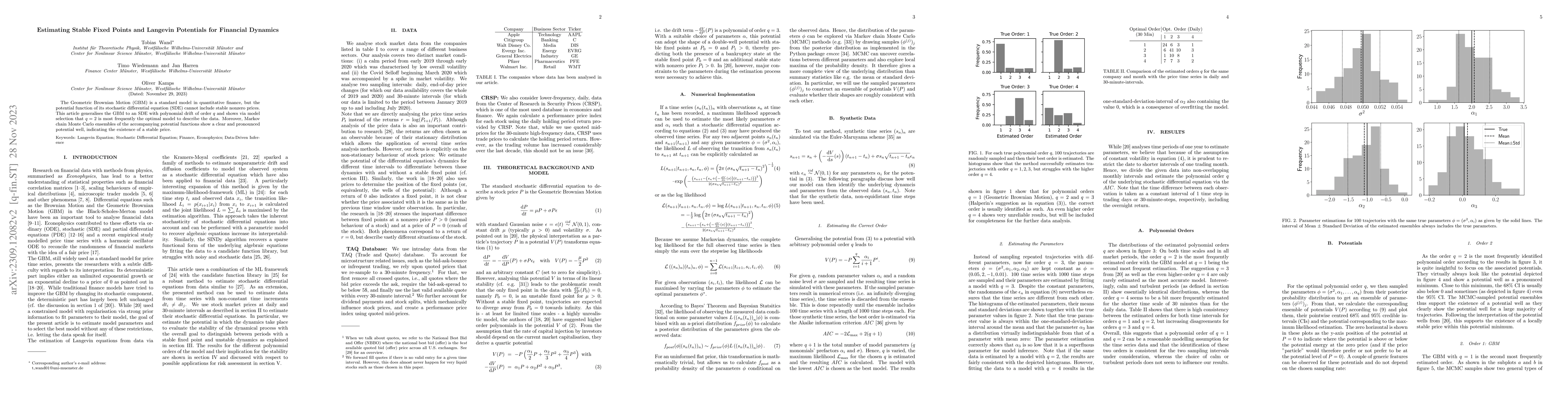

The Geometric Brownian Motion (GBM) is a standard model in quantitative finance, but the potential function of its stochastic differential equation (SDE) cannot include stable nonzero prices. This a...

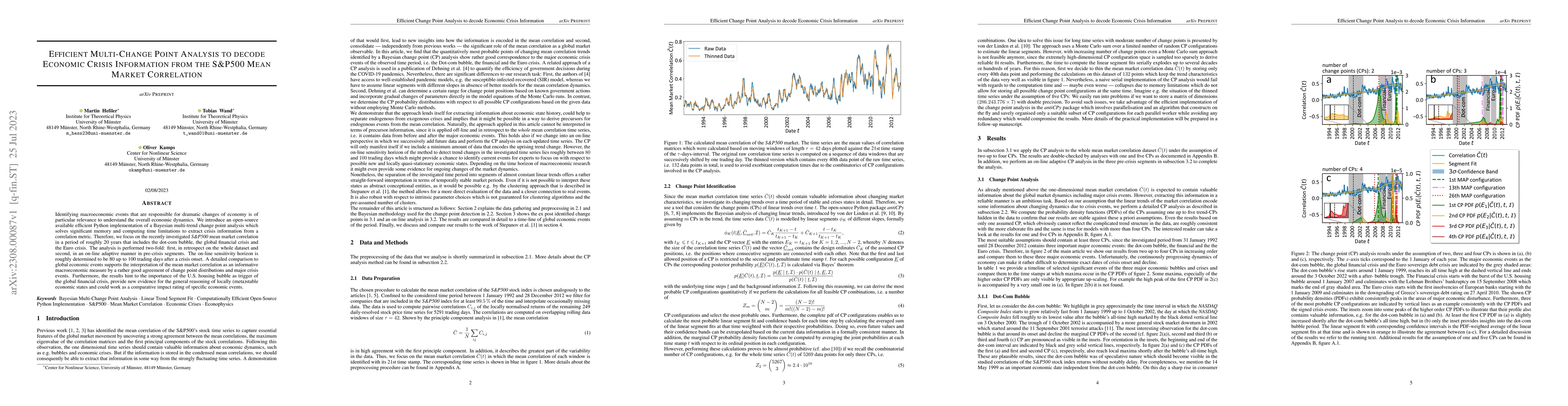

Identifying macroeconomic events that are responsible for dramatic changes of economy is of particular relevance to understand the overall economic dynamics. We introduce an open-source available ef...

The analysis of market correlations is crucial for optimal portfolio selection of correlated assets, but their memory effects have often been neglected. In this work, we analyse the mean market corr...

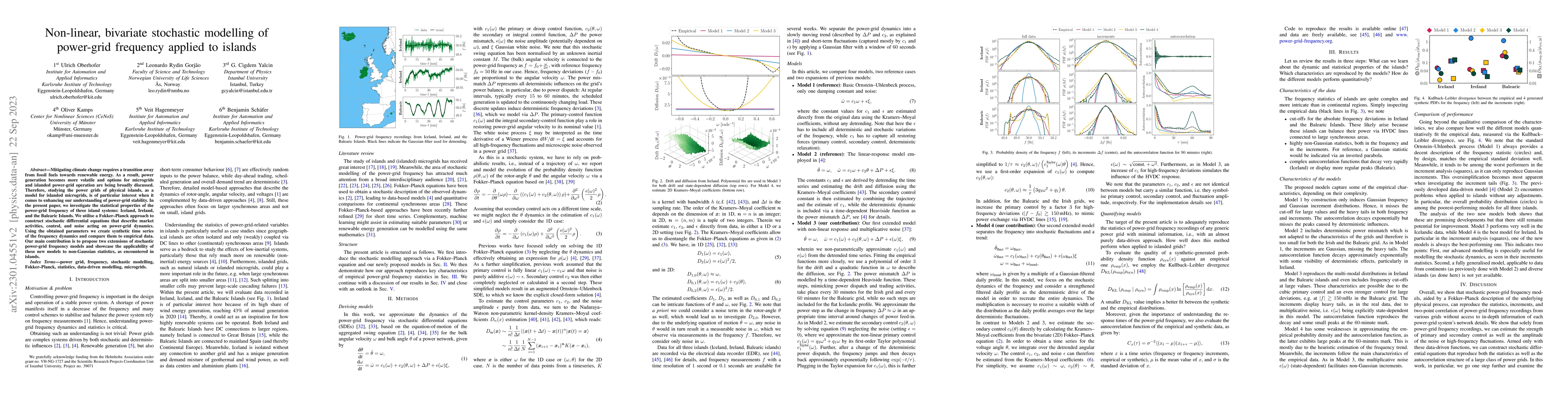

Mitigating climate change requires a transition away from fossil fuels towards renewable energy. As a result, power generation becomes more volatile and options for microgrids and islanded power-gri...

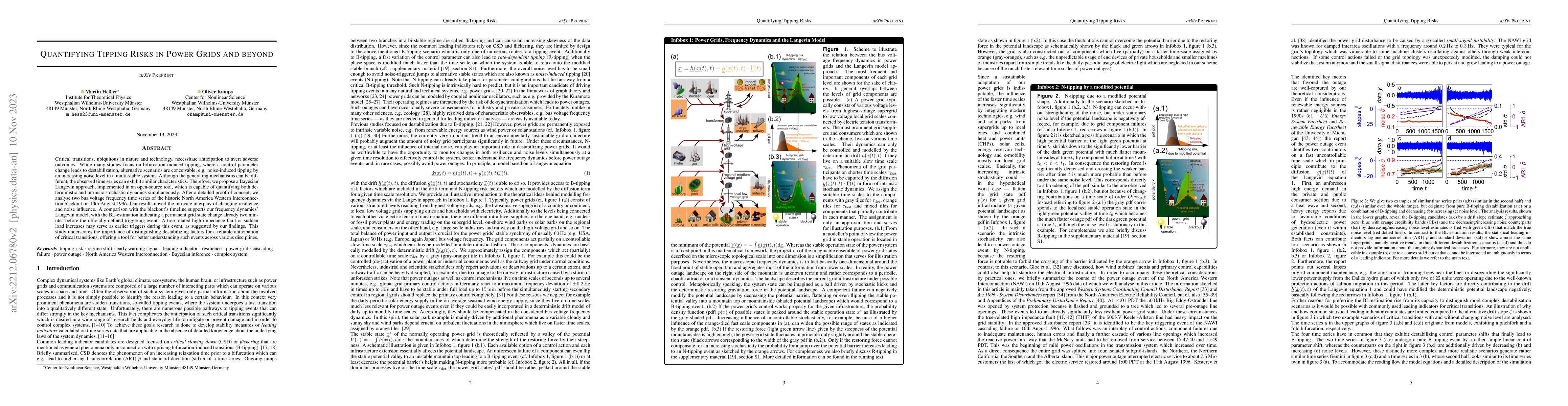

Critical transitions, ubiquitous in nature and technology, necessitate anticipation to avert adverse outcomes. While many studies focus on bifurcation-induced tipping, where a control parameter chan...

Understanding and forecasting changing market conditions in complex economic systems like the financial market is of great importance to various stakeholders such as financial institutions and regul...

Data-driven modeling of non-Markovian dynamics is a recent topic of research with applications in many fields such as climate research, molecular dynamics, biophysics, or wind power modeling. In the...

Early warning indicators often suffer from the shortness and coarse-graining of real-world time series. Furthermore, the typically strong and correlated noise contributions in real applications are ...

The design of reliable indicators to anticipate critical transitions in complex systems is an im portant task in order to detect a coming sudden regime shift and to take action in order to either pr...

Modeling non-Markovian time series is a recent topic of research in many fields such as climate modeling, biophysics, molecular dynamics, or finance. The generalized Langevin equation (GLE), given n...

Langevin models are frequently used to model various stochastic processes in different fields of natural and social sciences. They are adapted to measured data by estimation techniques such as maxim...

In future power systems, electrical storage will be the key technology for balancing feed-in fluctuations. With increasing share of renewables and reduction of system inertia, the focus of research ...

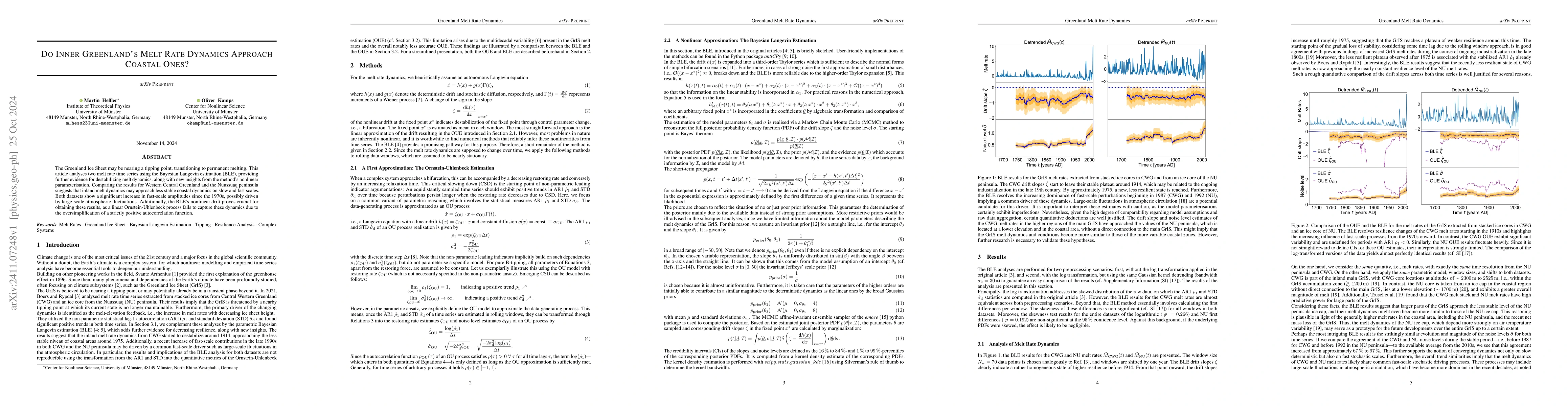

The Greenland Ice Sheet may be nearing a tipping point, transitioning to permanent melting. This article analyses two melt rate time series using the Bayesian Langevin estimation (BLE), providing furt...

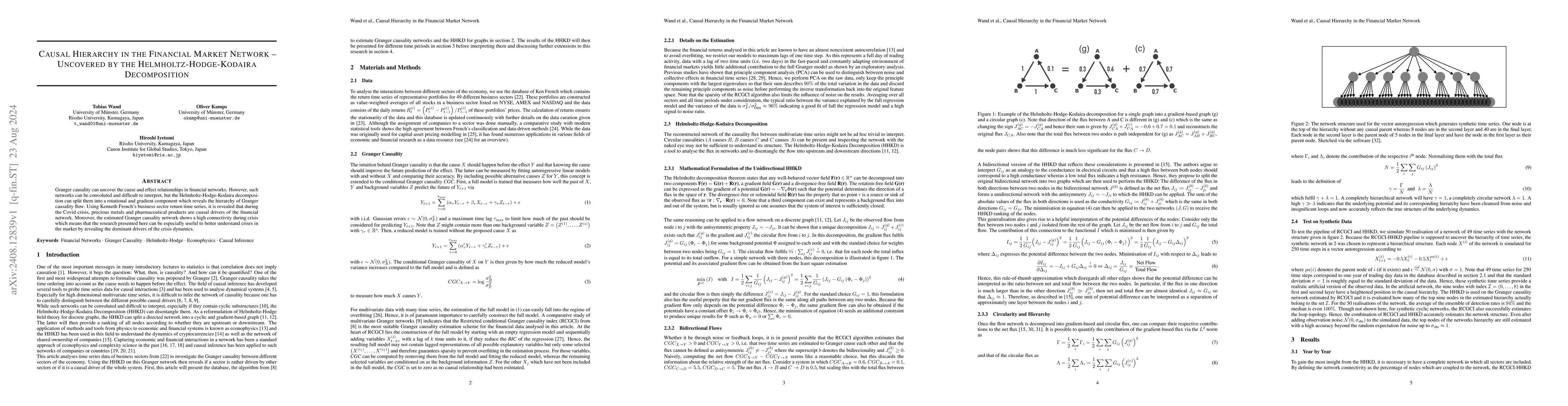

Granger causality can uncover the cause and effect relationships in financial networks. However, such networks can be convoluted and difficult to interpret, but the Helmholtz-Hodge-Kodaira decompositi...

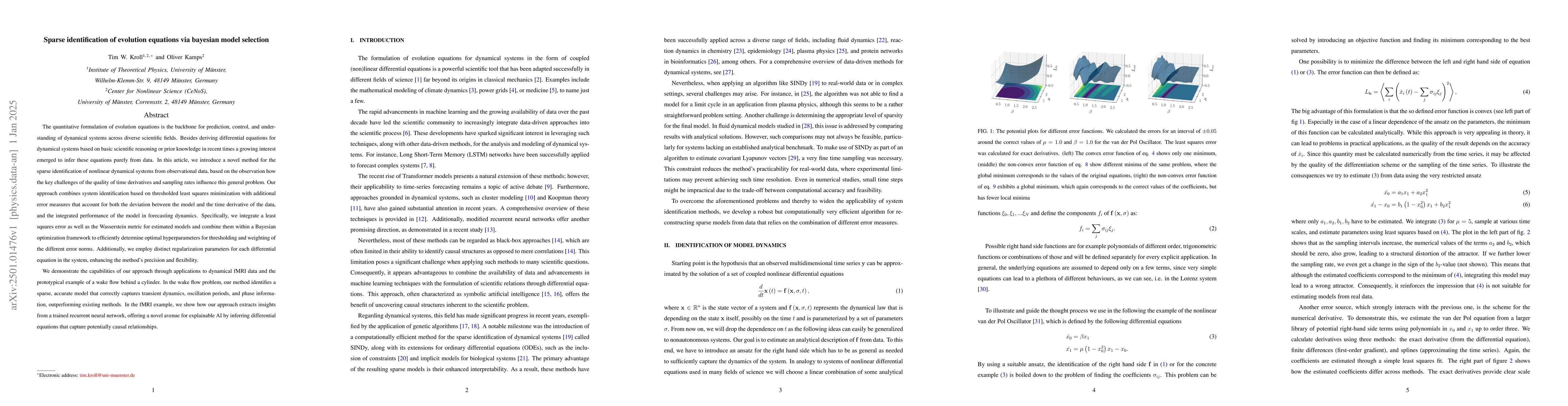

The quantitative formulation of evolution equations is the backbone for prediction, control, and understanding of dynamical systems across diverse scientific fields. Besides deriving differential equa...

We propose an improved method for estimating partial differential equations and delay partial differential equations from data, using Bayesian optimization and the Bayesian information criterion to au...