Academic Profile

Statistics

Similar Authors

Papers on arXiv

We study the role of contextual information in the online learning problem of brokerage between traders. At each round, two traders arrive with secret valuations about an asset they wish to trade. T...

In online bilateral trade, a platform posts prices to incoming pairs of buyers and sellers that have private valuations for a certain good. If the price is lower than the buyers' valuation and highe...

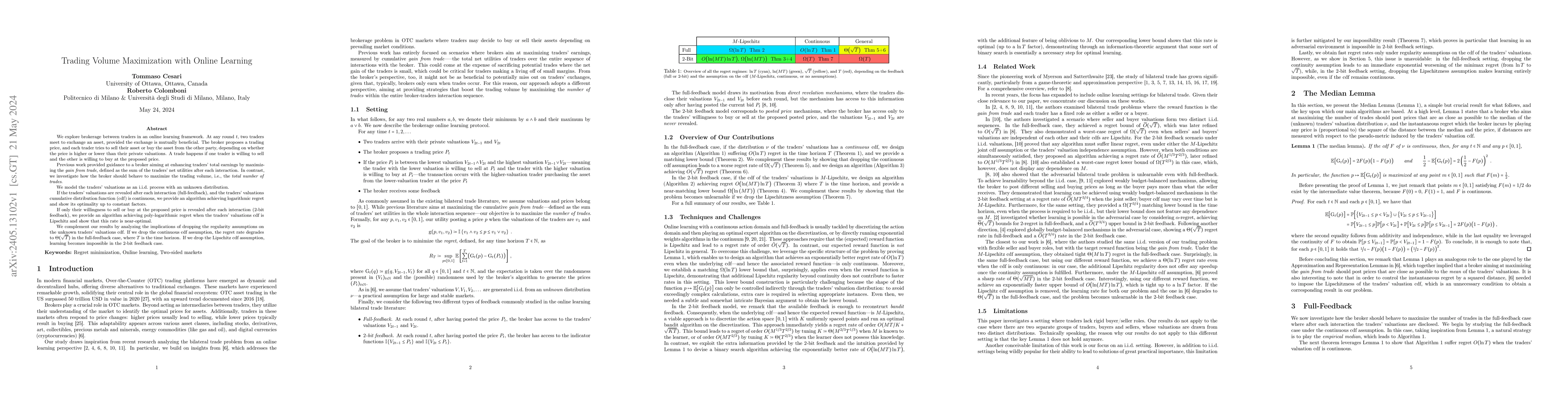

We explore brokerage between traders in an online learning framework. At any round $t$, two traders meet to exchange an asset, provided the exchange is mutually beneficial. The broker proposes a tra...

We investigate brokerage between traders from an online learning perspective. At any round $t$, two traders arrive with their private valuations, and the broker proposes a trading price. Unlike othe...

We consider the problem of repeatedly choosing policies to maximize social welfare. Welfare is a weighted sum of private utility and public revenue. Earlier outcomes inform later policies. Utility i...

We study the problem of regret minimization for a single bidder in a sequence of first-price auctions where the bidder discovers the item's value only if the auction is won. Our main contribution is...

The fat-shattering dimension characterizes the uniform convergence property of real-valued functions. The state-of-the-art upper bounds feature a multiplicative squared logarithmic factor on the sam...

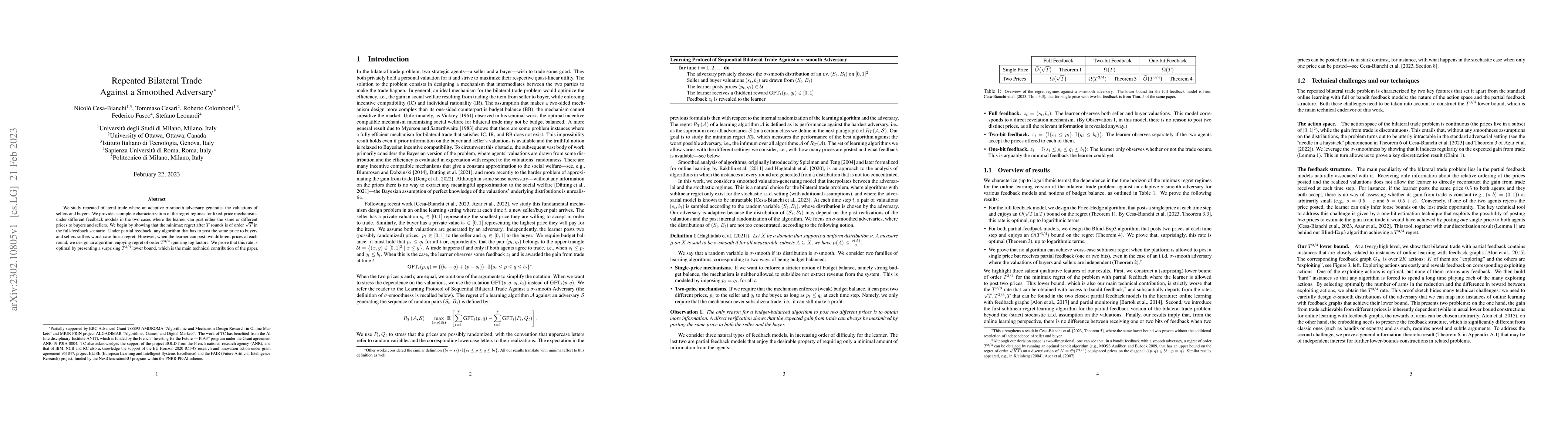

We study repeated bilateral trade where an adaptive $\sigma$-smooth adversary generates the valuations of sellers and buyers. We provide a complete characterization of the regret regimes for fixed-p...

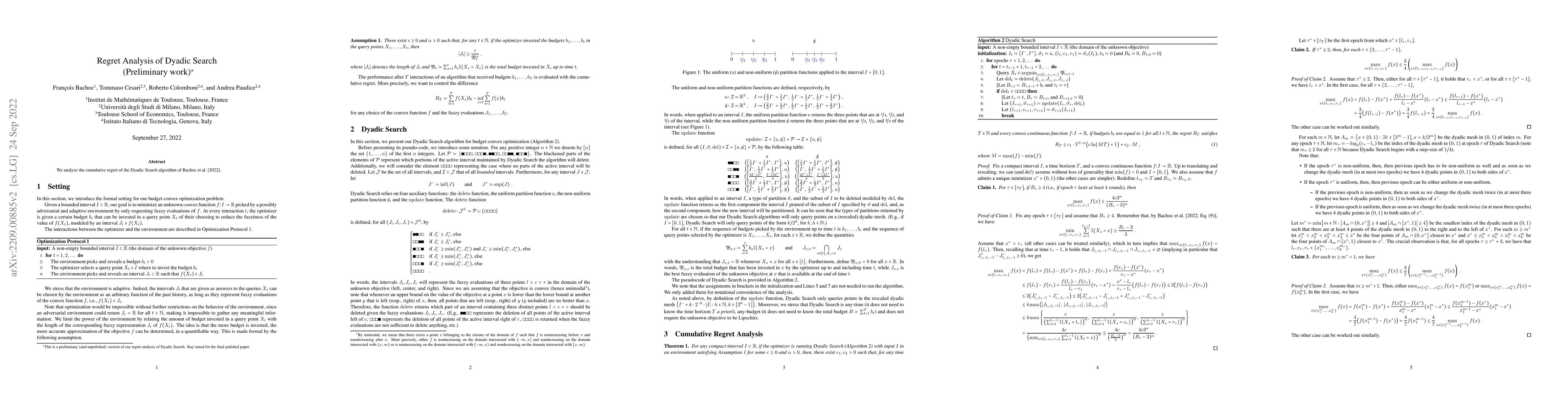

We analyze the cumulative regret of the Dyadic Search algorithm of Bachoc et al. [2022].

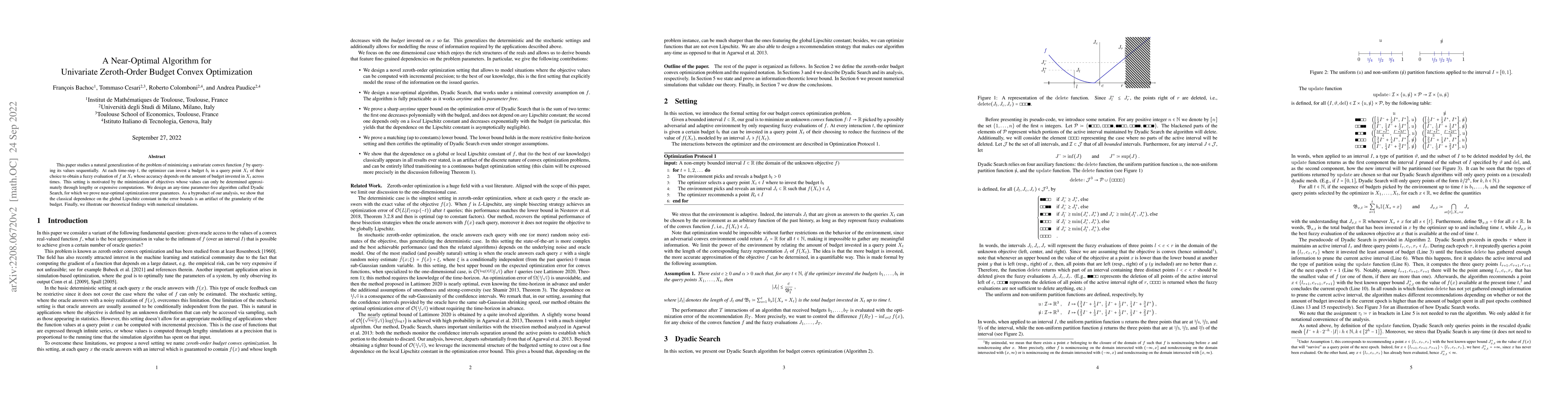

This paper studies a natural generalization of the problem of minimizing a univariate convex function $f$ by querying its values sequentially. At each time-step $t$, the optimizer can invest a budge...

We investigate a nonstochastic bandit setting in which the loss of an action is not immediately charged to the player, but rather spread over the subsequent rounds in an adversarial way. The instant...

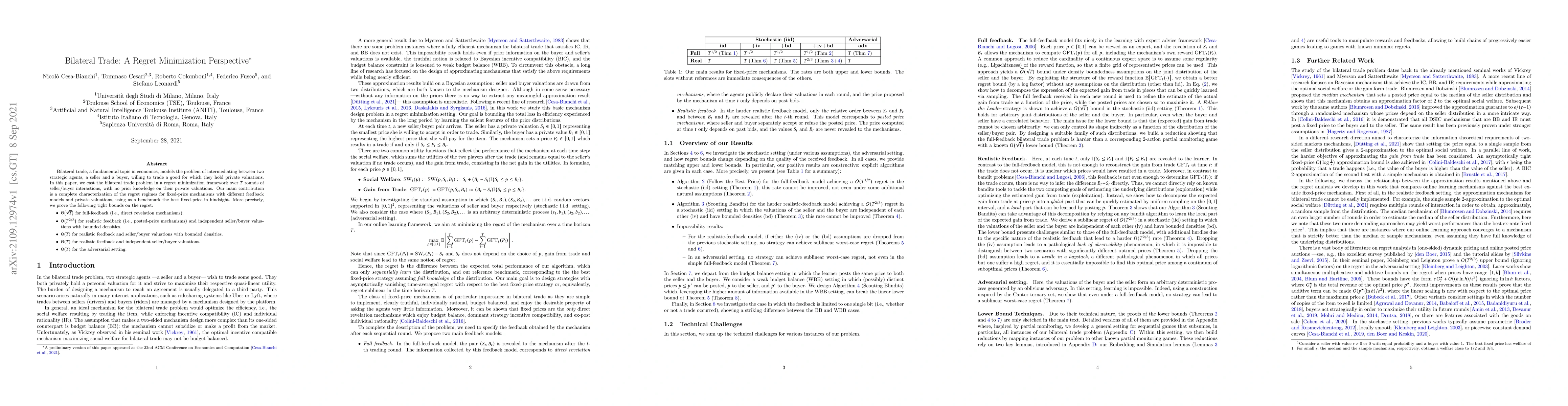

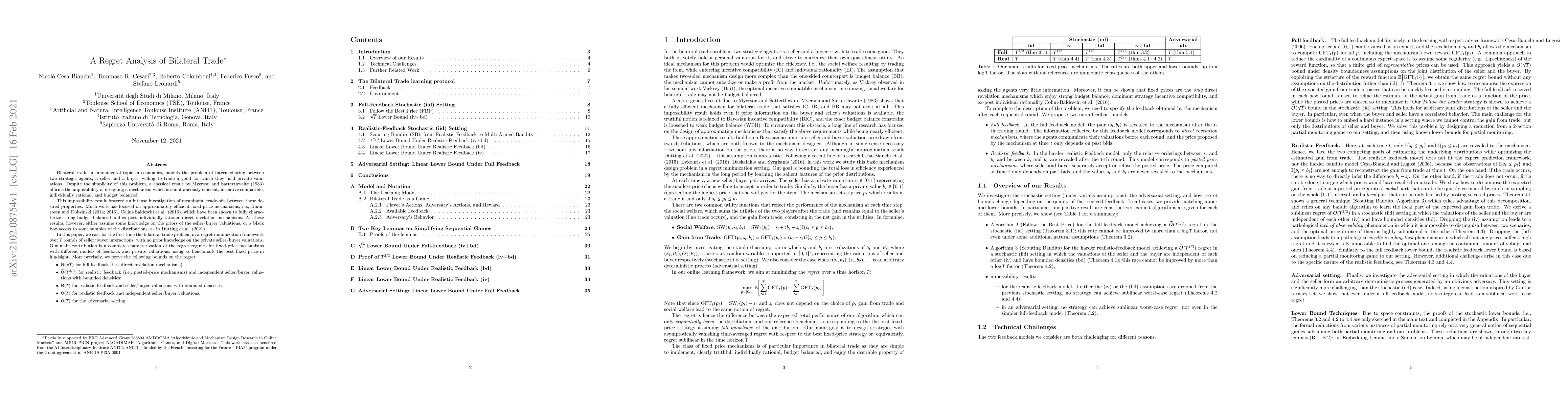

Bilateral trade, a fundamental topic in economics, models the problem of intermediating between two strategic agents, a seller and a buyer, willing to trade a good for which they hold private valuat...

Bilateral trade, a fundamental topic in economics, models the problem of intermediating between two strategic agents, a seller and a buyer, willing to trade a good for which they hold private valuat...

We consider a sequential decision-making setting where, at every round $t$, a market maker posts a bid price $B_t$ and an ask price $A_t$ to an incoming trader (the taker) with a private valuation for...

We study a contextual version of the repeated brokerage problem. In each interaction, two traders with private valuations for an item seek to buy or sell based on the learner's-a broker-proposed price...

Motivated by applications in crowdsourcing, where a fixed sum of money is split among $K$ workers, and autobidding, where a fixed budget is used to bid in $K$ simultaneous auctions, we define a stocha...

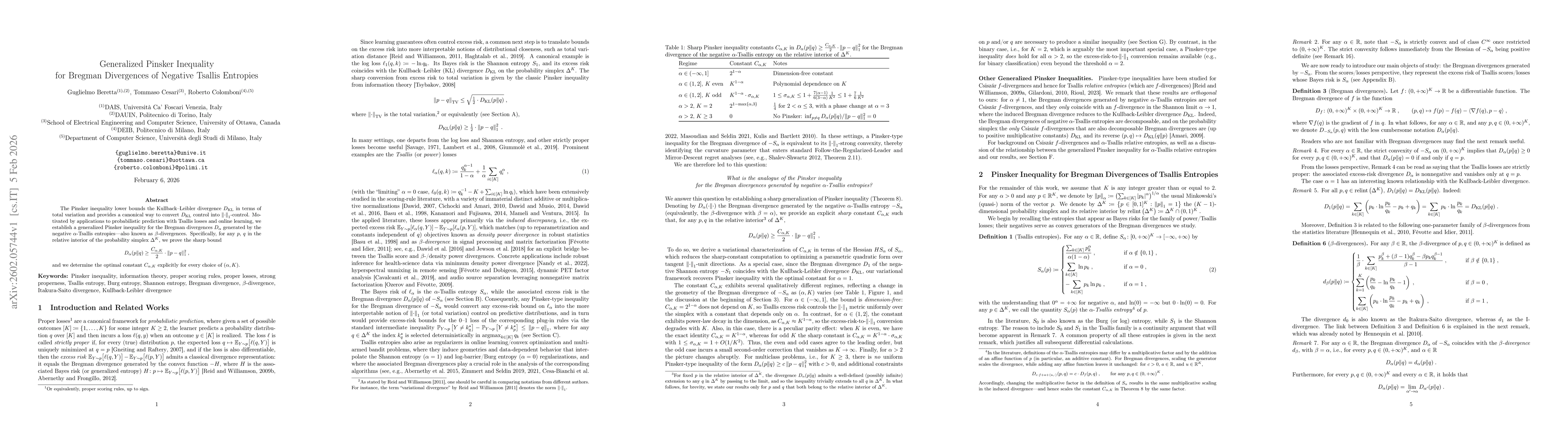

The Pinsker inequality lower bounds the Kullback--Leibler divergence $D_{\textrm{KL}}$ in terms of total variation and provides a canonical way to convert $D_{\textrm{KL}}$ control into $\lVert \cdot ...

We study stochastic decision-theoretic online learning with full information and event-level pure differential privacy. A COLT open problem of Hu and Mehta asks to determine the optimal gap-dependent ...

We study the two-action apple-tasting problem with switching costs against an oblivious adversary. In an equivalent normalized formulation, at each round the learner chooses between a revealing action...

We study repeated bilateral trade from a fairness perspective. At each round, a fresh seller-buyer pair arrives, and the platform posts a price before observing the traders' valuations. Trade occurs o...

We study the last iterate of the stochastic subgradient method for one-dimensional convex Lipschitz objectives. For a fixed horizon $n$, we consider the standard fixed stepsizes $η=Θ(1/\sqrt n)$. We p...

We prove an effective-resistance bound for fixed-rank external-field measures. Let $d\ge2$ be an integer, let $m\in\{1,\ldots,d-1\}$. Let $w\in(0,+\infty)^d$, and let $\mathsf S$ be an $m$-element ran...

We study the last iterate of the subGradient Method (sGM) for convex Lipschitz objectives defined on $\mathbb R^2$. We prove that for a finite horizon $n$ and a constant stepsize $η= Θ(1/\sqrt{n})$, t...

In information design, an informed sender aims to influence a receiver's decision by committing to a signaling scheme. However, optimal signaling schemes often rely on randomization or assign the same...