Academic Profile

Statistics

Similar Authors

Papers on arXiv

We study the class of continuous polynomial Volterra processes, which we define as solutions to stochastic Volterra equations driven by a continuous semimartingale with affine drift and quadratic di...

Signature stochastic differential equations (SDEs) constitute a large class of stochastic processes, here driven by Brownian motions, whose characteristics are entire or real-analytic functions of t...

We consider a stochastic volatility model where the dynamics of the volatility are described by linear functions of the (time extended) signature of a primary underlying process, which is supposed t...

We introduce a framework that allows to employ (non-negative) measure-valued processes for energy market modeling, in particular for electricity and gas futures. Interpreting the process' spatial st...

We consider asset price models whose dynamics are described by linear functions of the (time extended) signature of a primary underlying process, which can range from a (market-inferred) Brownian mo...

We introduce a class of measure-valued processes, which -- in analogy to their finite dimensional counterparts -- will be called measure-valued polynomial diffusions. We show the so-called moment fo...

We consider a class of stochastic control problems where the state process is a probability measure-valued process satisfying an additional martingale condition on its dynamics, called measure-value...

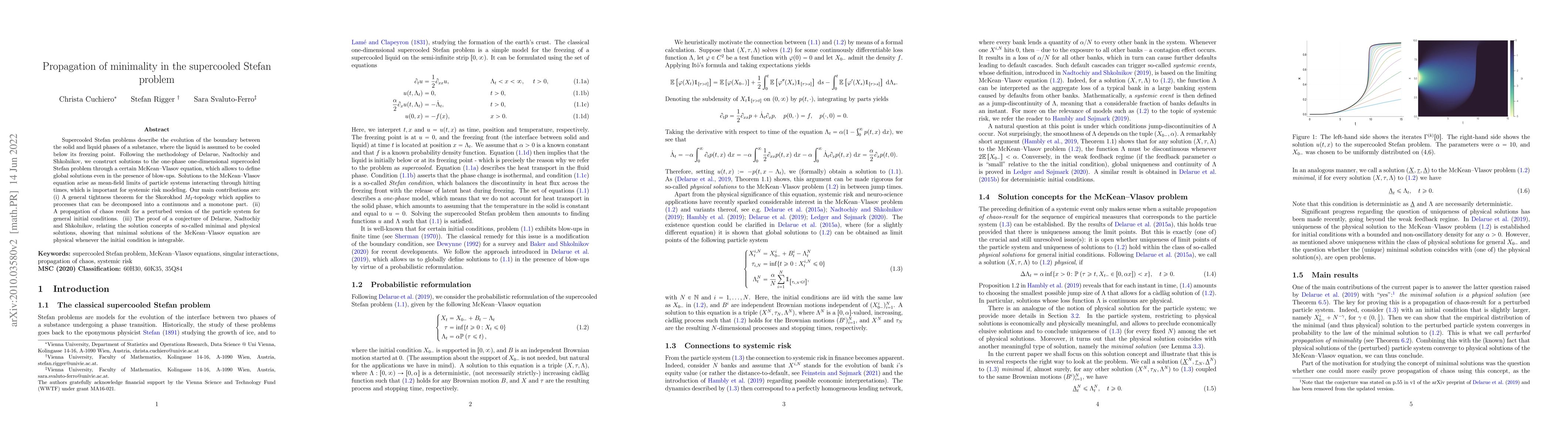

Supercooled Stefan problems describe the evolution of the boundary between the solid and liquid phases of a substance, where the liquid is assumed to be cooled below its freezing point. Following th...

We introduce polynomial processes taking values in an arbitrary Banach space $B$ via their infinitesimal generator $L$ and the associated martingale problem. We obtain two representations of the (co...

We introduce a class of jump-diffusions, called holomorphic, of which the well-known classes of affine and polynomial processes are particular instances. The defining property concerns the extended ge...

We study the local (in time) expansion of a continuous-time process and its conditional moments, including the process' characteristic function. The expansions are conducted by using the properties of...