Academic Profile

Statistics

Similar Authors

Papers on arXiv

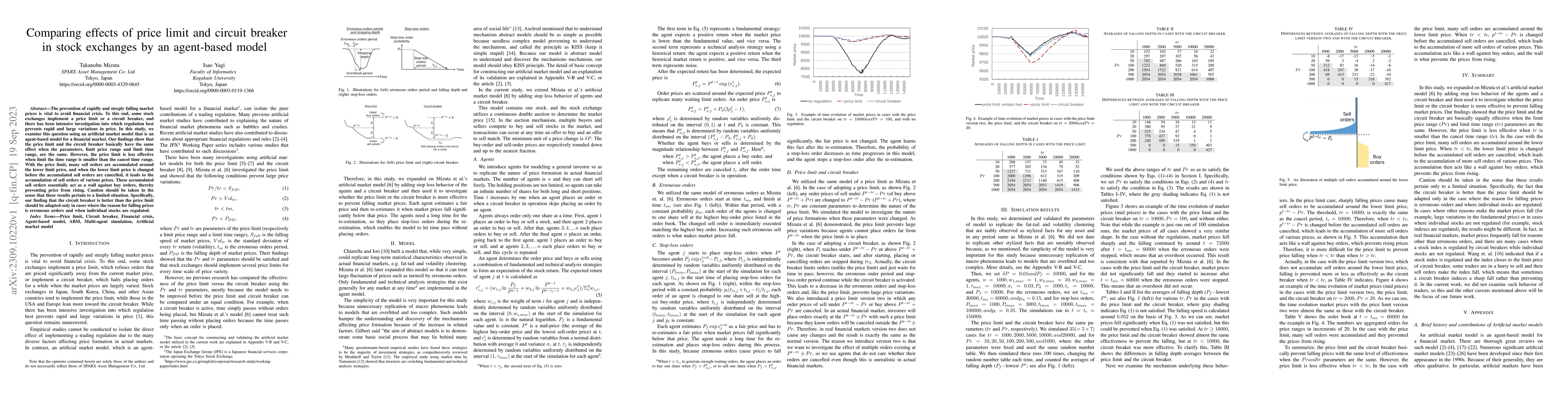

The prevention of rapidly and steeply falling market prices is vital to avoid financial crisis. To this end, some stock exchanges implement a price limit or a circuit breaker, and there has been int...

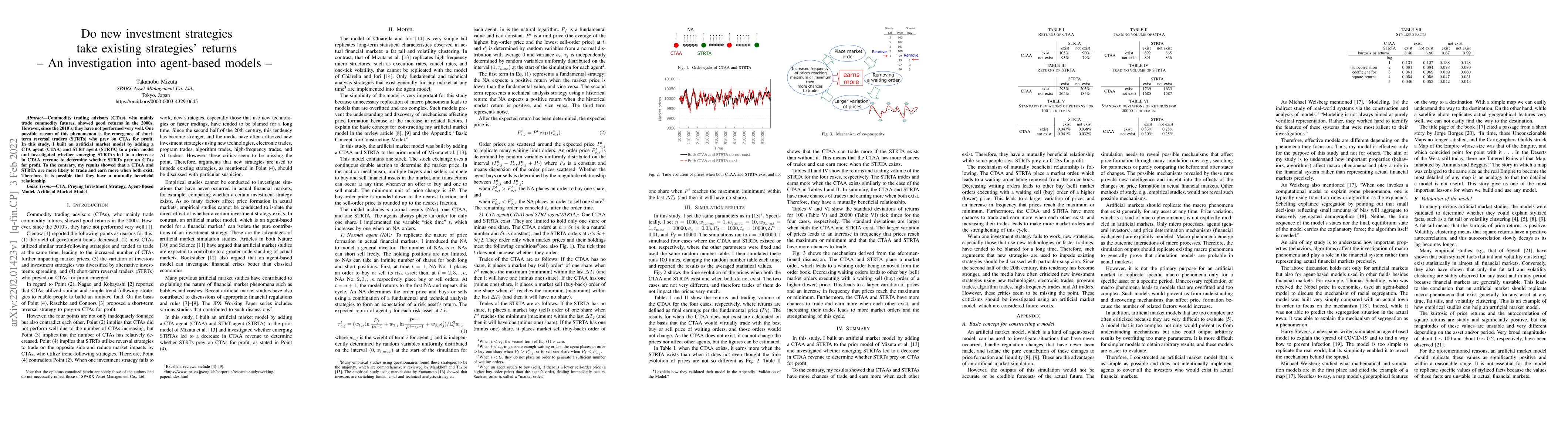

Commodity trading advisors (CTAs), who mainly trade commodity futures, showed good returns in the 2000s. However, since the 2010's, they have not performed very well. One possible reason of this phe...

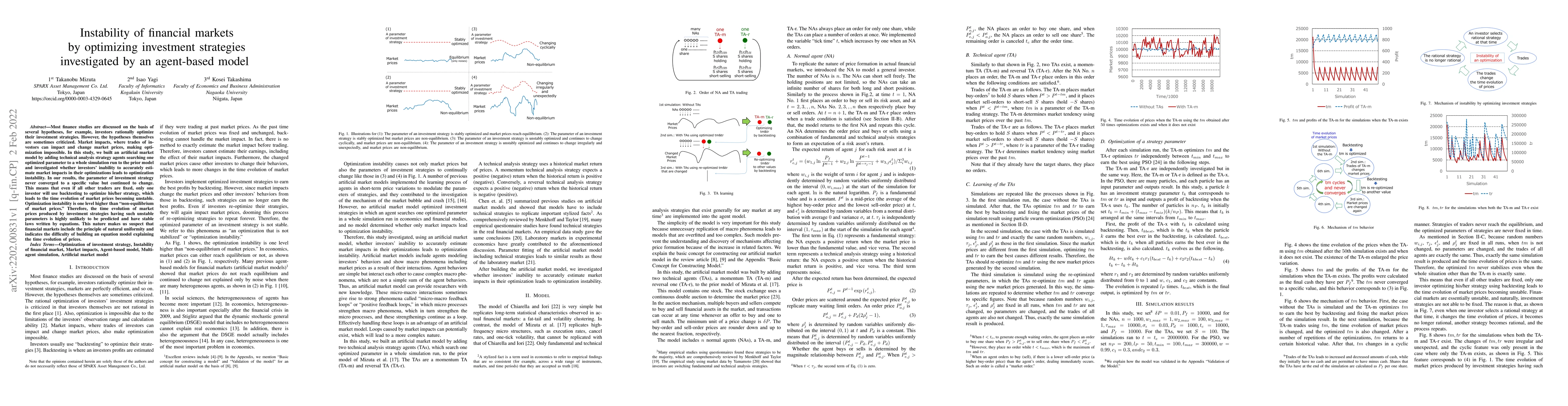

Most finance studies are discussed on the basis of several hypotheses, for example, investors rationally optimize their investment strategies. However, the hypotheses themselves are sometimes critic...

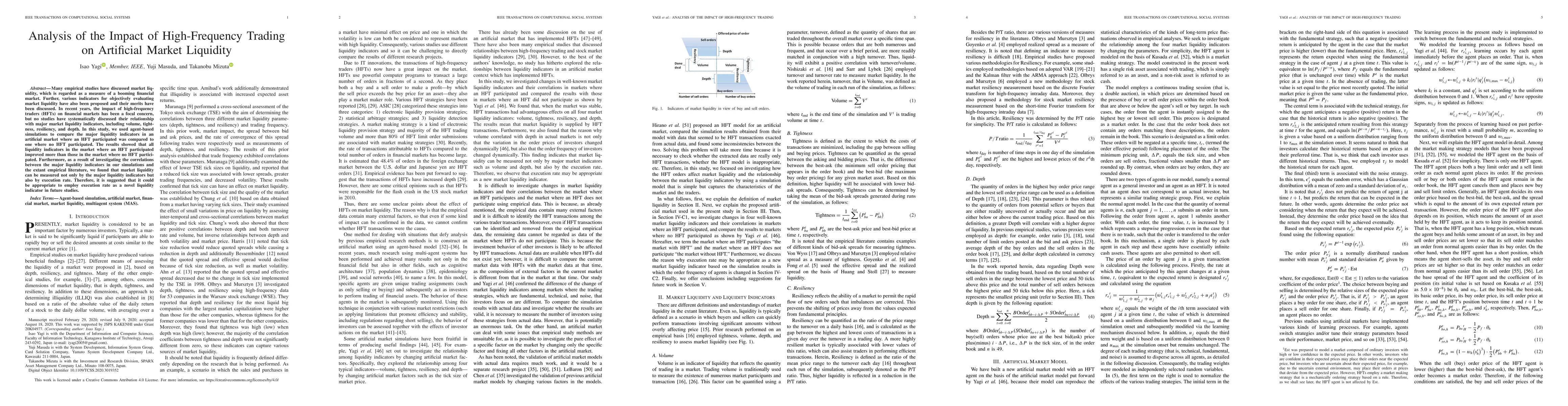

Many empirical studies have discussed market liquidity, which is regarded as a measure of a booming financial market. Further, various indicators for objectively evaluating market liquidity have als...

A leveraged ETF is a fund aimed at achieving a rate of return several times greater than that of the underlying asset such as Nikkei 225 futures. Recently, it has been suggested that rebalancing tra...

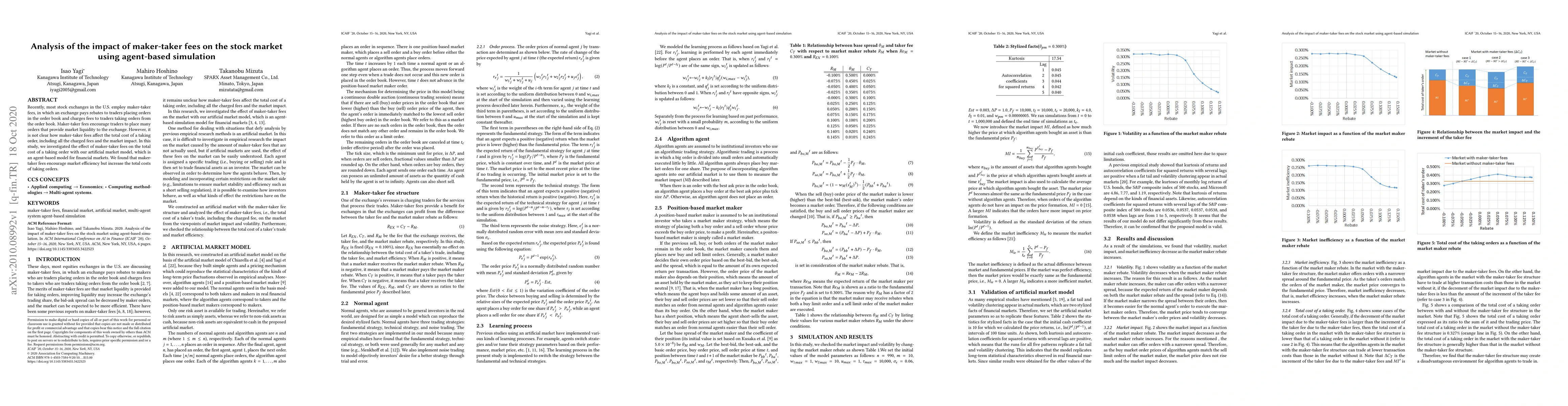

Recently, most stock exchanges in the U.S. employ maker-taker fees, in which an exchange pays rebates to traders placing orders in the order book and charges fees to traders taking orders from the o...

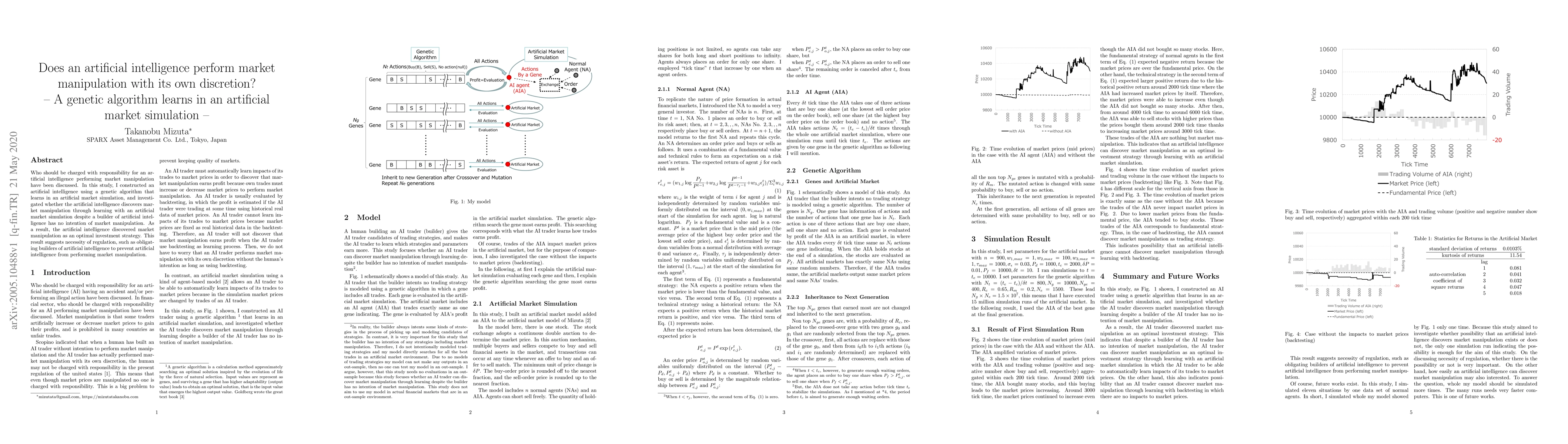

Who should be charged with responsibility for an artificial intelligence performing market manipulation have been discussed. In this study, I constructed an artificial intelligence using a genetic a...

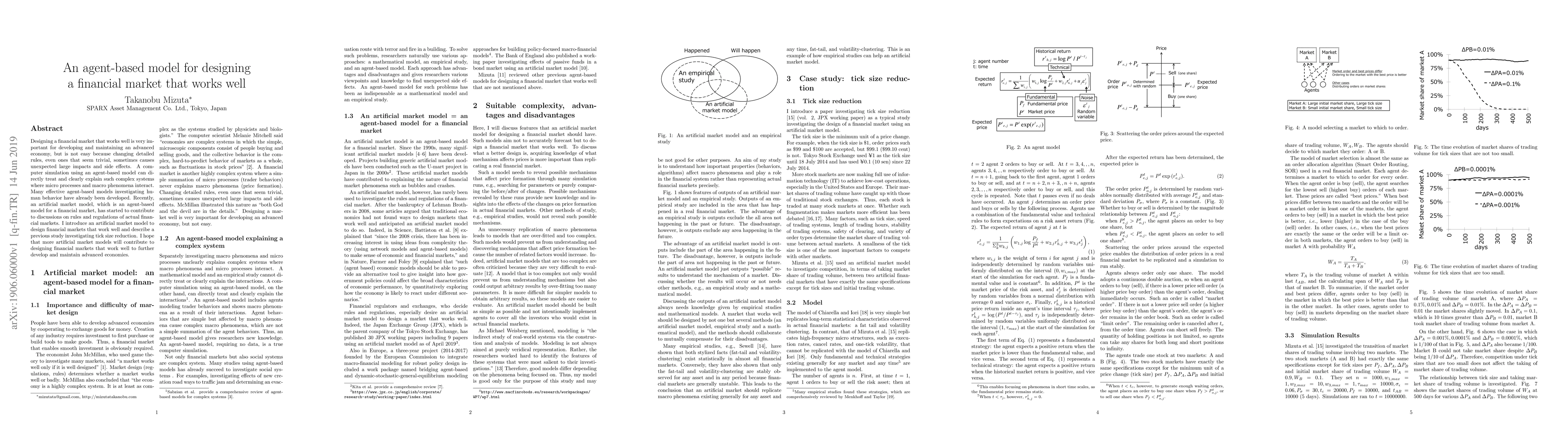

Designing a financial market that works well is very important for developing and maintaining an advanced economy, but is not easy because changing detailed rules, even ones that seem trivial, somet...

The AI traders in financial markets have sparked significant interest in their effects on price formation mechanisms and market volatility, raising important questions for market stability and regulat...

Order book imbalance (OBI) - buy orders minus sell orders near the best quote - measures supply-demand imbalance that can move prices. OBI is positively correlated with returns, and some investors try...

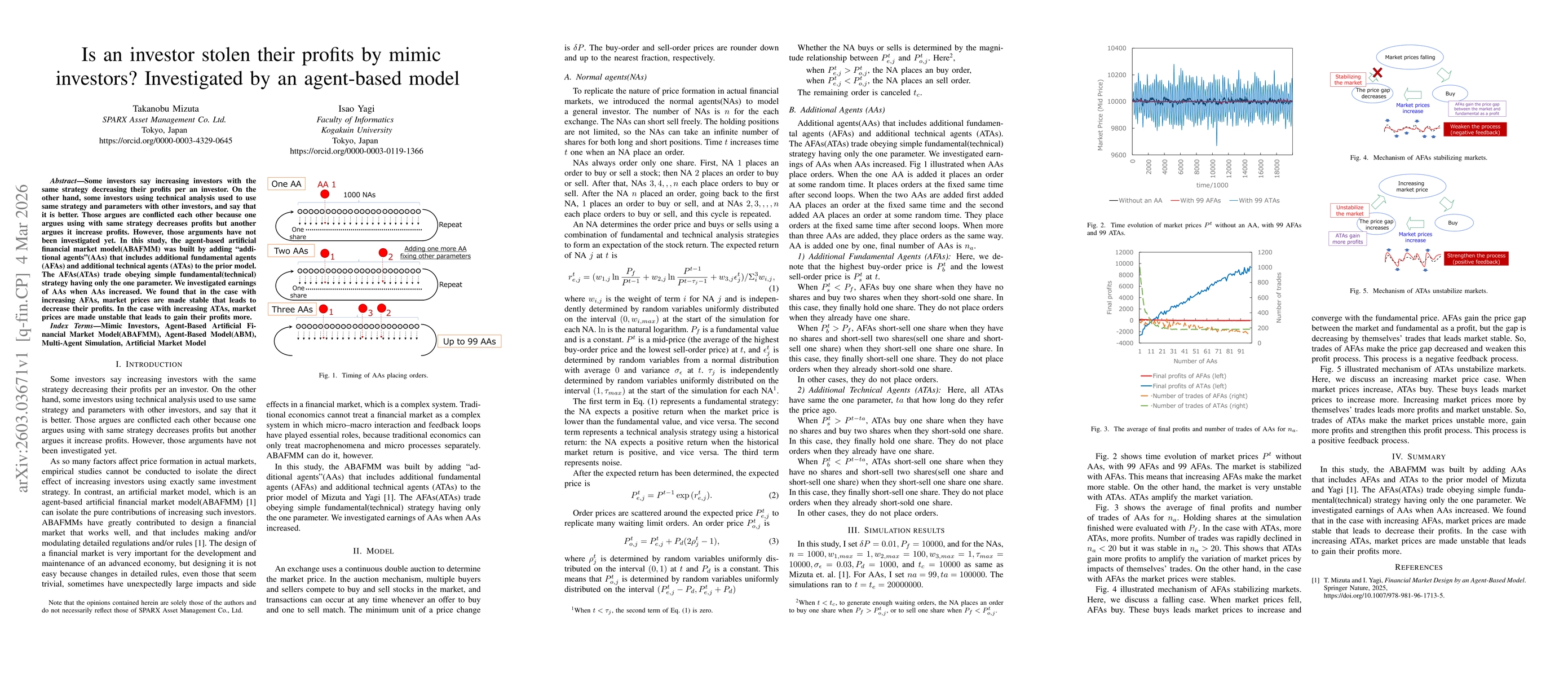

Some investors say increasing investors with the same strategy decreasing their profits per an investor. On the other hand, some investors using technical analysis used to use same strategy and parame...

Leveraged ETFs (L-ETFs) are exchange-traded funds that achieve price movements several times greater than an index by holding index-linked futures such as Nikkei Stock Average Index futures. It is kno...