Academic Profile

Statistics

Similar Authors

Papers on arXiv

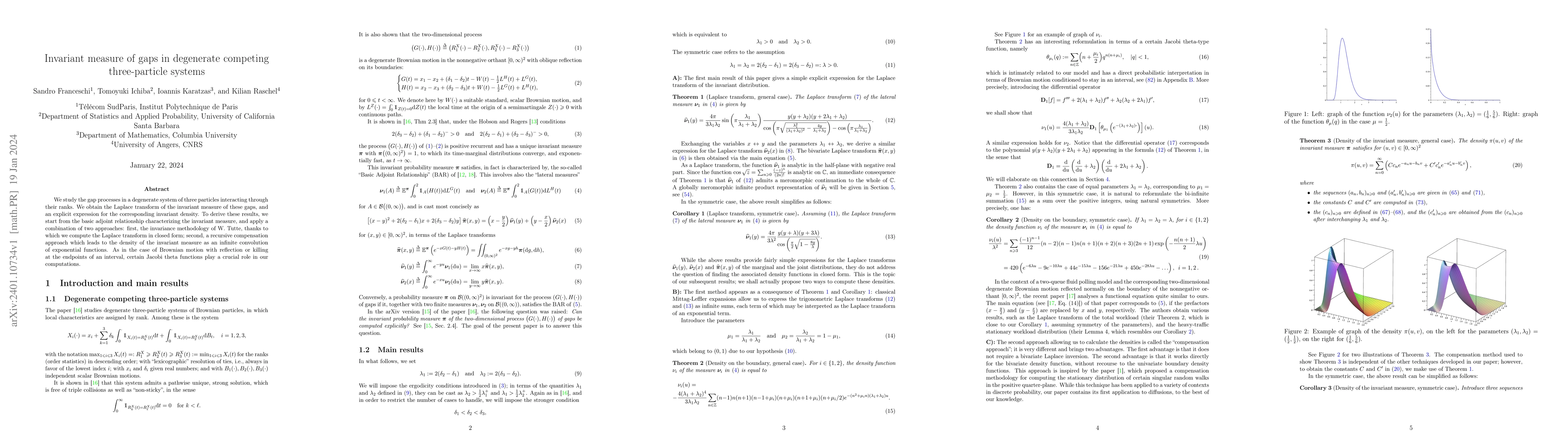

We study the gap processes in a degenerate system of three particles interacting through their ranks. We obtain the Laplace transform of the invariant measure of these gaps, and an explicit expressi...

This paper studies relative arbitrage opportunities in a market with infinitely many interacting investors. We establish a conditional McKean-Vlasov system to study the market dynamics coupled with ...

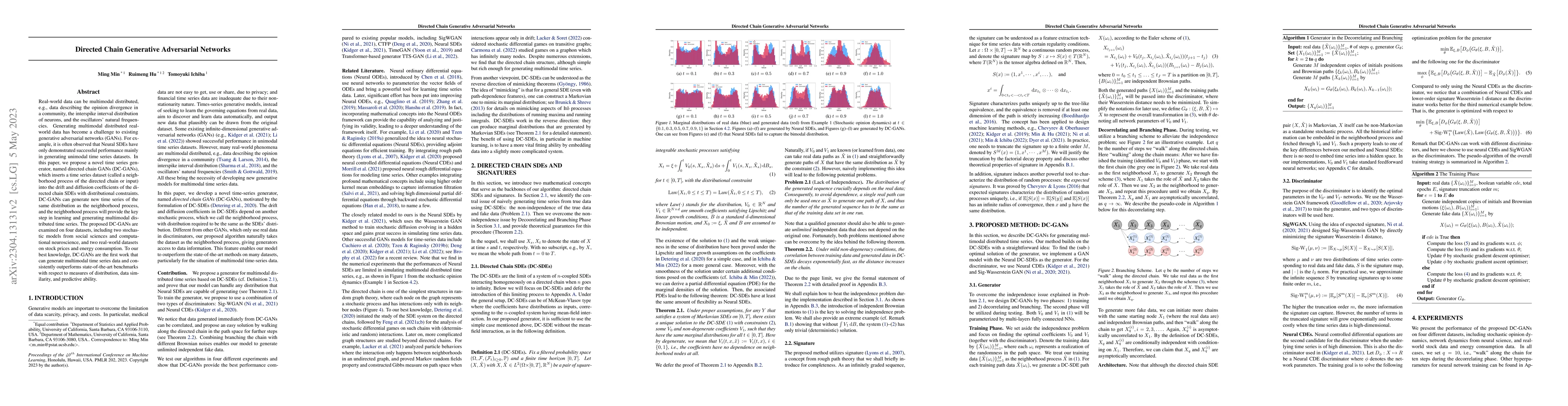

Real-world data can be multimodal distributed, e.g., data describing the opinion divergence in a community, the interspike interval distribution of neurons, and the oscillators natural frequencies. ...

We study the maximization of the logarithmic utility of an insider with different anticipating techniques. Our aim is to compare the usage of the forward and Skorokhod integrals in this context with...

We study the smoothness of the solution of the directed chain stochastic differential equations, where each process is affected by its neighborhood process in an infinite directed chain graph, intro...

We analyze the systemic risk for disjoint and overlapping groups (e.g., central clearing counterparties (CCP)) by proposing new models with realistic game features. Specifically, we generalize the s...

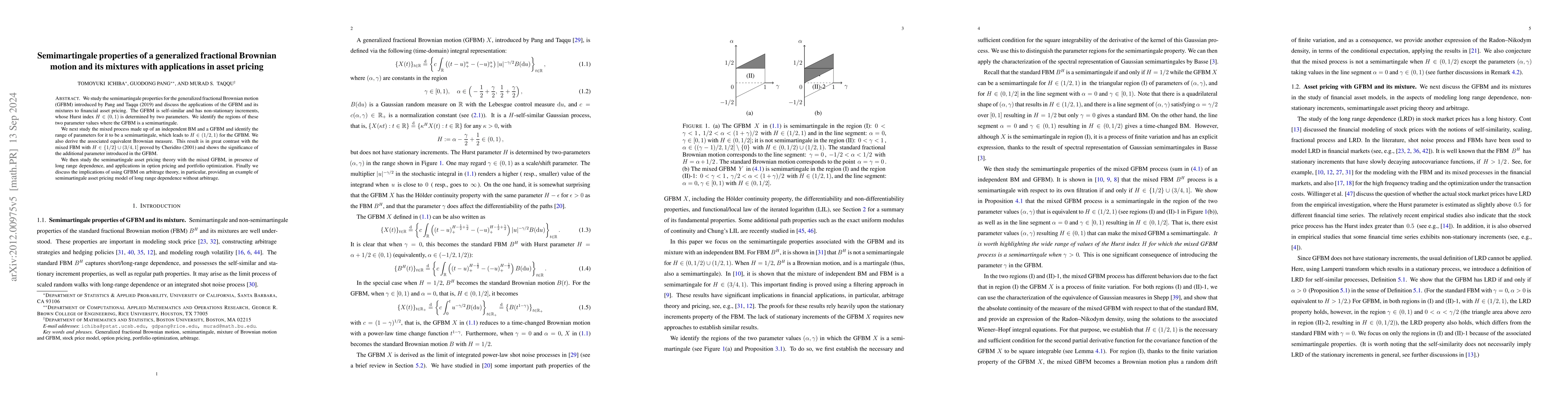

We study the semimartingale properties for the generalized fractional Brownian motion (GFBM) introduced by Pang and Taqqu (2019) and discuss the applications of the GFBM and its mixtures to financia...

The study of linear-quadratic stochastic differential games on directed networks was initiated in Feng, Fouque \& Ichiba \cite{fengFouqueIchiba2020linearquadratic}. In that work, the game on a direc...

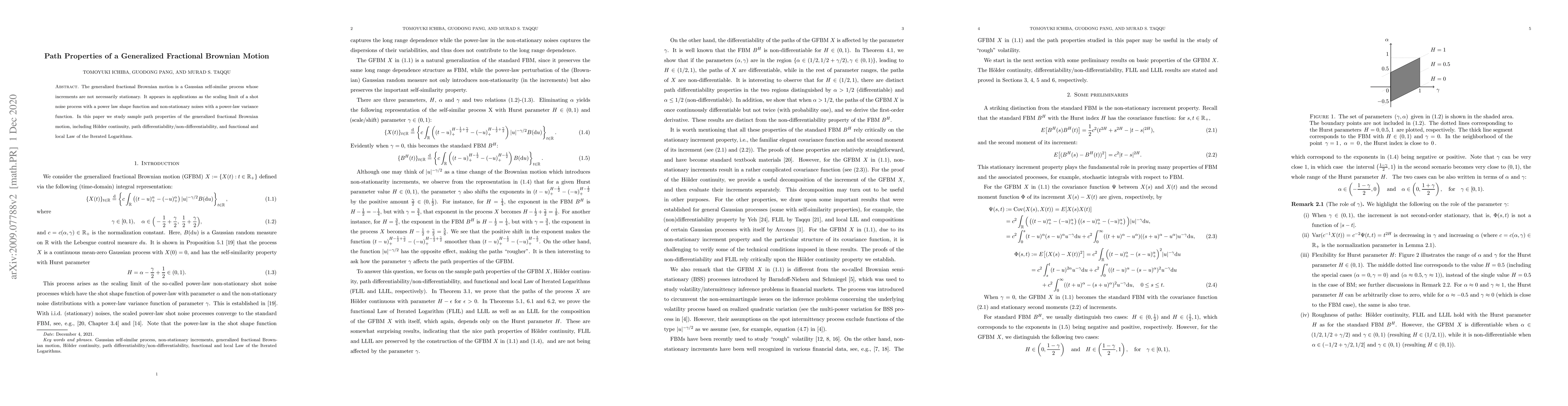

The generalized fractional Brownian motion is a Gaussian self-similar process whose increments are not necessarily stationary. It appears in applications as the scaling limit of a shot noise process...

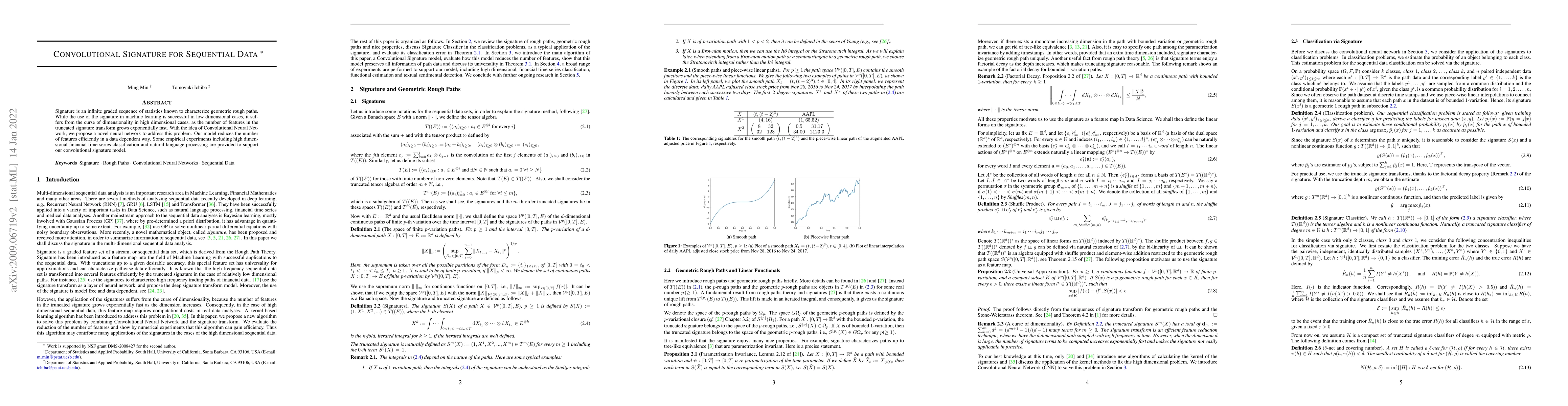

Signature is an infinite graded sequence of statistics known to characterize geometric rough paths, which includes the paths with bounded variation. This object has been studied successfully for mac...

We study systems of three interacting particles, in which drifts and variances are assigned by rank. These systems are "degenerate": the variances corresponding to one or two ranks can vanish, so th...

We consider a mean-field model for large banking systems, which takes into account default and recovery of the institutions. Building on models used for groups of interacting neurons, we first study...

We consider a dynamic model of interconnected banks. New banks can emerge, and existing banks can default, creating a birth-and-death setup. Microscopically, banks evolve as independent geometric Br...

We propose a particle system of diffusion processes coupled through a chain-like network structure described by an infinite-dimensional, nonlinear stochastic differential equation of McKean-Vlasov t...

The strong relative arbitrage problem in Stochastic Portfolio Theory seeks to generate an investment strategy that almost surely outperforms a benchmark portfolio at the end of a given time horizon. T...

This paper deals with bilateral-gamma (BG) approximation to functionals of an isonormal Gaussian process. We use Malliavin-Stein method to obtain the error bounds for the smooth Wasserstein distance. ...

In an earlier paper, a randomized load balancing model was studied in a heavy traffic asymptotic regime where the load balancing stream is thin compared to the total arrival stream. It was shown that ...

We analyze both finite and infinite systems of Riccati equations derived from stochastic differential games on infinite networks. We discuss a connection to the Catalan numbers and the convergence of ...

We consider a weighted sum of a series of independent Poisson random variables and show that it results in a new compound Poisson distribution which includes the Poisson distribution and Poisson distr...

We investigate the full dynamics of capital allocation and wealth distribution of heterogeneous agents in a frictional economy during booms and busts using tools from mean-field games. Two groups in o...

Built to generalise classical stochastic calculus, rough path theory provides a natural and pathwise framework to model continuous non-semimartingale assets. This paper investigates the ultimate capac...

We explicitly connect (discrete-time) quantum walks on Z with a four-state Markov additive process via a Feynman-type formula (2.5). Using this representation, we derive a relation between the spectra...