Academic Profile

Statistics

Similar Authors

Papers on arXiv

A continuous-time financial portfolio selection model with expected utility maximization typically boils down to solving a (static) convex stochastic optimization problem in terms of the terminal we...

A continuous-time Markowitz's mean-variance portfolio selection problem is studied in a market with one stock, one bond, and proportional transaction costs. This is a singular stochastic control pro...

We consider reinforcement learning for continuous-time Markov decision processes (MDPs) in the infinite-horizon, average-reward setting. In contrast to discrete-time MDPs, a continuous-time process mo...

We formulate an optimal stopping problem for a geometric Brownian motion where the probability scale is distorted by a general nonlinear function. The problem is inherently time inconsistent due to ...

We study Merton's expected utility maximization problem in an incomplete market, characterized by a factor process in addition to the stock price process, where all the model primitives are unknown....

We study a continuous-time expected utility maximization problem in which the investor at maturity receives the value of a contingent claim in addition to the investment payoff from the financial ma...

We study a multi-factor block model for variable clustering and connect it to the regularized subspace clustering by formulating a distributionally robust version of the nodewise regression. To solv...

We study a continuous-time Markowitz mean-variance portfolio selection model in which a naive agent, unaware of the underlying time-inconsistency, continuously reoptimizes over time. We define the r...

We study reinforcement learning for continuous-time Markov decision processes (MDPs) in the finite-horizon episodic setting. In contrast to discrete-time MDPs, the inter-transition times of a contin...

We propose \emph{Choquet regularizers} to measure and manage the level of exploration for reinforcement learning (RL), and reformulate the continuous-time entropy-regularized RL problem of Wang et a...

We define $g$-expectation of a distribution as the infimum of the $g$-expectations of all the terminal random variables sharing that distribution. We present two special cases for nonlinear $g$ wher...

We study the continuous-time counterpart of Q-learning for reinforcement learning (RL) under the entropy-regularized, exploratory diffusion process formulation introduced by Wang et al. (2020). As t...

We study policy gradient (PG) for reinforcement learning in continuous time and space under the regularized exploratory formulation developed by Wang et al. (2020). We represent the gradient of the ...

We study the exploratory Hamilton--Jacobi--Bellman (HJB) equation arising from the entropy-regularized exploratory control problem, which was formulated by Wang, Zariphopoulou and Zhou (J. Mach. Lea...

We propose a unified framework to study policy evaluation (PE) and the associated temporal difference (TD) methods for reinforcement learning in continuous time and space. We show that PE is equival...

Time inconsistency is prevalent in dynamic choice problems: a plan of actions to be taken in the future that is optimal for an agent today may not be optimal for the same agent in the future. If the...

We aim to cluster financial assets in order to identify a small set of stocks to approximate the level of diversification of the whole universe of stocks. We develop a data-driven approach to cluste...

We develop an approach to solve Barberis (2012)'s casino gambling model in which a gambler whose preferences are specified by the cumulative prospect theory (CPT) must decide when to stop gambling b...

We study the temperature control problem for Langevin diffusions in the context of non-convex optimization. The classical optimal control of such a problem is of the bang-bang type, which is overly ...

We study the design of an optimal insurance contract in which the insured maximizes her expected utility and the insurer limits the variance of his risk exposure while maintaining the principle of i...

We study portfolio selection in a complete continuous-time market where the preference is dictated by the rank-dependent utility. As such a model is inherently time inconsistent due to the underlyin...

We study reinforcement learning (RL) for a class of continuous-time linear-quadratic (LQ) control problems for diffusions where volatility of the state processes depends on both state and control vari...

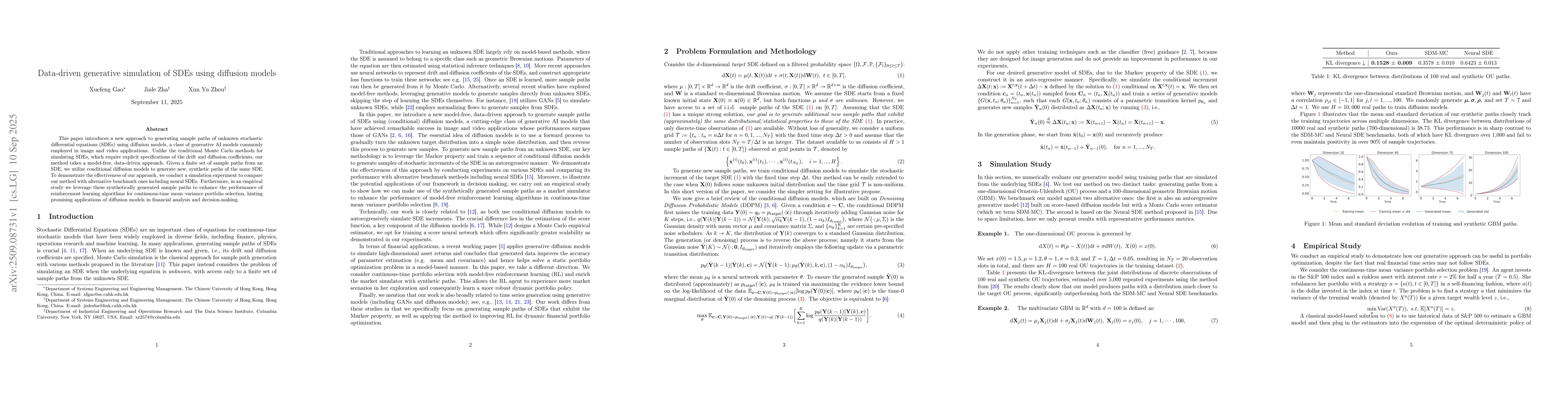

We propose a new reinforcement learning (RL) formulation for training continuous-time score-based diffusion models for generative AI to generate samples that maximize reward functions while keeping th...

We study the convergence of $q$-learning and related algorithms introduced by Jia and Zhou (J. Mach. Learn. Res., 24 (2023), 161) for controlled diffusion processes. Under suitable conditions on the g...

We study optimal stopping for diffusion processes with unknown model primitives within the continuous-time reinforcement learning (RL) framework developed by Wang et al. (2020), and present applicatio...

We study a model of a corporation which has the possibility to choose various production/business policies with different expected profits and risks. In the model there are restrictions on the dividen...

We study continuous-time mean--variance portfolio selection in markets where stock prices are diffusion processes driven by observable factors that are also diffusion processes yet the coefficients of...

We study reinforcement learning (RL) for the same class of continuous-time stochastic linear--quadratic (LQ) control problems as in \cite{huang2024sublinear}, where volatilities depend on both states ...

This paper introduces a new approach to generating sample paths of unknown stochastic differential equations (SDEs) using diffusion models, a class of generative AI models commonly employed in image a...

The classical Merton investment problem predicts deterministic, state-dependent portfolio rules; however, laboratory and field evidence suggests that individuals often prefer randomized decisions lead...

This paper is a continuation work of Ren et al. (2026) aiming to further devise q-learning algorithms for mean-field control (MFC) with controlled common noise. Based on the relaxed control formulatio...

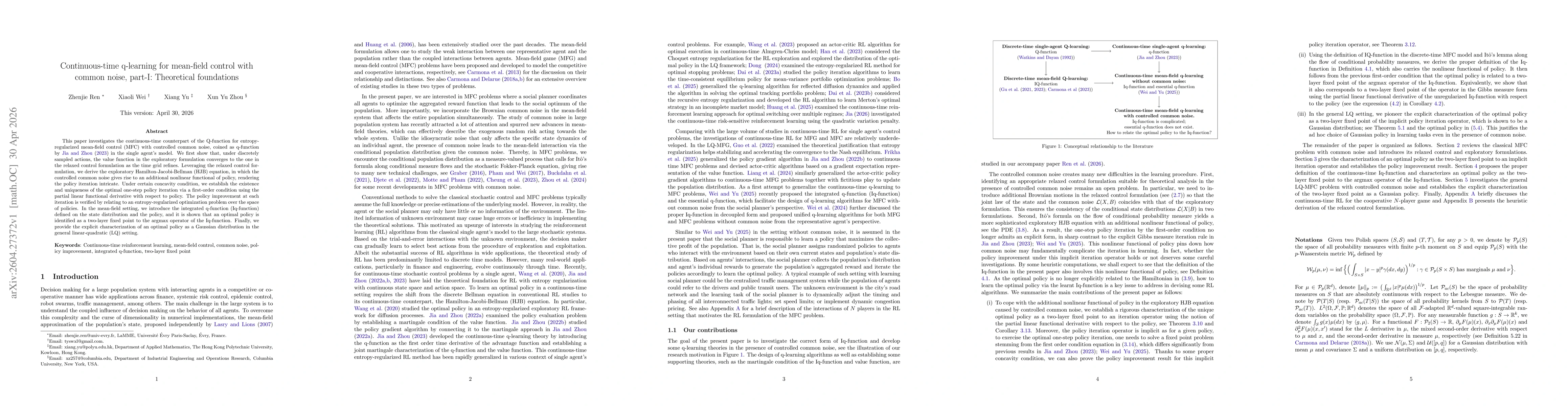

This paper investigates the continuous-time counterpart of the Q-function for entropy-regularized mean-field control (MFC) with controlled common noise, coined as q-function by Jia and Zhou (2023) in ...

We study image inpainting with generative diffusion models. Existing methods typically either train dedicated task-specific models, or adapt a pretrained diffusion model separately for each masked ima...

Diffusion models have achieved remarkable success in generating samples from unknown data distributions. Most popular stochastic differential equation-based diffusion models perturb the target distrib...

In this paper we study optimal exit strategies of gamblers with cumulative prospect theory (CPT) preferences in games where the expected payoff is strictly negative at each play, and formulate the pro...

High-dimensional partial differential equations (PDEs) with unknown coefficients arise widely in scientific machine learning, including continuous-time reinforcement learning, yet solving them efficie...

We study timestep allocation for score-based diffusion sampling, where a learned reverse-time dynamics is discretized on a finite grid. Uniform and hand-crafted schedules are standard choices, but the...