The Quarter-Hour Effect: Periodic Algorithmic Trading and Return Predictability in Cryptocurrency Futures

Publication

Metrics

Paper Preview

Abstract

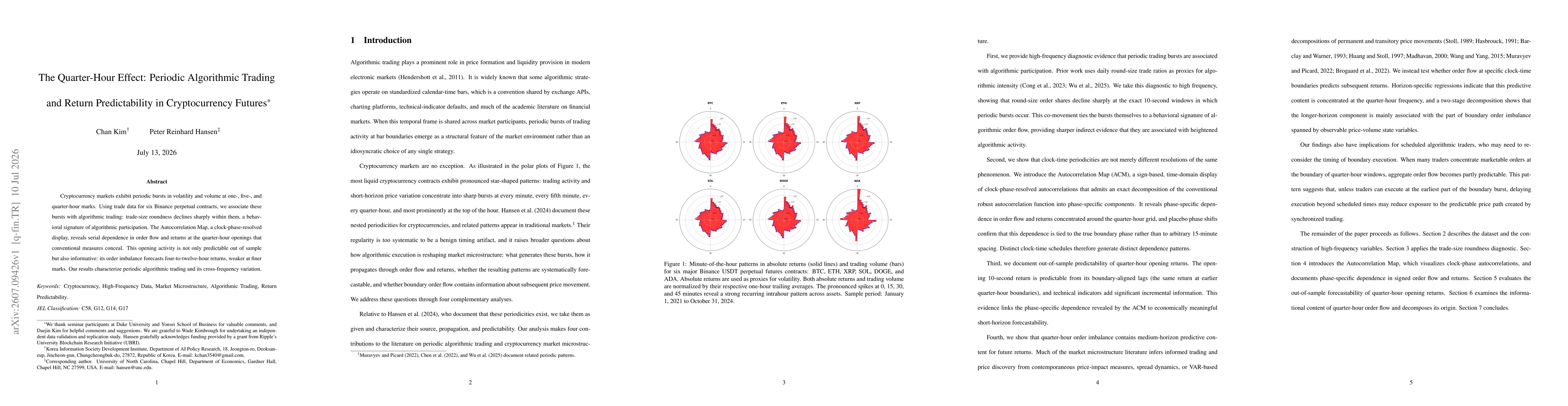

Cryptocurrency markets exhibit periodic bursts in volatility and volume at one-, five-, and quarter-hour marks. Using trade data for six Binance perpetual contracts, we associate these bursts with algorithmic trading: trade-size roundness declines sharply within them, a behavioral signature of algorithmic participation. The Autocorrelation Map, a clock-phase-resolved display, reveals serial dependence in order flow and returns at the quarter-hour openings that conventional measures conceal. This opening activity is not only predictable out of sample but also informative: its order imbalance forecasts four-to-twelve-hour returns, weaker at finer marks. Our results characterize periodic algorithmic trading and its cross-frequency variation.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0