Academic Profile

Statistics

Similar Authors

Papers on arXiv

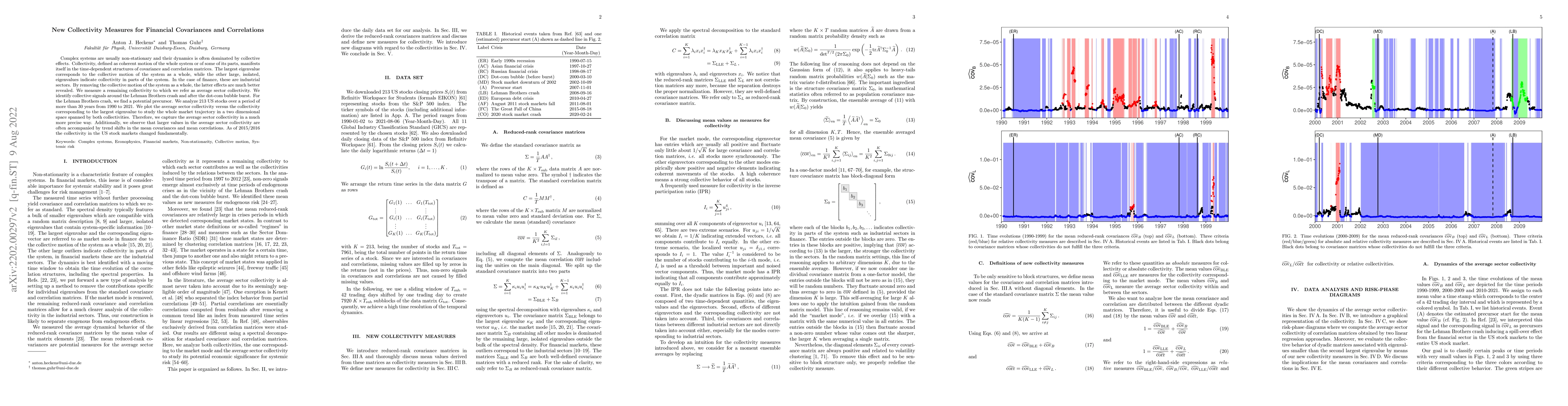

Complex systems are usually non-stationary and their dynamics is often dominated by collective effects. Collectivity, defined as coherent motion of the whole system or of some of its parts, manifest...

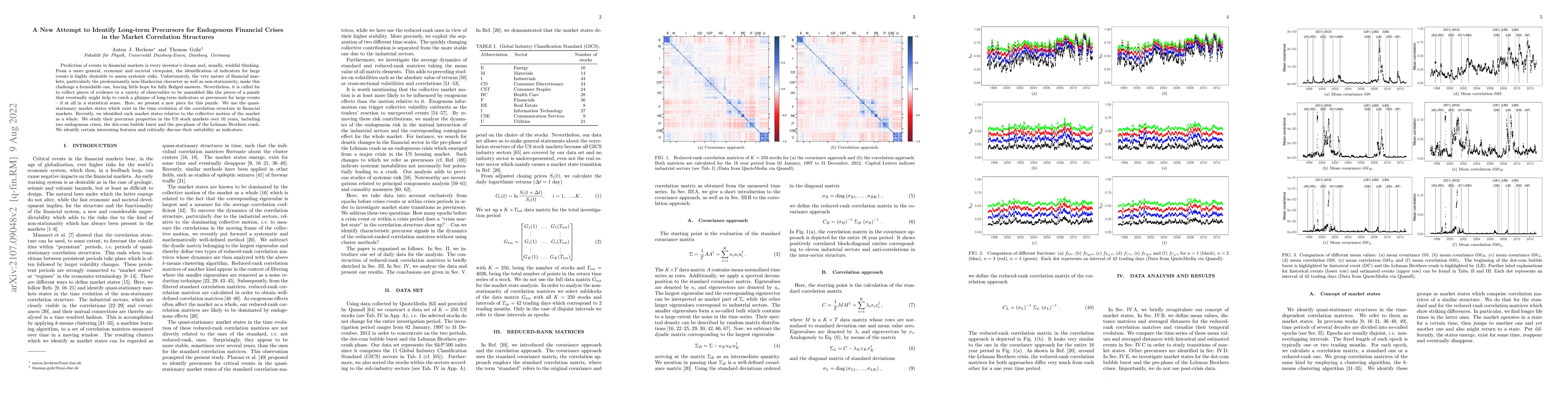

Prediction of events in financial markets is every investor's dream and, usually, wishful thinking. From a more general, economic and societal viewpoint, the identification of indicators for large e...

Multivariate Distributions are needed to capture the correlation structure of complex systems. In previous works, we developed a Random Matrix Model for such correlated multivariate joint probability ...

Risk assessment for rare events is essential for understanding systemic stability in complex systems. As rare events are typically highly correlated, it is important to study heavy-tailed multivariate...

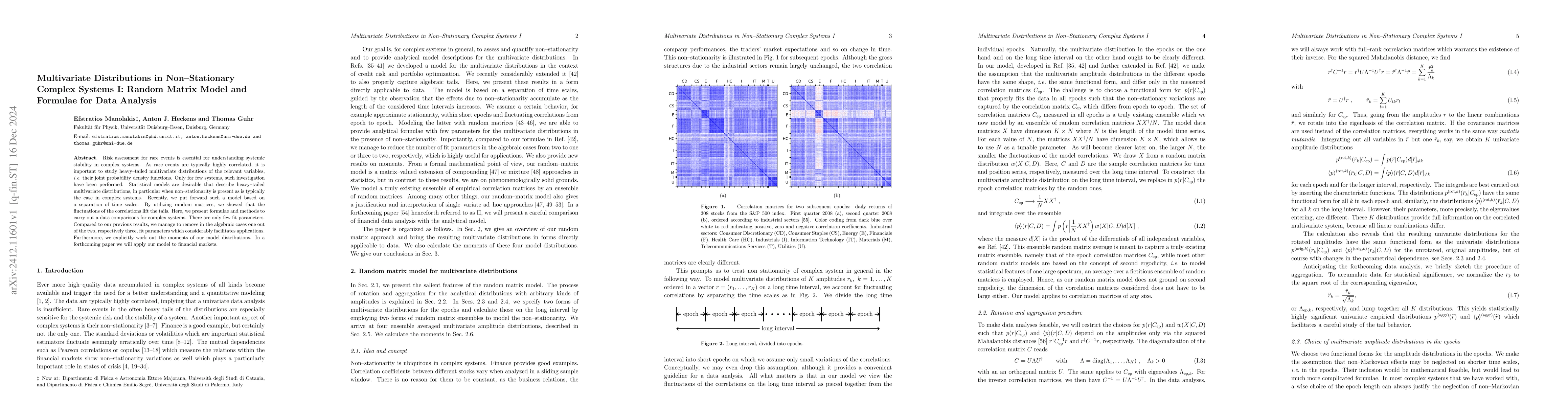

Traders on financial markets generate non-Markovian effects in various ways, particularly through their competition with one another which can be interpreted as a game between different (types of) tra...

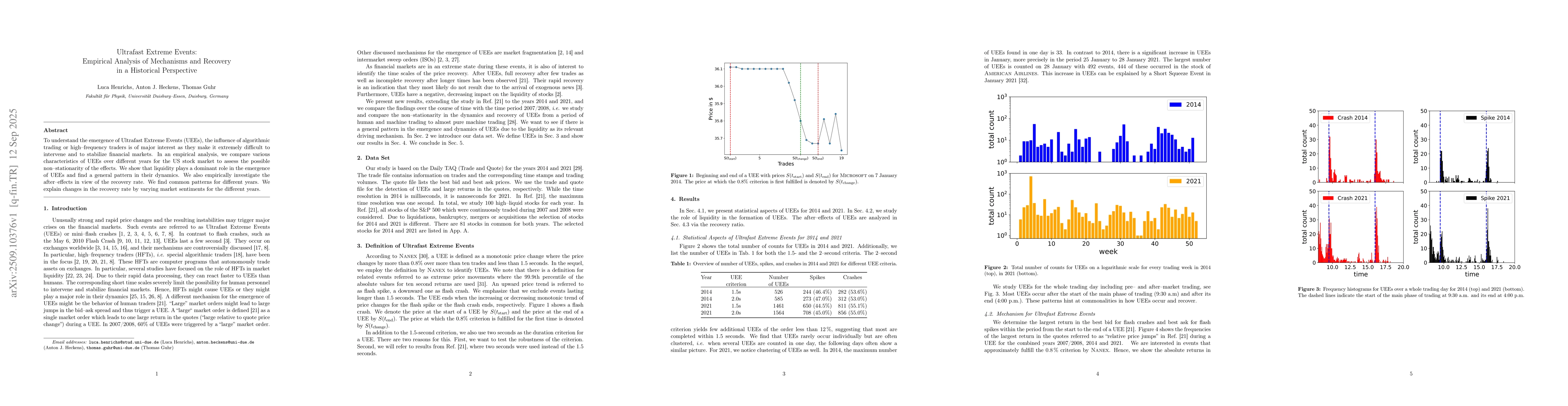

To understand the emergence of Ultrafast Extreme Events (UEEs), the influence of algorithmic trading or high-frequency traders is of major interest as they make it extremely difficult to intervene and...

Extreme values and the tail behavior of probability distributions are essential for quantifying and mitigating risk in complex systems of all kinds. In multivariate settings, accounting for correlatio...