Academic Profile

Statistics

Similar Authors

Papers on arXiv

We introduce GECKO, a bilingual large language model (LLM) optimized for Korean and English, along with programming languages. GECKO is pretrained on the balanced, high-quality corpus of Korean and ...

In this paper, we introduce a novel method for predicting intraday instantaneous volatility based on Ito semimartingale models using high-frequency financial data. Several studies have highlighted s...

Baker and Bowler (2019) showed that the Grassmannian can be defined over a tract, a ring-like structure generalizing both partial fields and hyperfields. This notion unifies theories for matroids ov...

In the evolving landscape of federated learning (FL), addressing label noise presents unique challenges due to the decentralized and diverse nature of data collection across clients. Traditional cen...

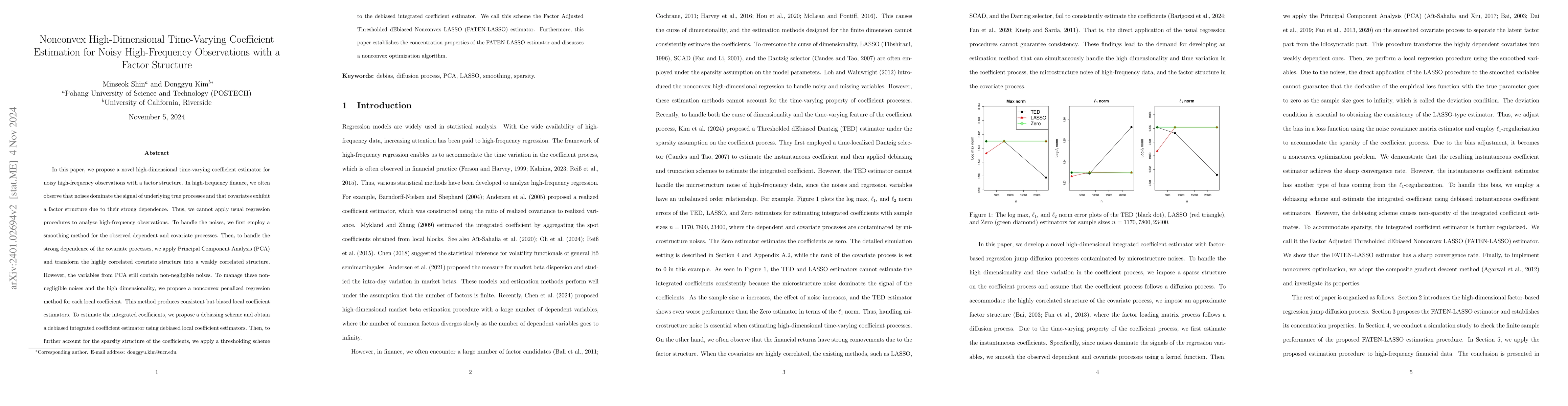

In this paper, we propose a novel high-dimensional time-varying coefficient estimator for noisy high-frequency observations. In high-frequency finance, we often observe that noises dominate a signal...

As social and socially assistive robots are becoming more prevalent in our society, it is beneficial to understand how people form first impressions of them and eventually come to trust and accept t...

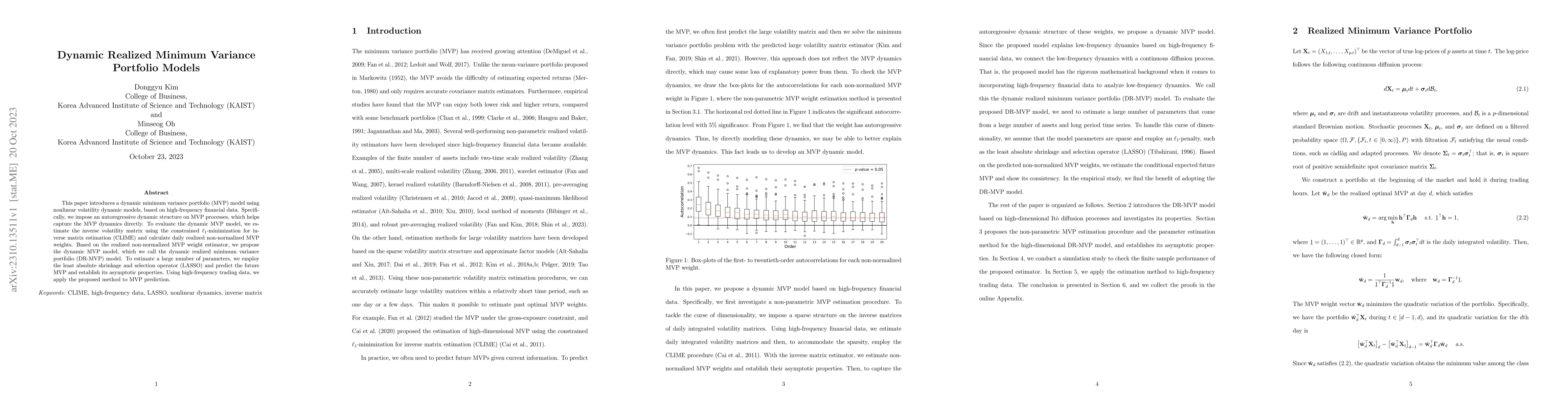

This paper introduces a dynamic minimum variance portfolio (MVP) model using nonlinear volatility dynamic models, based on high-frequency financial data. Specifically, we impose an autoregressive dy...

We show that the basis graph of an even delta-matroid is Hamiltonian if it has more than two vertices. More strongly, we prove that for two distinct edges $e$ and $f$ sharing a common end, it has a ...

Preparation of a target quantum many-body state on quantum simulators is one of the significant steps in quantum science and technology. With a small number of qubits, a few quantum states, such as ...

In this paper, we develop a novel large volatility matrix estimation procedure for analyzing global financial markets. Practitioners often use lower-frequency data, such as weekly or monthly returns...

We generalize Baker-Bowler's theory of matroids over tracts to orthogonal matroids, define orthogonal matroids with coefficients in tracts in terms of Wick functions, orthogonal signatures, circuit ...

In this paper, we develop a novel high-dimensional coefficient estimation procedure based on high-frequency data. Unlike usual high-dimensional regression procedure such as LASSO, we additionally ha...

In this paper, we develop a robust non-parametric realized integrated beta estimator using high-frequency financial data contaminated by microstructure noises, which is robust to the stylized featur...

We investigate the twin-width of the Erd\H{o}s-R\'enyi random graph $G(n,p)$. We unveil a surprising behavior of this parameter by showing the existence of a constant $p^*\approx 0.4$ such that with...

Several large volatility matrix inference procedures have been developed, based on the latent factor model. They often assumed that there are a few of common factors, which can account for volatilit...

Precipitation forecasting is an important scientific challenge that has wide-reaching impacts on society. Historically, this challenge has been tackled using numerical weather prediction (NWP) model...

This paper introduces novel volatility diffusion models to account for the stylized facts of high-frequency financial data such as volatility clustering, intra-day U-shape, and leverage effect. For ...

This paper introduces a unified parametric modeling approach for time-varying market betas that can accommodate continuous-time diffusion and discrete-time series models based on a continuous-time s...

In this paper, we develop a novel high-dimensional time-varying coefficient estimation method, based on high-dimensional Ito diffusion processes. To account for high-dimensional time-varying coeffic...

A graph is prime if it does not admit a partition $(A,B)$ of its vertex set such that $\min\{|A|,|B|\} \geq 2$ and the rank of the $A\times B$ submatrix of its adjacency matrix is at most $1$. A ver...

Let $G$ be a graph and let $g, f$ be nonnegative integer-valued functions defined on $V(G)$ such that $g(v) \le f(v)$ and $g(v) \equiv f(v) \pmod{2}$ for all $v \in V(G)$. A $(g,f)$-parity factor of...

In this paper, we investigate the effect of the U.S.--China trade war on stock markets from a financial contagion perspective, based on high-frequency financial data. Specifically, to account for ri...

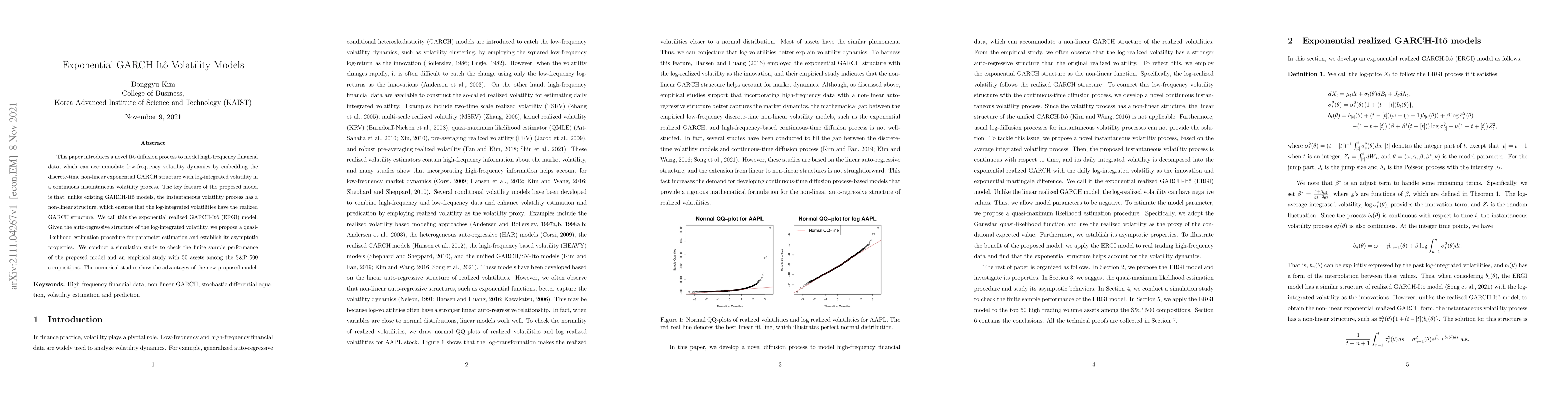

This paper introduces a novel Ito diffusion process to model high-frequency financial data, which can accommodate low-frequency volatility dynamics by embedding the discrete-time non-linear exponent...

Bonnet, Kim, Thomass\'{e}, and Watrigant (2020) introduced the twin-width of a graph. We show that the twin-width of an $n$-vertex graph is less than $(n+\sqrt{n\ln n}+\sqrt{n}+2\ln n)/2$, and the t...

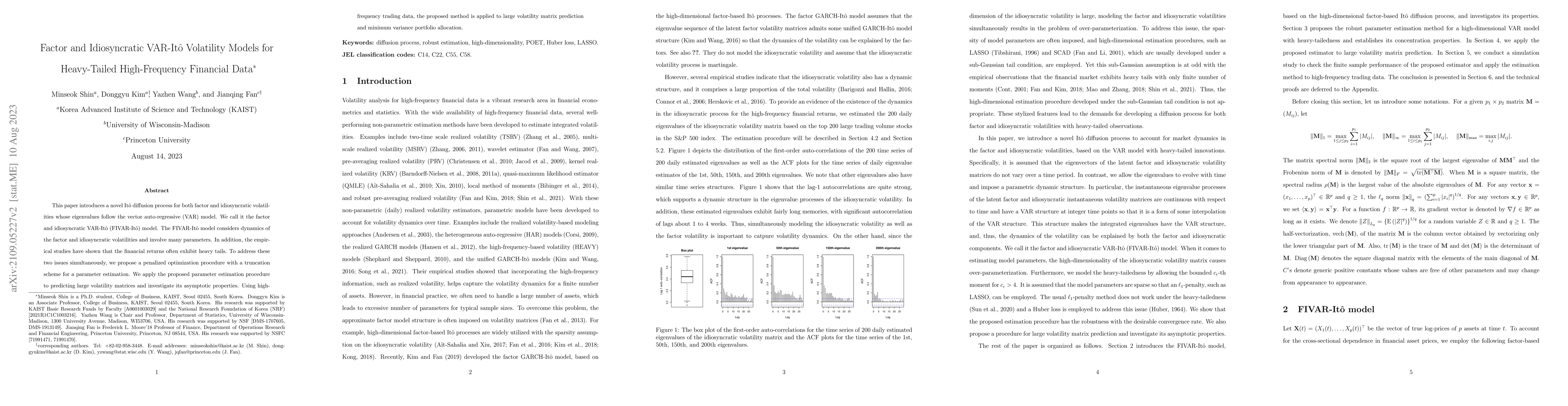

This paper introduces a novel It\^{o} diffusion process for both factor and idiosyncratic volatilities whose eigenvalues follow the vector auto-regressive (VAR) model. We call it the factor and idio...

This paper introduces a novel quantile approach to harness the high-frequency information and improve the daily conditional quantile estimation. Specifically, we model the conditional standard devia...

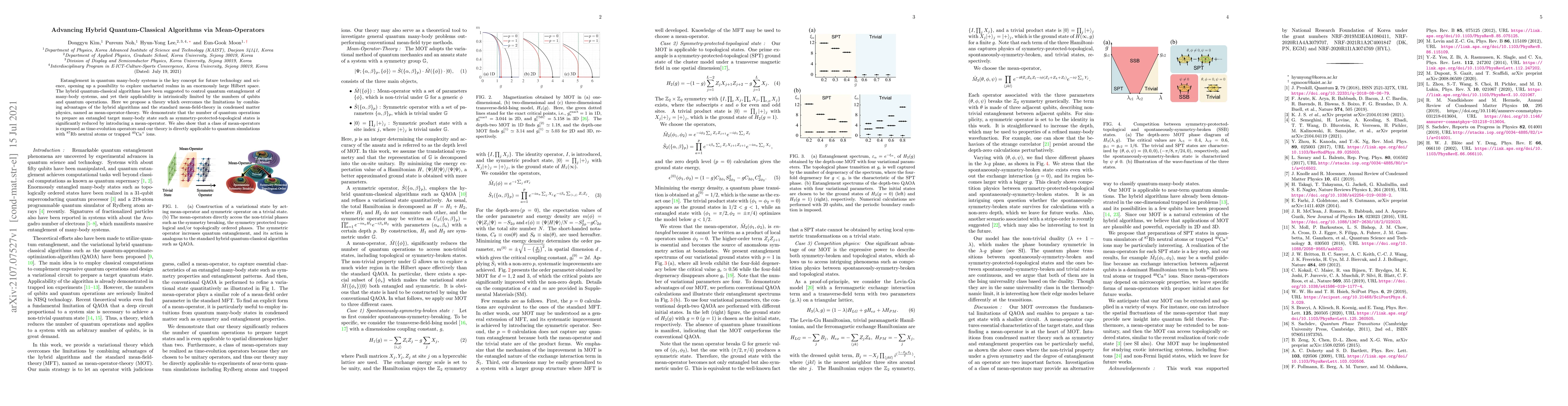

Entanglement in quantum many-body systems is the key concept for future technology and science, opening up a possibility to explore uncharted realms in an enormously large Hilbert space. The hybrid ...

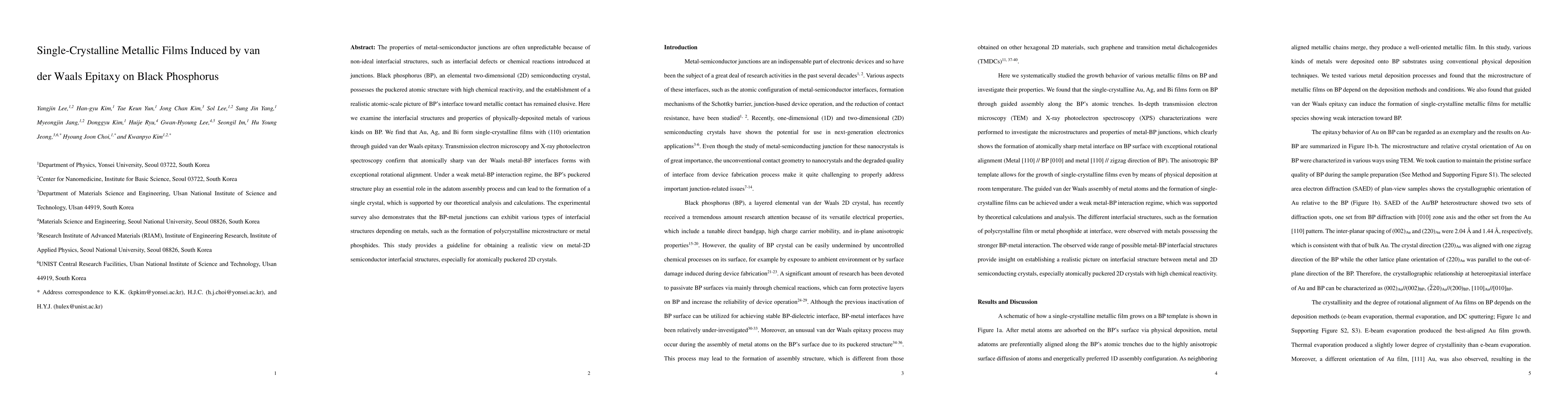

The properties of metal-semiconductor junctions are often unpredictable because of non-ideal interfacial structures, such as interfacial defects or chemical reactions introduced at junctions. Black ...

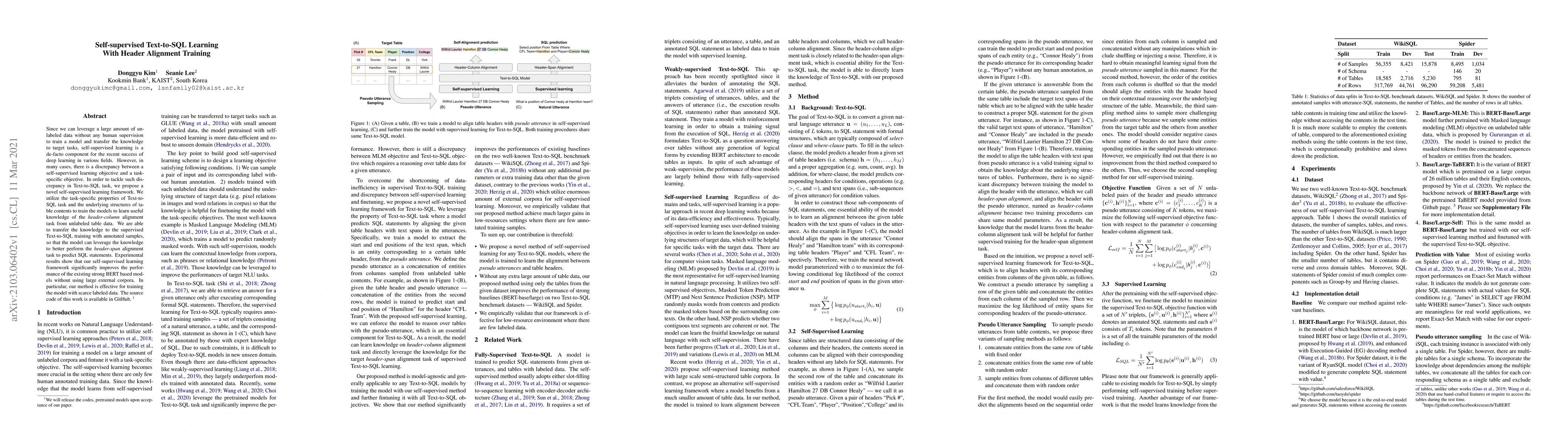

Since we can leverage a large amount of unlabeled data without any human supervision to train a model and transfer the knowledge to target tasks, self-supervised learning is a de-facto component for...

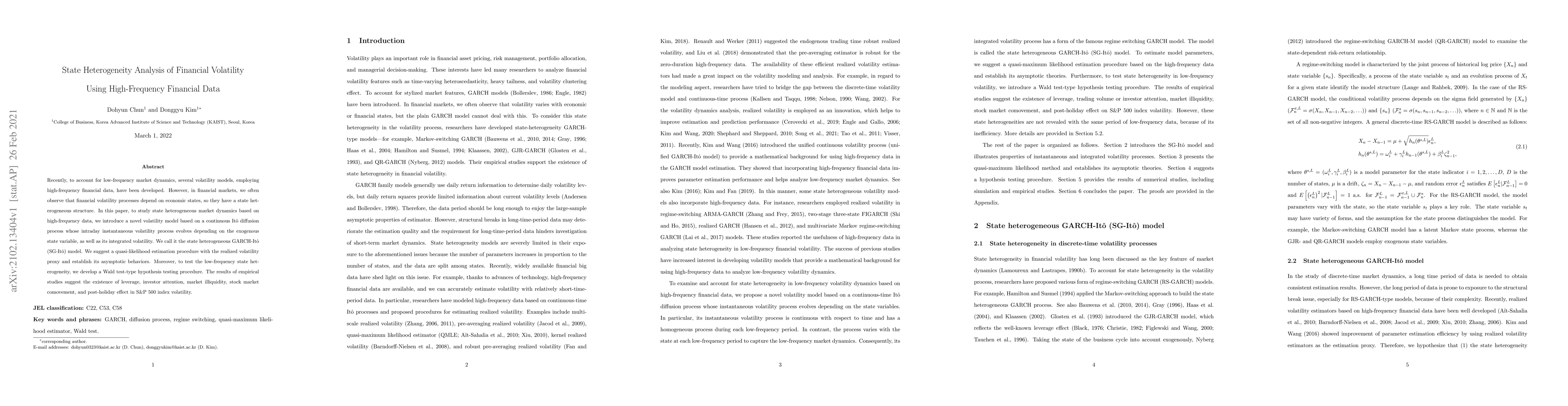

Recently, to account for low-frequency market dynamics, several volatility models, employing high-frequency financial data, have been developed. However, in financial markets, we often observe that ...

This paper proposes a dynamic process of portfolio risk measurement to address potential information loss. The proposed model takes advantage of financial big data to incorporate out-of-target-portf...

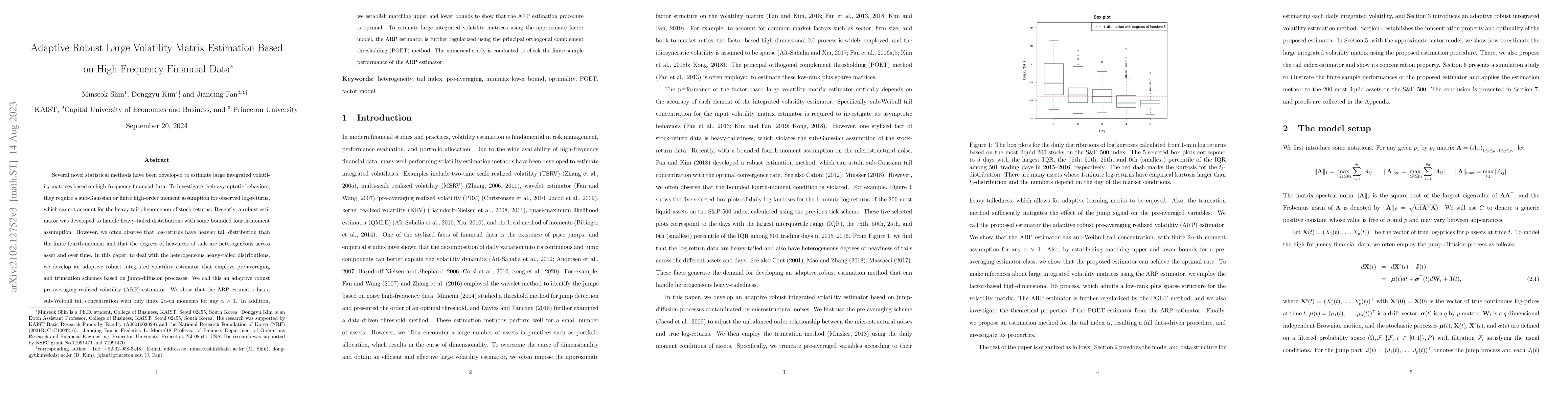

Several novel statistical methods have been developed to estimate large integrated volatility matrices based on high-frequency financial data. To investigate their asymptotic behaviors, they require...

Quantum computers use quantum resources to carry out computational tasks and may outperform classical computers in solving certain computational problems. Special-purpose quantum computers such as q...

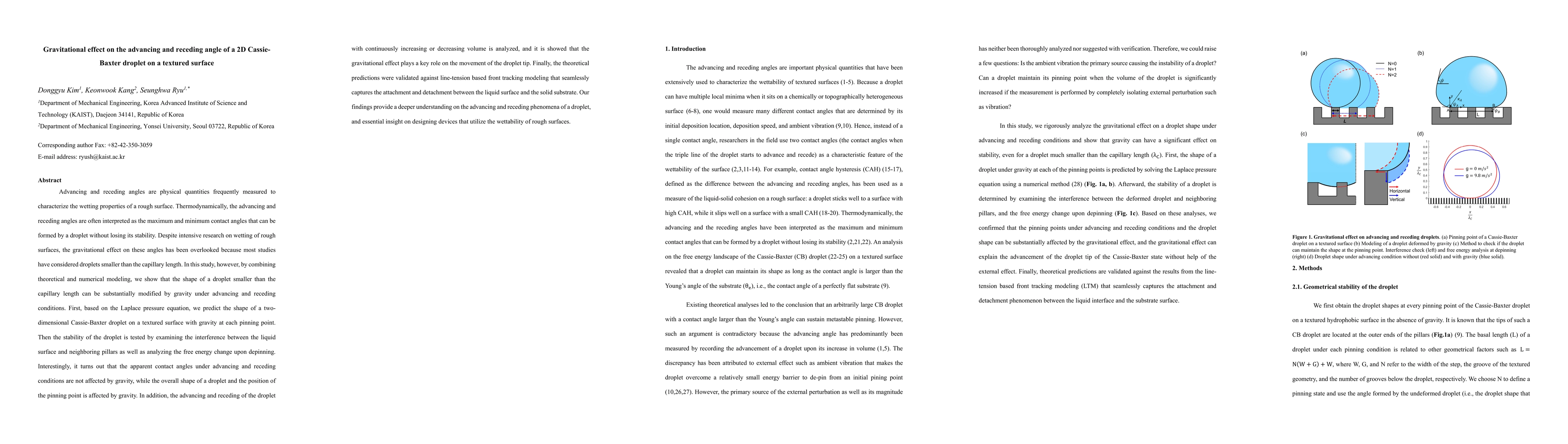

The Cassie-Baxter state droplet has many local energy minima on the textured surface, while the amount of the energy barrier between them can be affected by the gravity. When the droplet cannot find...

This paper introduces unified models for high-dimensional factor-based Ito process, which can accommodate both continuous-time Ito diffusion and discrete-time stochastic volatility (SV) models by em...

Advancing and receding angles are physical quantities frequently measured to characterize the wetting properties of a rough surface. Thermodynamically, the advancing and receding angles are often in...

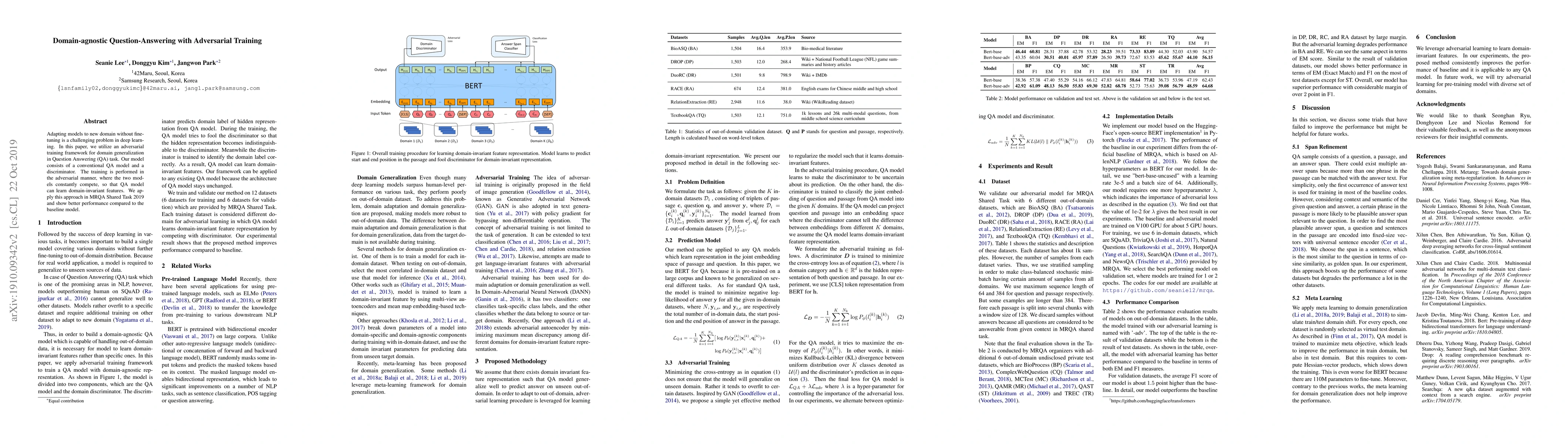

Adapting models to new domain without finetuning is a challenging problem in deep learning. In this paper, we utilize an adversarial training framework for domain generalization in Question Answerin...

This paper introduces a unified approach for modeling high-frequency financial data that can accommodate both the continuous-time jump-diffusion and discrete-time realized GARCH model by embedding t...

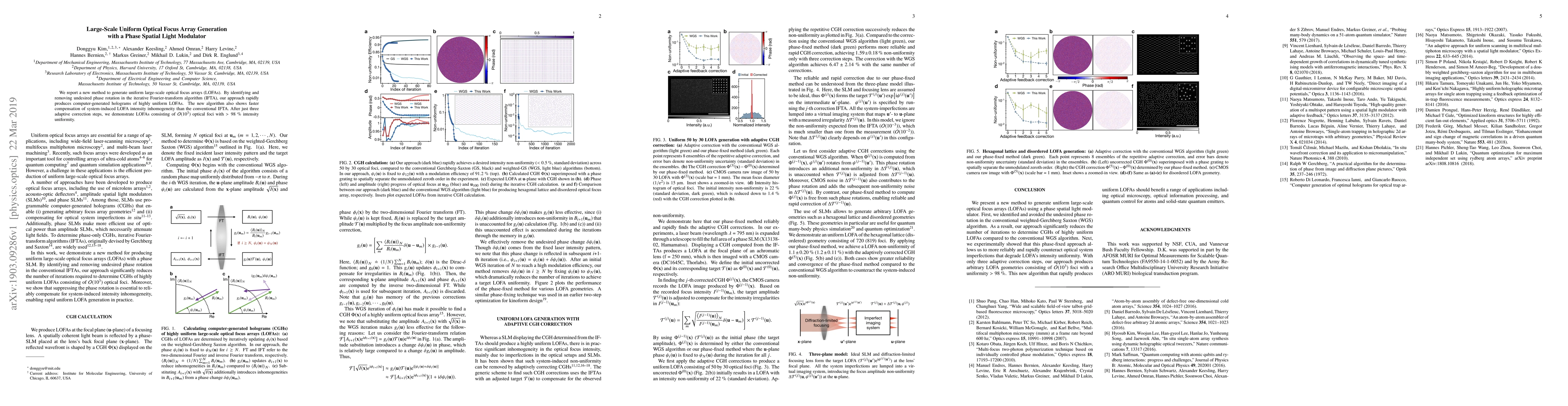

We report a new method to generate uniform large-scale optical focus arrays (LOFAs). By identifying and removing undesired phase rotation in the iterative Fourier-transform algorithm (IFTA), our app...

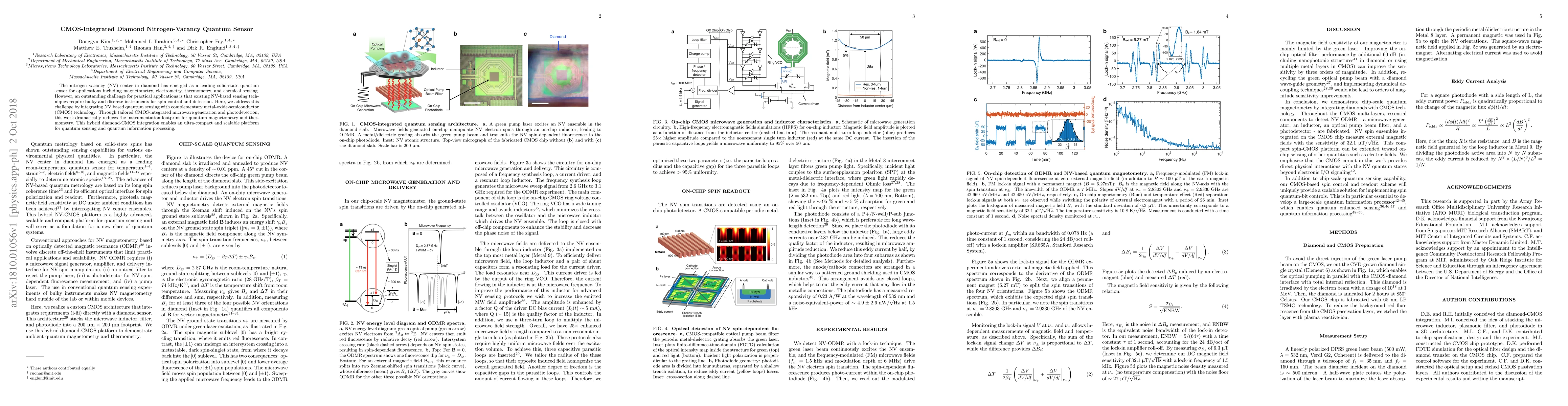

The nitrogen vacancy (NV) center in diamond has emerged as a leading solid-state quantum sensor for applications including magnetometry, electrometry, thermometry, and chemical sensing. However, an ...

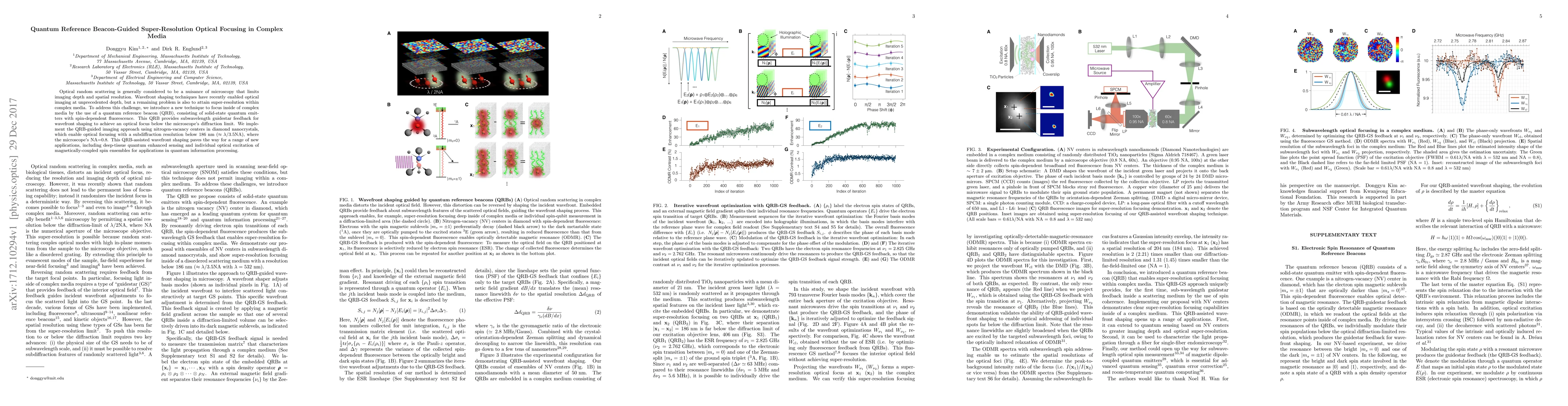

Optical random scattering is generally considered to be a nuisance of microscopy that limits imaging depth and spatial resolution. Wavefront shaping techniques have recently enabled optical imaging ...

Reinforcement Learning (RL) has proven effective in solving complex decision-making tasks across various domains, but challenges remain in continuous-time settings, particularly when state dynamics ar...

In financial applications, we often observe both global and local factors that are modeled by a multi-level factor model. When detecting unknown local group memberships under such a model, employing a...

In this paper, we develop a novel method for predicting future large volatility matrices based on high-dimensional factor-based It\^o processes. Several studies have proposed volatility matrix predict...

Previous work of Chan--Church--Grochow and Baker--Wang shows that the set of spanning trees in a plane graph $G$ is naturally a torsor for the Jacobian group of $G$. Informally, this means that the se...

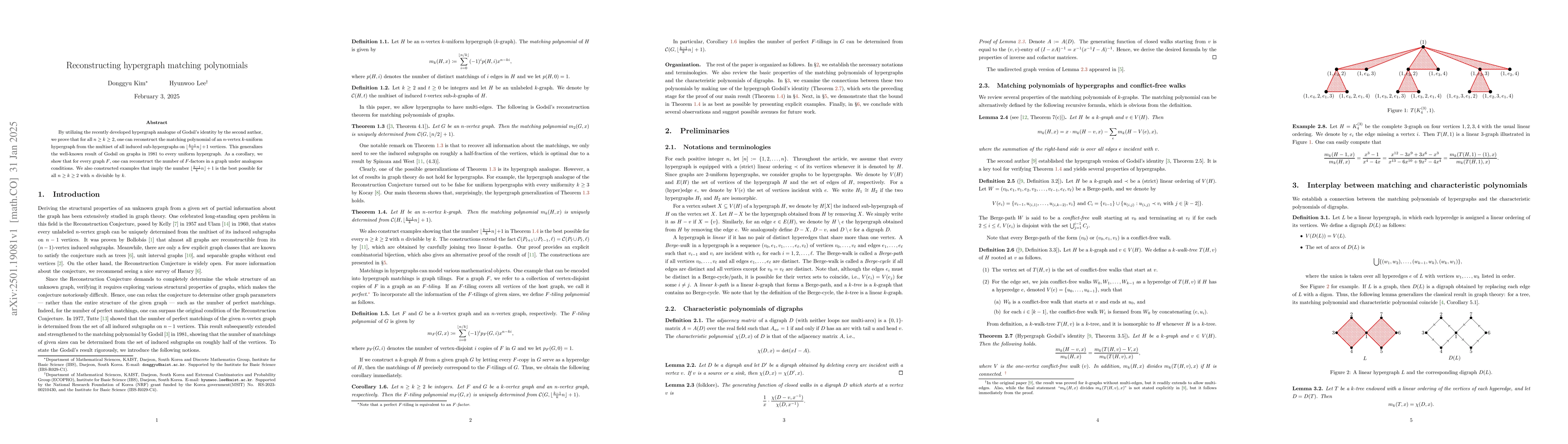

By utilizing the recently developed hypergraph analogue of Godsil's identity by the second author, we prove that for all $n \geq k \geq 2$, one can reconstruct the matching polynomial of an $n$-vertex...

Based on It\^o semimartingale models, several studies have proposed methods for forecasting intraday volatility using high-frequency financial data. These approaches typically rely on restrictive para...

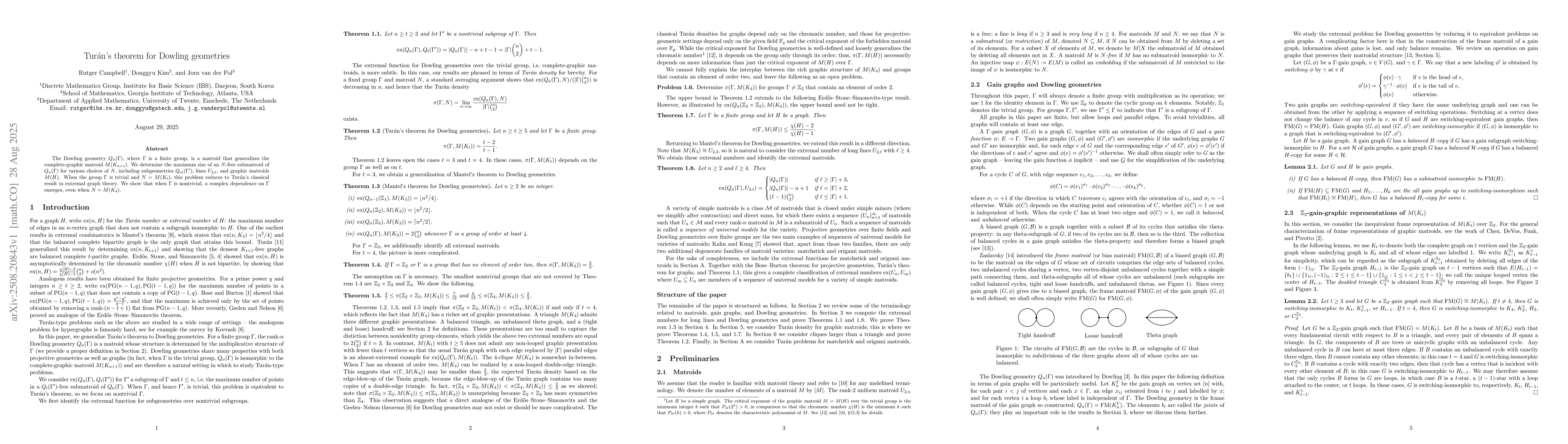

The Dowling geometry $Q_n(\Gamma)$, where $\Gamma$ is a finite group, is a matroid that generalizes the complete-graphic matroid $M(K_{n+1})$. We determine the maximum size of an $N$-free submatroid o...

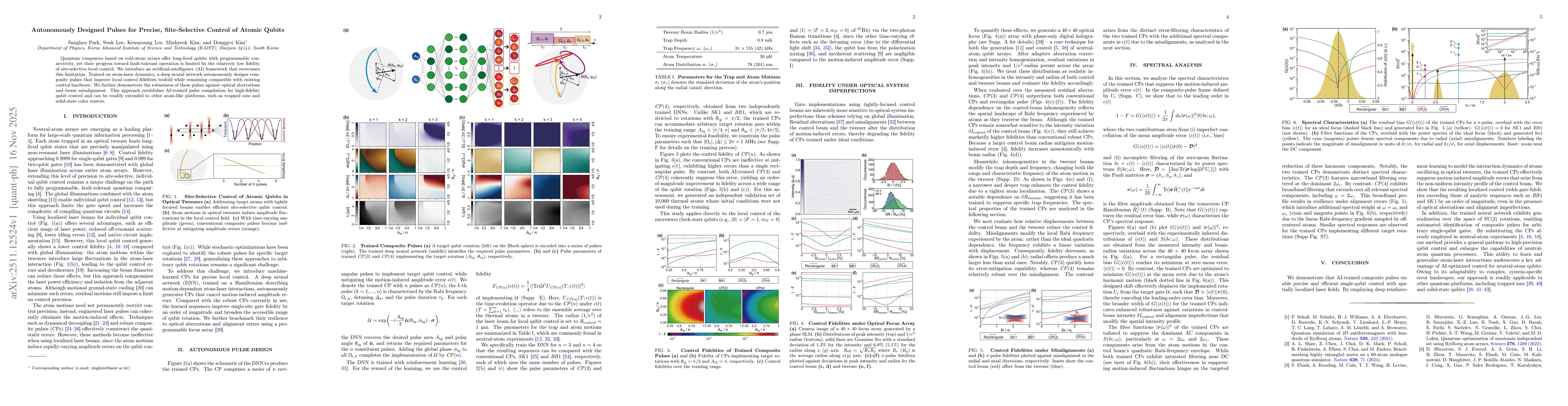

Quantum computers based on cold-atom arrays offer long-lived qubits with programmable connectivity, yet their progress toward fault-tolerant operation is limited by the relatively low fidelity of site...

Finite drive power leaves unavoidable spatial gradients in control fields, preventing spin ensembles from reaching the standard-quantum-limit sensitivity. We derive an analytic expression of ensemble ...

We present a new cryptomorphic definition of orthogonal matroids with coefficients using Grassmann--Plücker functions. The equivalence is motivated by Cayley's identities expressing principal and almo...

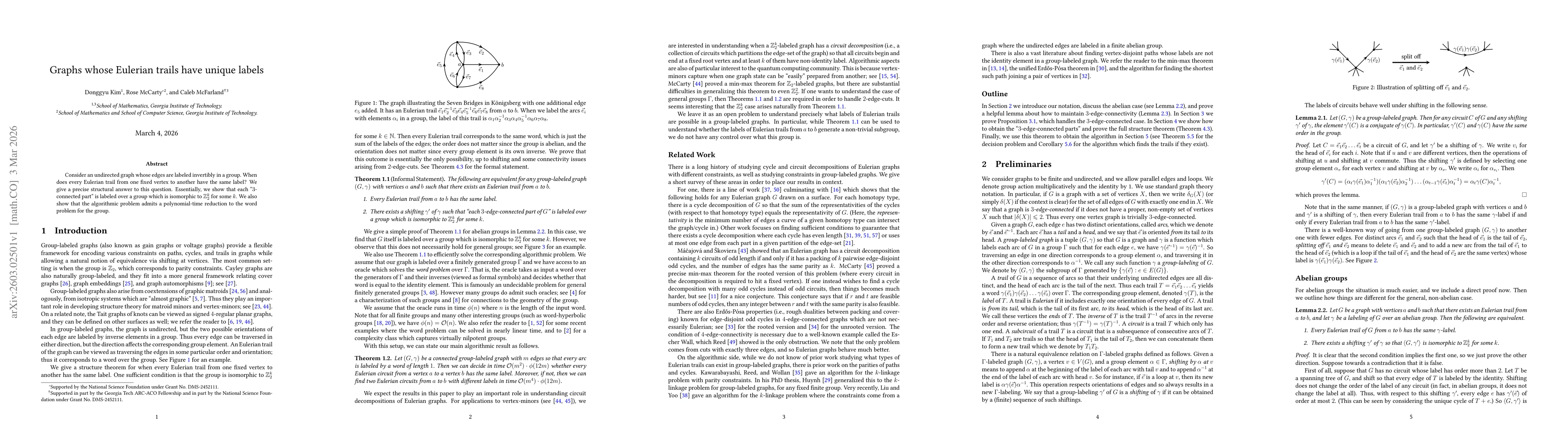

Consider an undirected graph whose edges are labeled invertibly in a group. When does every Eulerian trail from one fixed vertex to another have the same label? We give a precise structural answer to ...

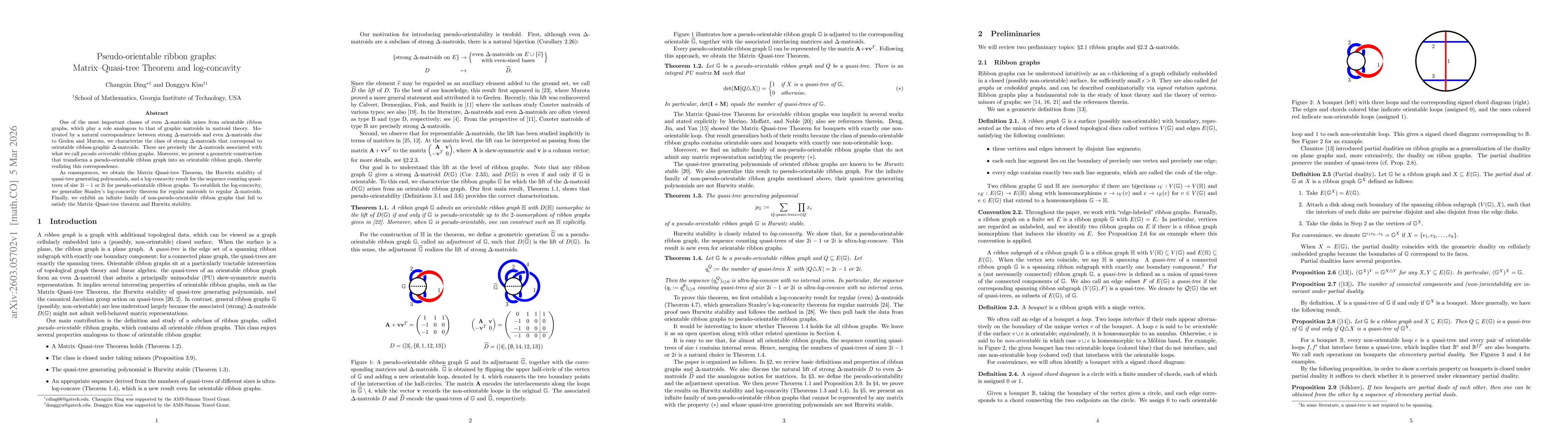

One of the most important classes of even $Δ$-matroids arises from orientable ribbon graphs, which play a role analogous to that of graphic matroids in matroid theory. Motivated by a natural correspon...