Academic Profile

Statistics

Similar Authors

Papers on arXiv

Over the past 60 years, there has been a gradual increase in the volatility of daily returns for the S&P 500 Index. Hypothetically, suppose that market forces determine daily volatility such that a ...

Consider a closed pooled annuity fund investing in n assets with discrete-time rebalancing. At time 0, each annuitant makes an initial contribution to the fund, committing to a predetermined schedul...

For $n$ assets and discrete-time rebalancing, the probability to complete a given schedule of investments and withdrawals is maximized over progressively measurable portfolio weight functions. Appli...

Daily leveraged exchange traded funds amplify gains and losses of their underlying benchmark indexes on a daily basis. The result of going long in a daily leveraged ETF for more than one day is less...

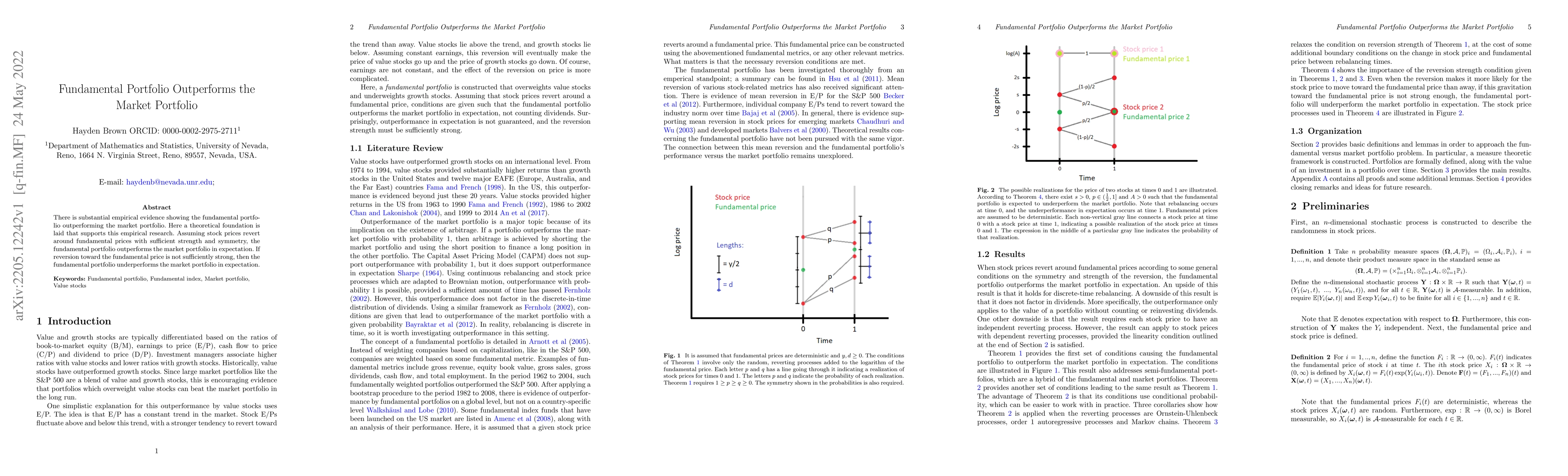

There is substantial empirical evidence showing the fundamental portfolio outperforming the market portfolio. Here a theoretical foundation is laid that supports this empirical research. Assuming st...

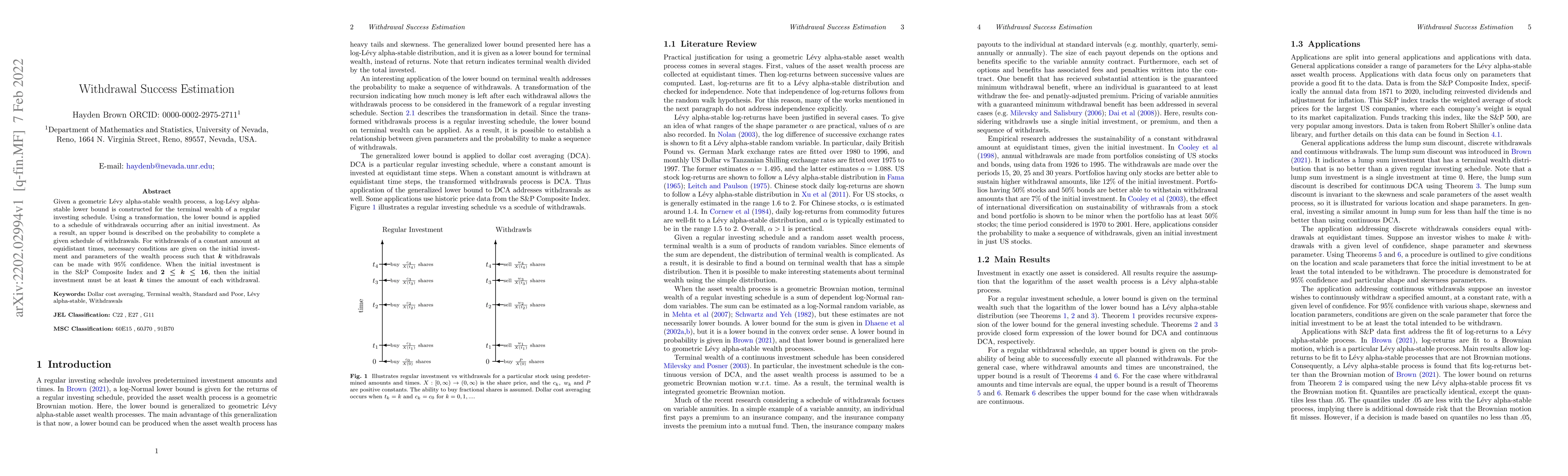

Given a geometric Levy alpha-stable wealth process, a log-Levy alpha-stable lower bound is constructed for the terminal wealth of a regular investing schedule. Using a transformation, the lower boun...

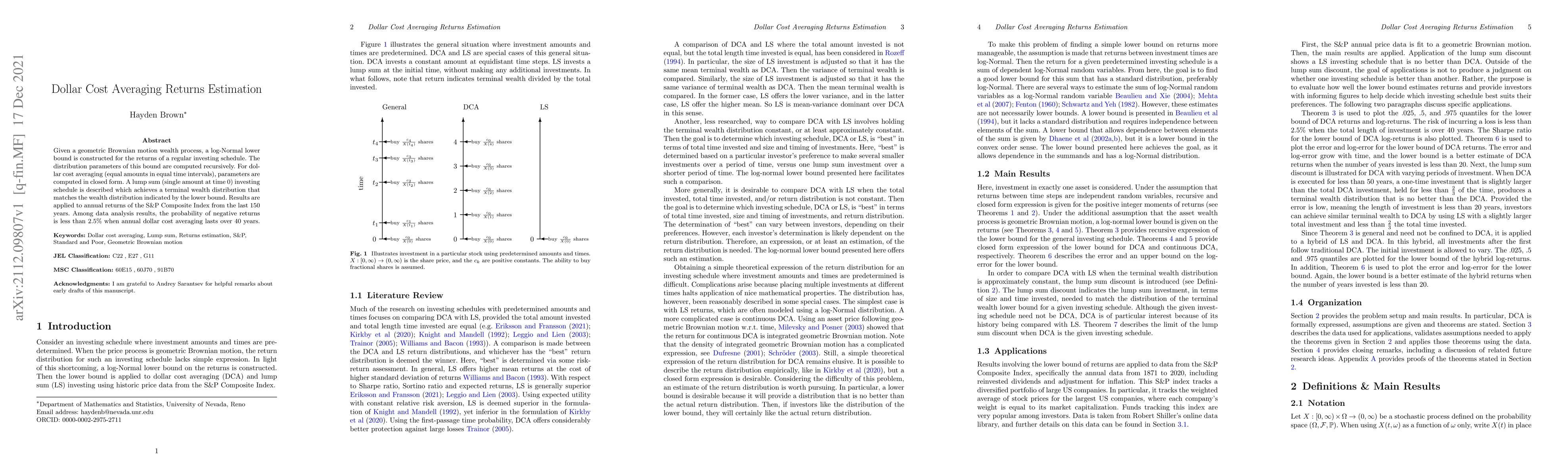

Given a geometric Brownian motion wealth process, a log-Normal lower bound is constructed for the returns of a regular investing schedule. The distribution parameters of this bound are computed recu...

Heisenberg exchange coupling (HC) and biquadratic exchange coupling (BQC) are known to occur in magnetic tunnel junctions (MTJ) and nanoscale spintronics structures. MTJ-based molecular spintronics de...