Academic Profile

Statistics

Similar Authors

Papers on arXiv

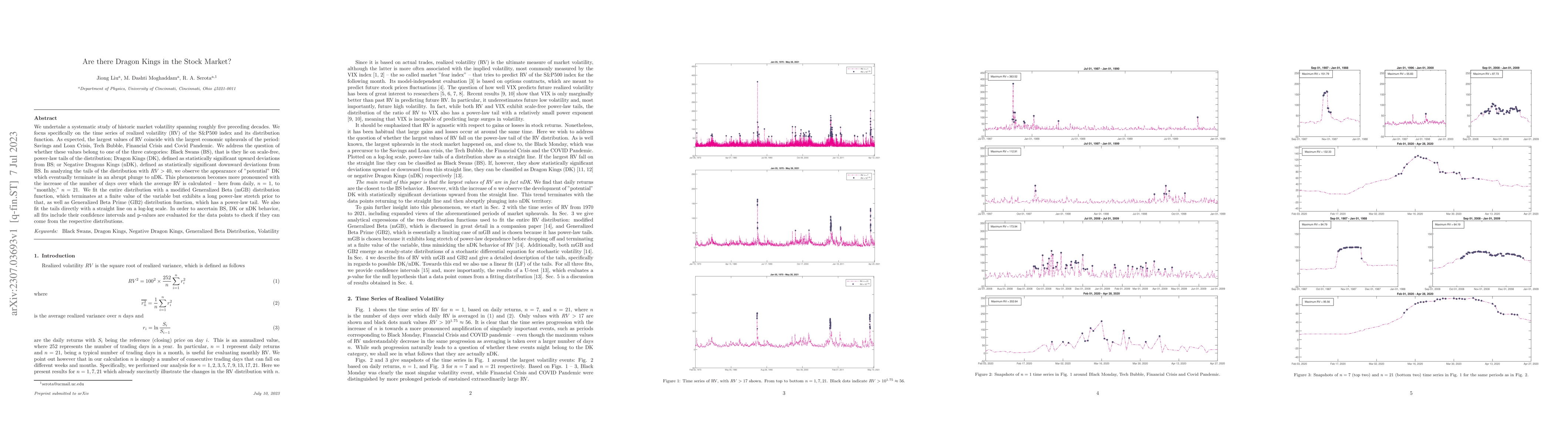

We undertake a systematic study of historic market volatility spanning roughly five preceding decades. We focus specifically on the time series of realized volatility (RV) of the S&P500 index and it...

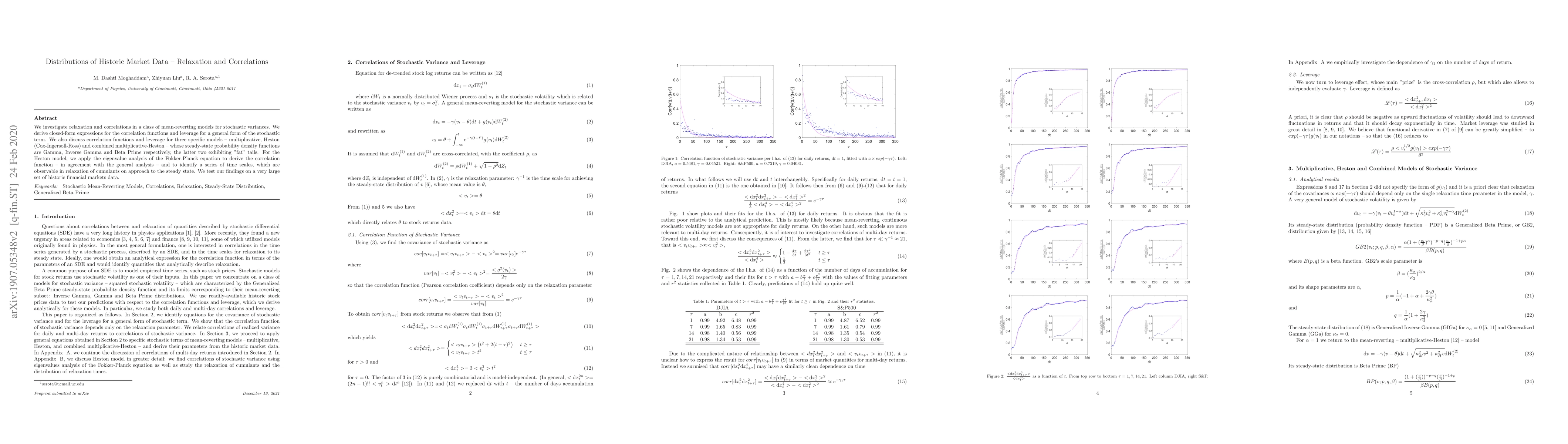

We investigate relaxation and correlations in a class of mean-reverting models for stochastic variances. We derive closed-form expressions for the correlation functions and leverage for a general fo...

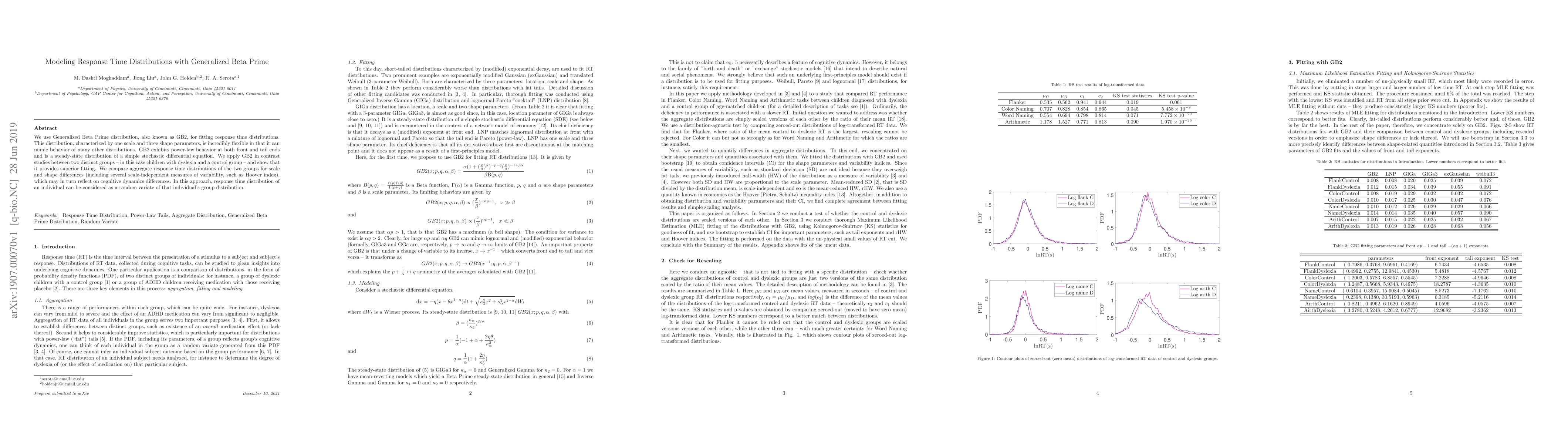

We use Generalized Beta Prime distribution, also known as GB2, for fitting response time distributions. This distribution, characterized by one scale and three shape parameters, is incredibly flexib...

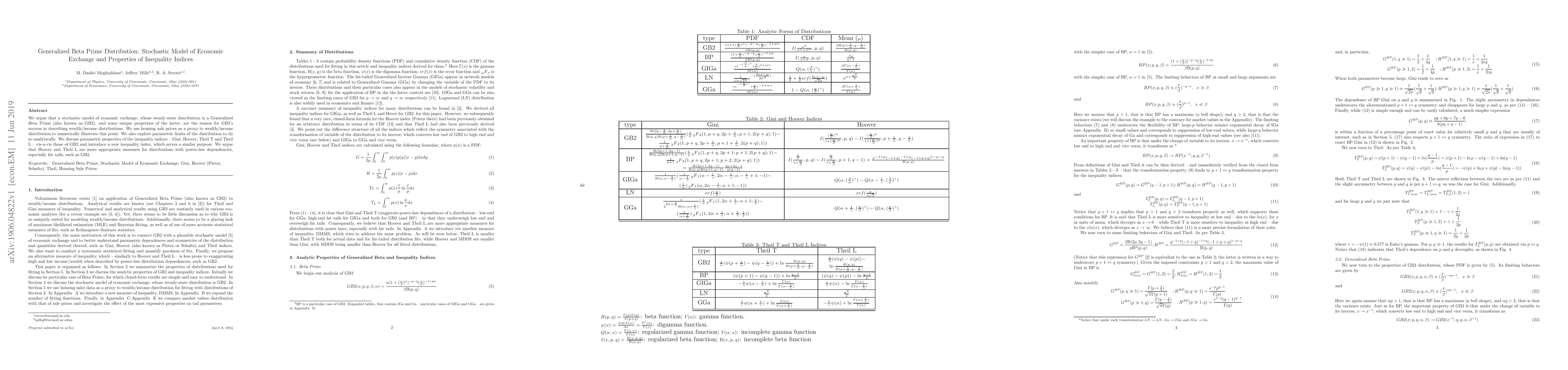

We argue that a stochastic model of economic exchange, whose steady-state distribution is a Generalized Beta Prime (also known as GB2), and some unique properties of the latter, are the reason for G...

We study distributions of realized variance (squared realized volatility) and squared implied volatility, as represented by VIX and VXO indices. We find that Generalized Beta distribution provide th...

We analyze correlations between squared volatility indices, VIX and VXO, and realized variances -- the known one, for the current month, and the predicted one, for the following month. We show that ...

We consider a model of stochastic volatility which combines features of the multiplicative model for large volatilities and of the Heston model for small volatilities. The steady-state distribution ...

We undertake a systematic comparison between implied volatility, as represented by VIX (new methodology) and VXO (old methodology), and realized volatility. We compare visually and statistically dis...