Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper, we introduce a suite of models for price-aware automated market making platforms willing to optimize their quotes. These models incorporate advanced price dynamics, including stochast...

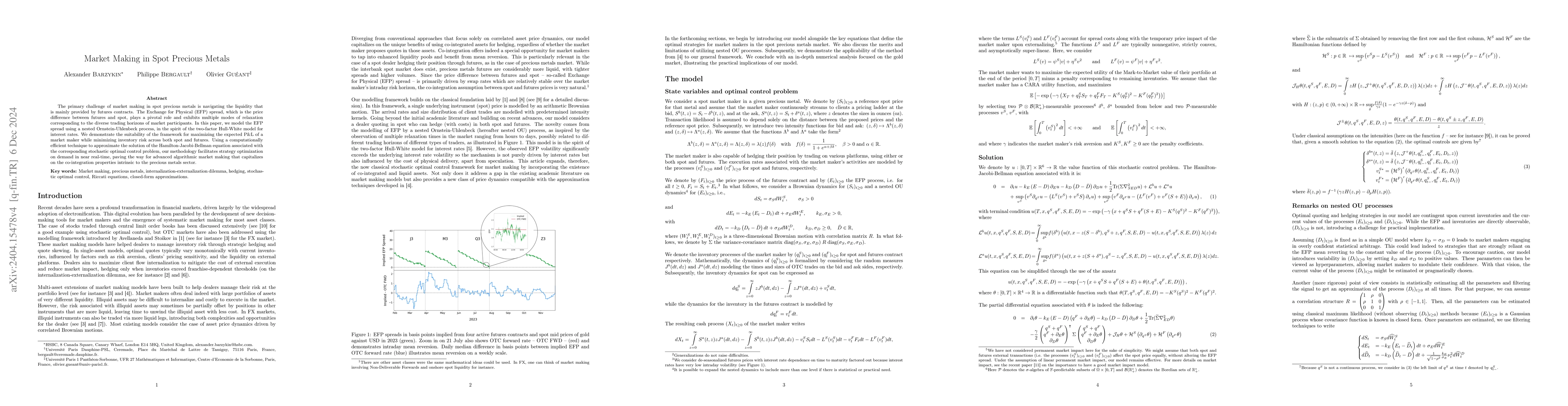

The primary challenge of market making in spot precious metals is navigating the liquidity that is mainly provided by futures contracts. The Exchange for Physical (EFP) spread, which is the price di...

This paper introduces a novel methodology for the pricing and management of share buyback contracts, overcoming the limitations of traditional optimal control methods, which frequently encounter dif...

Portfolio optimization methods have evolved significantly since Markowitz introduced the mean-variance framework in 1952. While the theoretical appeal of this approach is undeniable, its practical i...

To assign a value to a portfolio, it is common to use Mark-to-Market prices. However, how should one proceed when the securities are illiquid? When transaction prices are scarce, how can one use all...

With the emergence of decentralized finance, new trading mechanisms called Automated Market Makers have appeared. The most popular Automated Market Makers are Constant Function Market Makers. They h...

Modern portfolio theory has provided for decades the main framework for optimizing portfolios. Because of its sensitivity to small changes in input parameters, especially expected returns, the mean-...

In FX cash markets, market makers provide liquidity to clients for a wide variety of currency pairs. Because of flow uncertainty and market volatility, they face inventory risk. To mitigate this ris...

Dealers make money by providing liquidity to clients but face flow uncertainty and thus price risk. They can efficiently skew their prices and wait for clients to mitigate risk (internalization), or...

In dealer markets, dealers provide prices at which they agree to buy and sell the assets and securities they have in their scope. With ever increasing trading volume, this quoting task has to be don...

In recent years, academics, regulators, and market practitioners have increasingly addressed liquidity issues. Amongst the numerous problems addressed, the optimal execution of large orders is proba...

For optimal control problems on finite graphs in continuous time, the dynamic programming principle leads to value functions characterized by systems of nonlinear ordinary differential equations. In...

In this paper, we address the question of the optimal Delta and Vega hedging of a book of exotic options when there are execution costs associated with the trading of vanilla options. In a framework...

In corporate bond markets, which are mainly OTC markets, market makers play a central role by providing bid and ask prices for a large number of bonds to asset managers from all around the globe. De...

In this article, we tackle the problem of a market maker in charge of a book of options on a single liquid underlying asset. By using an approximation of the portfolio in terms of its vega, we show ...

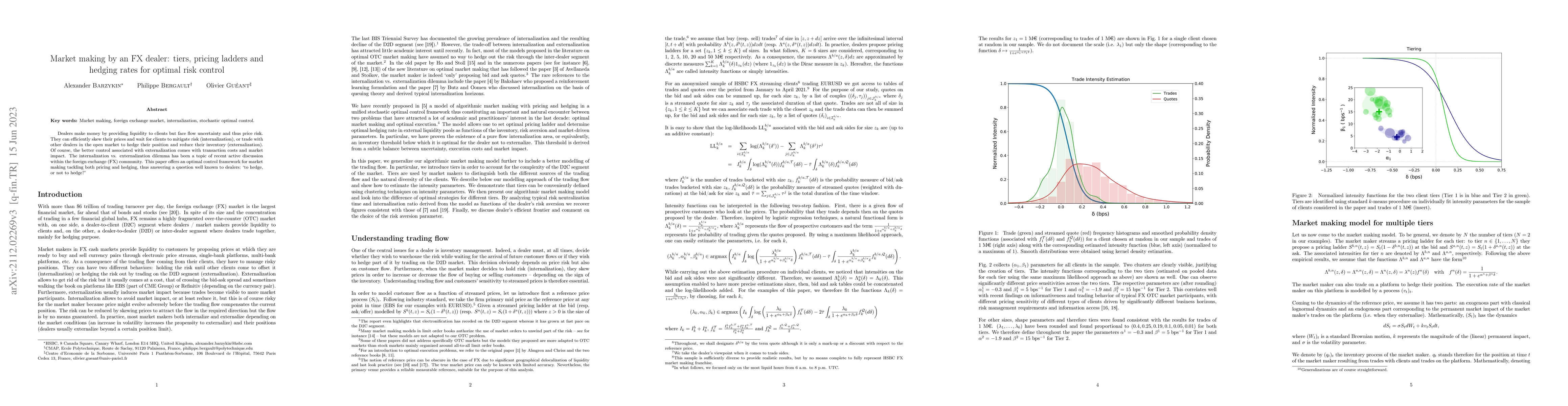

In most OTC markets, a small number of market makers provide liquidity to other market participants. More precisely, for a list of assets, they set prices at which they agree to buy and sell. Market...

The literature on continuous-time stochastic optimal control seldom deals with the case of discrete state spaces. In this paper, we provide a general framework for the optimal control of continuous-...

A large proportion of market making models derive from the seminal model of Avellaneda and Stoikov. The numerical approximation of the value function and the optimal quotes in these models remains a...

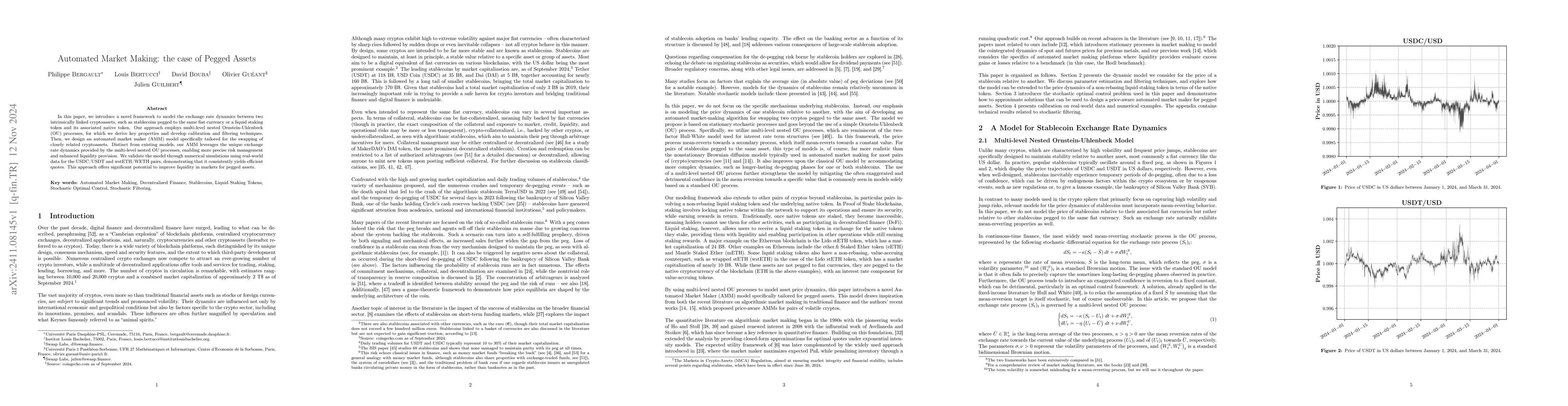

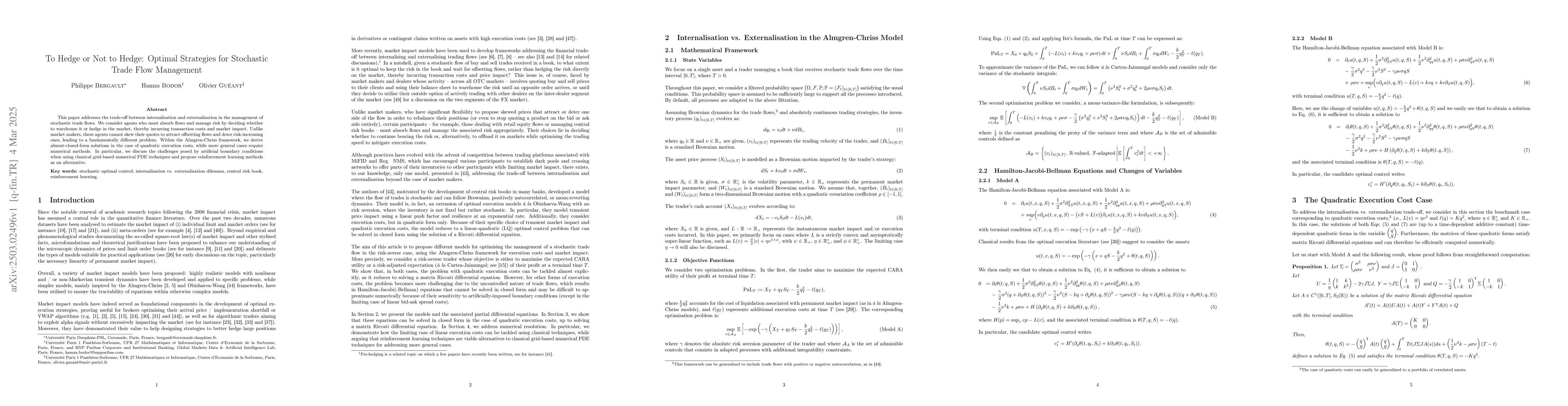

In this paper, we introduce a novel framework to model the exchange rate dynamics between two intrinsically linked cryptoassets, such as stablecoins pegged to the same fiat currency or a liquid stakin...

This paper addresses the trade-off between internalisation and externalisation in the management of stochastic trade flows. We consider agents who must absorb flows and manage risk by deciding whether...

In traditional financial markets, yield curves are widely available for countries (and, by extension, currencies), financial institutions, and large corporates. These curves are used to calibrate stoc...

Over the past decade, many dealers have implemented algorithmic models to automatically respond to RFQs and manage flows originating from their electronic platforms. In parallel, building on the found...