Academic Profile

Statistics

Similar Authors

Papers on arXiv

When estimating the risk of a financial position with empirical data or Monte Carlo simulations via a tail-dependent law invariant risk measure such as the Conditional Value-at-Risk (CVaR), it is im...

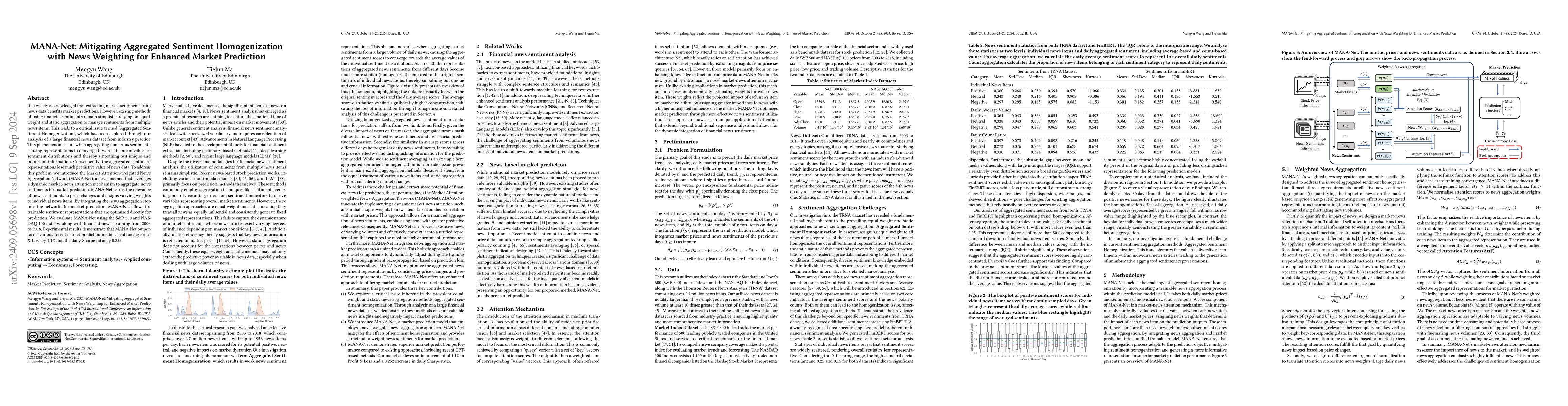

It is widely acknowledged that extracting market sentiments from news data benefits market predictions. However, existing methods of using financial sentiments remain simplistic, relying on equal-weig...

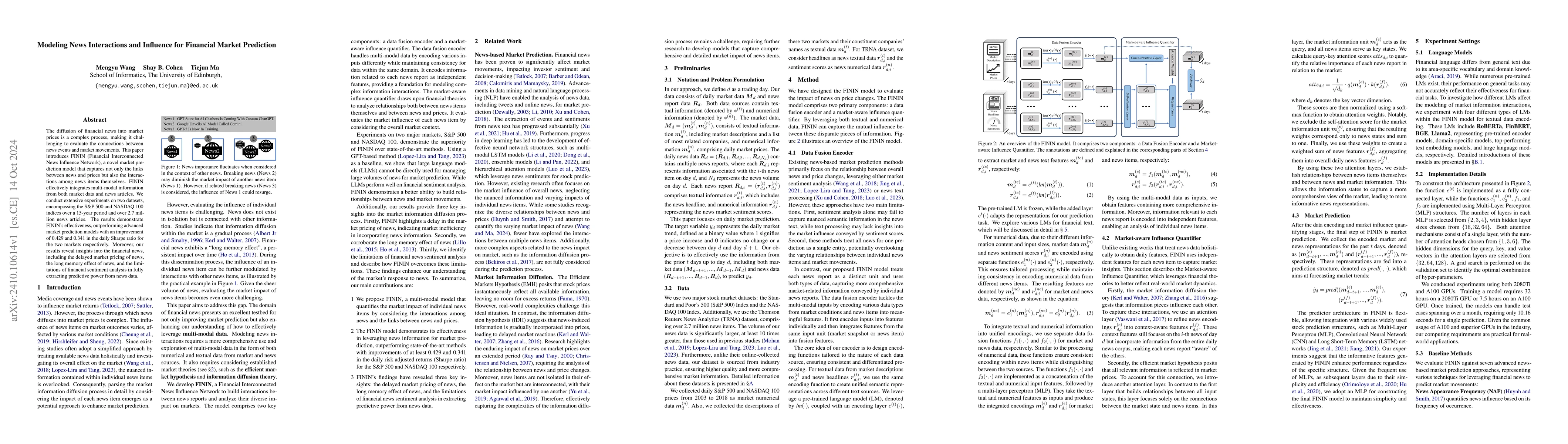

The diffusion of financial news into market prices is a complex process, making it challenging to evaluate the connections between news events and market movements. This paper introduces FININ (Financ...

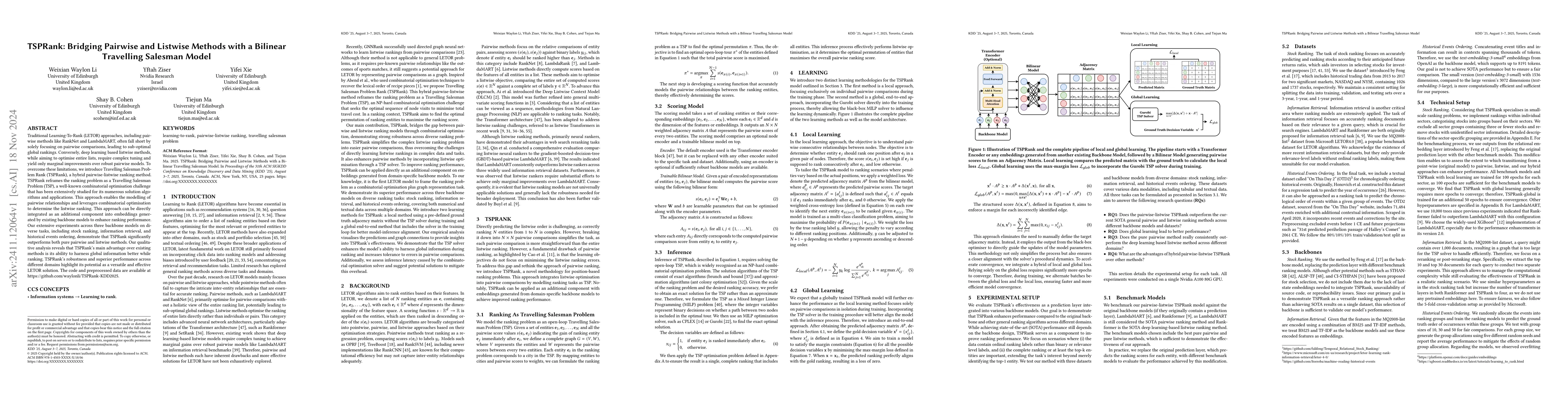

Traditional Learning-To-Rank (LETOR) approaches, including pairwise methods like RankNet and LambdaMART, often fall short by solely focusing on pairwise comparisons, leading to sub-optimal global rank...

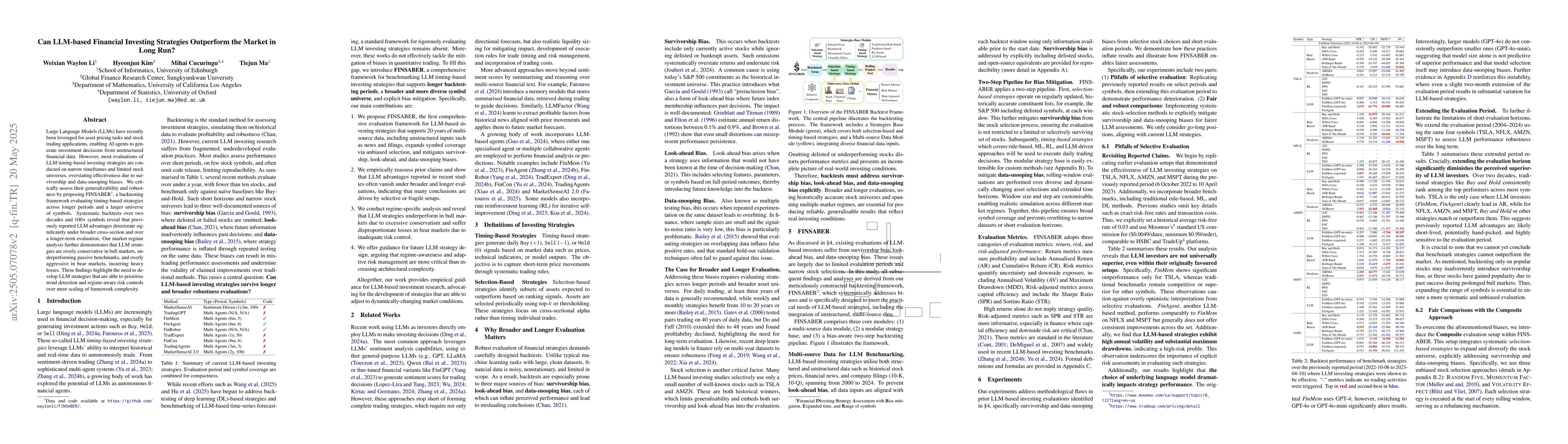

Large Language Models (LLMs) have recently been leveraged for asset pricing tasks and stock trading applications, enabling AI agents to generate investment decisions from unstructured financial data. ...

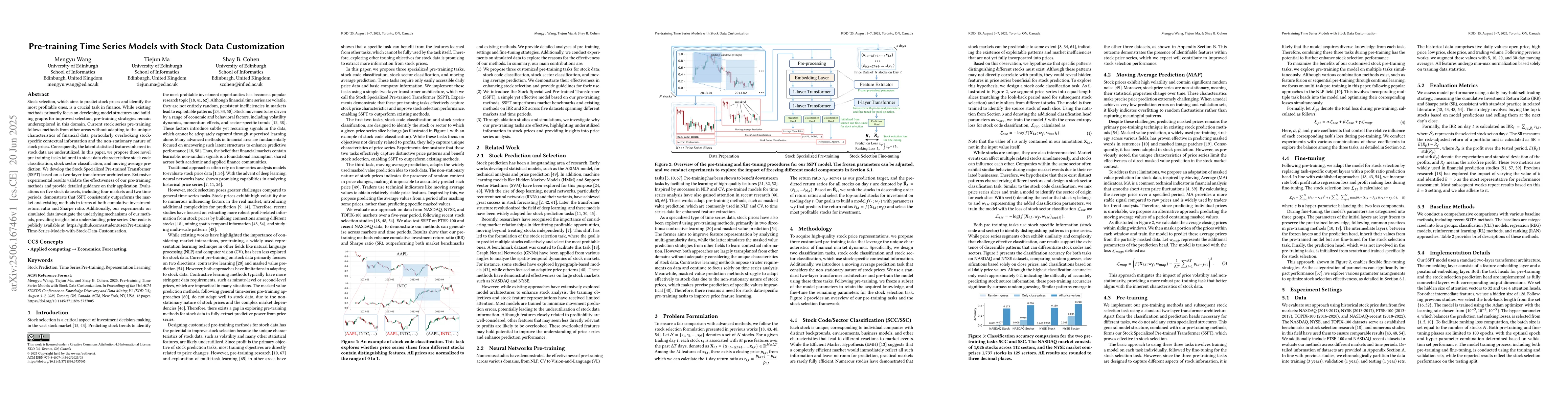

Stock selection, which aims to predict stock prices and identify the most profitable ones, is a crucial task in finance. While existing methods primarily focus on developing model structures and build...

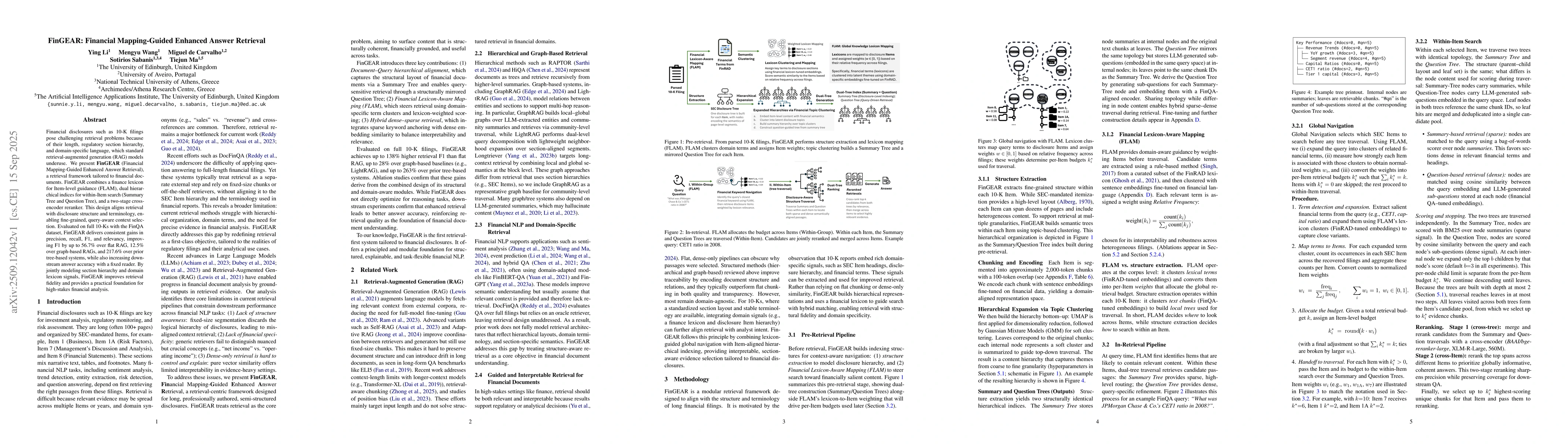

Financial disclosures such as 10-K filings present challenging retrieval problems due to their length, regulatory section hierarchy, and domain-specific language, which standard retrieval-augmented ge...

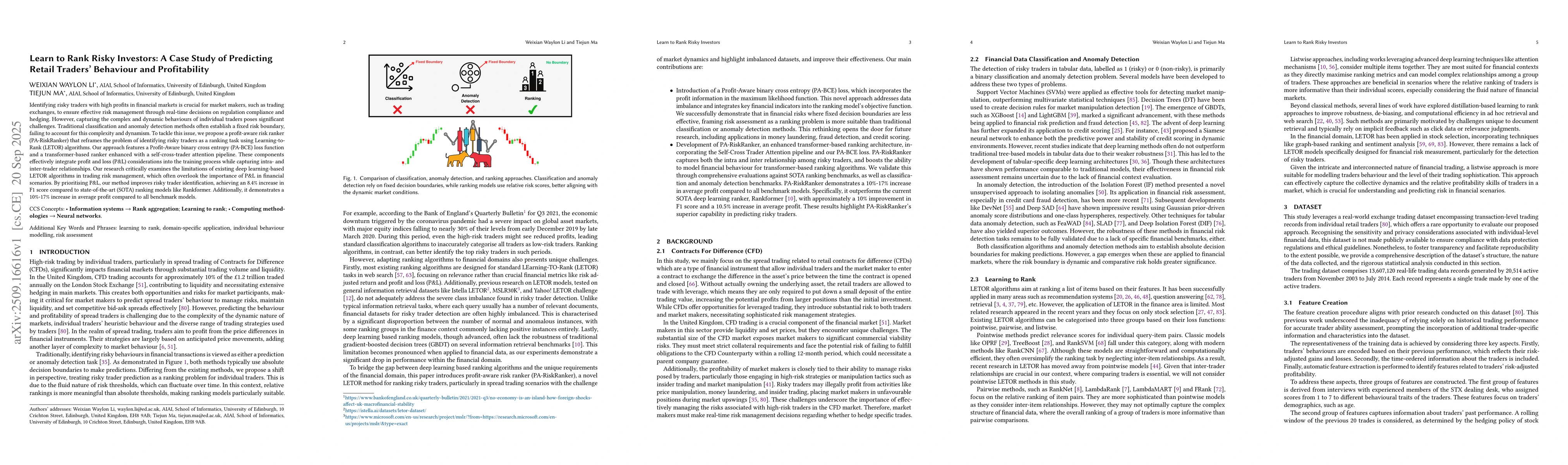

Identifying risky traders with high profits in financial markets is crucial for market makers, such as trading exchanges, to ensure effective risk management through real-time decisions on regulation ...

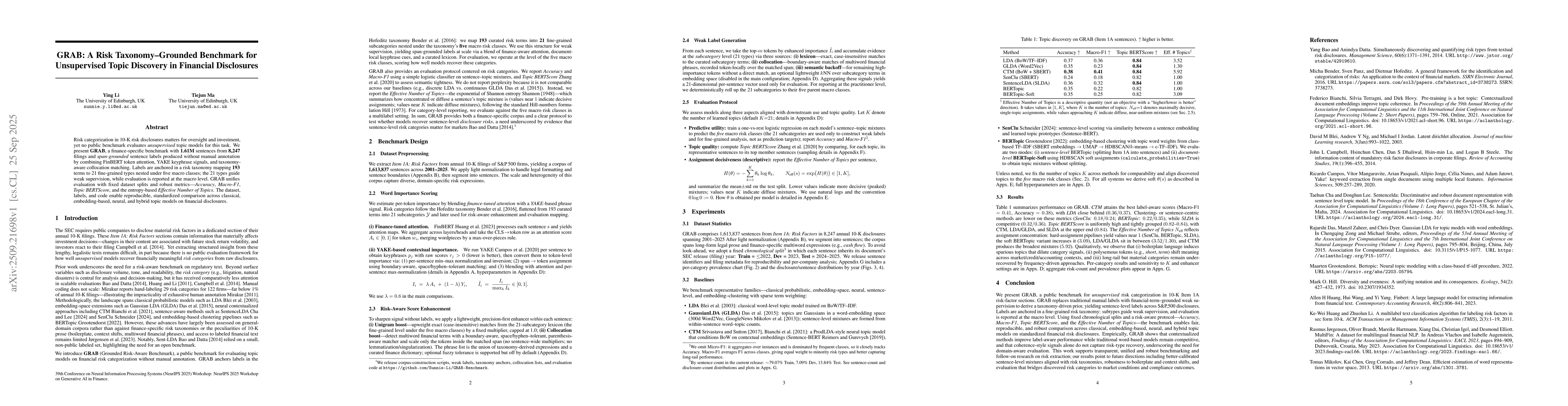

Risk categorization in 10-K risk disclosures matters for oversight and investment, yet no public benchmark evaluates unsupervised topic models for this task. We present GRAB, a finance-specific benchm...

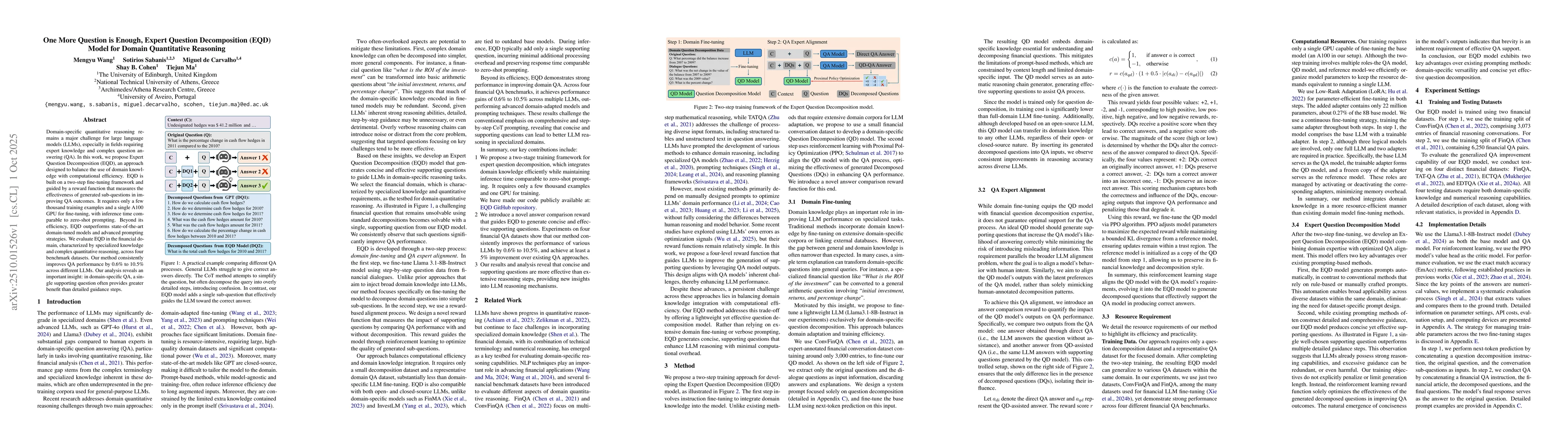

Domain-specific quantitative reasoning remains a major challenge for large language models (LLMs), especially in fields requiring expert knowledge and complex question answering (QA). In this work, we...

The parallel Byzantine Fault Tolerant (BFT) protocol is viewed as a promising solution to address the consensus scalability issue of the permissioned blockchain. One of the main challenges in parallel...

Attention steering is an important technique for controlling model focus, enabling capabilities such as prompt highlighting, where the model prioritises user-specified text. However, existing attentio...

Parallel Byzantine Fault Tolerant (BFT) protocols based on committee-based sharding improve scalability but weaken safety since smaller node groups are responsible for consensus. Recent approaches int...

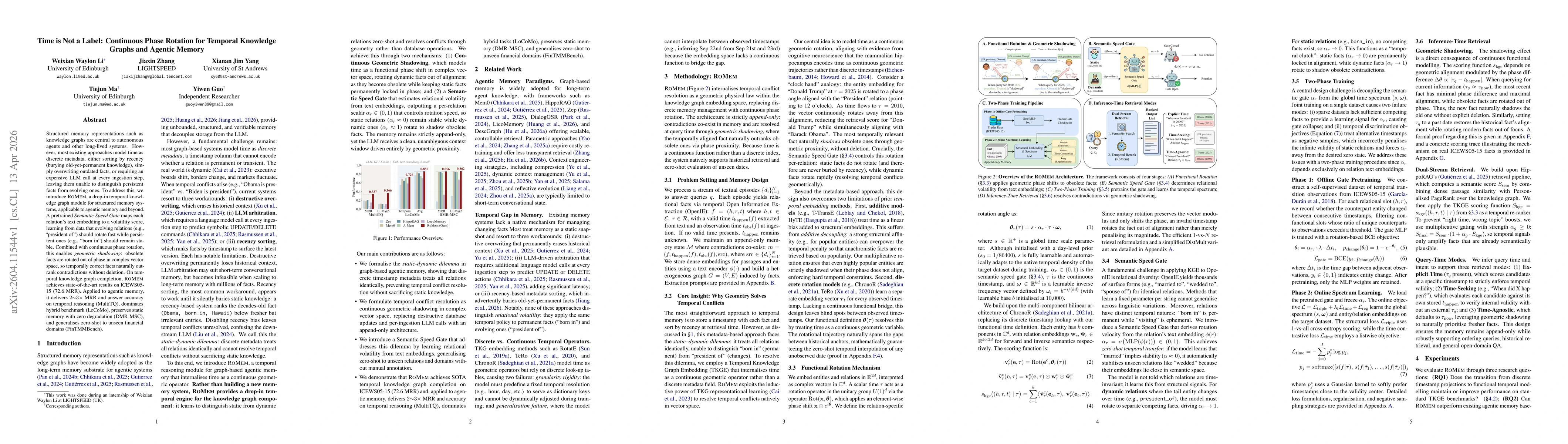

Structured memory representations such as knowledge graphs are central to autonomous agents and other long-lived systems. However, most existing approaches model time as discrete metadata, either sort...

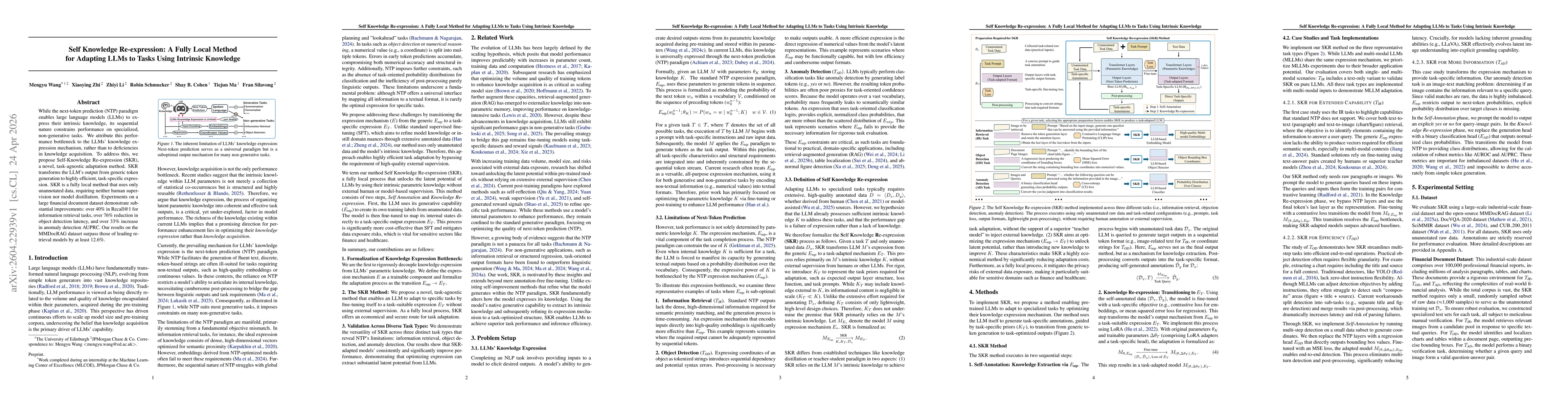

While the next-token prediction (NTP) paradigm enables large language models (LLMs) to express their intrinsic knowledge, its sequential nature constrains performance on specialized, non-generative ta...

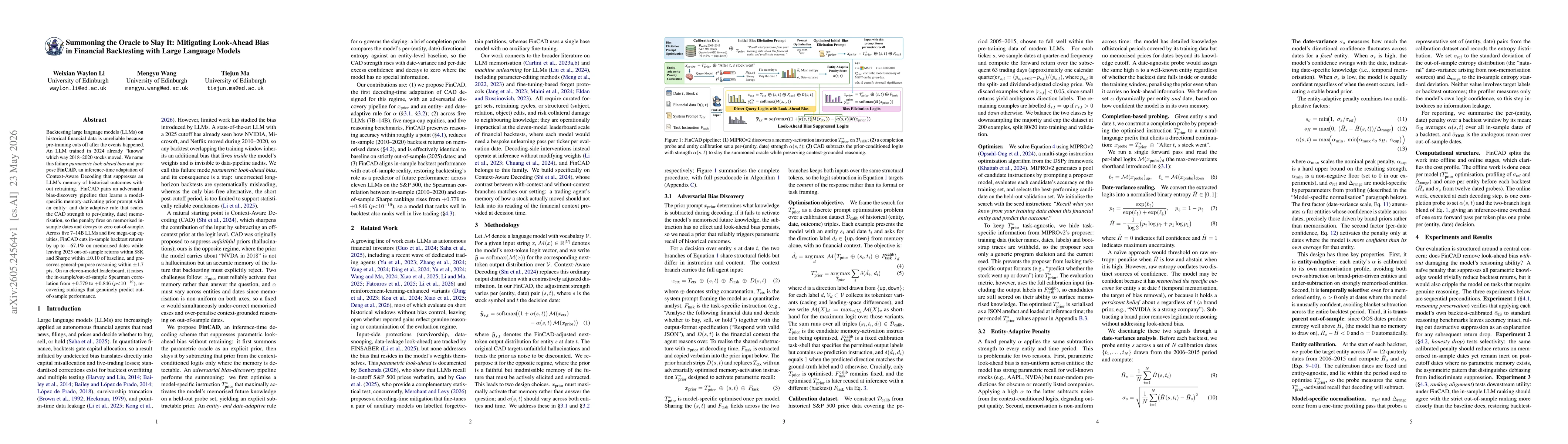

Backtesting large language models (LLMs) on historical financial data is unreliable because pre-training cuts off after the events happened. An LLM trained in 2024 already "knows" which way 2018-2020 ...