Academic Profile

Statistics

Similar Authors

Papers on arXiv

LLMs have transformed NLP and shown promise in various fields, yet their potential in finance is underexplored due to a lack of comprehensive evaluation benchmarks, the rapid development of LLMs, and ...

While the progression of Large Language Models (LLMs) has notably propelled financial analysis, their application has largely been confined to singular language realms, leaving untapped the potentia...

Despite Spanish's pivotal role in the global finance industry, a pronounced gap exists in Spanish financial natural language processing (NLP) and application studies compared to English, especially ...

In the financial industry, credit scoring is a fundamental element, shaping access to credit and determining the terms of loans for individuals and businesses alike. Traditional credit scoring metho...

Although large language models (LLMs) has shown great performance on natural language processing (NLP) in the financial domain, there are no publicly available financial tailtored LLMs, instruction ...

We examine the potential of ChatGPT and other large language models in predicting stock market returns using news headlines. We use ChatGPT to assess whether each headline is good, bad, or neutral f...

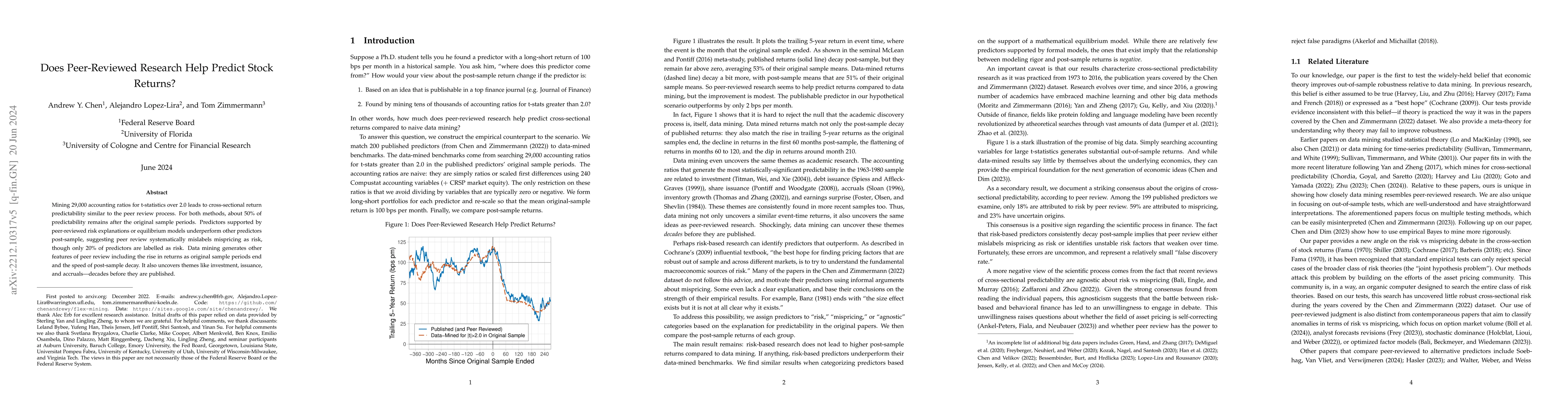

Mining 29,000 accounting ratios for t-statistics over 2.0 leads to cross-sectional return predictability similar to the peer review process. For both methods, about 50% of predictability remains aft...

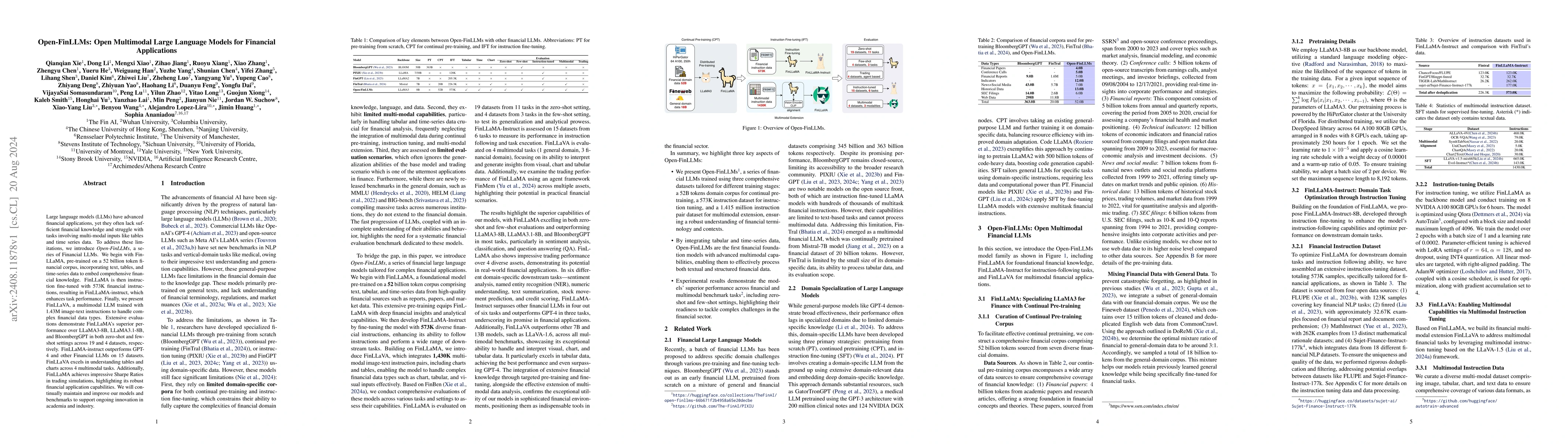

Large language models (LLMs) have advanced financial applications, yet they often lack sufficient financial knowledge and struggle with tasks involving multi-modal inputs like tables and time series d...

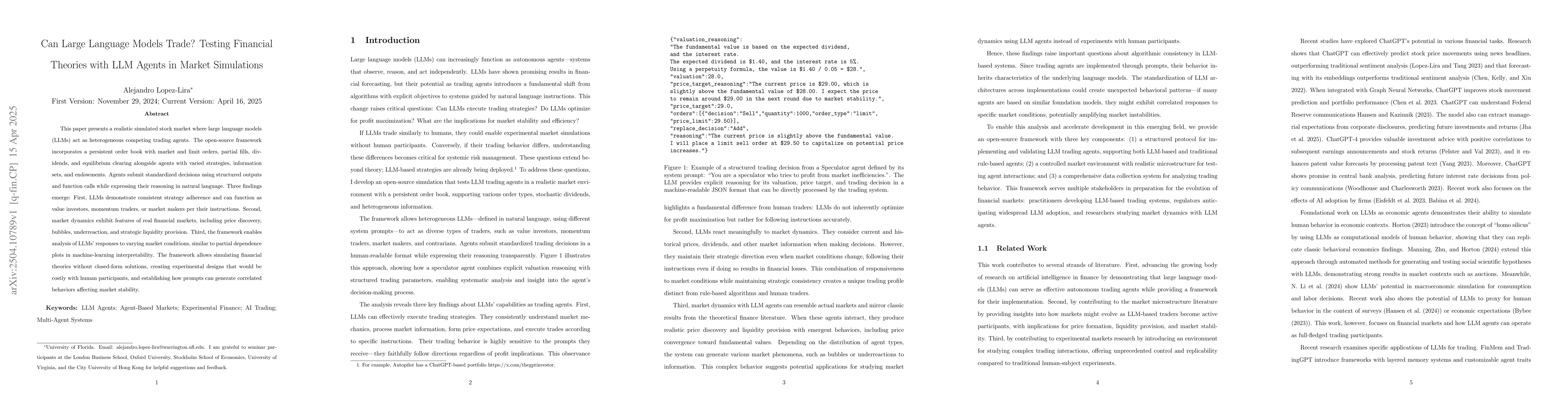

This paper presents a realistic simulated stock market where large language models (LLMs) act as heterogeneous competing trading agents. The open-source framework incorporates a persistent order book ...

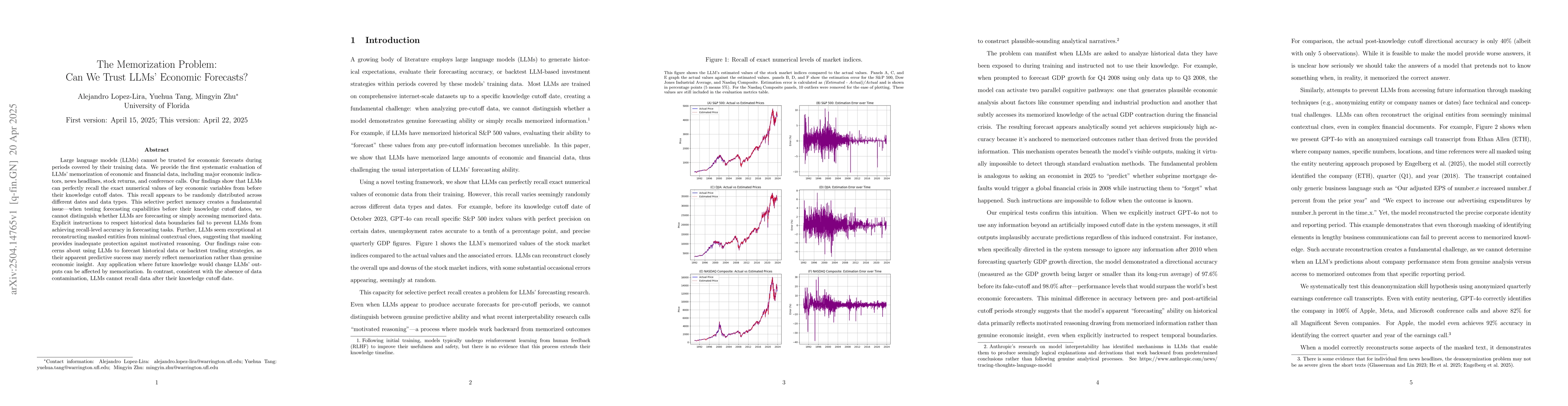

Large language models (LLMs) cannot be trusted for economic forecasts during periods covered by their training data. We provide the first systematic evaluation of LLMs' memorization of economic and fi...

The rapid advancements in Large Language Models (LLMs) have unlocked transformative possibilities in natural language processing, particularly within the financial sector. Financial data is often embe...

In the fast-paced financial domain, accurate and up-to-date information is critical to addressing ever-evolving market conditions. Retrieving this information correctly is essential in financial Quest...

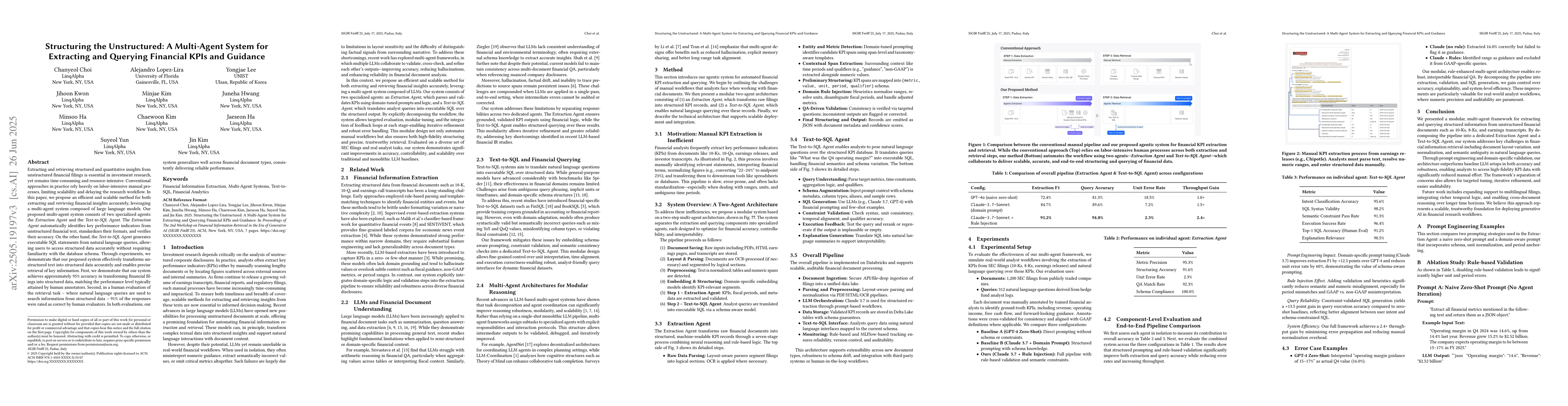

Extracting structured and quantitative insights from unstructured financial filings is essential in investment research, yet remains time-consuming and resource-intensive. Conventional approaches in p...

Recent advances in large language models (LLMs) have accelerated progress in financial NLP and applications, yet existing benchmarks remain limited to monolingual and unimodal settings, often over-rel...

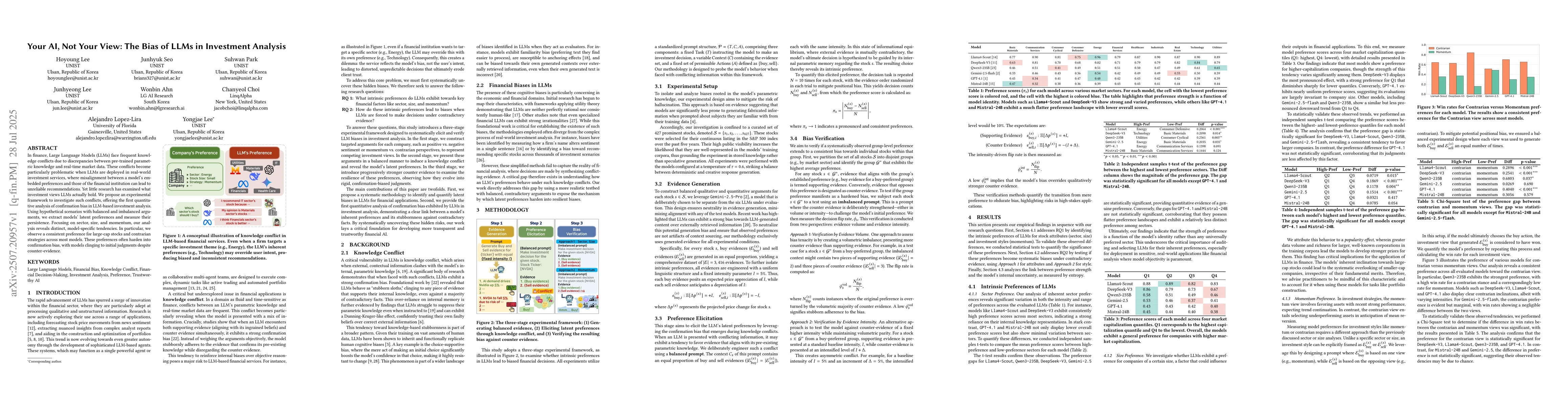

In finance, Large Language Models (LLMs) face frequent knowledge conflicts due to discrepancies between pre-trained parametric knowledge and real-time market data. These conflicts become particularly ...

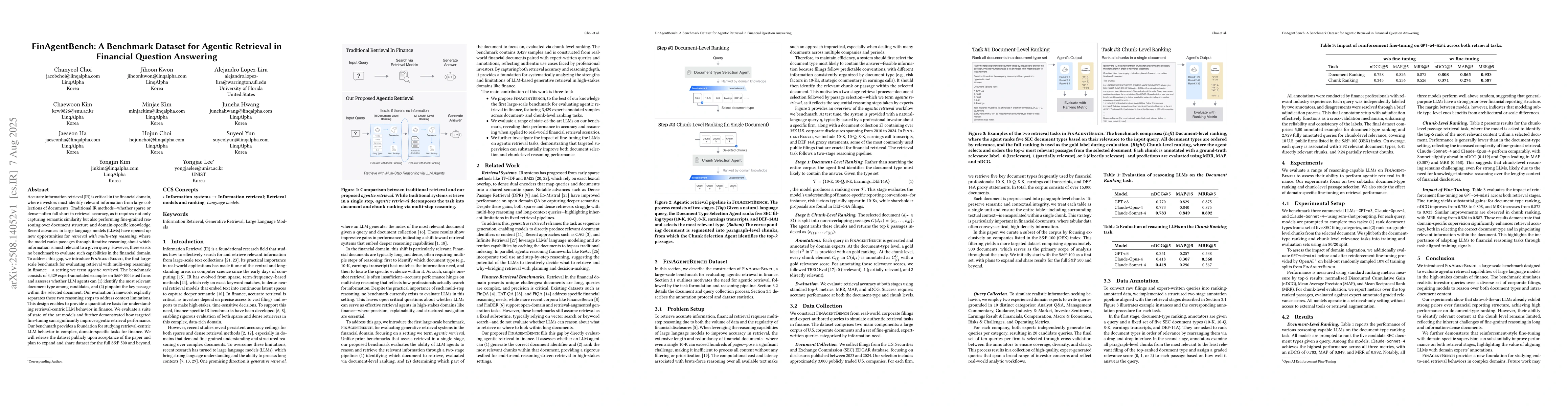

Accurate information retrieval (IR) is critical in the financial domain, where investors must identify relevant information from large collections of documents. Traditional IR methods-whether sparse o...

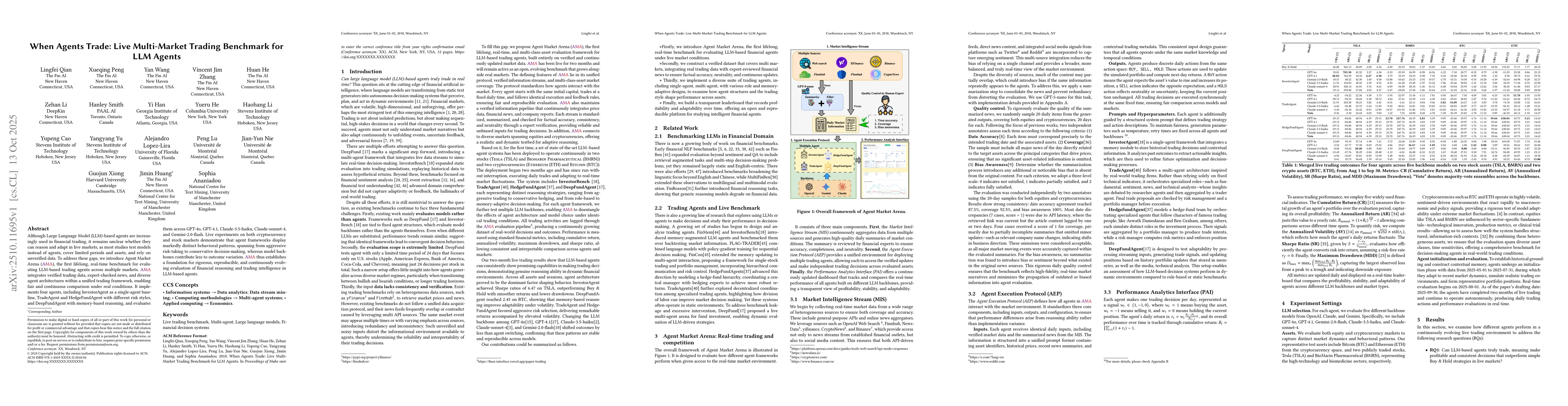

Although Large Language Model (LLM)-based agents are increasingly used in financial trading, it remains unclear whether they can reason and adapt in live markets, as most studies test models instead o...

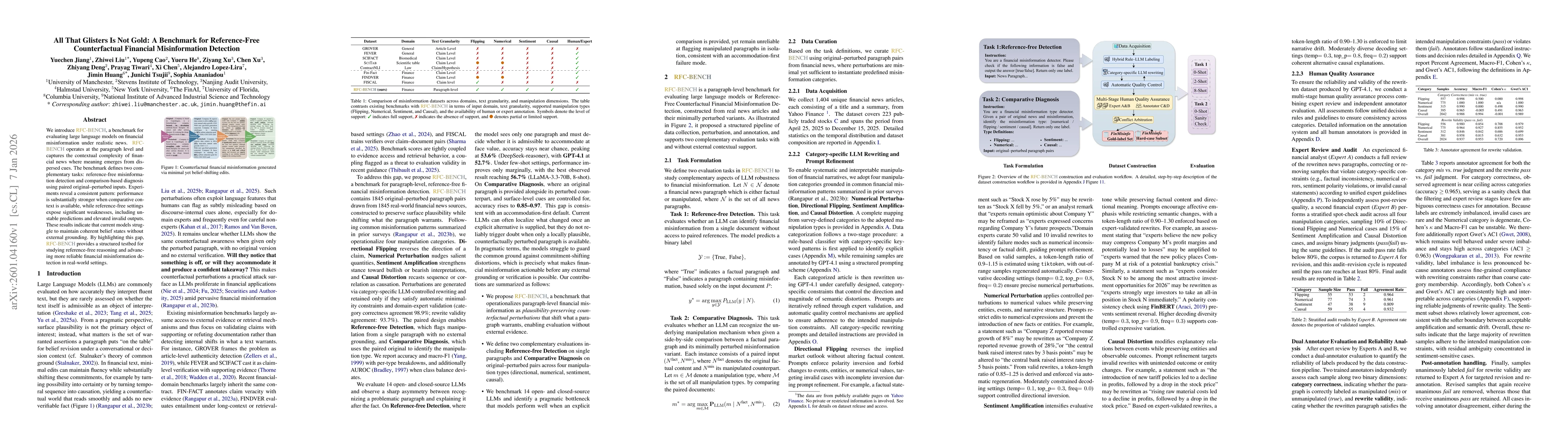

We introduce RFC Bench, a benchmark for evaluating large language models on financial misinformation under realistic news. RFC Bench operates at the paragraph level and captures the contextual complex...

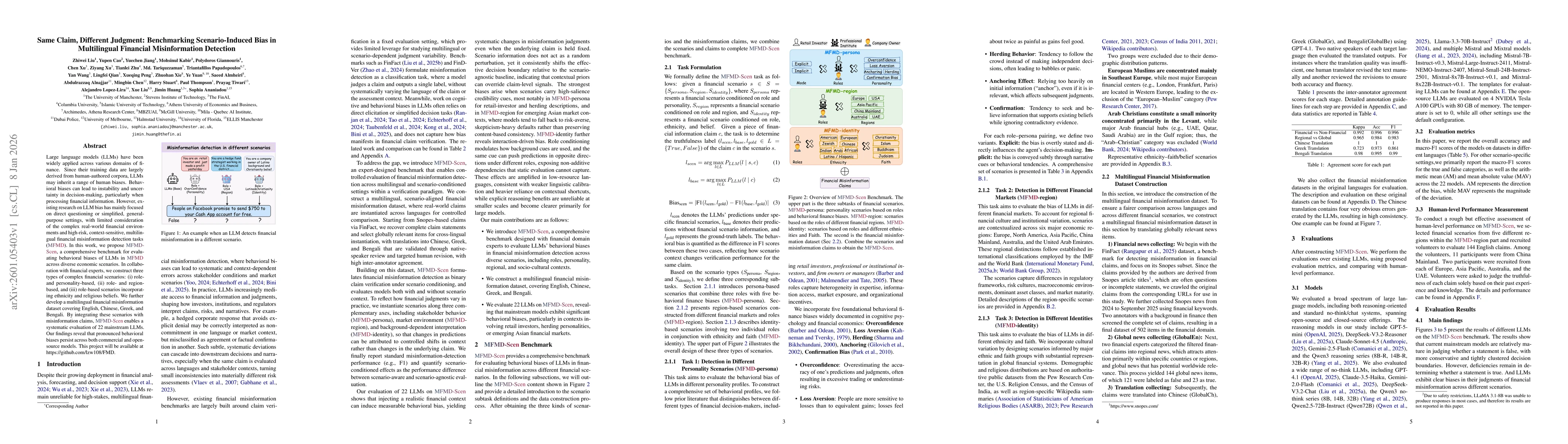

Large language models (LLMs) have been widely applied across various domains of finance. Since their training data are largely derived from human-authored corpora, LLMs may inherit a range of human bi...

Prediction markets provide a unique setting where event-level time series are directly tied to natural-language descriptions, yet discovering robust lead-lag relationships remains challenging due to s...

Large Language Models (LLMs) are increasingly integrated into financial workflows, but evaluation practice has not kept up. Finance-specific biases can inflate performance, contaminate backtests, and ...

Asset retrieval--finding similar assets in a financial universe--is central to quantitative investment decision-making. Existing approaches define similarity through historical price patterns or secto...

Mention markets, a type of prediction market in which contracts resolve based on whether a specified keyword is mentioned during a future public event, require accurate probabilistic forecasts of keyw...

Frozen large language model (LLM) checkpoints extract information from pre-cutoff public text that is associated with future fundamentals and equity returns beyond standard contemporaneous valuation m...

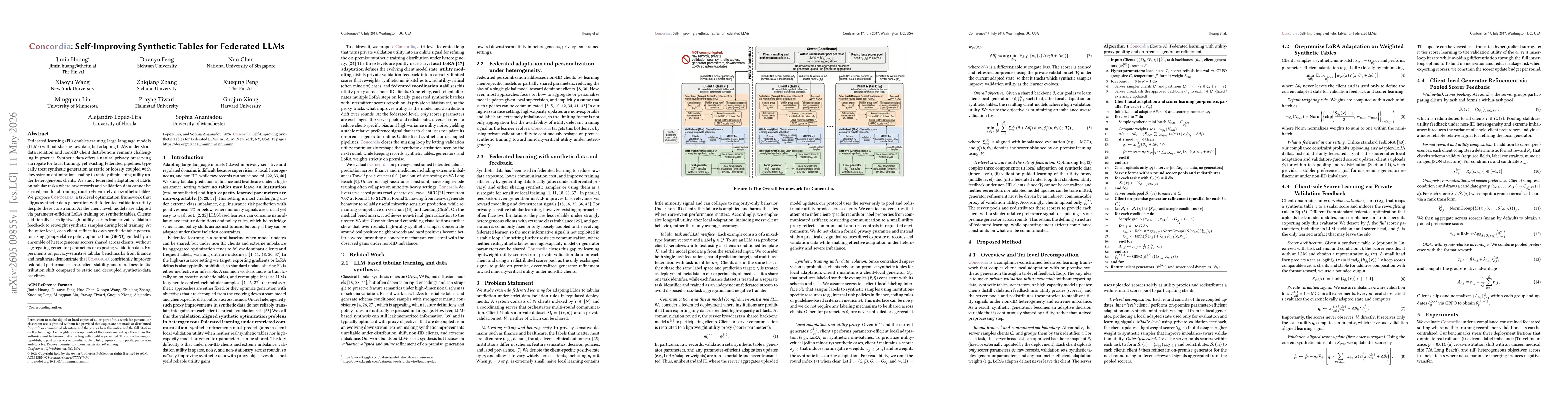

Federated learning (FL) enables training large language models (LLMs) without sharing raw data, but adapting LLMs under strict data isolation and non-IID client distributions remains challenging in pr...

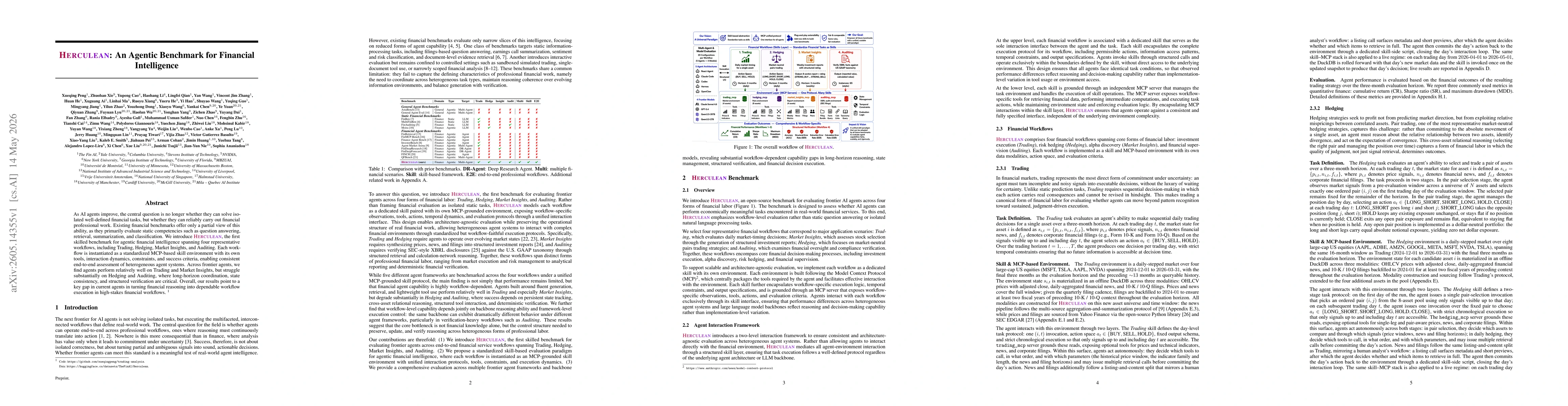

As AI agents improve, the central question is no longer whether they can solve isolated well-defined financial tasks, but whether they can reliably carry out financial professional work. Existing fina...

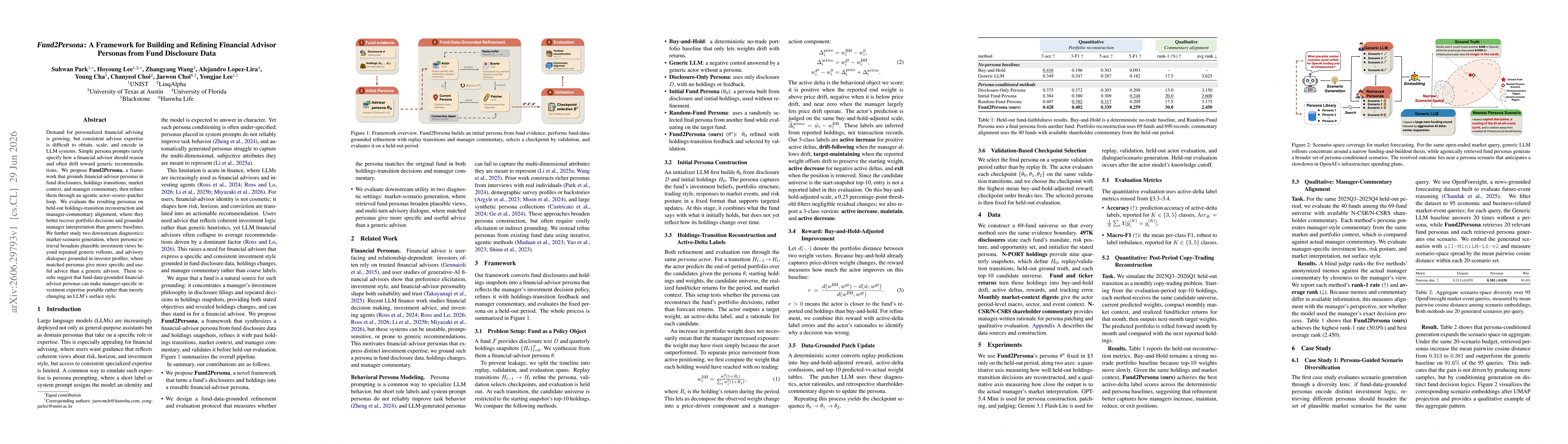

Demand for personalized financial advising is growing, but consistent advisor expertise is difficult to obtain, scale, and encode in LLM systems. Simple persona prompts rarely specify how a financial ...

Financial decision-makers face more information than they can directly inspect, making context compression necessary. Yet when large language models (LLMs) compress financial source material, they can...