Academic Profile

Statistics

Similar Authors

Papers on arXiv

Time-series data in real-world settings typically exhibit long-range dependencies and are observed at non-uniform intervals. In these settings, traditional sequence-based recurrent models struggle. ...

Time-series data in real-world medical settings typically exhibit long-range dependencies and are observed at non-uniform intervals. In such contexts, traditional sequence-based recurrent models str...

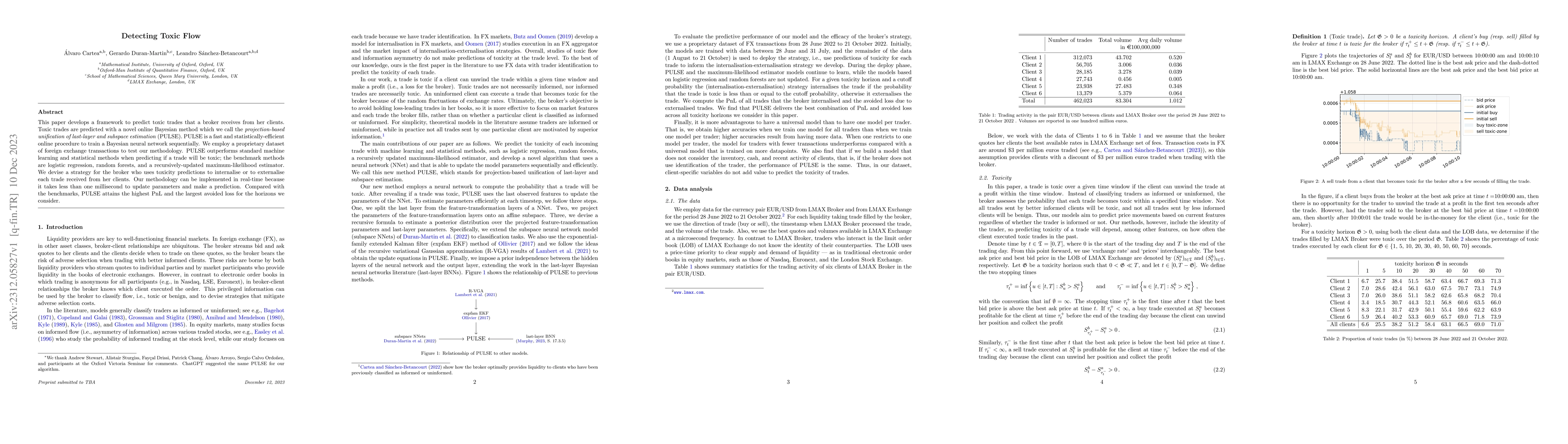

This paper develops a framework to predict toxic trades that a broker receives from her clients. Toxic trades are predicted with a novel online Bayesian method which we call the projection-based uni...

Constant product markets with concentrated liquidity (CL) are the most popular type of automated market makers. In this paper, we characterise the continuous-time wealth dynamics of strategic LPs wh...

Automated market makers (AMMs) are a new prototype of trading venues which are revolutionising the way market participants interact. At present, the majority of AMMs are constant function market mak...

We propose a price impact model where changes in prices are purely driven by the order flow in the market. The stochastic price impact of market orders and the arrival rates of limit and market orde...

We propose a novel framework to solve risk-sensitive reinforcement learning (RL) problems where the agent optimises time-consistent dynamic spectral risk measures. Based on the notion of conditional...

Linear multivariate Hawkes processes (MHP) are a fundamental class of point processes with self-excitation. When estimating parameters for these processes, a difficulty is that the two main error fu...

We develop the optimal trading strategy for a foreign exchange (FX) broker who must liquidate a large position in an illiquid currency pair. To maximize revenues, the broker considers trading in a c...

Latency (i.e., time delay) in electronic markets affects the efficacy of liquidity taking strategies. During the time liquidity takers process information and send marketable limit orders (MLOs) to ...

We study the perfect information Nash equilibrium between a broker and her clients -- an informed trader and an uniformed trader. In our model, the broker trades in the lit exchange where trades have ...

We model the trading activity between a broker and her clients (informed and uninformed traders) as an infinite-horizon stochastic control problem. We derive the broker's optimal dealing strategy in c...

We introduce scalable algorithms for online learning and generalized Bayesian inference of neural network parameters, designed for sequential decision making tasks. Our methods combine the strengths o...

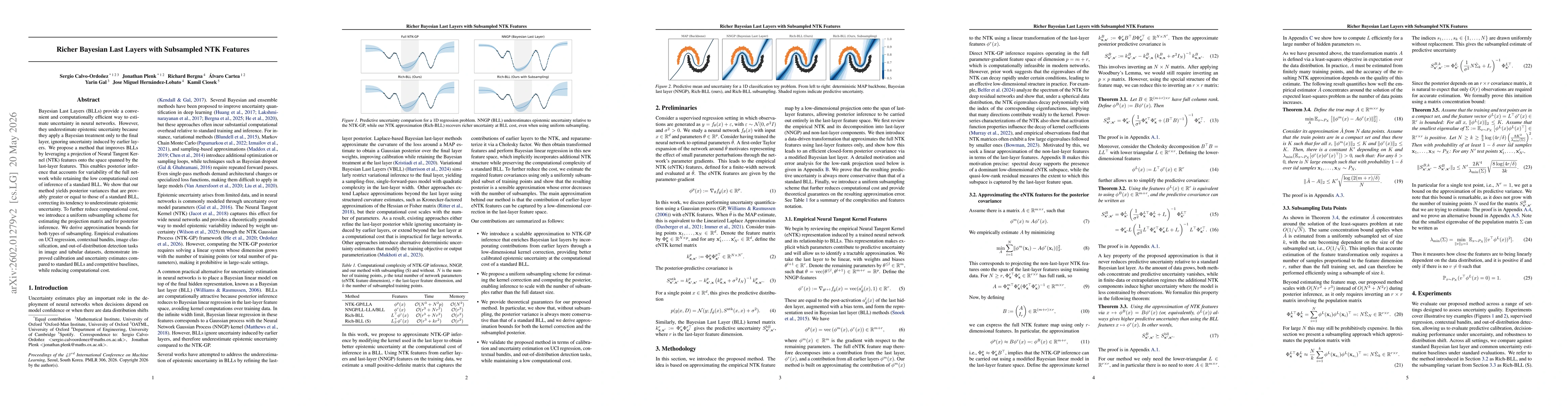

Bayesian Last Layers (BLLs) provide a convenient and computationally efficient way to estimate uncertainty in neural networks. However, they underestimate epistemic uncertainty because they apply a Ba...

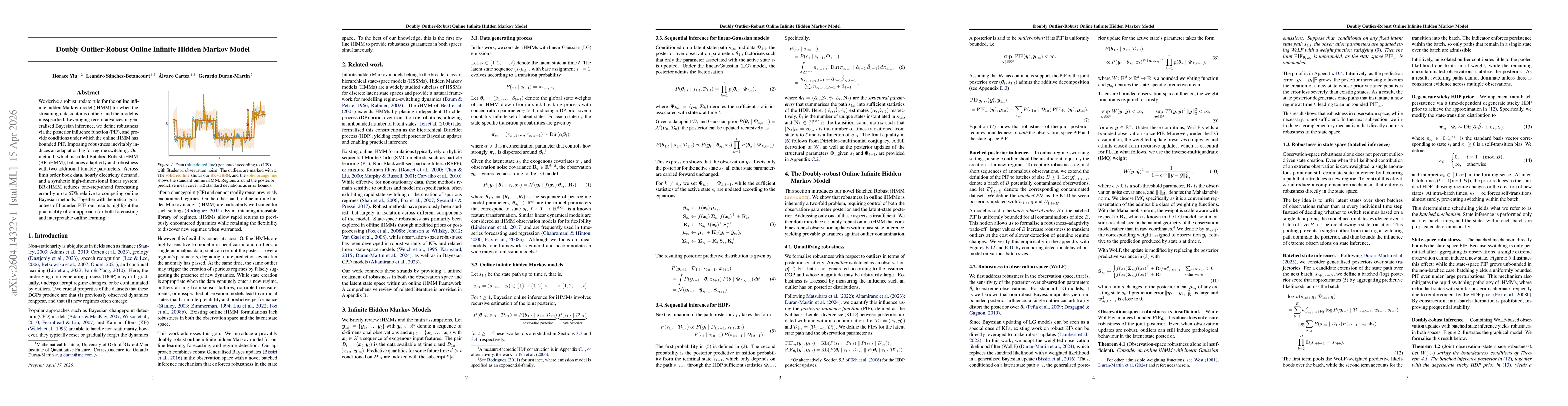

We derive a robust update rule for the online infinite hidden Markov model (iHMM) for when the streaming data contains outliers and the model is misspecified. Leveraging recent advances in generalised...

This paper develops a model to evaluate the viability of blockchain markets as the sole venue for price formation. Blockchains clear at discrete intervals called block time, and transactions are execu...