Academic Profile

Statistics

Similar Authors

Papers on arXiv

Take a multidimensional normally or obliquely reflected diffusion in a smooth domain. Approximate it by solutions of stochastic differential equations without reflection using the penalty method. Th...

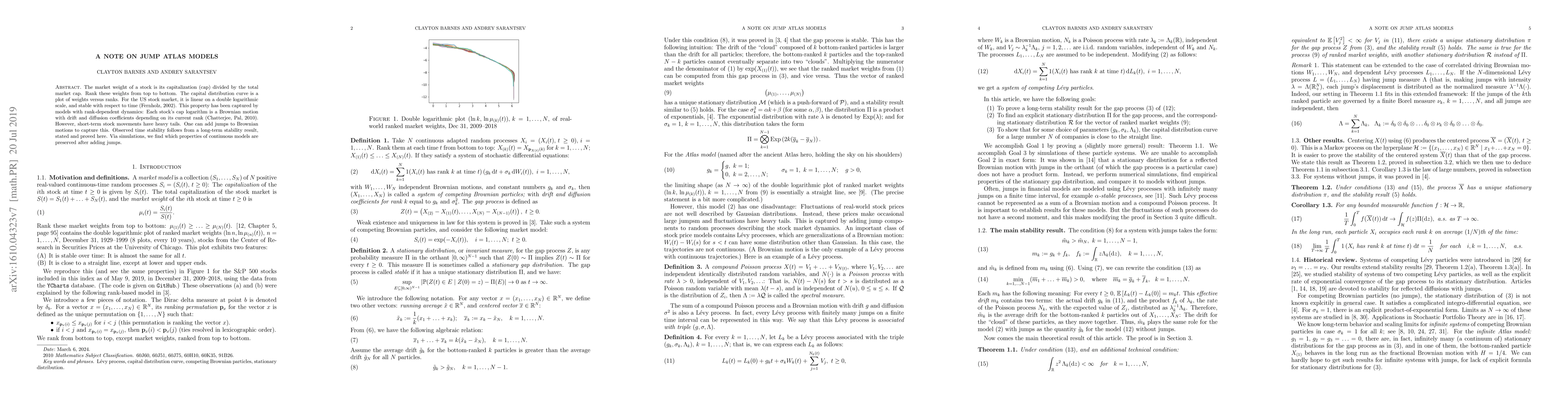

The market weight of a stock is its capitalization (cap) divided by the total market cap. Rank these weights from top to bottom. The capital distribution curve is a plot of weights versus ranks. For...

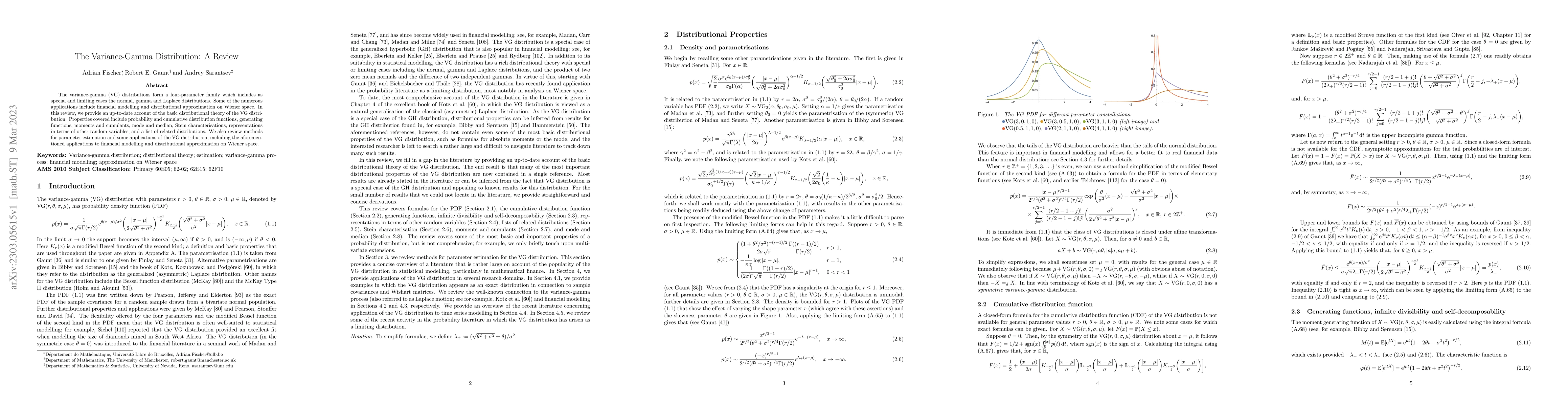

The variance-gamma (VG) distributions form a four-parameter family which includes as special and limiting cases the normal, gamma and Laplace distributions. Some of the numerous applications include...

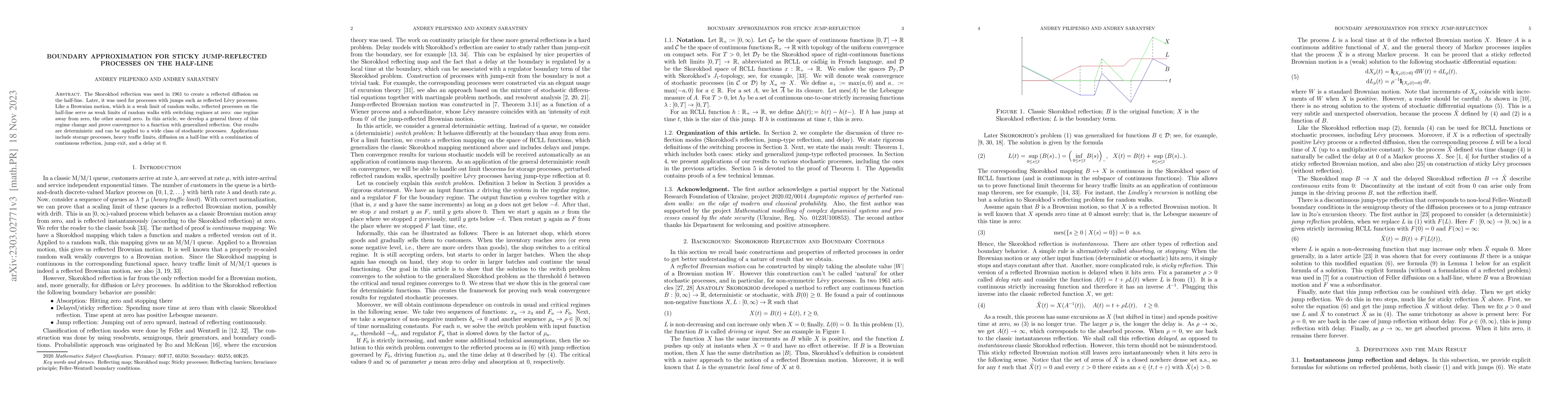

The Skorokhod reflection was used in 1961 to create a reflected diffusion on the half-line. Later, it was used for processes with jumps such as reflected L\'evy processes. Like a Brownian motion, wh...

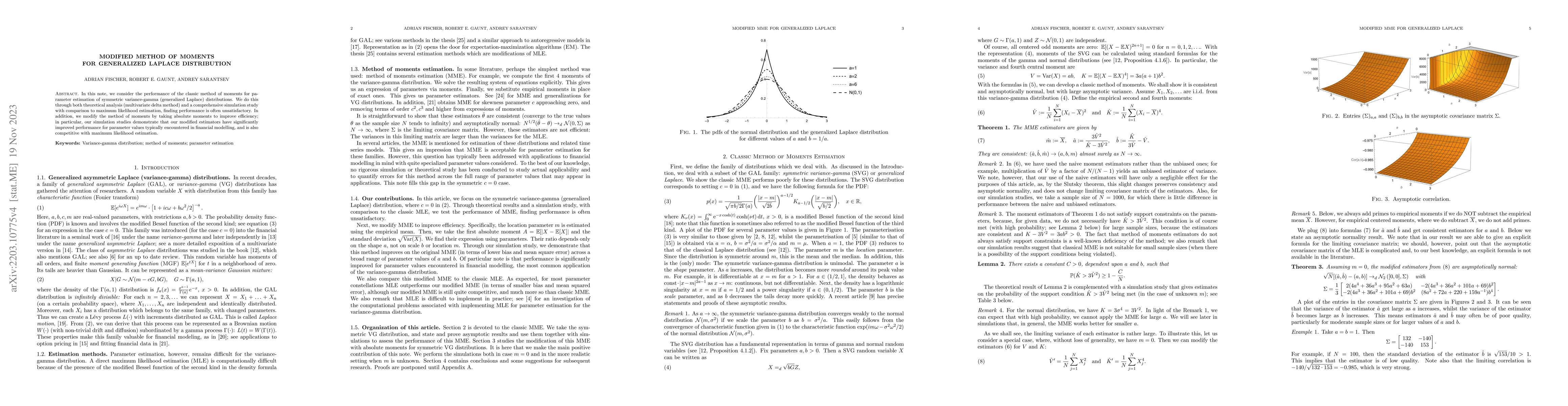

In this note, we consider the performance of the classic method of moments for parameter estimation of symmetric variance-gamma (generalized Laplace) distributions. We do this through both theoretic...

This paper studies birth and death processes in interactive random environments where the birth and death rates and the dynamics of the state of the environment are dependent on each other. Two mode...

Traditional white noise testing, for example the Ljung-Box test, studies only the autocorrelation function (ACF). Time series can be heteroscedastic and therefore not i.i.d. but still white noise (t...

Portfolio managers often evaluate performance relative to benchmark, usually taken to be the Standard & Poor 500 stock index fund. This relative portfolio wealth is defined as the absolute portfolio...

We propose to create a secondary beam of neutral kaons in Hall D at Jefferson Lab to be used with the GlueX experimental setup for strange hadron spectroscopy. The superior CEBAF electron beam will ...

Convergence rate to the stationary distribution for continuous-time Markov processes can be studied using Lyapunov functions. Recent work by the author provided explicit rates of convergence in spec...

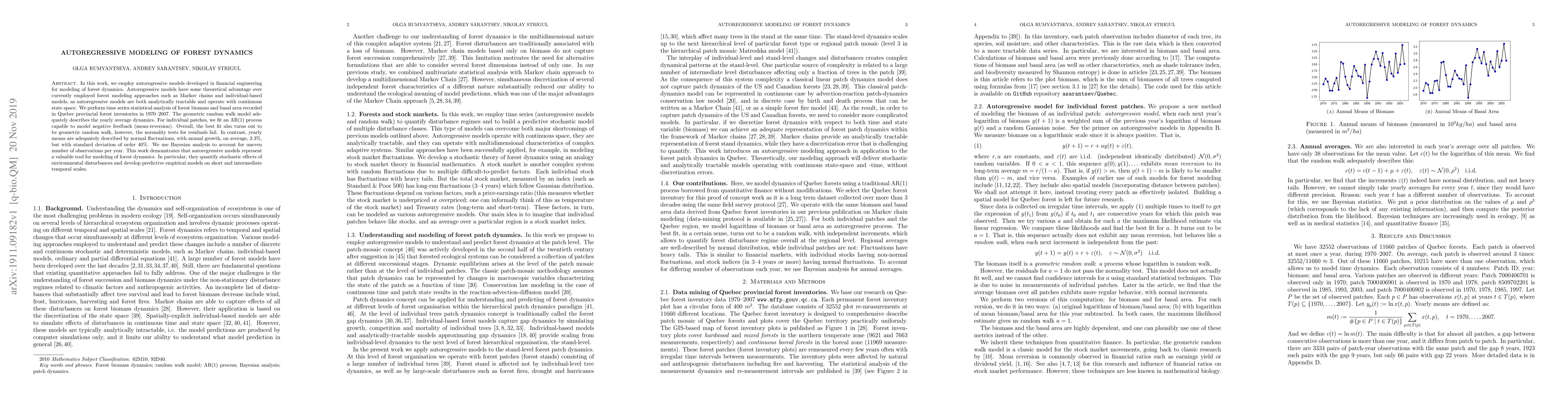

In this work, we employ autoregressive models developed in financial engineering for modeling of forest dynamics. Autoregressive models have some theoretical advantage over currently employed forest...

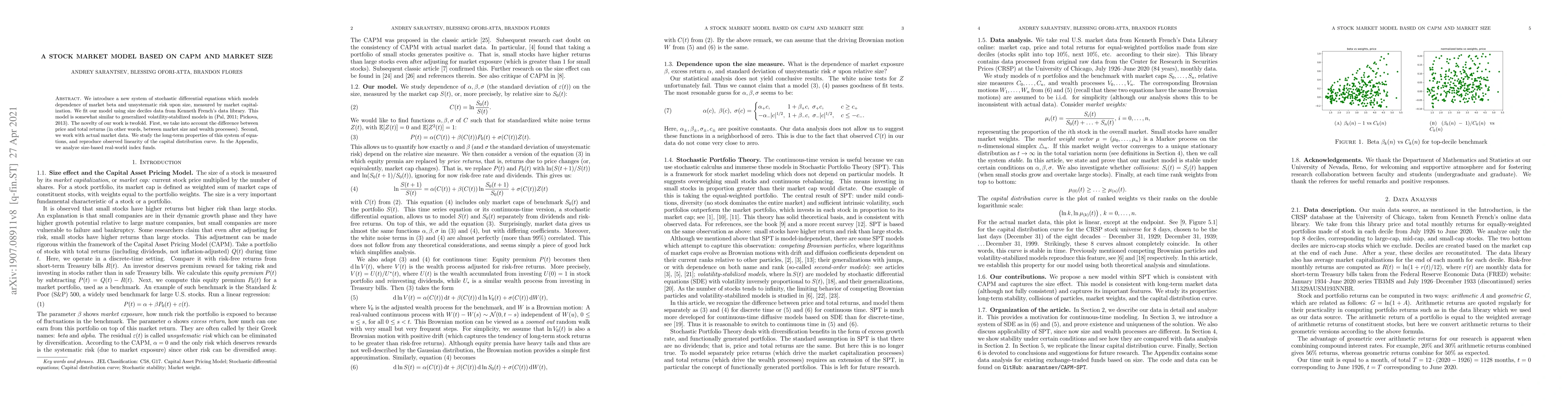

We introduce a new system of stochastic differential equations which models dependence of market beta and unsystematic risk upon size, measured by market capitalization. We fit our model using size ...

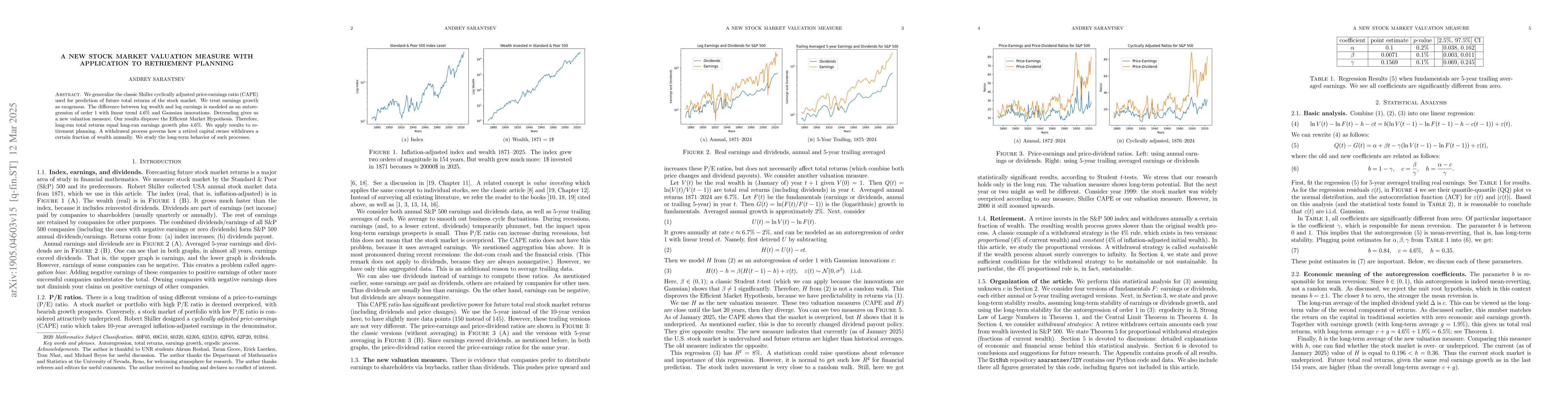

We generalize the classic Shiller cyclically adjusted price-earnings ratio (CAPE) used for prediction of future total returns of the stock market. We treat earnings growth as exogenous. The differen...

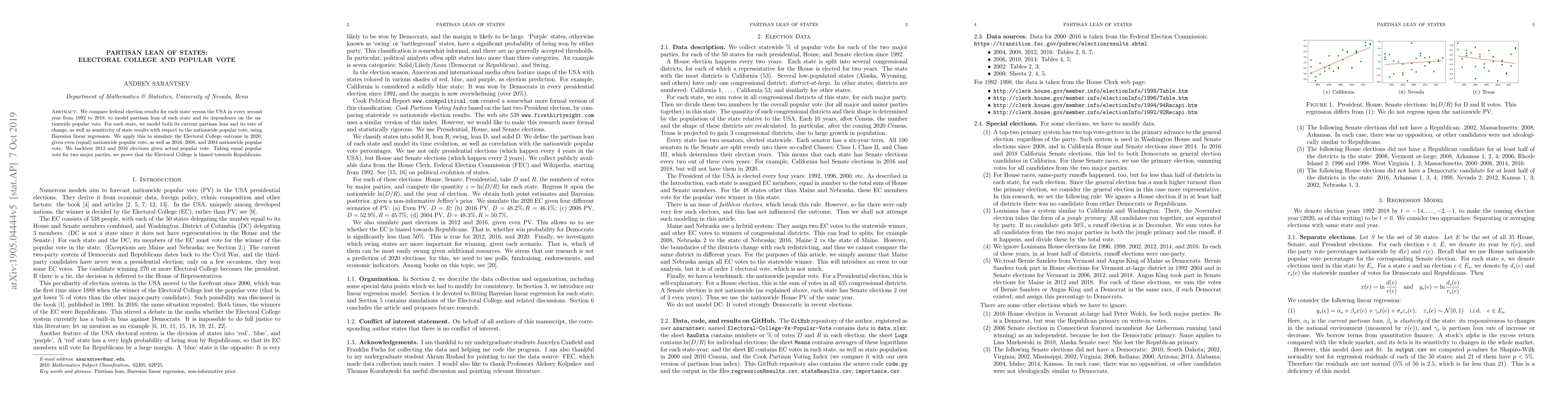

We compare federal election results for each state versus the USA in every second year from 1992 to 2018, to model partisan lean of each state and its dependence on the nationwide popular vote. For ...

We consider a dynamic model of interconnected banks. New banks can emerge, and existing banks can default, creating a birth-and-death setup. Microscopically, banks evolve as independent geometric Br...

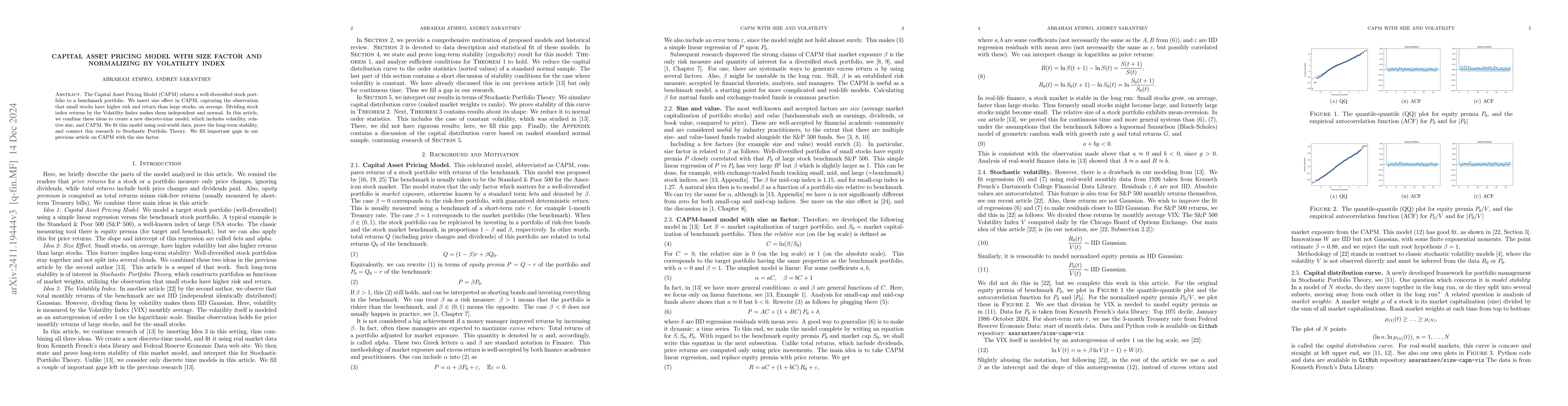

The Capital Asset Pricing Model (CAPM) relates a well-diversified stock portfolio to a benchmark portfolio. We insert size effect in CAPM, capturing the observation that small stocks have higher risk ...

Running Median Subtraction Filter (RMSF) is a robust statistical tool for removing slowly varying baselines in data streams containing transients (short-duration signals) of interest. In this work, we...

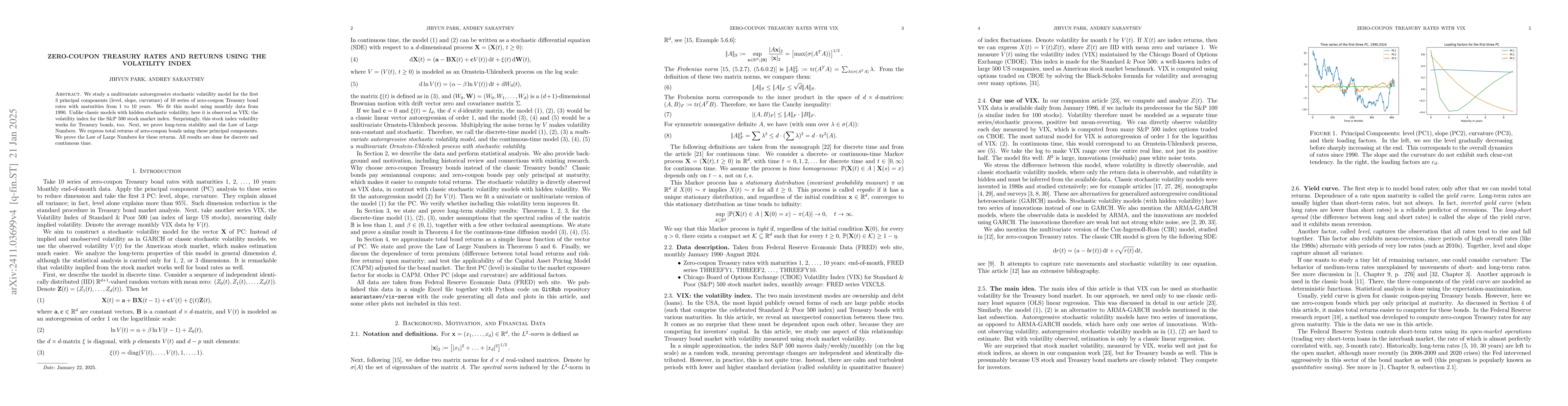

We study a multivariate autoregressive stochastic volatility model for the first 3 principal components (level, slope, curvature) of 10 series of zero-coupon Treasury bond rates with maturities from 1...

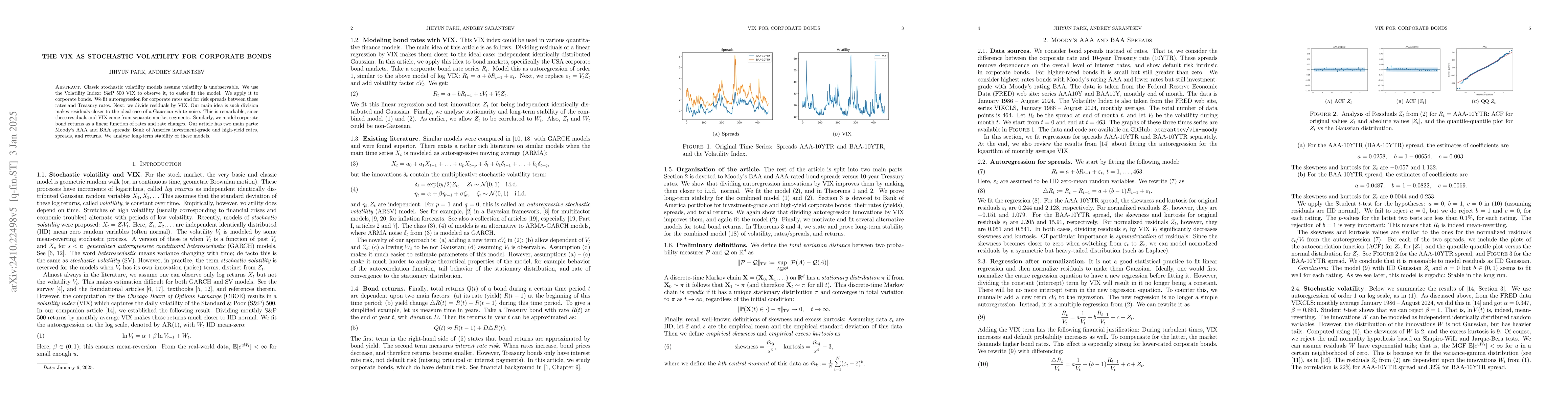

Classic stochastic volatility models assume volatility is unobservable. We use the Volatility Index: S\&P 500 VIX to observe it, to easier fit the model. We apply it to corporate bonds. We fit autoreg...

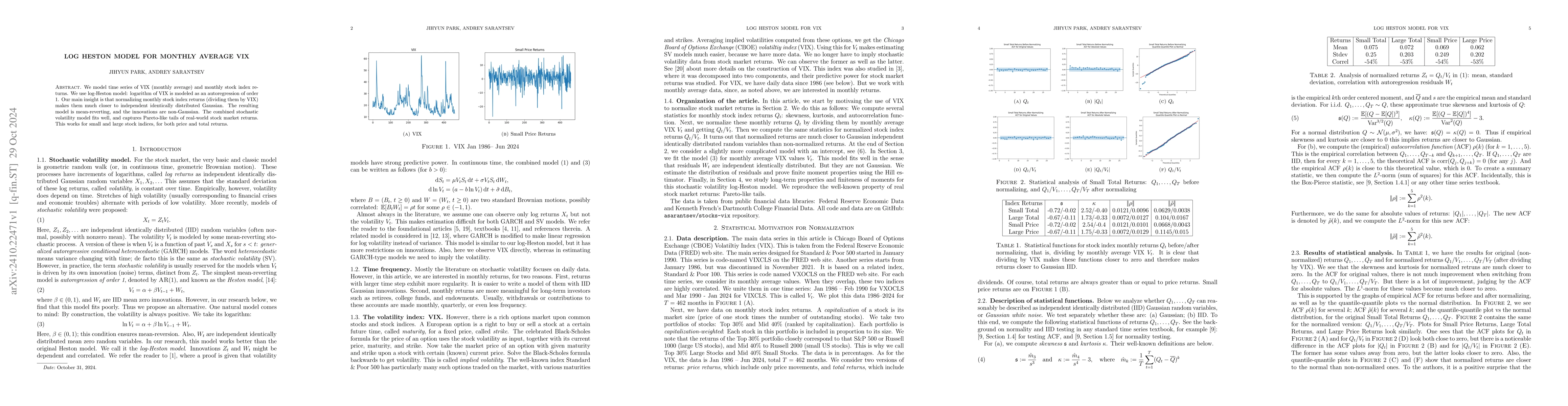

We model time series of VIX (monthly average) and monthly stock index returns. We use log-Heston model: logarithm of VIX is modeled as an autoregression of order 1. Our main insight is that normalizin...

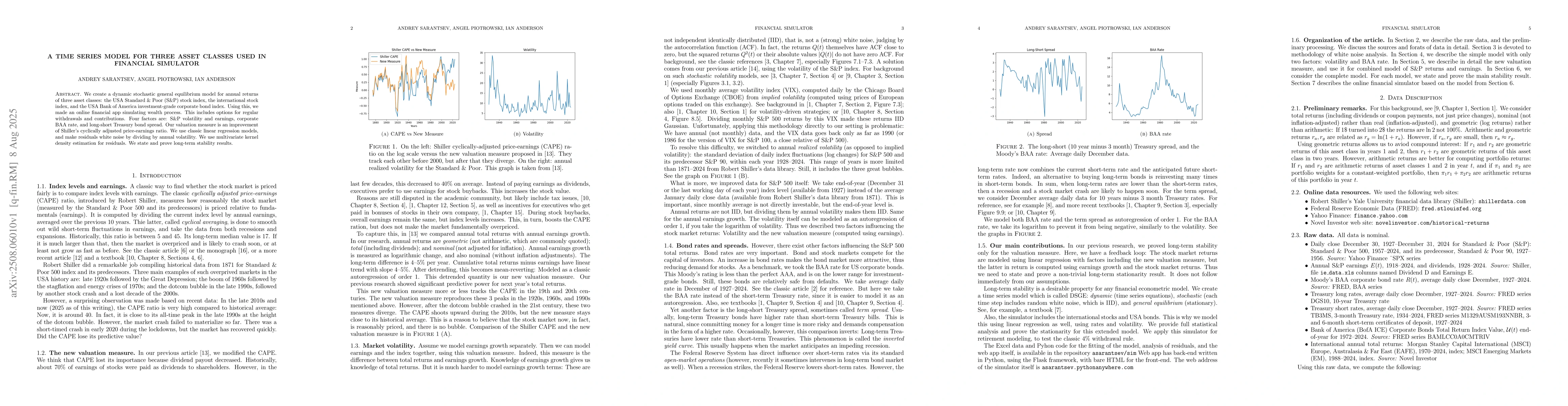

We create a dynamic stochastic general equilibrium model for annual returns of three asset classes: the USA Standard & Poor (S&P) stock index, the international stock index, and the USA Bank of Americ...

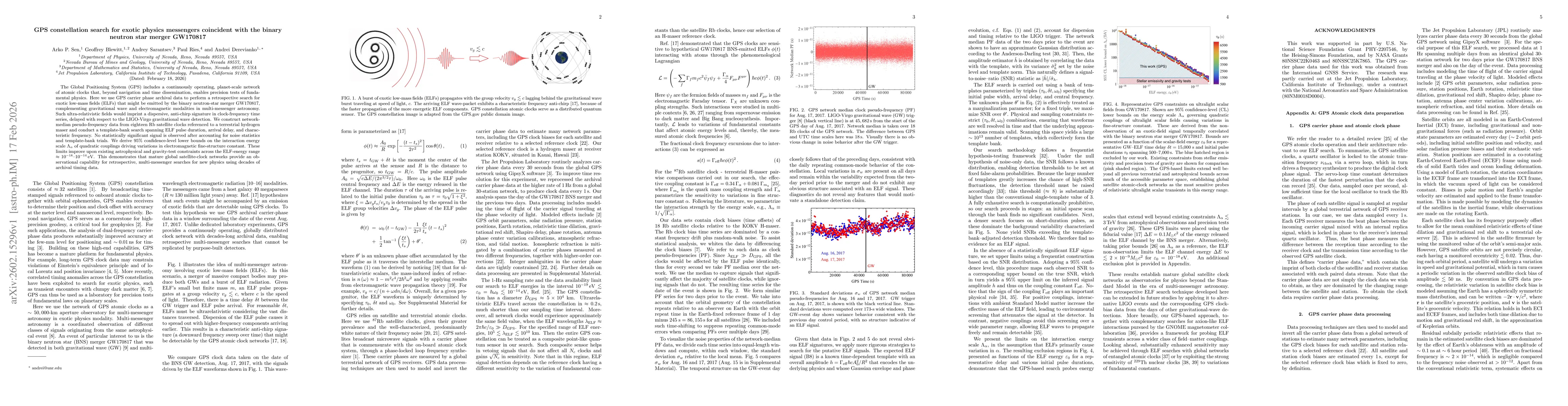

The Global Positioning System (GPS) includes a continuously operating, planet-scale network of atomic clocks that, beyond navigation and time dissemination, enables precision tests of fundamental phys...

For a random variable $N = 0, 1, 2, \ldots$ we study the following question: When does the sum of $N$ many independent and identically distributed copies of a random variable $X$ have the same law a a...

We consider a generalization of the variance-gamma (generalized asymmetric Laplace) distribution, defined as a normal mean - variance mixture with a gamma mixing distribution. While this model is typi...

We present a one-parameter family of bivariate absolutely continuous distributions based on location-scale family of variance Gaussian mixtures, with continuous densities with the same support (effect...