Academic Profile

Statistics

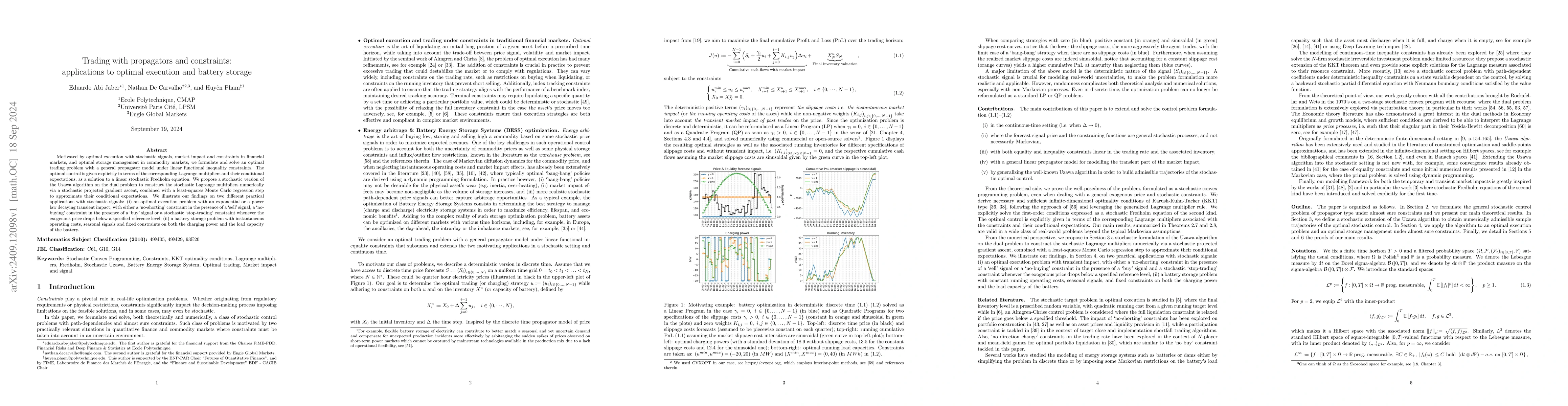

Similar Authors

Papers on arXiv

We consider the Fourier-Laplace transforms of a broad class of polynomial Ornstein-Uhlenbeck (OU) volatility models, including the well-known Stein-Stein, Sch\"obel-Zhu, one-factor Bergomi, and the ...

We study the class of continuous polynomial Volterra processes, which we define as solutions to stochastic Volterra equations driven by a continuous semimartingale with affine drift and quadratic di...

We consider a class of optimal portfolio choice problems in continuous time where the agent's transactions create both transient cross-impact driven by a matrix-valued Volterra propagator, as well a...

We consider a stochastic volatility model where the dynamics of the volatility are given by a possibly infinite linear combination of the elements of the time extended signature of a Brownian motion...

An extensive empirical study of the class of Volterra Bergomi models using SPX options data between 2011 and 2022 reveals the following fact-check on two fundamental claims echoed in the rough volat...

We consider a general class of finite-player stochastic games with mean-field interaction, in which the linear-quadratic cost functional includes linear operators acting on controls in $L^2$. We pro...

We reconcile rough volatility models and jump models using a class of reversionary Heston models with fast mean reversions and large vol-of-vols. Starting from hyper-rough Heston models with a Hurst...

The quintic Ornstein-Uhlenbeck volatility model is a stochastic volatility model where the volatility process is a polynomial function of degree five of a single Ornstein-Uhlenbeck process with fast...

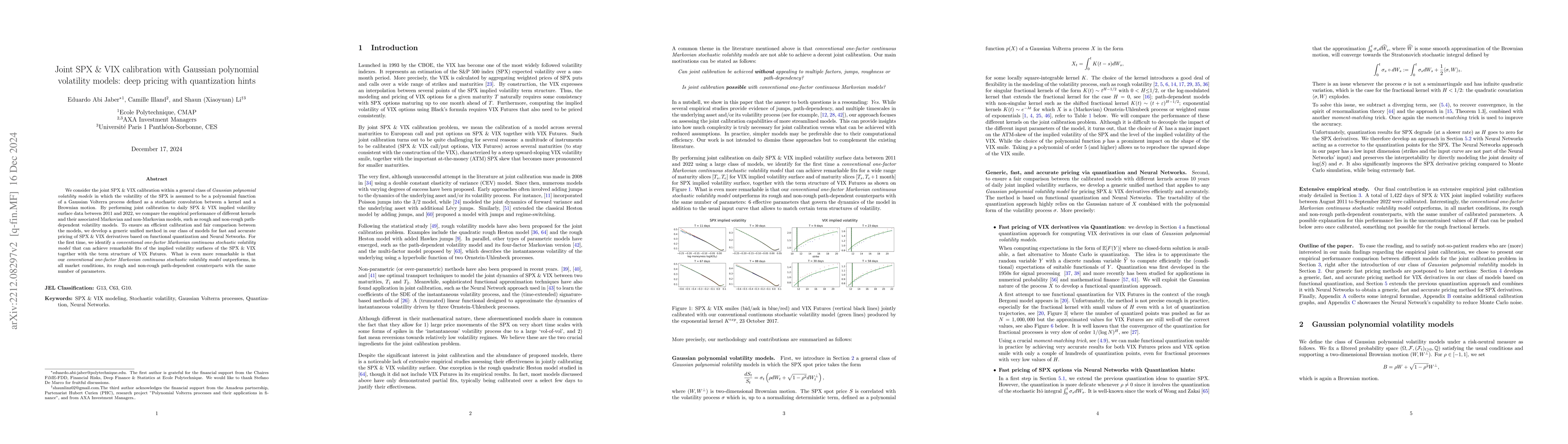

We consider the joint SPX-VIX calibration within a general class of Gaussian polynomial volatility models in which the volatility of the SPX is assumed to be a polynomial function of a Gaussian Volt...

We consider a class of optimal liquidation problems where the agent's transactions create transient price impact driven by a Volterra-type propagator along with temporary price impact. We formulate ...

Can a principal still offer optimal dynamic contracts that are linear in end-of-period outcomes when the agent controls a process that exhibits memory? We provide a positive answer by considering a ...

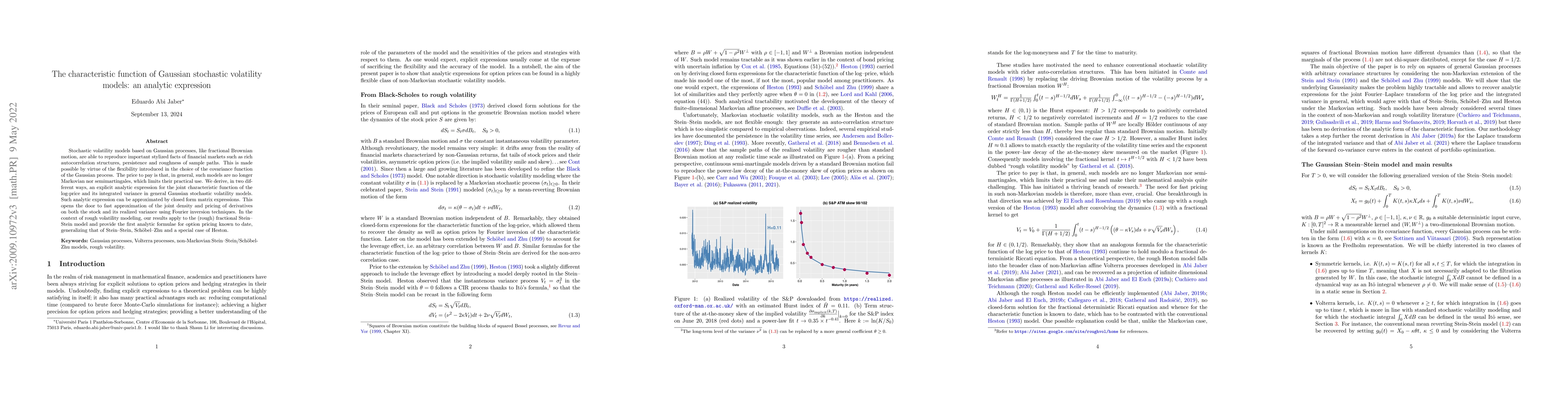

Stochastic volatility models based on Gaussian processes, like fractional Brownian motion, are able to reproduce important stylized facts of financial markets such as rich autocorrelation structures...

We establish an explicit expression for the conditional Laplace transform of the integrated Volterra Wishart process in terms of a certain resolvent of the covariance function. The core ingredient i...

We establish existence and uniqueness for infinite dimensional Riccati equations taking values in the Banach space L 1 ($\mu$ $\otimes$ $\mu$) for certain signed matrix measures $\mu$ which are not ...

We obtain general weak existence and stability results for stochastic convolution equations with jumps under mild regularity assumptions, allowing for non-Lipschitz coefficients and singular kernels...

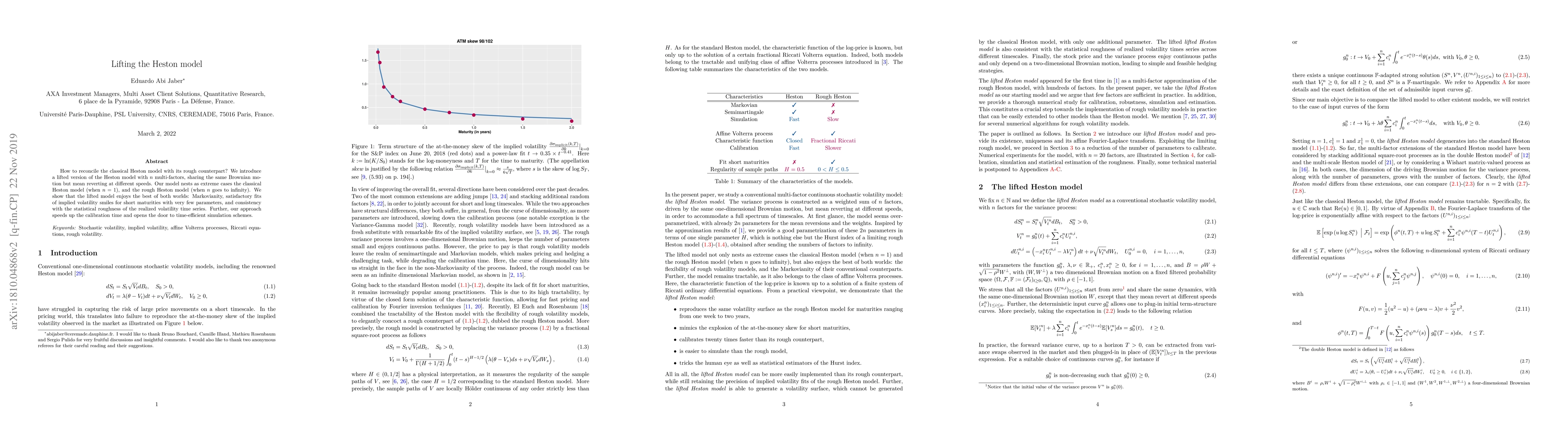

How to reconcile the classical Heston model with its rough counterpart? We introduce a lifted version of the Heston model with n multi-factors, sharing the same Brownian motion but mean reverting at...

We introduce affine Volterra processes, defined as solutions of certain stochastic convolution equations with affine coefficients. Classical affine diffusions constitute a special case, but affine V...

Motivated by optimal execution with stochastic signals, market impact and constraints in financial markets, and optimal storage management in commodity markets, we formulate and solve an optimal tradi...

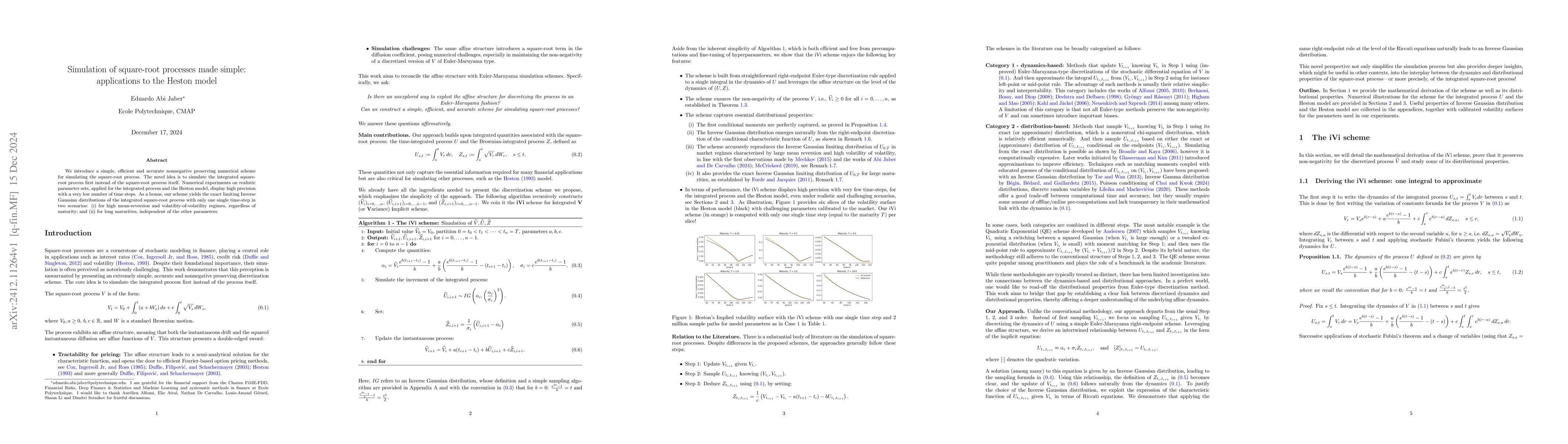

We introduce a simple, efficient and accurate nonnegative preserving numerical scheme for simulating the square-root process. The novel idea is to simulate the integrated square-root process first ins...

We show that the state spaces of multifactor Markovian processes, coming from approximations of nonnegative Volterra processes, are given by explicit linear transformation of the nonnegative orthant. ...

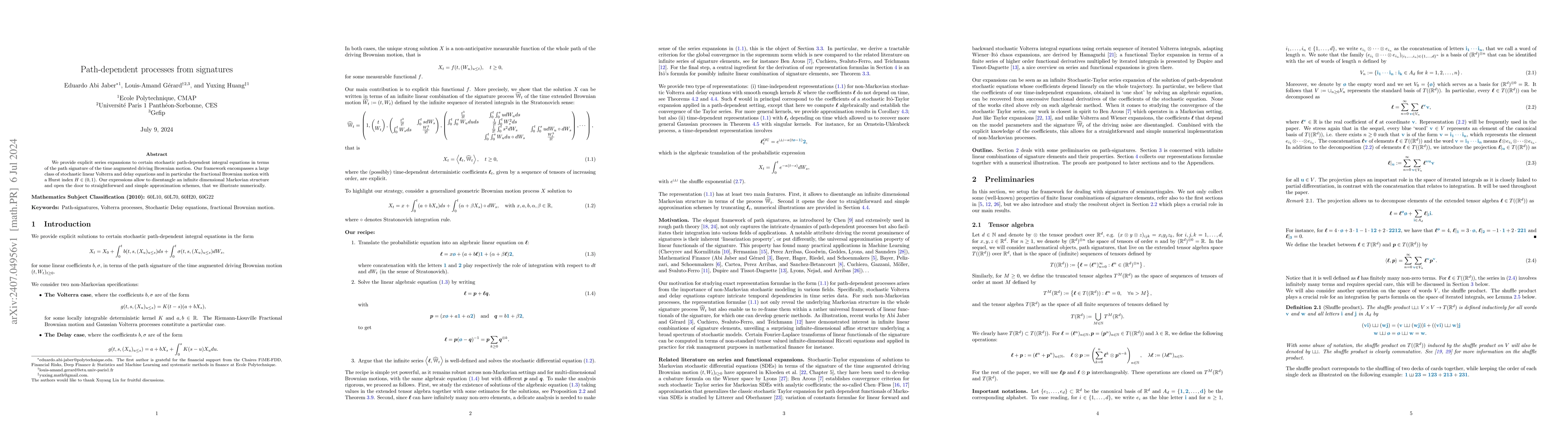

We provide explicit series expansions to certain stochastic path-dependent integral equations in terms of the path signature of the time augmented driving Brownian motion. Our framework encompasses a ...

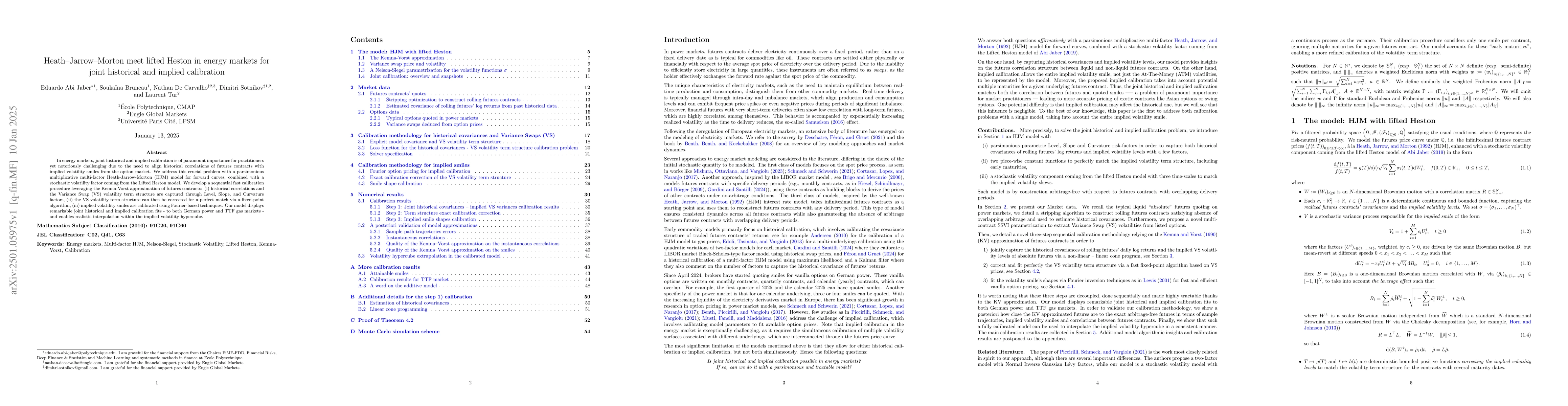

In energy markets, joint historical and implied calibration is of paramount importance for practitioners yet notoriously challenging due to the need to align historical correlations of futures contrac...

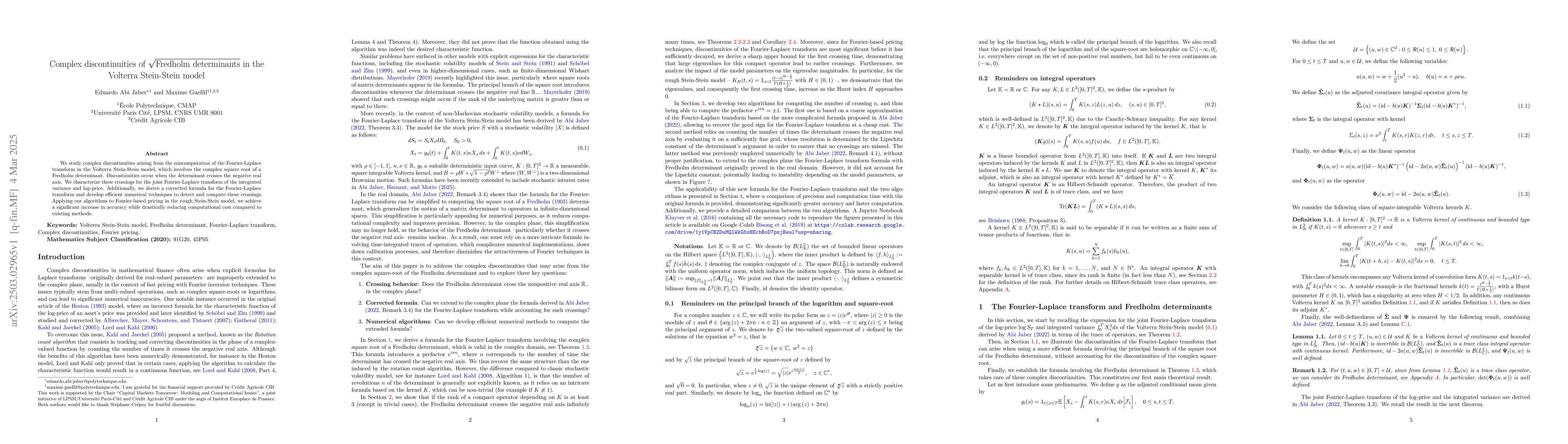

We study complex discontinuities arising from the miscomputation of the Fourier-Laplace transform in the Volterra Stein-Stein model, which involves the complex square root of a Fredholm determinant. D...

We formulate and solve an optimal trading problem with alpha signals, where transactions induce a nonlinear transient price impact described by a general propagator model, including power-law decay. U...

We introduce the Volterra Stein-Stein model with stochastic interest rates, where both volatility and interest rates are driven by correlated Gaussian Volterra processes. This framework unifies variou...

We study the martingale property and moment explosions of a signature volatility model, where the volatility process of the log-price is given by a linear form of the signature of a time-extended Brow...

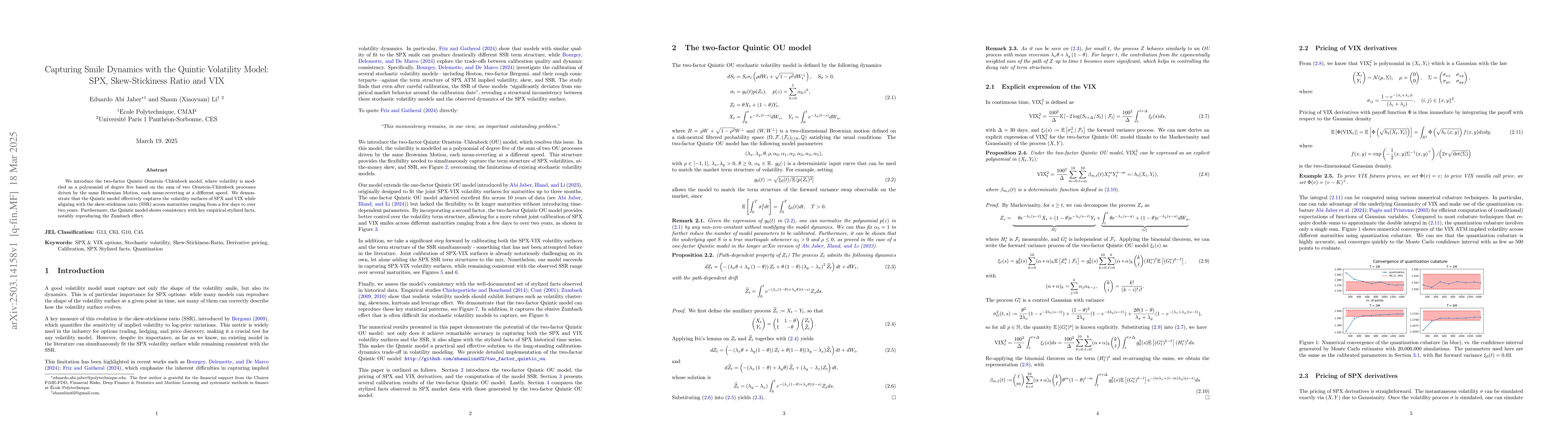

We introduce the two-factor Quintic Ornstein-Uhlenbeck model, where volatility is modeled as a polynomial of degree five based on the sum of two Ornstein-Uhlenbeck processes driven by the same Brownia...

We investigate the weak limit of the hyper-rough square-root process as the Hurst index $H$ goes to $-1/2\,$. This limit corresponds to the fractional kernel $t^{H - 1 / 2}$ losing integrability. We e...

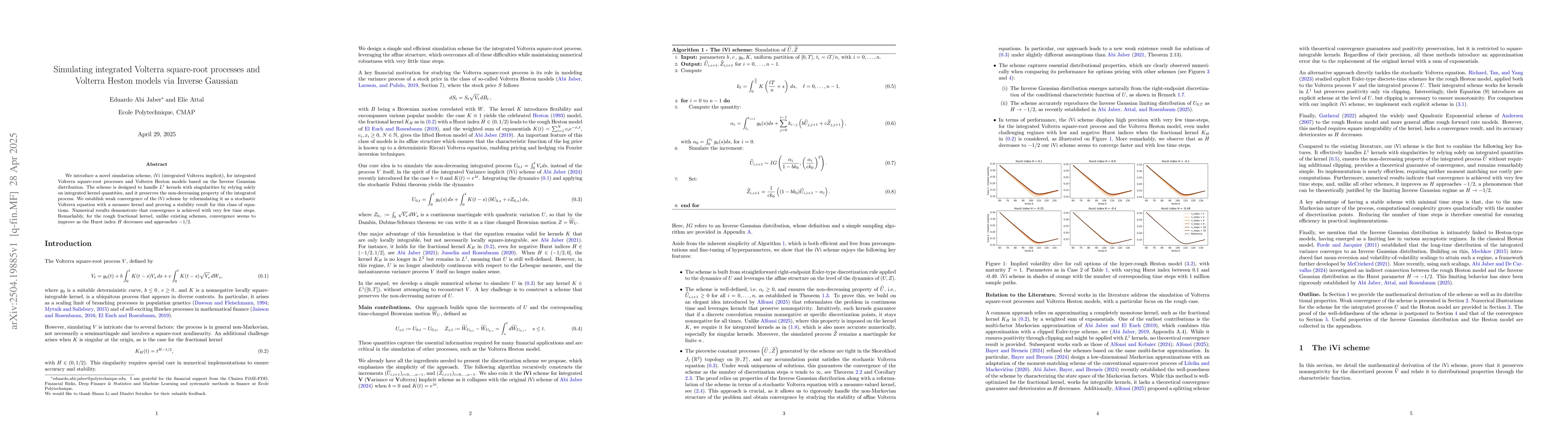

We introduce a novel simulation scheme, iVi (integrated Volterra implicit), for integrated Volterra square-root processes and Volterra Heston models based on the Inverse Gaussian distribution. The sch...

We establish new weak existence results for $d$-dimensional Stochastic Volterra Equations (SVEs) with continuous coefficients and possibly singular one-dimensional non-convolution kernels. These resul...

We introduce the exponentially fading memory (EFM) signature, a time-invariant transformation of an infinite (possibly rough) path that serves as a mean-reverting analogue of the classical path signat...

We investigate the use of path signatures in a machine learning context for hedging exotic derivatives under non-Markovian stochastic volatility models. In a deep learning setting, we use signatures a...

We introduce a novel signature approach for pricing and hedging path-dependent options with instantaneous and permanent market impact under a mean-quadratic variation criterion. Leveraging the express...

We introduce a novel and efficient simulation scheme for Hawkes processes on a fixed time grid, leveraging their affine Volterra structure. The key idea is to first simulate the integrated intensity a...

We establish necessary and sufficient conditions for stochastic invariance of closed subsets in Hilbert spaces for solutions to infinite-dimensional stochastic differential equations (SDEs) under mild...

Malliavin calculus is a powerful and general framework for the analysis of square-integrable random variables, but it often suffers from a lack of tractability and explicit representations. To address...

We introduce a class of continuous Volterra processes, called Volterra clocks, and study their singular limit as the memory kernel collapses to a Dirac mass at zero. The dynamics are parametrised by a...

We establish an infinite-dimensional affine transform theory for the time-augmented Brownian signature. Our first main result shows that, for a suitable class of linear functions of the signature, the...

We solve in semi-explicit form a class of non-Markovian stochastic optimal control problems with path-dependent rewards, using path signatures. We reformulate the control problem as the computation of...