Academic Profile

Statistics

Similar Authors

Papers on arXiv

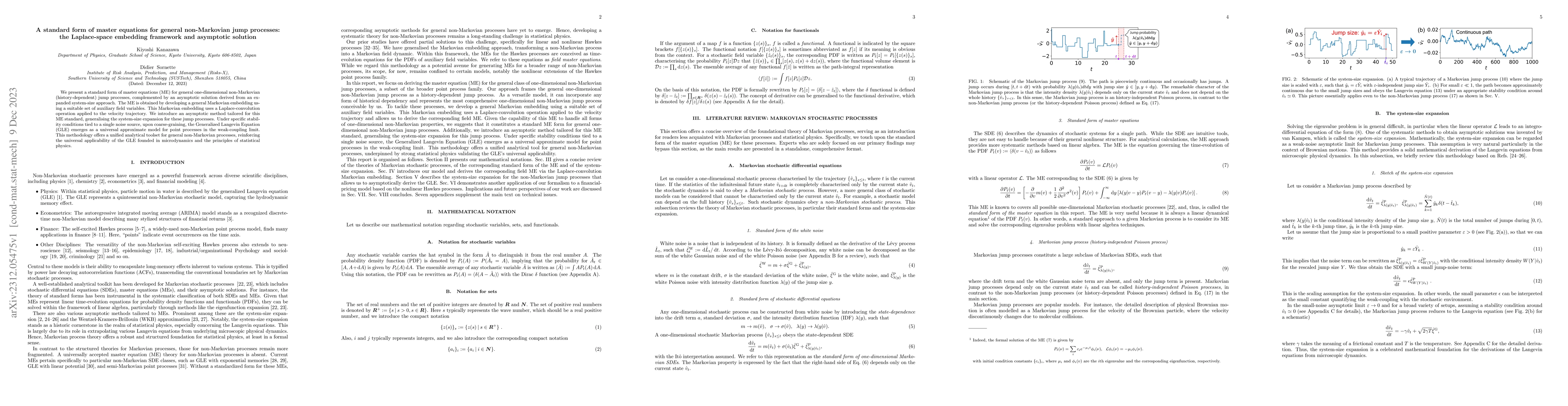

We present a standard form of master equations (ME) for general one-dimensional non-Markovian (history-dependent) jump processes, complemented by an asymptotic solution derived from an expanded syst...

In this research, we focus on the order-splitting behavior. The order splitting is a trading strategy to execute their large potential metaorder into small pieces to reduce transaction cost. This st...

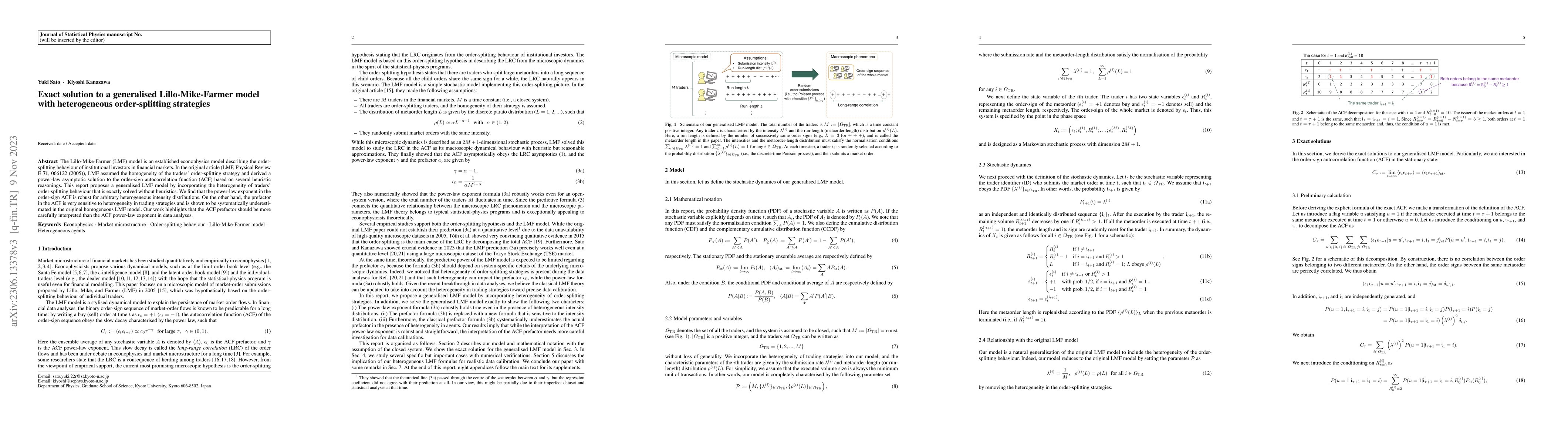

The Lillo-Mike-Farmer (LMF) model is an established econophysics model describing the order-splitting behaviour of institutional investors in financial markets. In the original article (LMF, Physica...

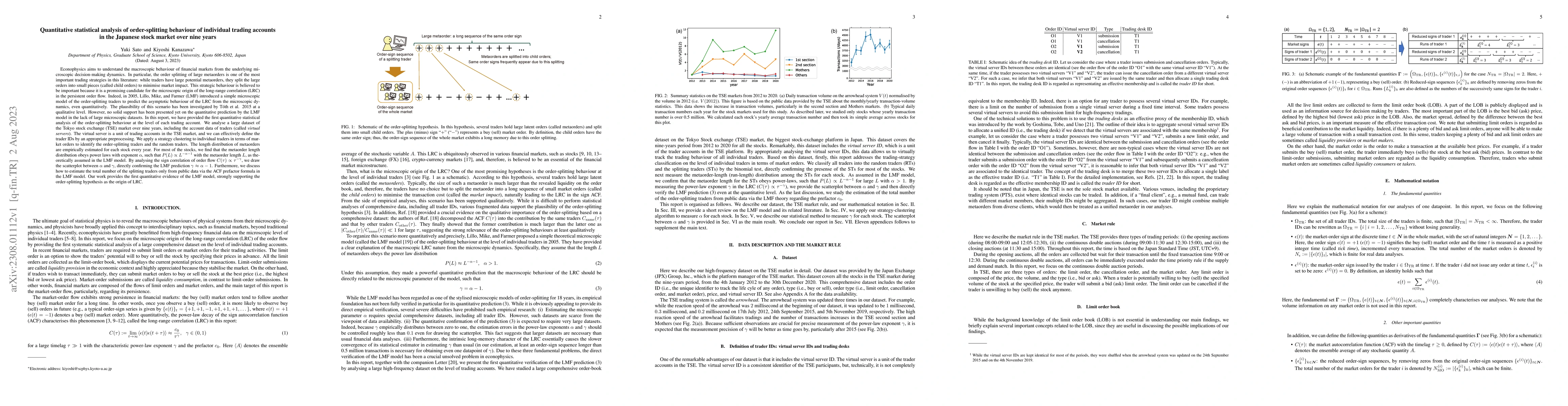

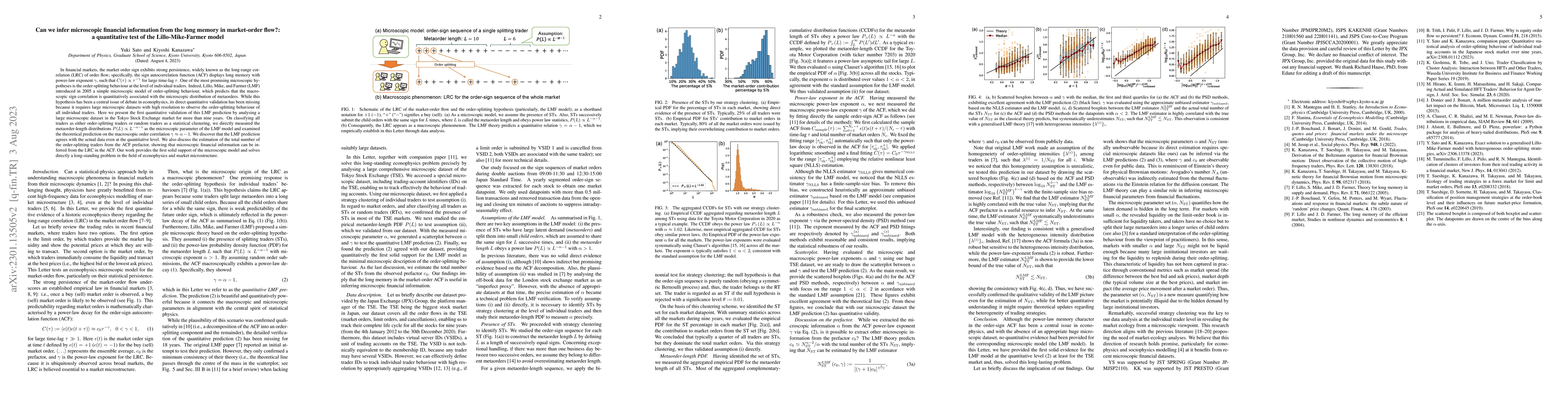

In financial markets, the market order sign exhibits strong persistence, widely known as the long-range correlation (LRC) of order flow; specifically, the sign correlation function displays long mem...

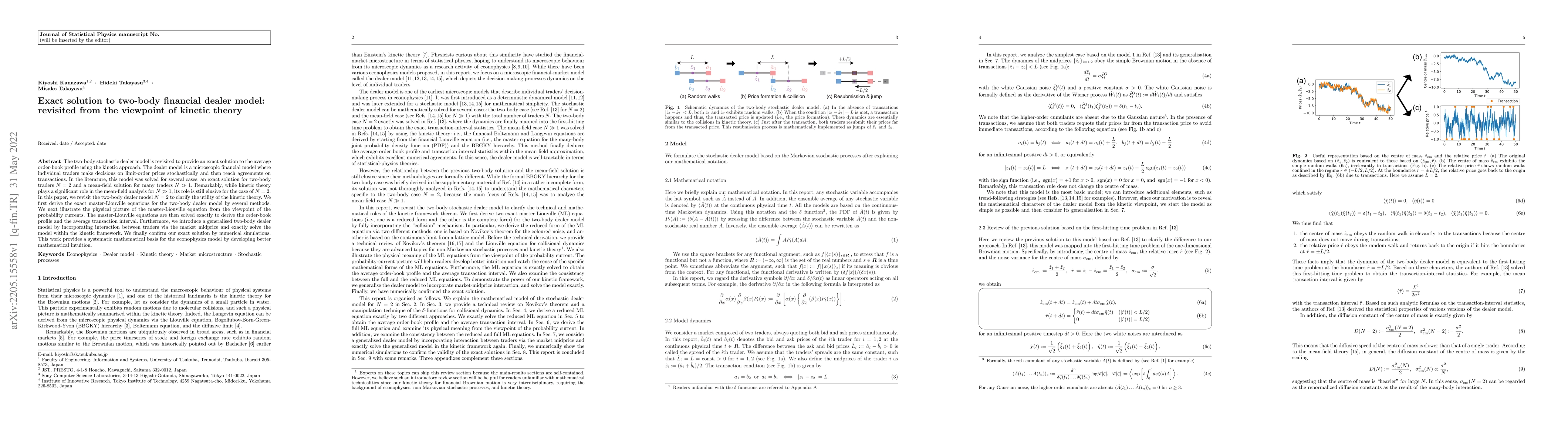

The two-body stochastic dealer model is revisited to provide an exact solution to the average order-book profile using the kinetic approach. The dealer model is a microscopic financial model where i...

Recent decades have seen a rise in the use of physics methods to study different societal phenomena. This development has been due to physicists venturing outside of their traditional domains of int...

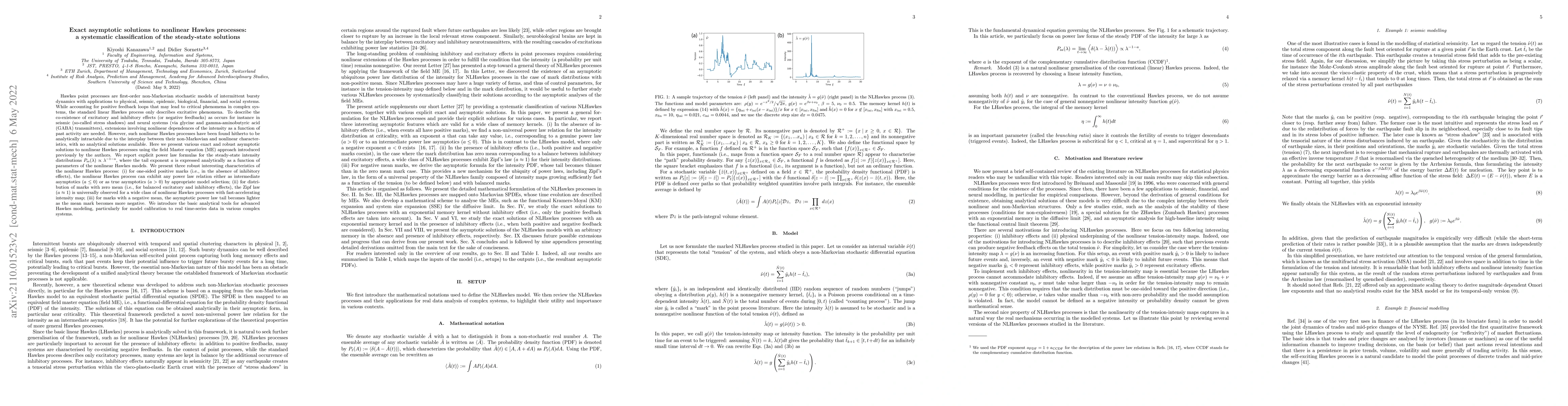

Hawkes point processes are first-order non-Markovian stochastic models of intermittent bursty dynamics with applications to physical, seismic, epidemic, biological, financial, and social systems. Wh...

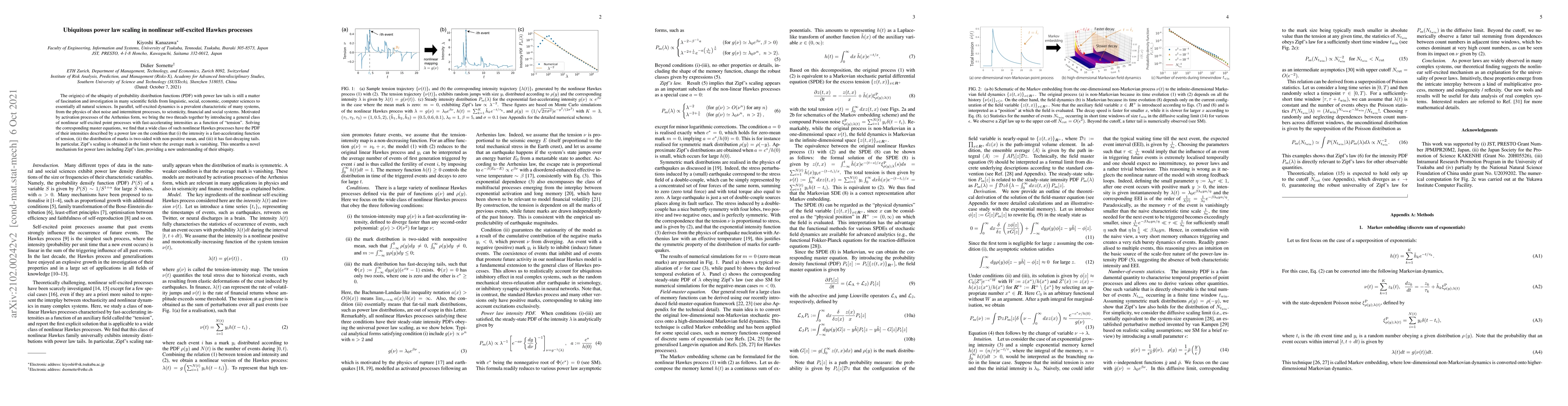

The origin(s) of the ubiquity of probability distribution functions (PDF) with power law tails is still a matter of fascination and investigation in many scientific fields from linguistic, social, e...

A field theoretical framework is developed for the Hawkes self-excited point process with arbitrary memory kernels by embedding the original non-Markovian one-dimensional dynamics onto a Markovian i...

Brownian motion is widely used as a paradigmatic model of diffusion in equilibrium media throughout the physical, chemical, and biological sciences. However, many real world systems, particularly bi...

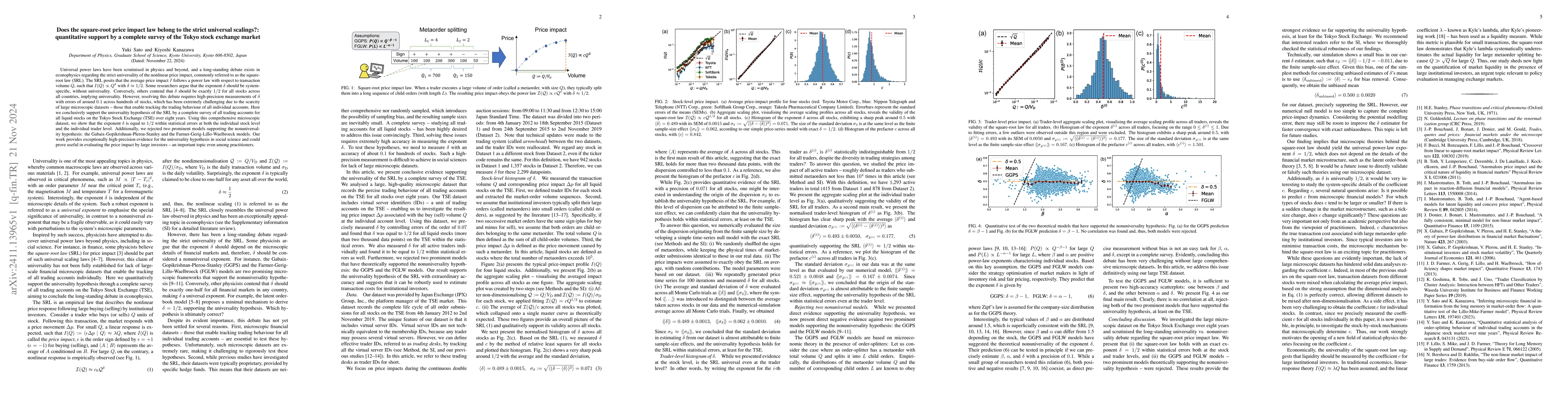

Universal power laws have been scrutinised in physics and beyond, and a long-standing debate exists in econophysics regarding the strict universality of the nonlinear price impact, commonly referred t...

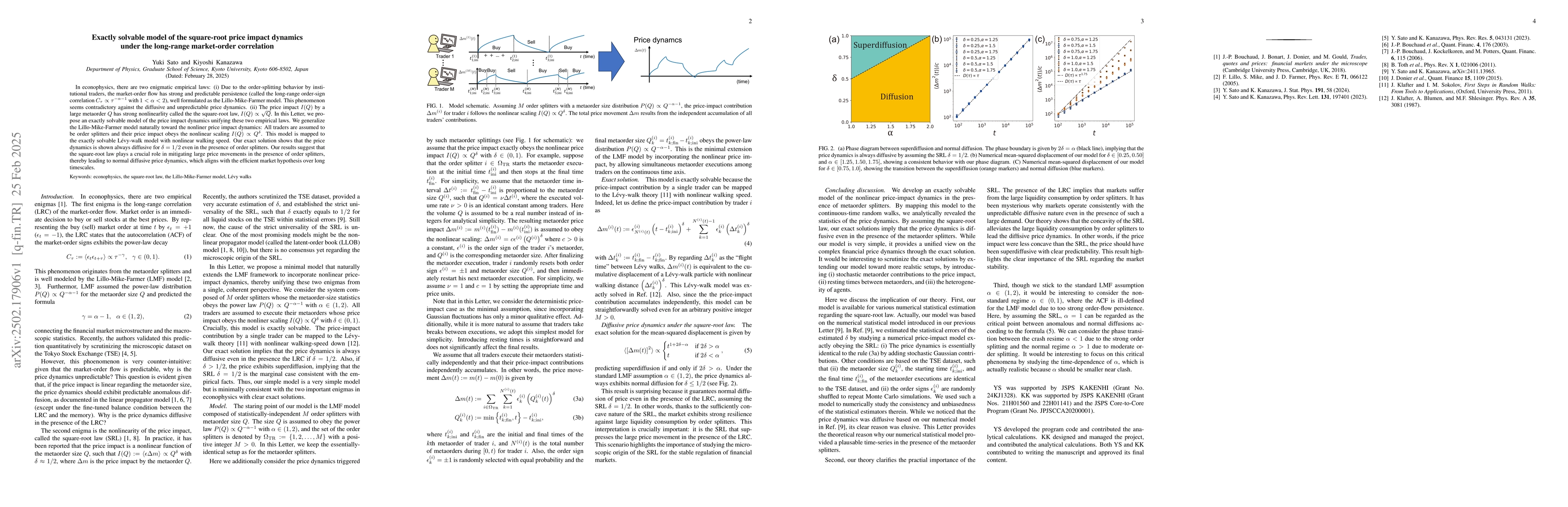

In econophysics, there are two enigmatic empirical laws: (i) Due to the order-splitting behavior by institutional traders, the market-order flow has strong and predictable persistence (called the long...

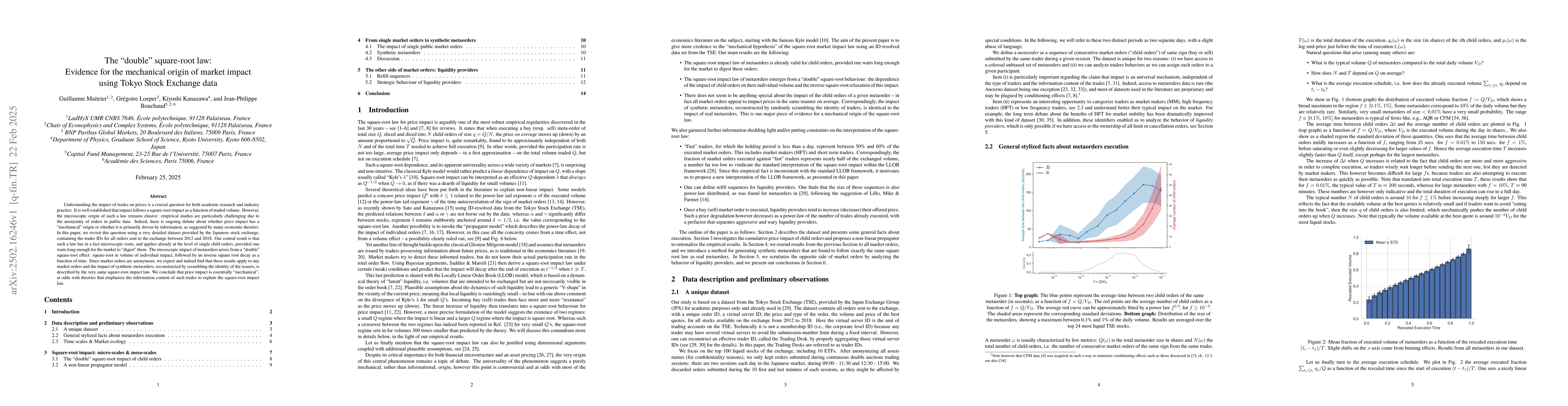

Understanding the impact of trades on prices is a crucial question for both academic research and industry practice. It is well established that impact follows a square-root impact as a function of tr...

Stochastic thermodynamics investigates energetic/entropic bounds in small systems, such as biomolecular motors, chemical-reaction networks, and quantum nano-devices. Foundational results, including th...

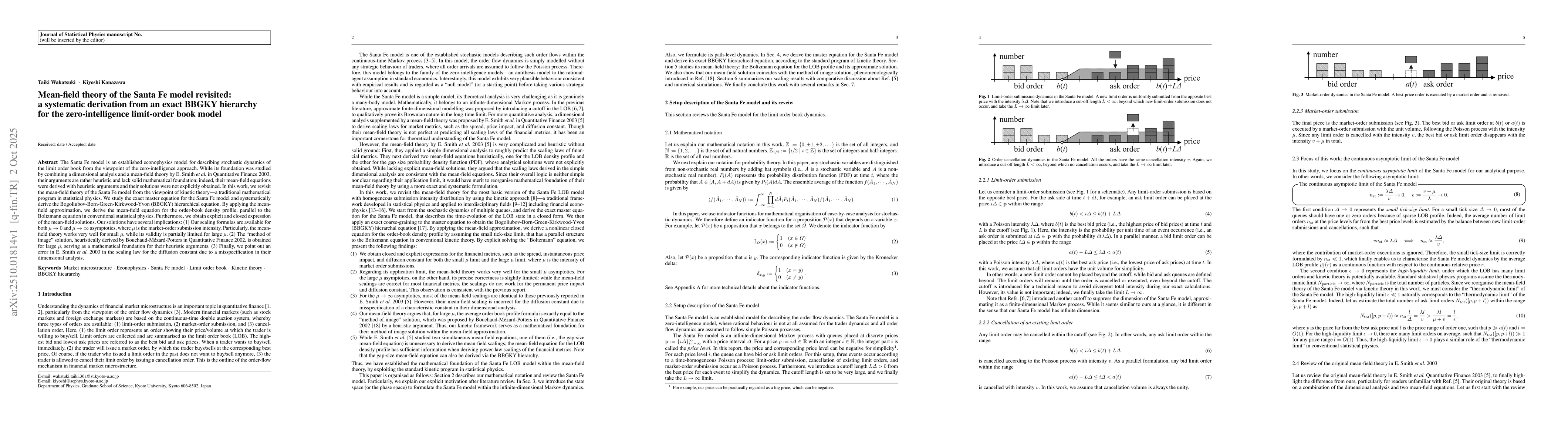

The Santa Fe model is an established econophysics model for describing stochastic dynamics of the limit order book from the viewpoint of the zero-intelligence approach. While its foundation was studie...

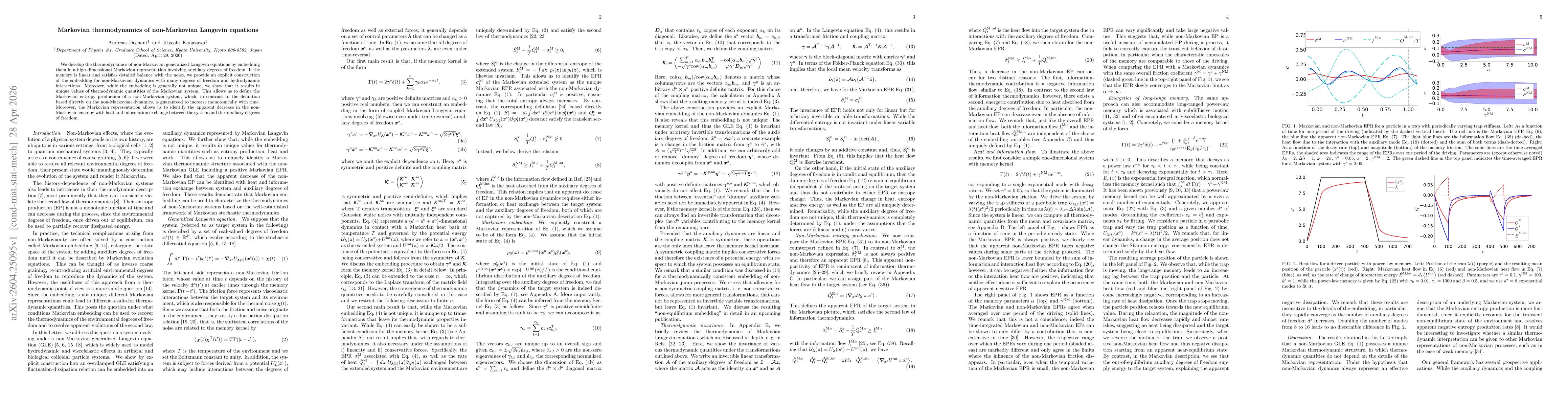

We develop the thermodynamics of non-Markovian generalized Langevin equations by embedding them in a high-dimensional Markovian representation involving auxiliary degrees of freedom. If the memory is ...