Academic Profile

Statistics

Similar Authors

Papers on arXiv

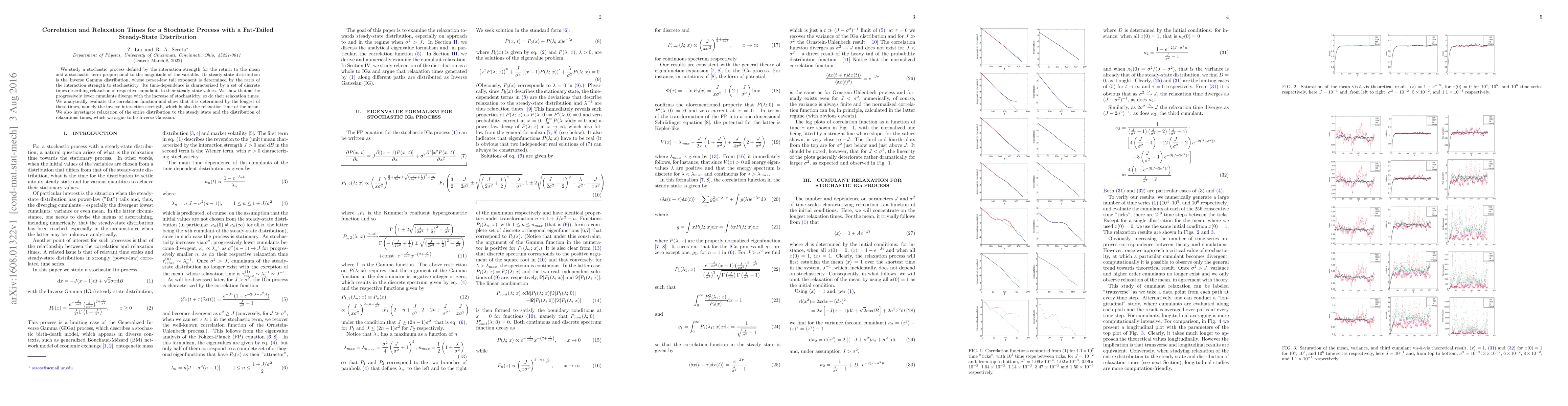

We study a stochastic process defined by the interaction strength for the return to the mean and a stochastic term proportional to the magnitude of the variable. Its steady-state distribution is the...

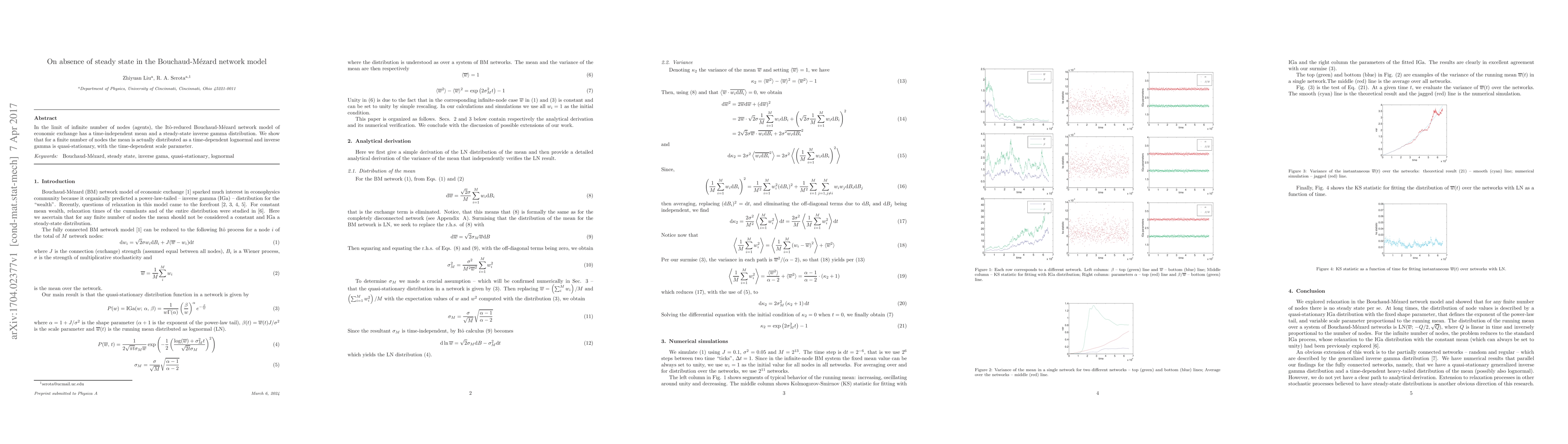

In the limit of infinite number of nodes (agents), the It\^o-reduced Bouchaud-M\'ezard network model of economic exchange has a time-independent mean and a steady-state inverse gamma distribution. W...

We use house prices (HP) and house price indices (HPI) as a proxy to income distribution. Specifically, we analyze sale prices in the 1970-2010 window of over 116,000 single-family homes in Hamilton...

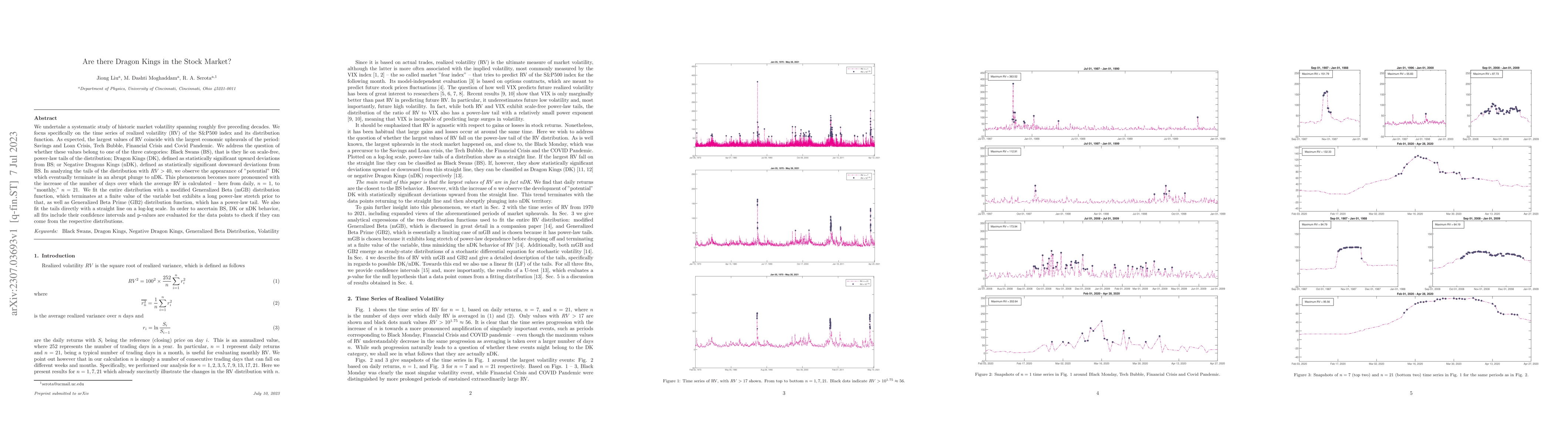

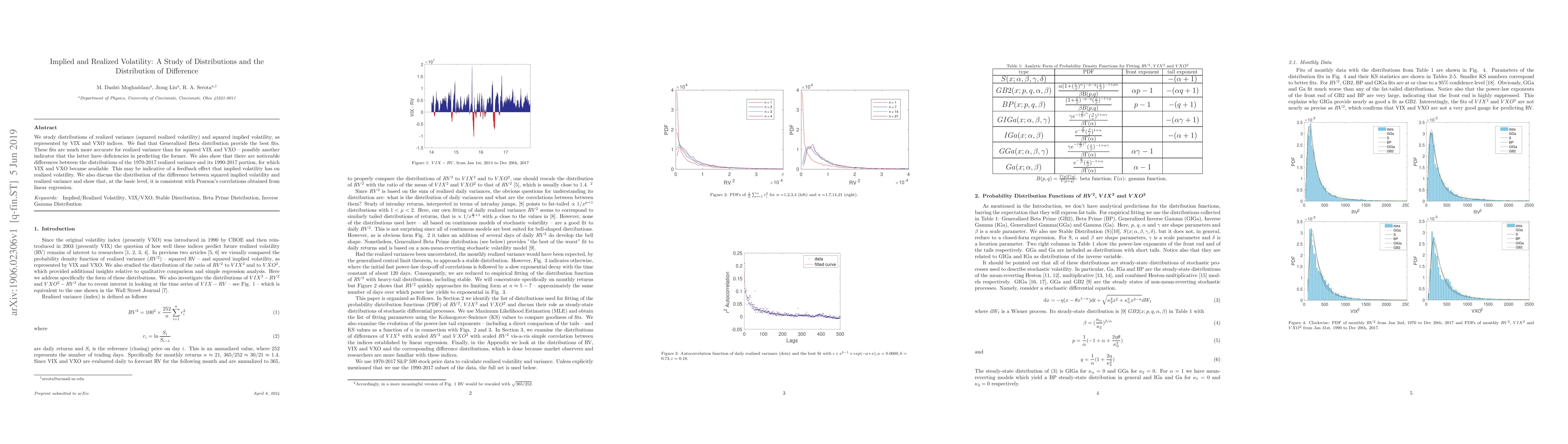

We undertake a systematic study of historic market volatility spanning roughly five preceding decades. We focus specifically on the time series of realized volatility (RV) of the S&P500 index and it...

We approach the Generalized Beta (GB) family of distributions using a mean-reverting stochastic differential equation (SDE) for a power of the variable, whose steady-state (stationary) probability d...

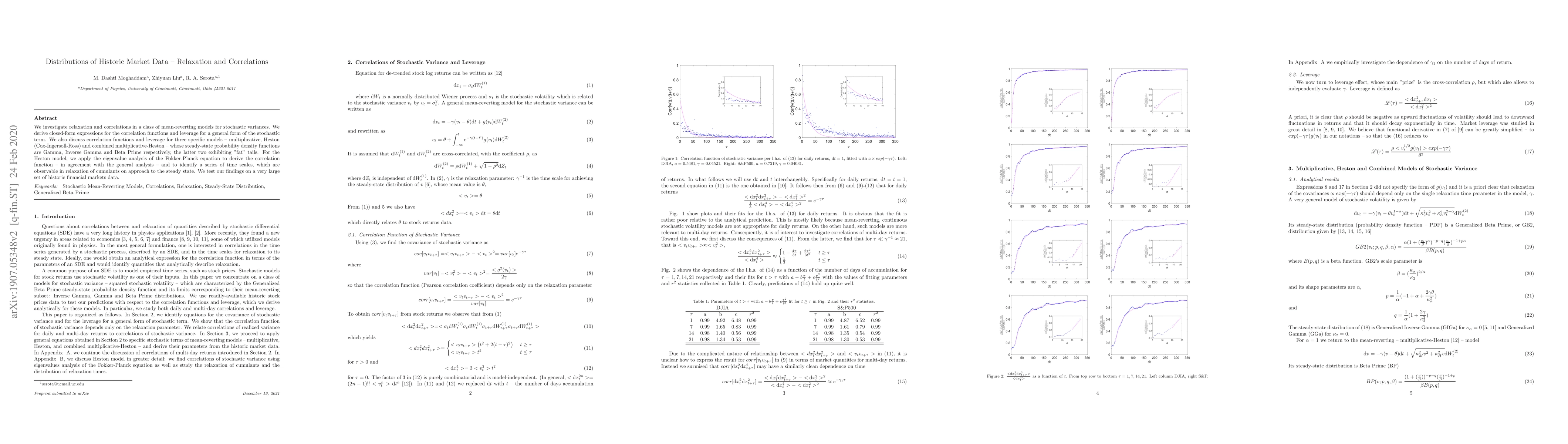

We investigate relaxation and correlations in a class of mean-reverting models for stochastic variances. We derive closed-form expressions for the correlation functions and leverage for a general fo...

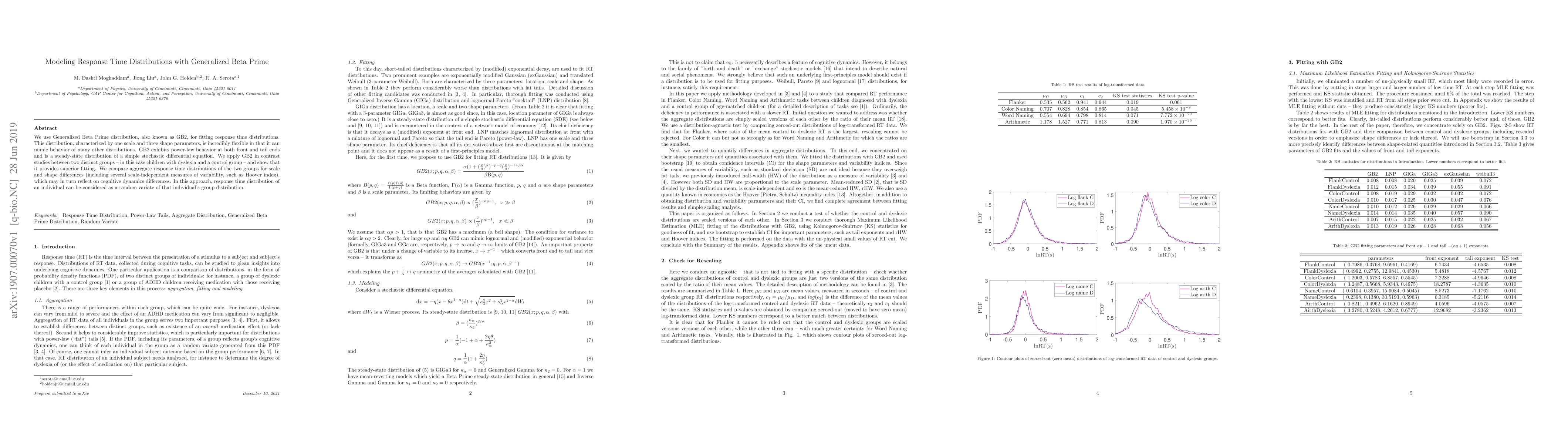

We use Generalized Beta Prime distribution, also known as GB2, for fitting response time distributions. This distribution, characterized by one scale and three shape parameters, is incredibly flexib...

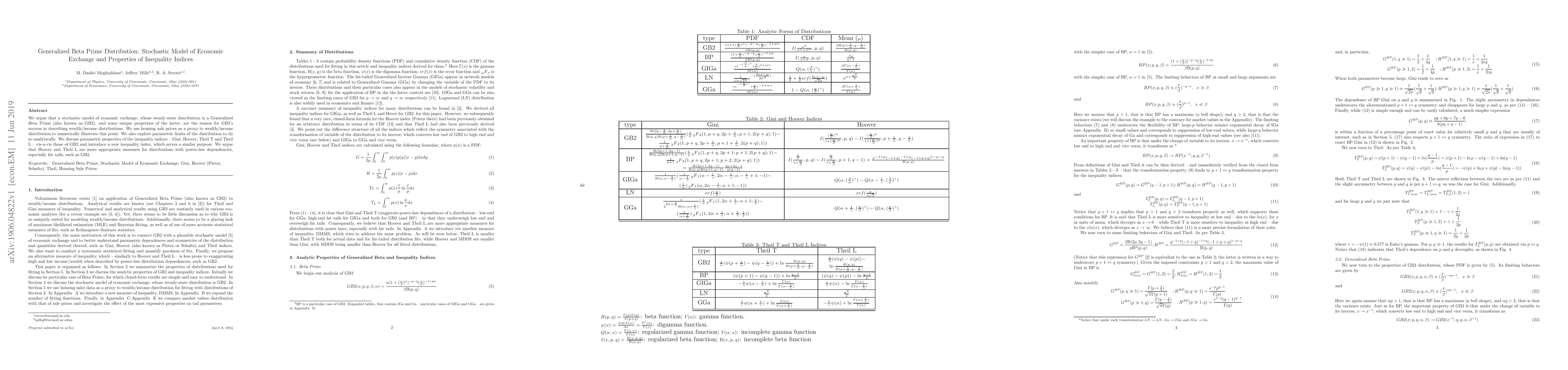

We argue that a stochastic model of economic exchange, whose steady-state distribution is a Generalized Beta Prime (also known as GB2), and some unique properties of the latter, are the reason for G...

We study distributions of realized variance (squared realized volatility) and squared implied volatility, as represented by VIX and VXO indices. We find that Generalized Beta distribution provide th...

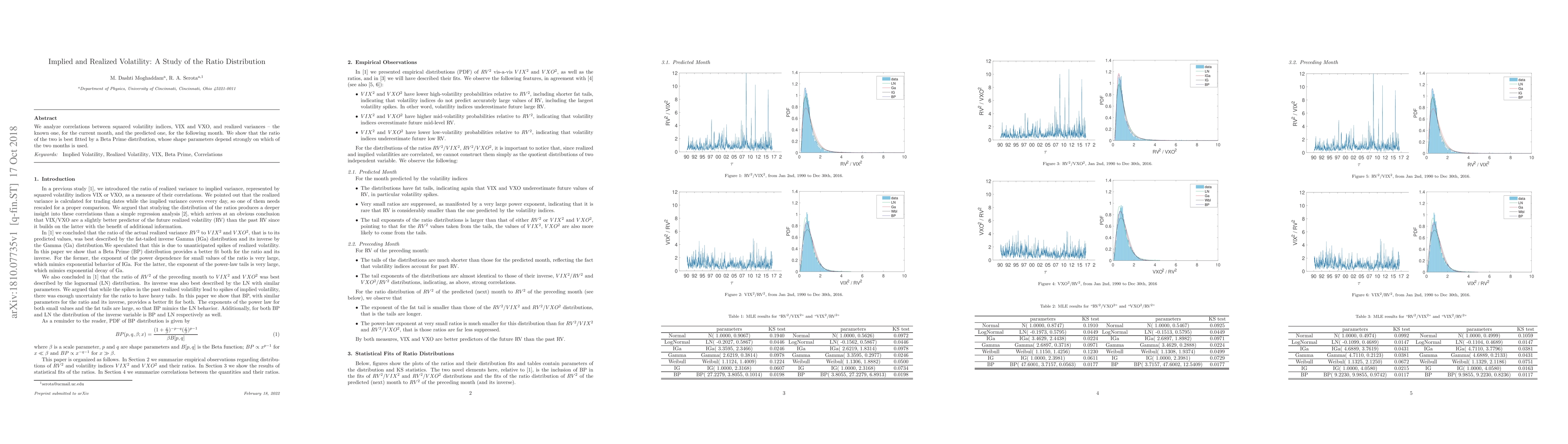

We analyze correlations between squared volatility indices, VIX and VXO, and realized variances -- the known one, for the current month, and the predicted one, for the following month. We show that ...

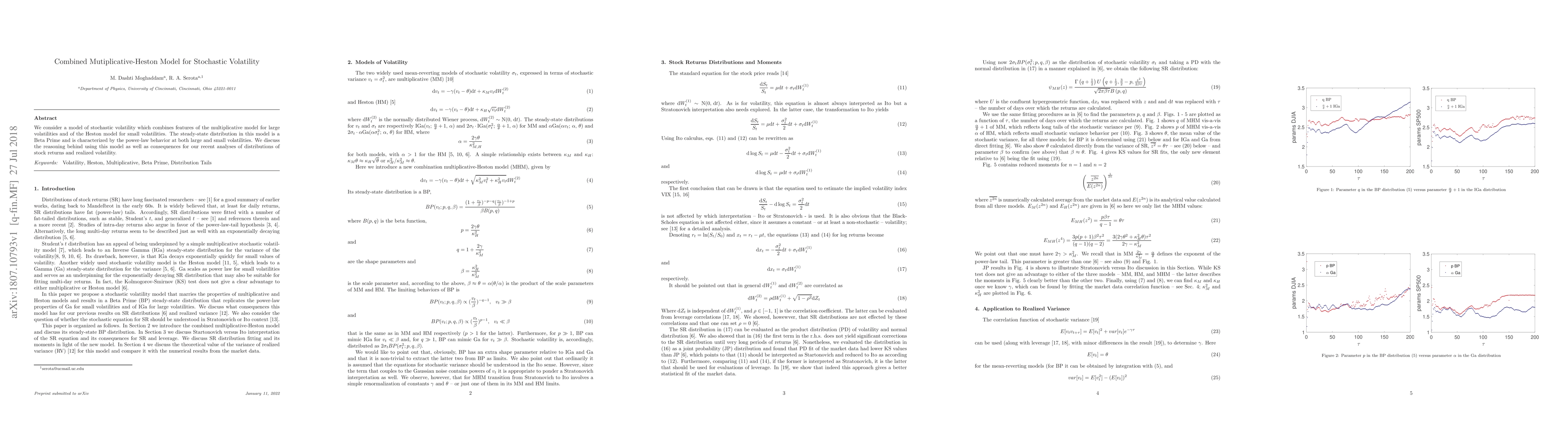

We consider a model of stochastic volatility which combines features of the multiplicative model for large volatilities and of the Heston model for small volatilities. The steady-state distribution ...

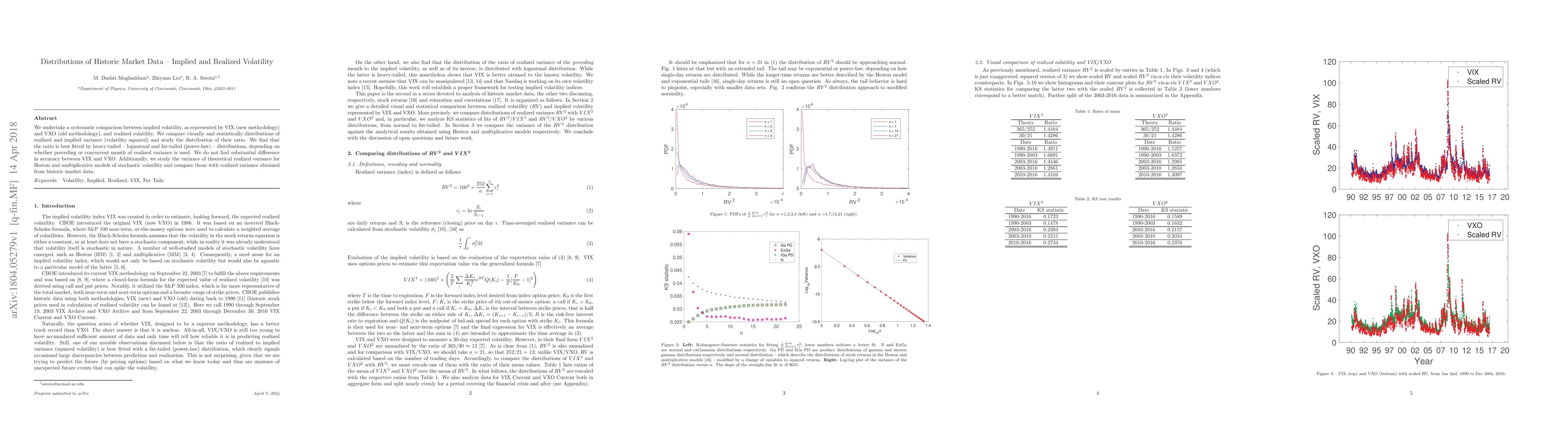

We undertake a systematic comparison between implied volatility, as represented by VIX (new methodology) and VXO (old methodology), and realized volatility. We compare visually and statistically dis...

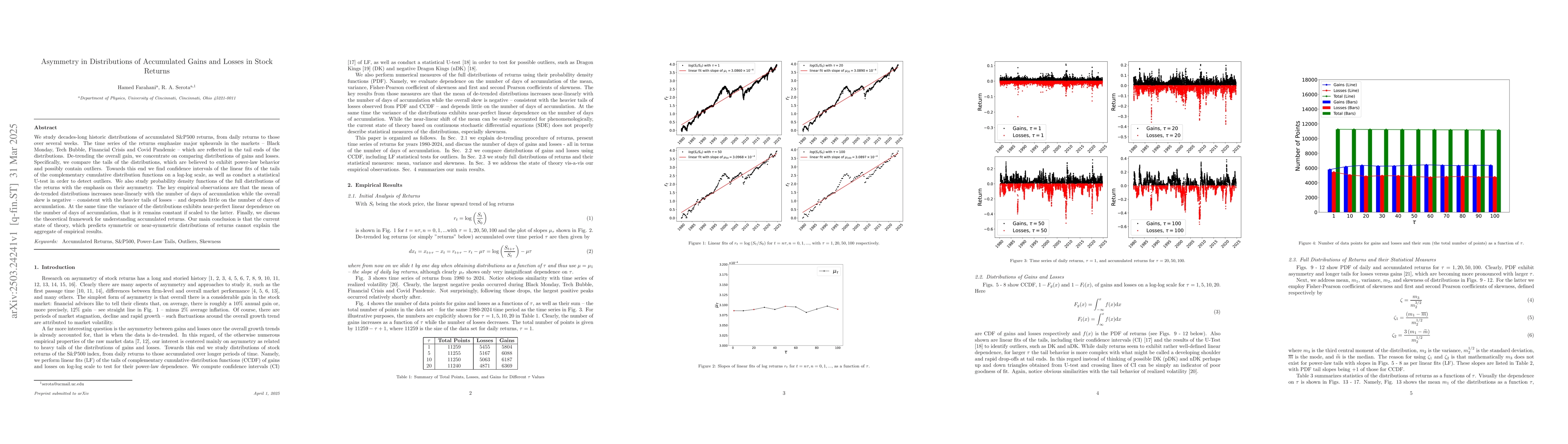

We study decades-long historic distributions of accumulated S\&P500 returns, from daily returns to those over several weeks. The time series of the returns emphasize major upheavals in the markets -- ...

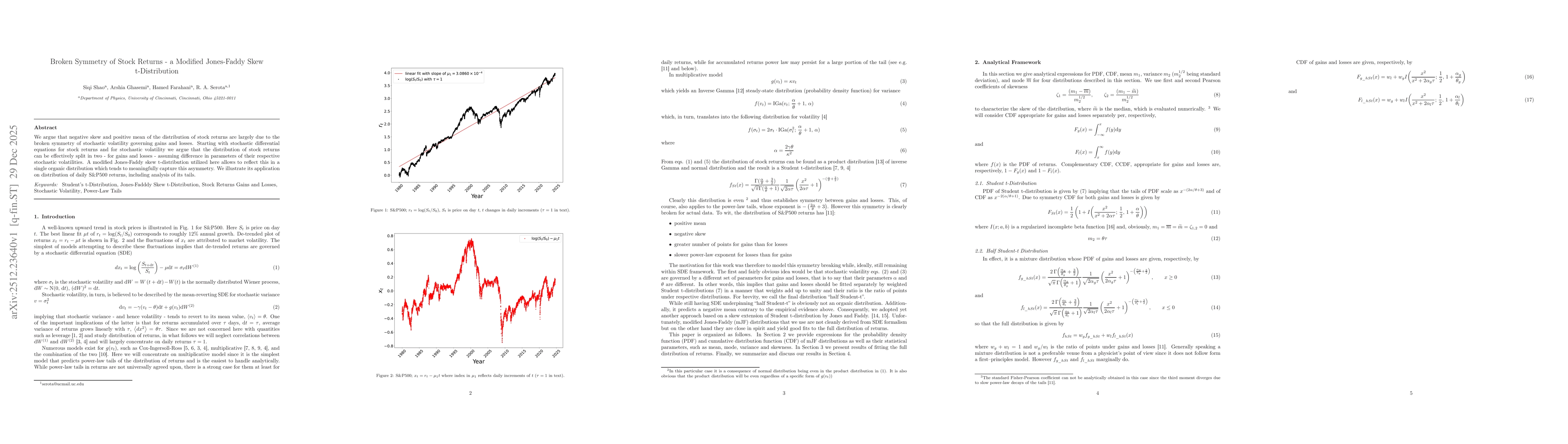

We argue that negative skew and positive mean of the distribution of stock returns are largely due to the broken symmetry of stochastic volatility governing gains and losses. Starting with stochastic ...

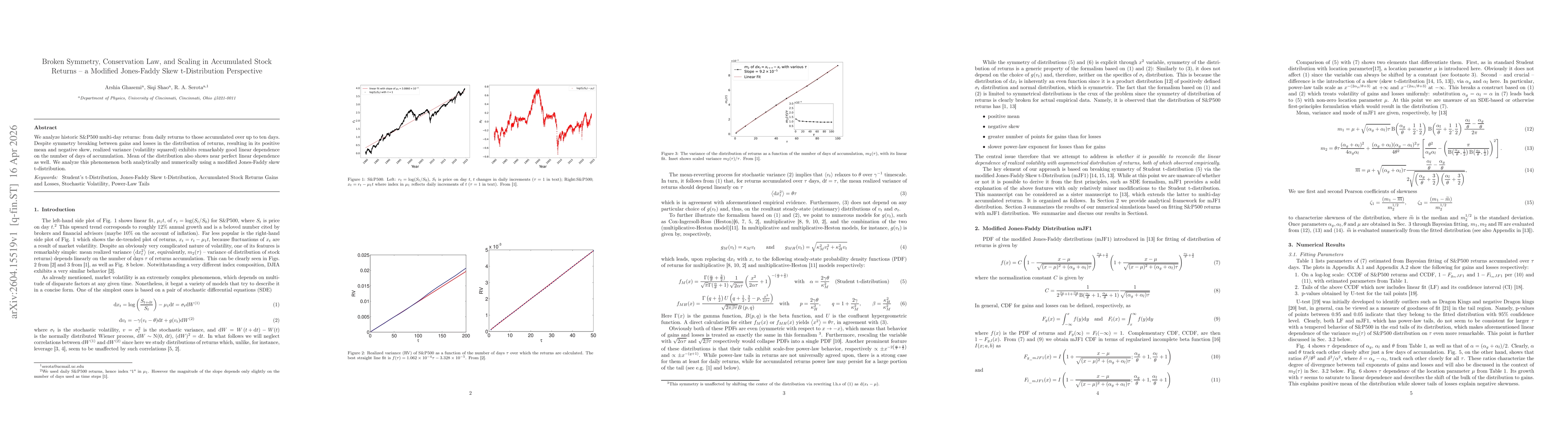

We analyze historic S&P500 multi-day returns: from daily returns to those accumulated over up to ten days. Despite symmetry breaking between gains and losses in the distribution of returns, resulting ...

We analyze distributions of historic S&P500 multi-day returns, for the number of days of accumulation from 20 to 120. With the increase of the number of days of accumulation, we observe clear temperin...