Academic Profile

Statistics

Similar Authors

Papers on arXiv

Effective utilization of time series data is often constrained by the scarcity of data quantity that reflects complex dynamics, especially under the condition of distributional shifts. Existing data...

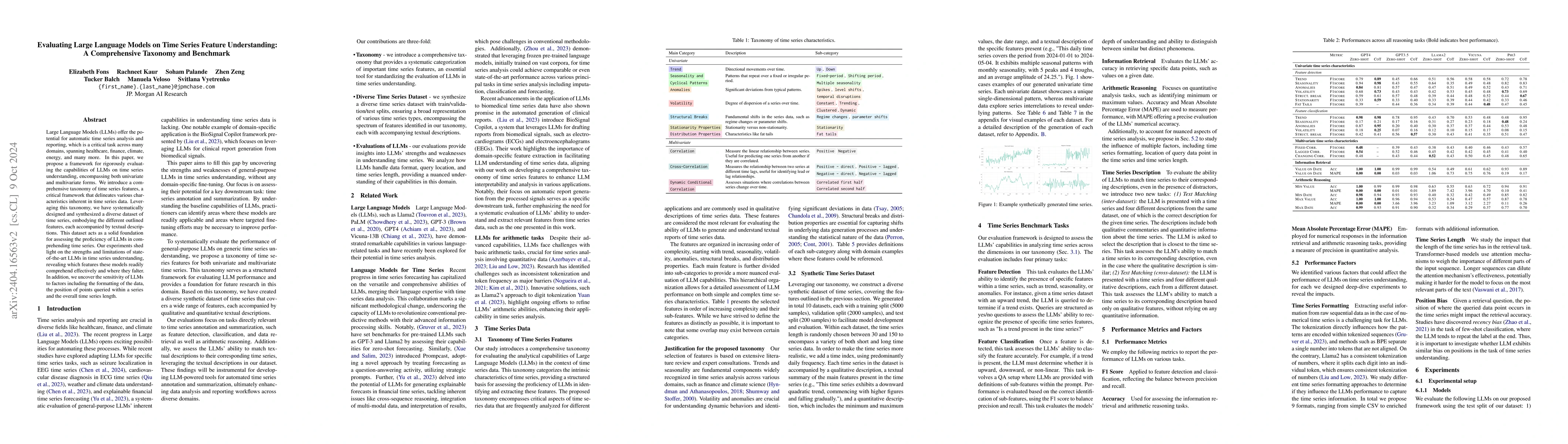

Large Language Models (LLMs) offer the potential for automatic time series analysis and reporting, which is a critical task across many domains, spanning healthcare, finance, climate, energy, and ma...

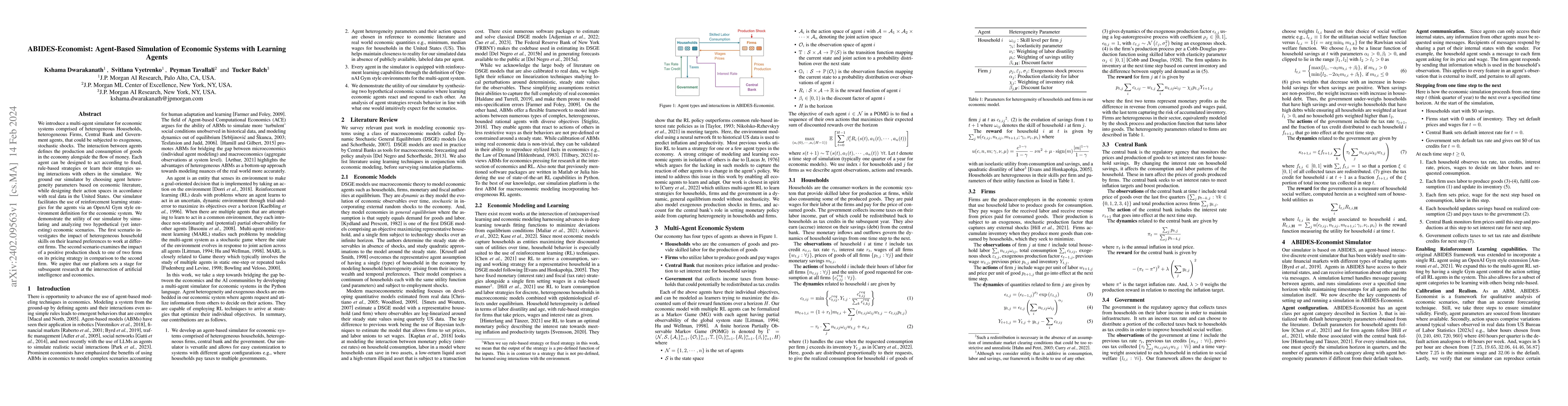

We introduce a multi-agent simulator for economic systems comprised of heterogeneous Households, heterogeneous Firms, Central Bank and Government agents, that could be subjected to exogenous, stocha...

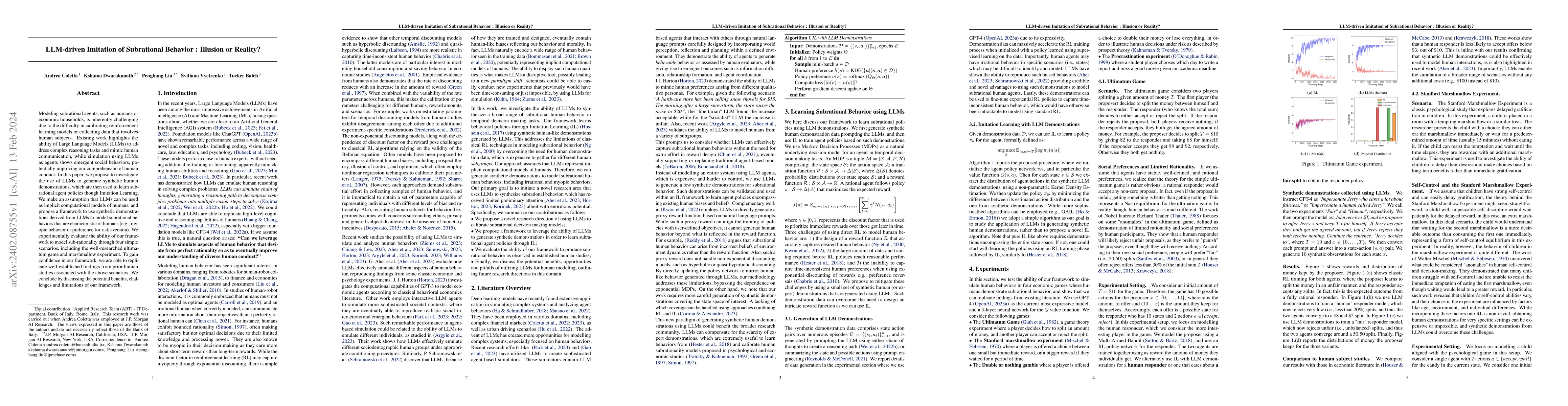

Modeling subrational agents, such as humans or economic households, is inherently challenging due to the difficulty in calibrating reinforcement learning models or collecting data that involves huma...

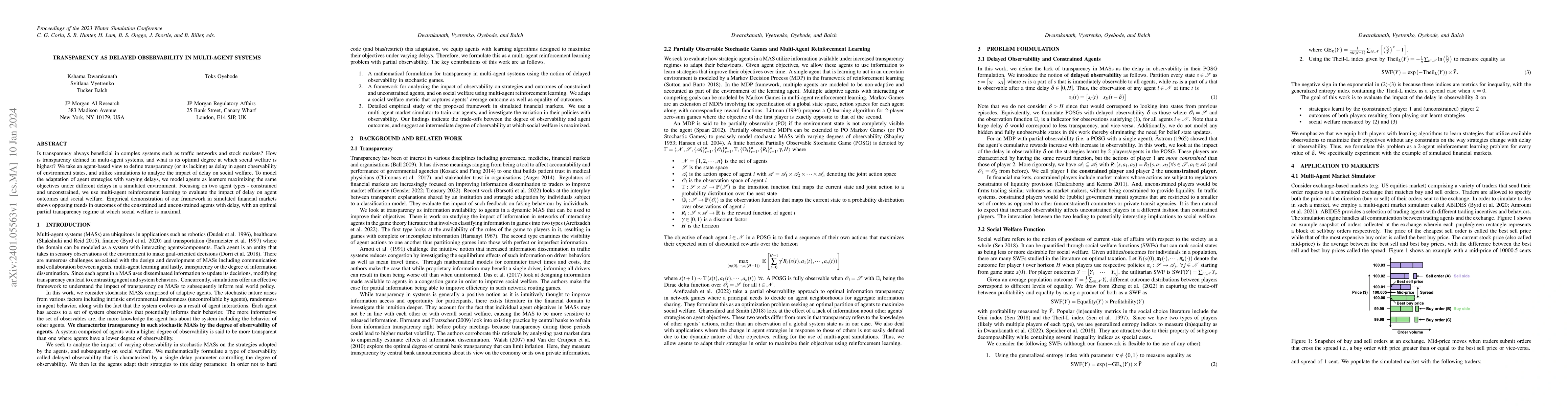

Is transparency always beneficial in complex systems such as traffic networks and stock markets? How is transparency defined in multi-agent systems, and what is its optimal degree at which social we...

Synthetic data has made tremendous strides in various commercial settings including finance, healthcare, and virtual reality. We present a broad overview of prototypical applications of synthetic da...

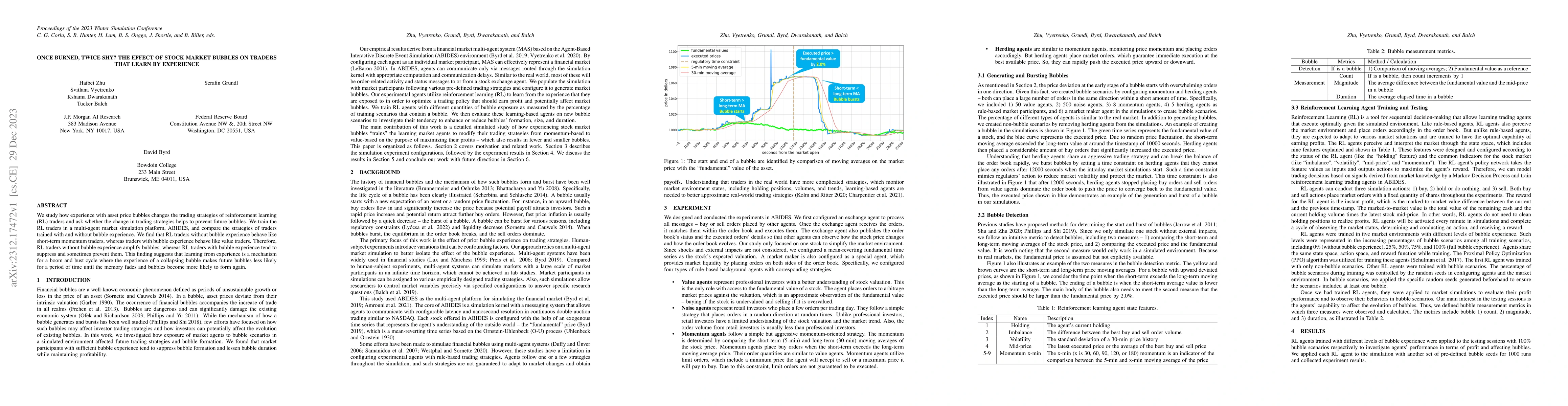

We study how experience with asset price bubbles changes the trading strategies of reinforcement learning (RL) traders and ask whether the change in trading strategies helps to prevent future bubble...

Stochastic differential equations (SDEs) have been widely used to model real world random phenomena. Existing works mainly focus on the case where the time series is modeled by a single SDE, which m...

Data augmentation techniques play an important role in enhancing the performance of deep learning models. Despite their proven benefits in computer vision tasks, their application in the other domai...

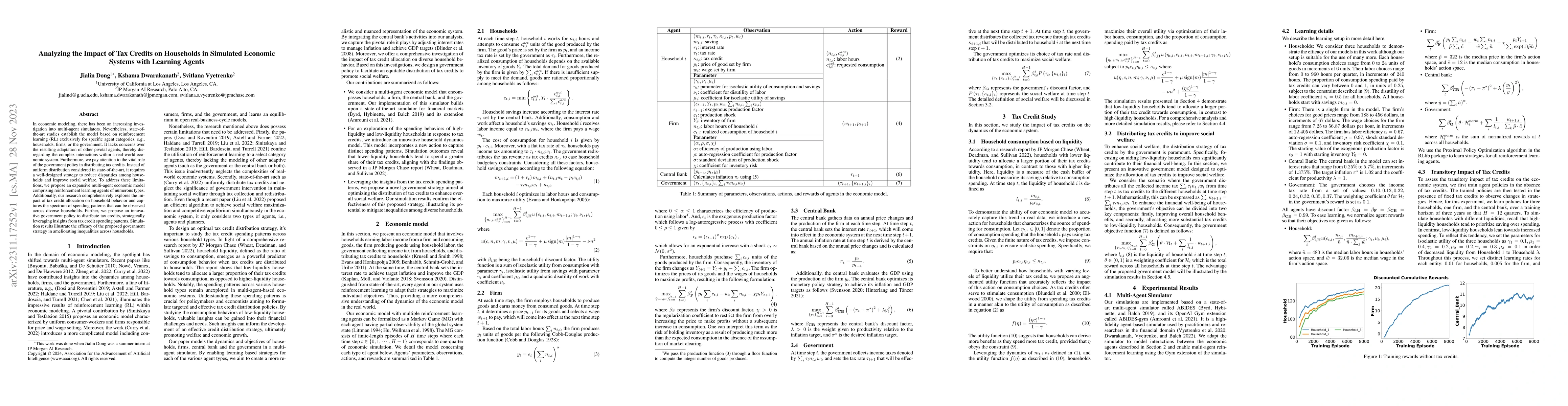

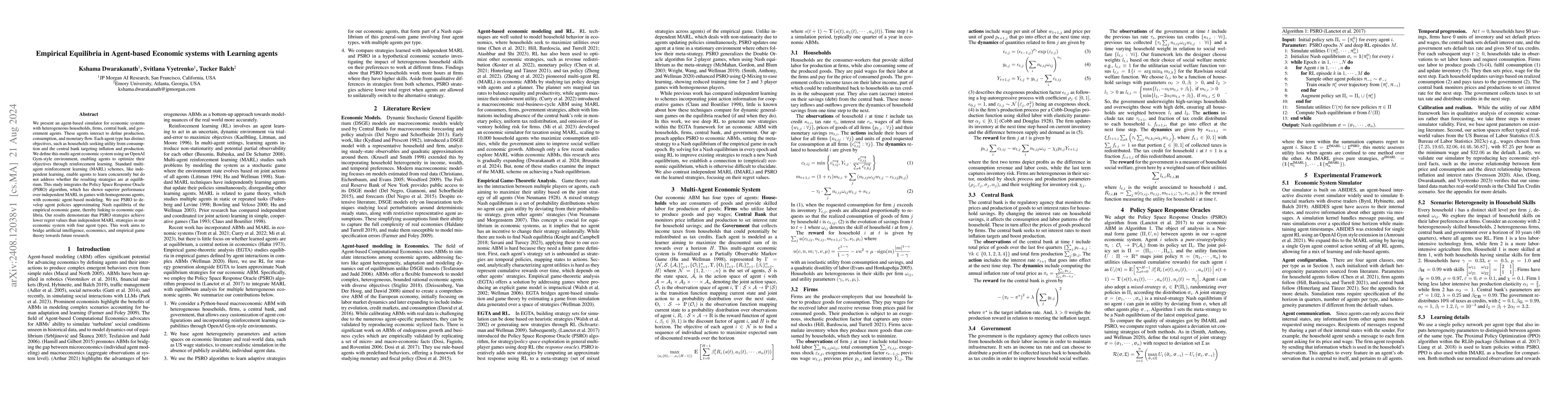

In economic modeling, there has been an increasing investigation into multi-agent simulators. Nevertheless, state-of-the-art studies establish the model based on reinforcement learning (RL) exclusiv...

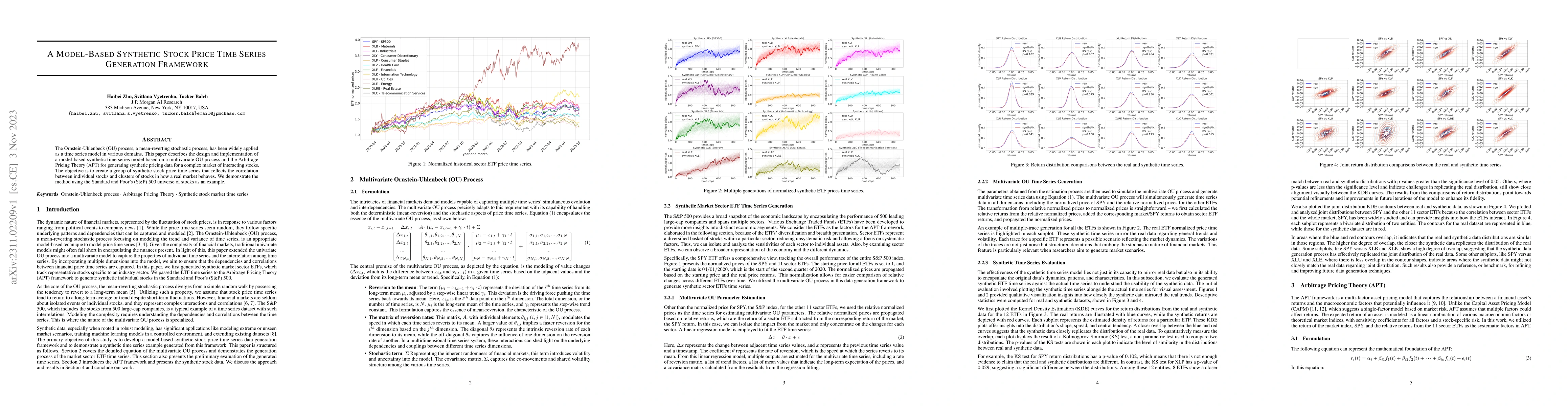

The Ornstein-Uhlenbeck (OU) process, a mean-reverting stochastic process, has been widely applied as a time series model in various domains. This paper describes the design and implementation of a m...

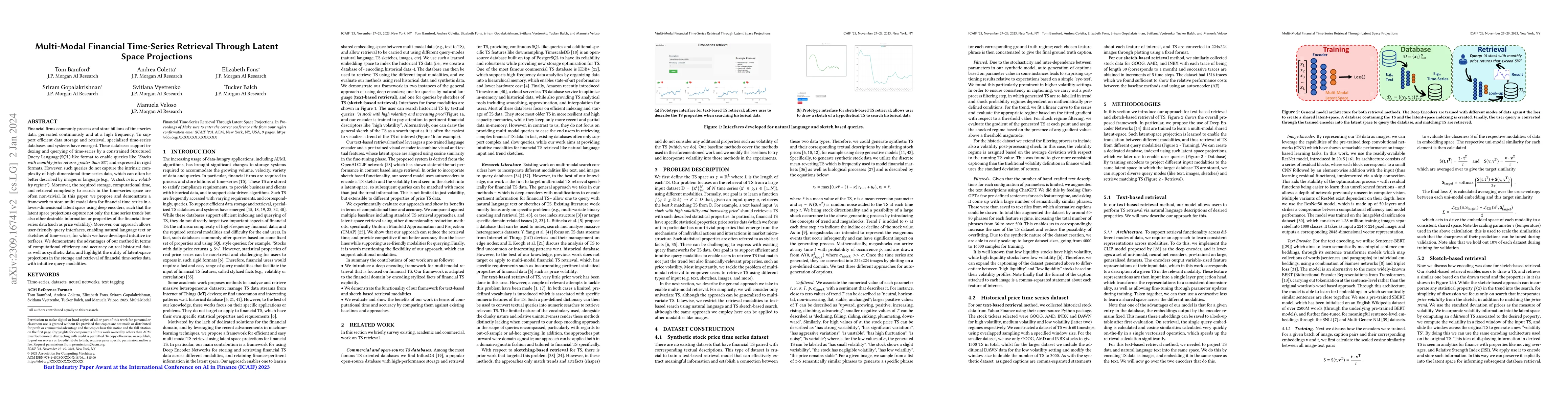

Financial firms commonly process and store billions of time-series data, generated continuously and at a high frequency. To support efficient data storage and retrieval, specialized time-series data...

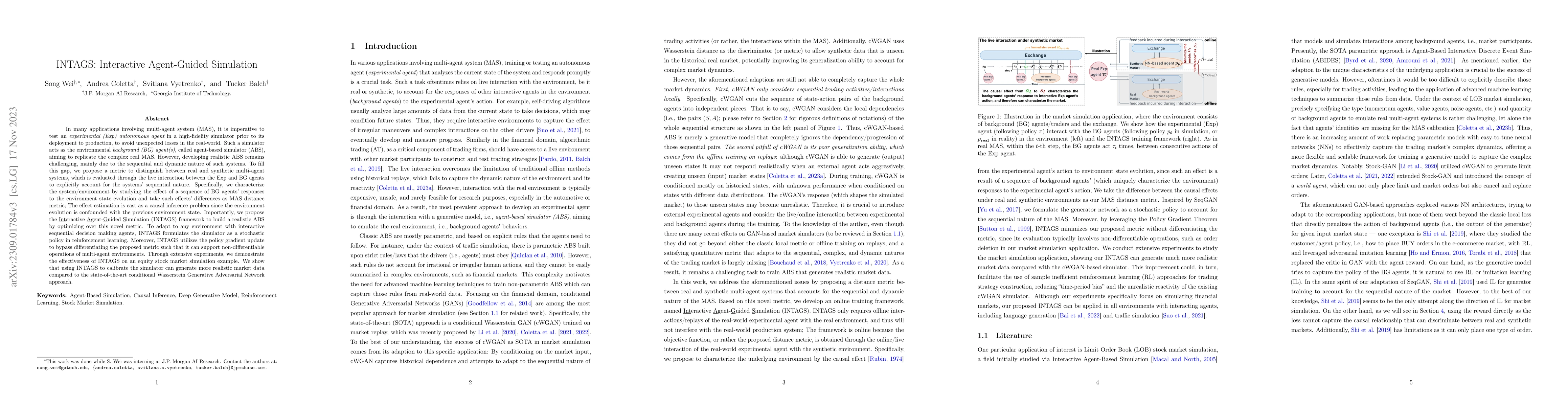

In many applications involving multi-agent system (MAS), it is imperative to test an experimental (Exp) autonomous agent in a high-fidelity simulator prior to its deployment to production, to avoid ...

The recent advancements in Deep Learning (DL) research have notably influenced the finance sector. We examine the robustness and generalizability of fifteen state-of-the-art DL models focusing on St...

Synthetic time series are often used in practical applications to augment the historical time series dataset for better performance of machine learning algorithms, amplify the occurrence of rare eve...

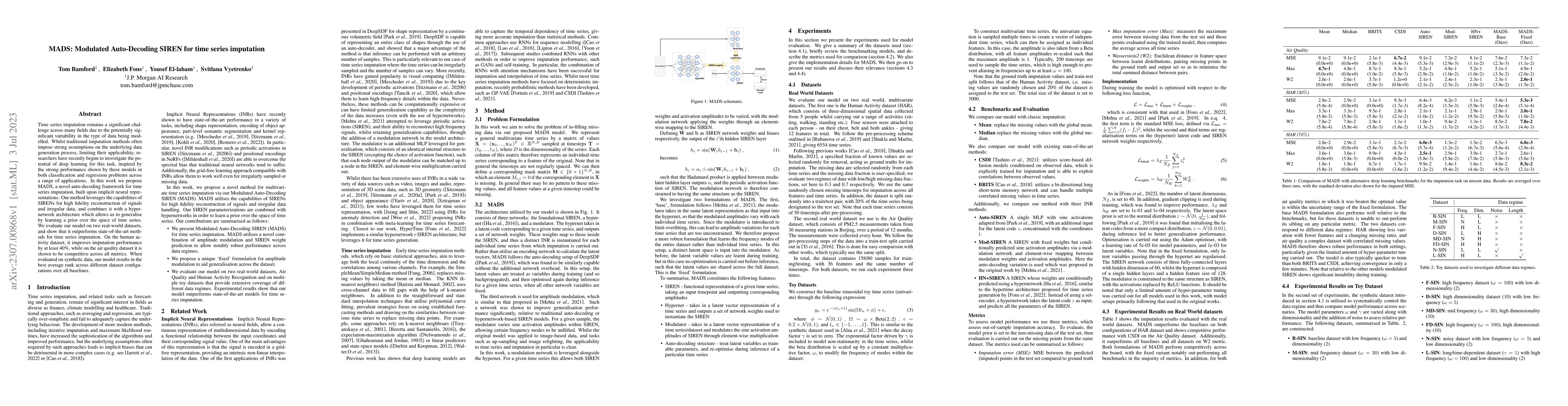

Time series imputation remains a significant challenge across many fields due to the potentially significant variability in the type of data being modelled. Whilst traditional imputation methods oft...

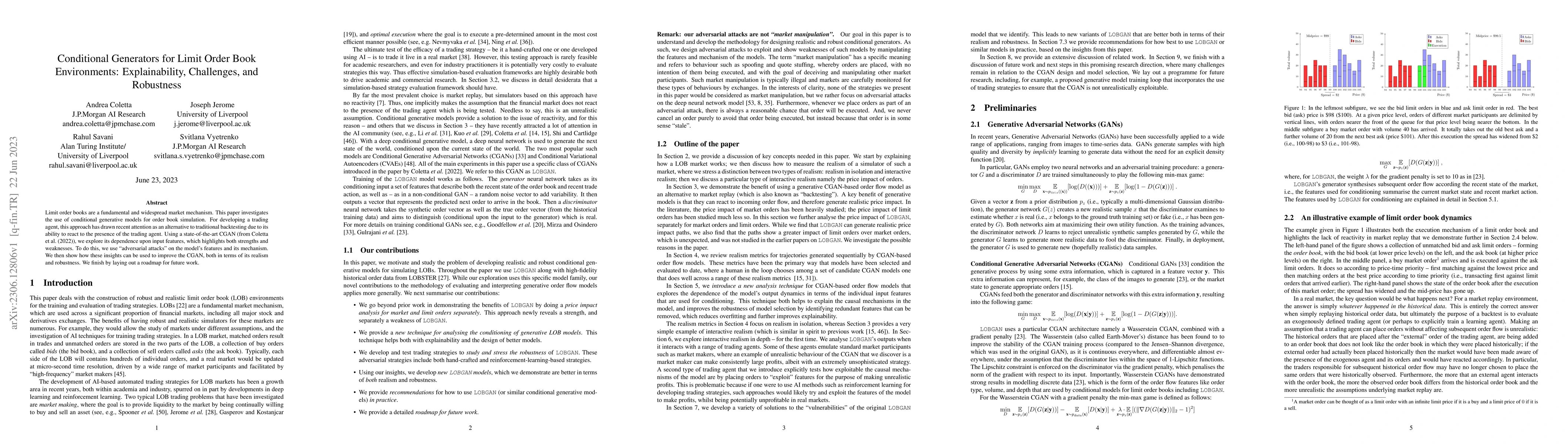

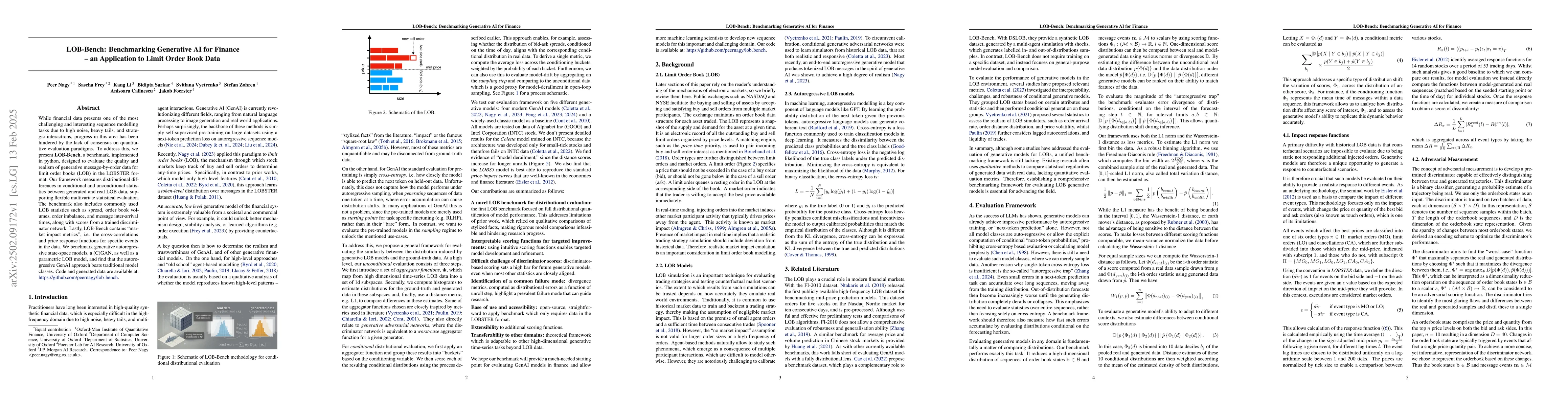

Limit order books are a fundamental and widespread market mechanism. This paper investigates the use of conditional generative models for order book simulation. For developing a trading agent, this ...

This work introduces a novel probabilistic deep learning technique called deep Gaussian mixture ensembles (DGMEs), which enables accurate quantification of both epistemic and aleatoric uncertainty. ...

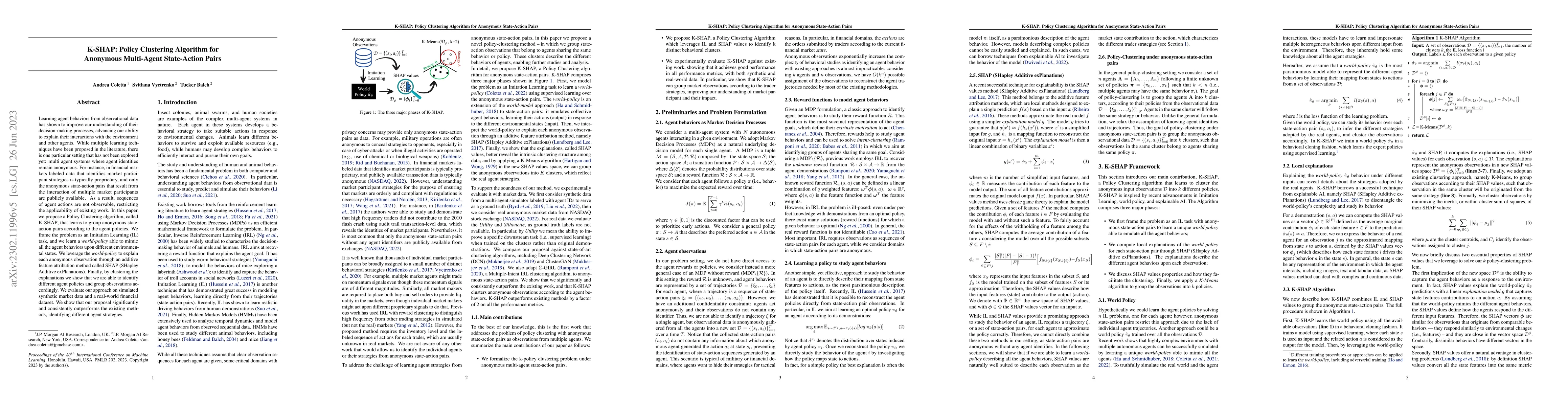

Learning agent behaviors from observational data has shown to improve our understanding of their decision-making processes, advancing our ability to explain their interactions with the environment a...

In electronic trading markets, limit order books (LOBs) provide information about pending buy/sell orders at various price levels for a given security. Recently, there has been a growing interest in...

Multi-agent market simulators usually require careful calibration to emulate real markets, which includes the number and the type of agents. Poorly calibrated simulators can lead to misleading concl...

Neural style transfer is a powerful computer vision technique that can incorporate the artistic "style" of one image to the "content" of another. The underlying theory behind the approach relies on ...

Implicit neural representations (INRs) have recently emerged as a powerful tool that provides an accurate and resolution-independent encoding of data. Their robustness as general approximators has b...

Multi-agent simulation is commonly used across multiple disciplines, specifically in artificial intelligence in recent years, which creates an environment for downstream machine learning or reinforc...

Model-free Reinforcement Learning (RL) requires the ability to sample trajectories by taking actions in the original problem environment or a simulated version of it. Breakthroughs in the field of R...

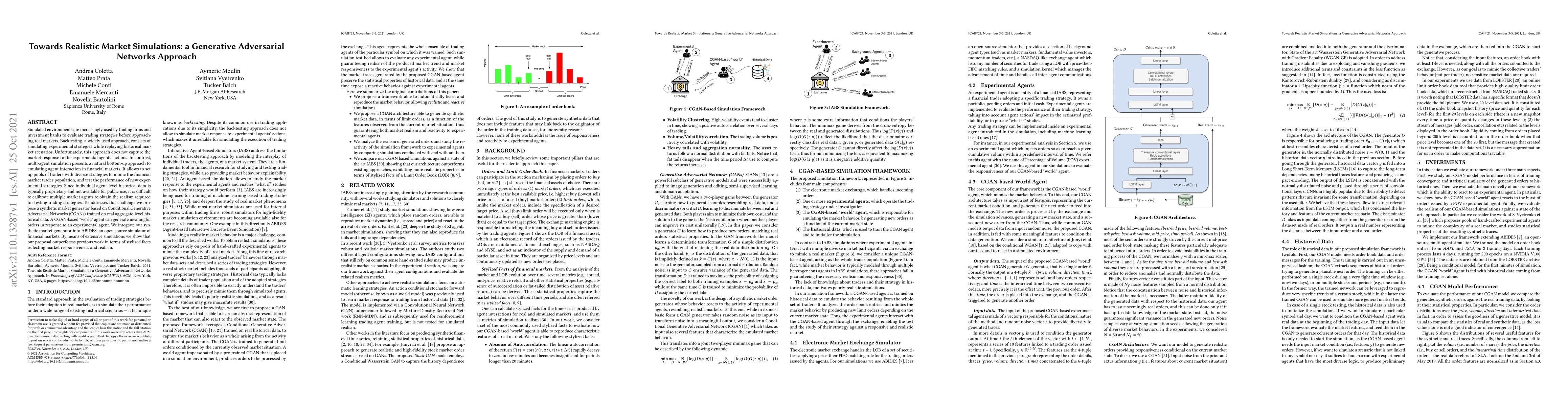

Simulated environments are increasingly used by trading firms and investment banks to evaluate trading strategies before approaching real markets. Backtesting, a widely used approach, consists of si...

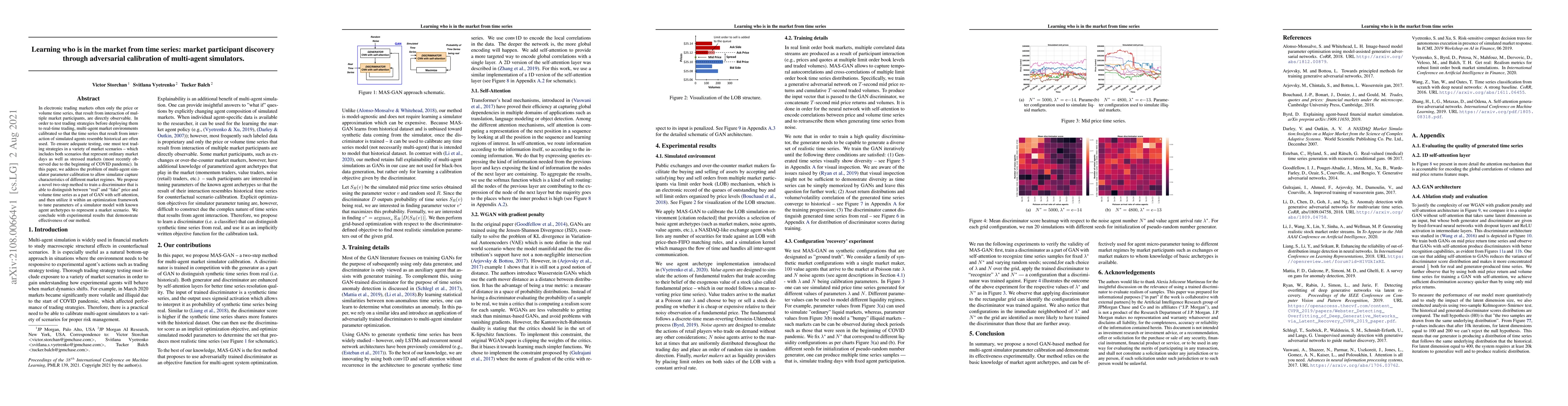

In electronic trading markets often only the price or volume time series, that result from interaction of multiple market participants, are directly observable. In order to test trading strategies b...

Stochastic simulation aims to compute output performance for complex models that lack analytical tractability. To ensure accurate prediction, the model needs to be calibrated and validated against r...

Machine learning (especially reinforcement learning) methods for trading are increasingly reliant on simulation for agent training and testing. Furthermore, simulation is important for validation of...

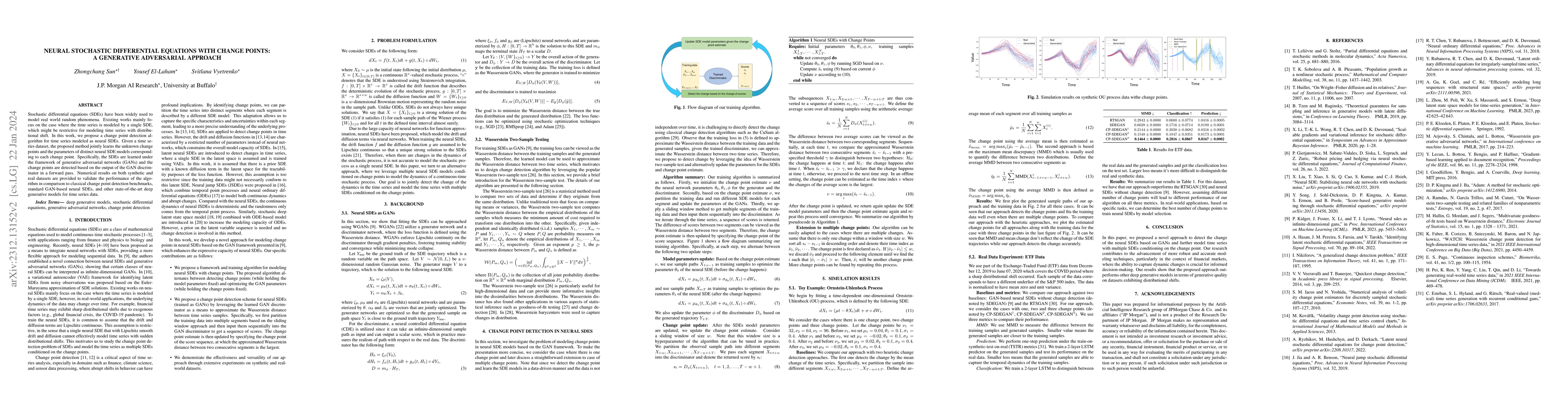

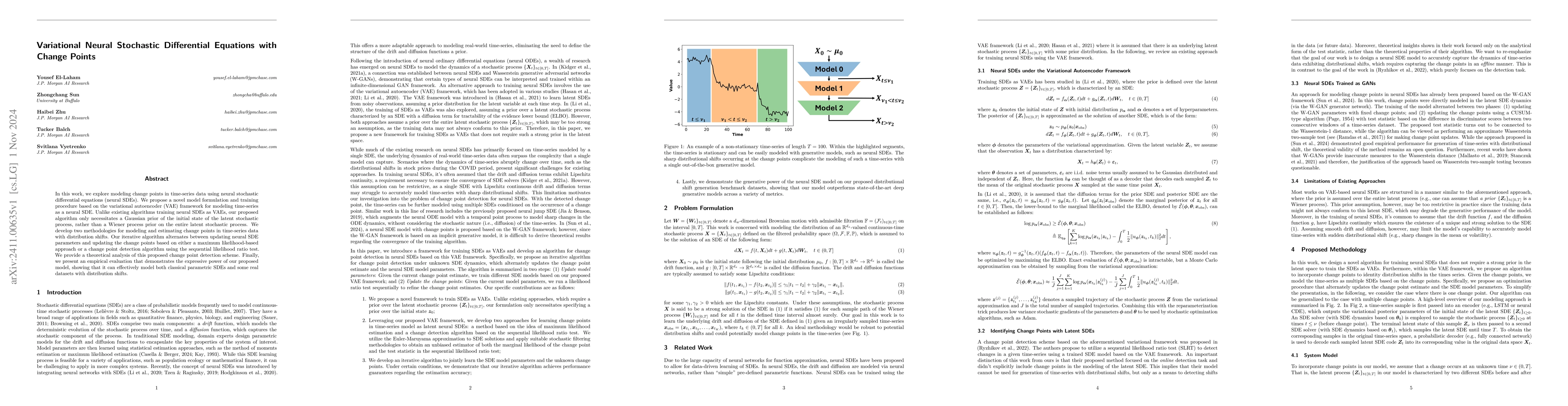

In this work, we explore modeling change points in time-series data using neural stochastic differential equations (neural SDEs). We propose a novel model formulation and training procedure based on t...

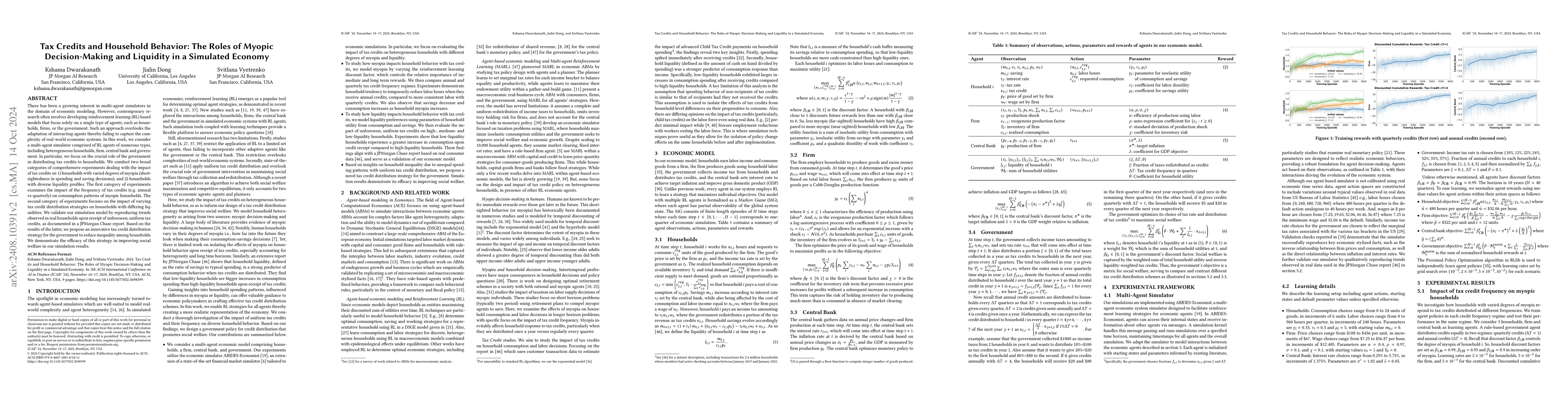

There has been a growing interest in multi-agent simulators in the domain of economic modeling. However, contemporary research often involves developing reinforcement learning (RL) based models that f...

We present an agent-based simulator for economic systems with heterogeneous households, firms, central bank, and government agents. These agents interact to define production, consumption, and monetar...

While financial data presents one of the most challenging and interesting sequence modelling tasks due to high noise, heavy tails, and strategic interactions, progress in this area has been hindered b...

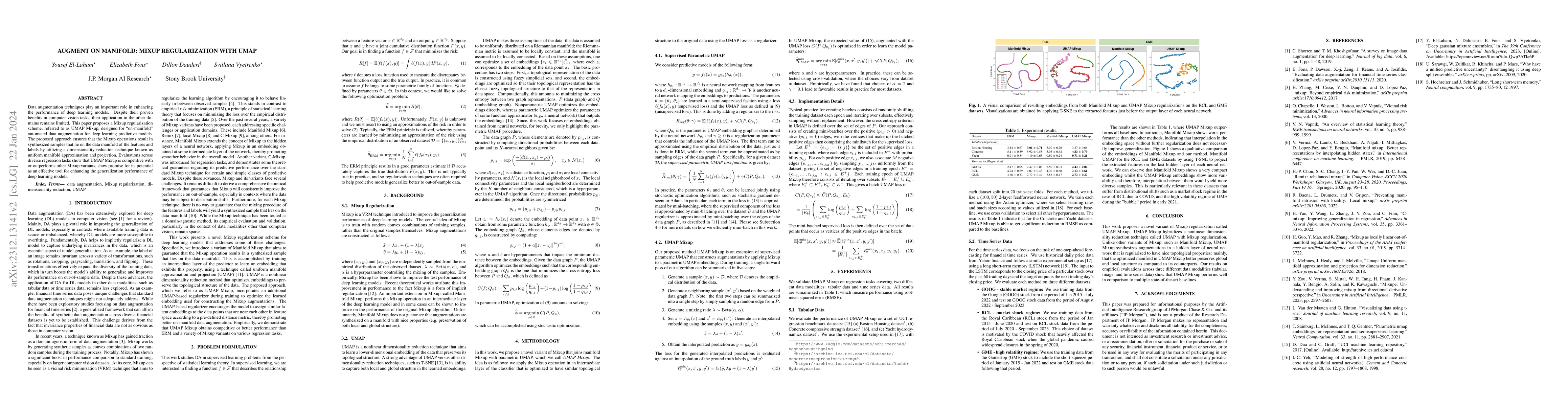

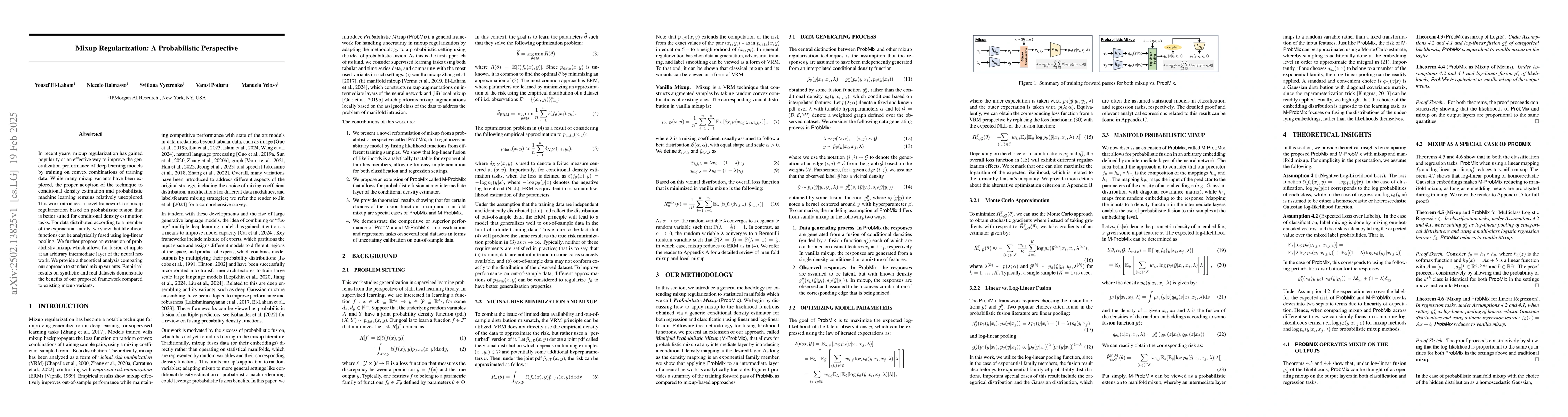

In recent years, mixup regularization has gained popularity as an effective way to improve the generalization performance of deep learning models by training on convex combinations of training data. W...

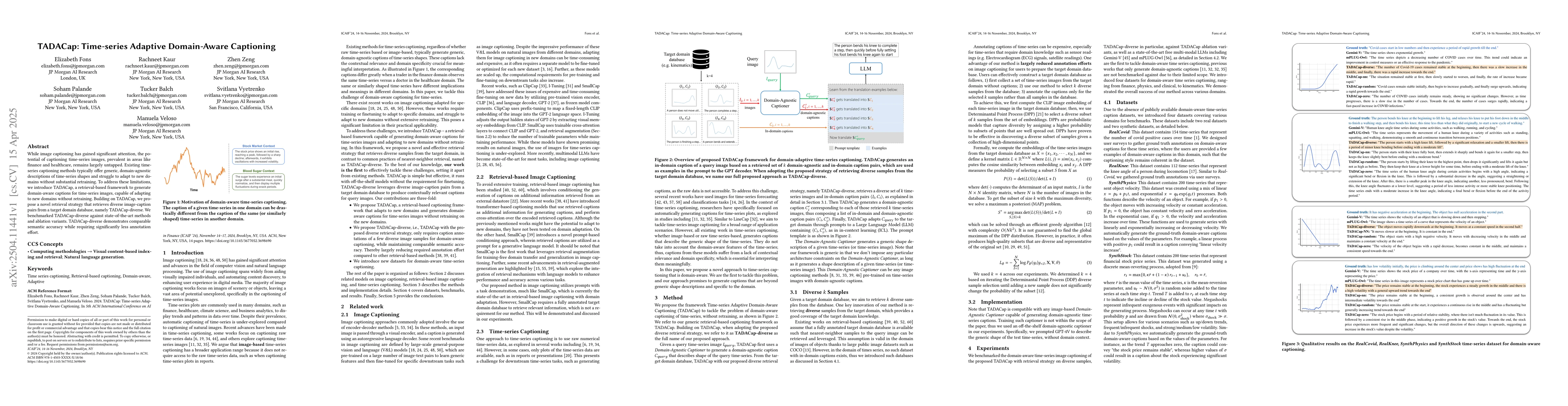

While image captioning has gained significant attention, the potential of captioning time-series images, prevalent in areas like finance and healthcare, remains largely untapped. Existing time-series ...

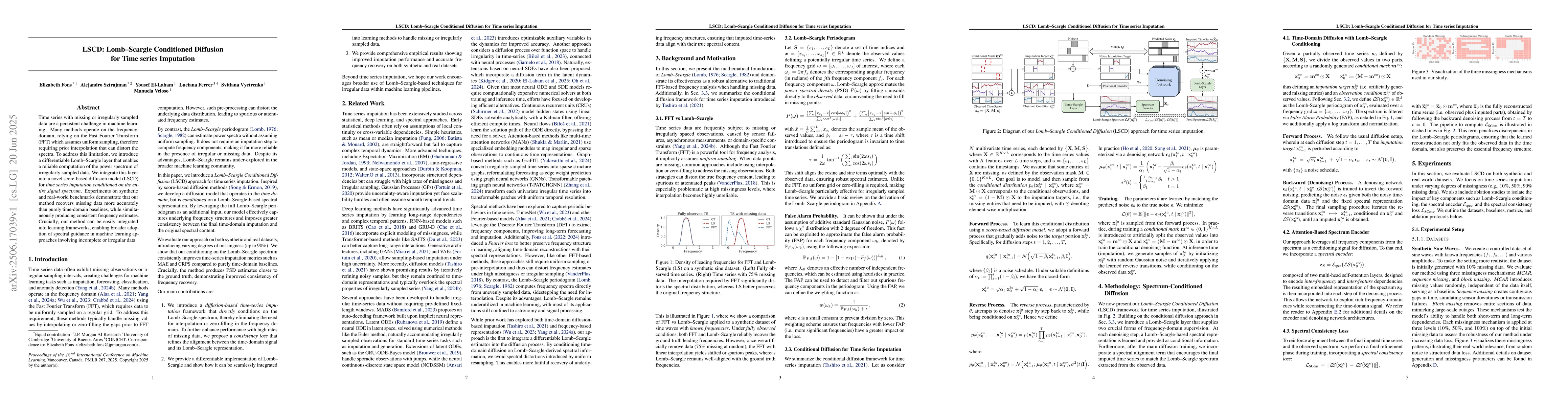

Time series with missing or irregularly sampled data are a persistent challenge in machine learning. Many methods operate on the frequency-domain, relying on the Fast Fourier Transform (FFT) which ass...

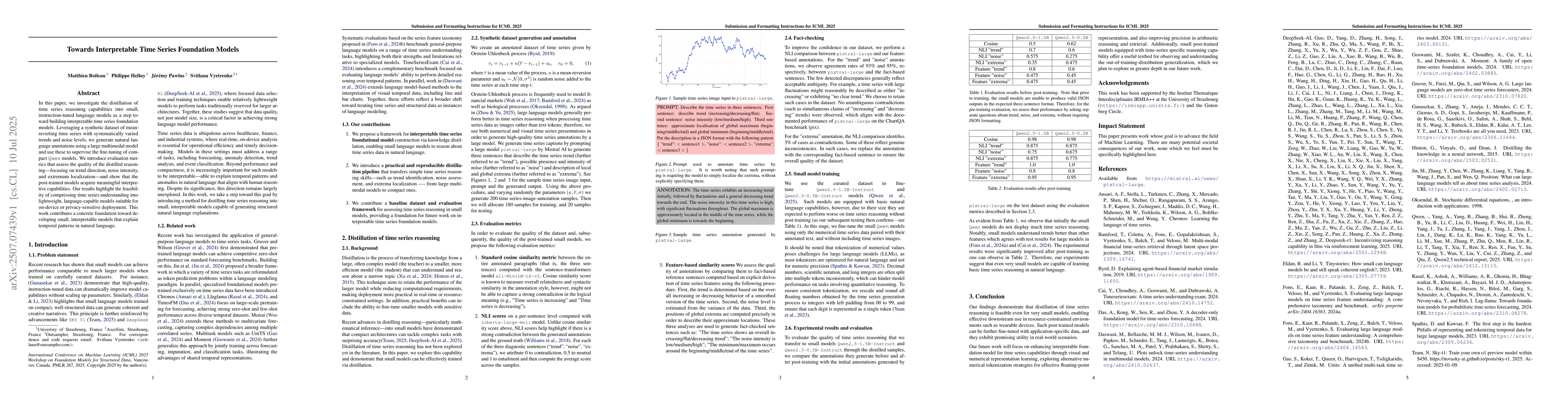

In this paper, we investigate the distillation of time series reasoning capabilities into small, instruction-tuned language models as a step toward building interpretable time series foundation models...

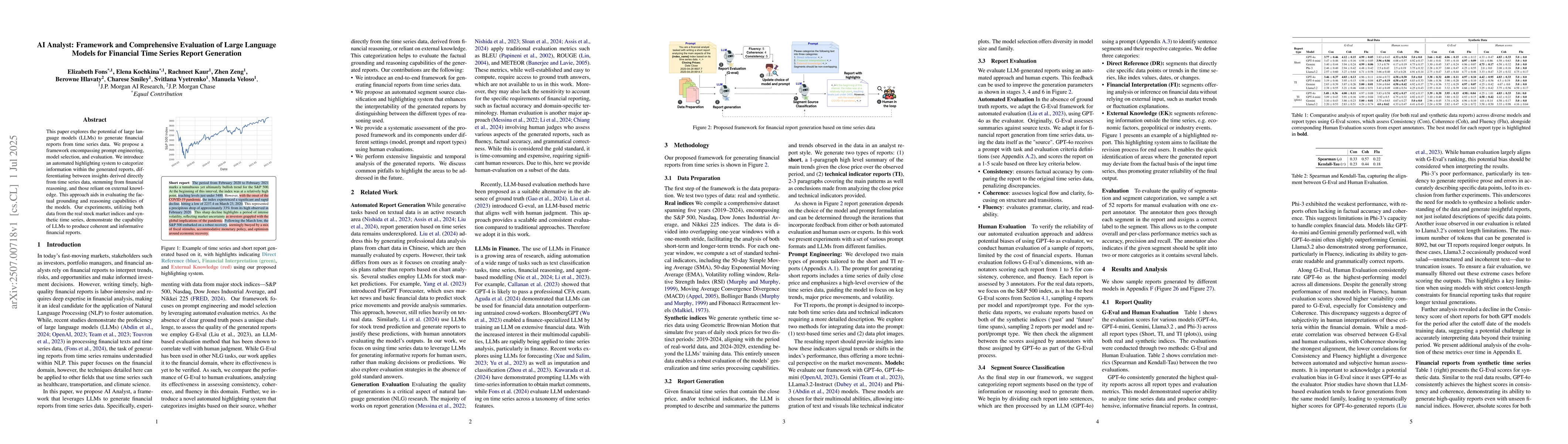

This paper explores the potential of large language models (LLMs) to generate financial reports from time series data. We propose a framework encompassing prompt engineering, model selection, and eval...

Time series anomaly detection is critical across various domains, yet current approaches often limit analysis to mere binary anomaly classification without detailed categorization or further explanato...

Large language models (LLMs) have shown strong abilities in reasoning and problem solving, but recent studies reveal that they still struggle with time series reasoning tasks, where outputs are often ...